By Elias Maren, Senior Policy Analyst

Over US$50 billion in cumulative GDP impact is not a conventional starting point for a discussion about an African infrastructure financier. Yet that figure is precisely why the africa finance corporation deserves closer attention from G7 and G20 delegates. As of August 2025, AFC-backed projects had also supported 7 million jobs, mobilised US$14 billion in capital, and connected 4.1 million homes to electricity across 36 African countries, according to AFC's August 2025 impact release.

Those numbers matter for more than institutional branding. They suggest that AFC has become one of the clearest tests of whether an African-led, commercially disciplined, development-oriented institution can turn infrastructure finance into measurable economic transformation. For G20 governments facing tighter fiscal space, contested industrial policy, and pressure to mobilise private capital rather than rely solely on public balance sheets, AFC is more than a regional case. It is a governance model with implications for how multilateral finance may evolve.

The strategic question isn't whether AFC has scale. It does. The more important question is how its structure, financing methods, and risk profile should shape partnership choices by G7 and G20 actors seeking bankable, climate-relevant, and politically durable infrastructure platforms in Africa.

Table of Contents

- The AFC Mission and Mandate for African Infrastructure

- Understanding AFC Governance and Membership

- The Blended Finance Engine De-risking Investment

- Flagship Projects and Sectoral Portfolios

- Driving Climate Action and Regional Integration

- Policy Implications and Risks for G7/G20 Stakeholders

- Pathways for Partnership and Strategic Engagement

The AFC Mission and Mandate for African Infrastructure

AFC was created to solve a specific market failure: too many African infrastructure projects reach technical viability but fail to reach financial close. Its mandate is narrower, and more operational, than that of a traditional development lender. Since its establishment in 2007, the institution has focused on building, financing, and scaling assets in power, transport, logistics, telecommunications, natural resources, and industry where weak preparation capacity, political risk, and long payback periods often deter private capital.

An African institution with a practical mandate

That design choice matters for policy. AFC was set up to originate and execute infrastructure transactions in sectors that shape productivity, export capacity, and energy security. In other words, its mandate sits closer to economic transformation than to social spending. For G20 delegates, this is the relevant distinction. Institutions of this type can influence whether industrial policy is financeable, whether regional trade corridors become bankable projects, and whether energy transition targets are matched by investable pipelines.

The strategic value lies in how AFC defines the problem. The binding constraint in much of African infrastructure is not only the absence of capital. It is the shortage of institutions willing to structure complex projects early, absorb selected risks, and remain involved long enough to crowd in other investors. That is why AFC matters beyond its own balance sheet.

AFC's own institutional materials describe a model centered on scalable infrastructure and productive sectors rather than broad sovereign lending or grant-based intervention. This places it in a growing group of African financial institutions that are shaping project pipelines from within the continent's policy and capital markets environment, alongside initiatives such as the African Investment Forum's role in African financial governance.

Why the mandate matters for global governance

For G7 and G20 stakeholders, AFC's mandate raises a practical question: which institutions can convert political commitments on infrastructure, climate, and trade into transactions that private investors will fund? AFC offers one answer. Its sector focus aligns with issues already high on the G20 agenda, including energy access, supply-chain resilience, regional integration, and industrial development.

That creates a partnership opportunity, but also a policy test. If external partners treat AFC only as a co-financier, they underuse the institution. Its larger value is upstream. It can help identify commercially plausible projects, shape transaction structures around local constraints, and connect development objectives to revenue models that institutional investors can assess.

This has implications for global governance. African infrastructure finance is no longer defined only by bilateral creditors, export credit agencies, or large multilateral banks. Regionally anchored institutions increasingly influence which projects proceed, which risks are priced in, and which sectors attract long-term capital.

The deeper policy insight

The central point is agency. AFC represents an African capacity to set terms in infrastructure finance, not a vehicle for receiving external funding. That changes the logic of engagement for advanced economies and multilateral partners.

A more effective approach would combine capital partnership with policy coordination, technical cooperation, and pipeline development. It would also require realism about risk. A mandate concentrated in infrastructure and productive sectors can generate high development returns, but it also exposes the institution to commodity cycles, construction delays, regulatory uncertainty, and political interference. For G20 policymakers, the policy challenge is therefore twofold: use AFC's execution model to expand bankable infrastructure, while strengthening the safeguards, transparency standards, and co-investment frameworks that keep that model credible at scale.

Understanding AFC Governance and Membership

AFC's institutional design matters because governance determines how quickly capital can be deployed, how risk is priced, and whose priorities shape project selection. For G20 policymakers, the relevant question is not only whether AFC can fund infrastructure, but whether its governance model makes it a credible partner for scaling investment while maintaining accountability.

AFC combines public anchoring with a shareholder structure that imposes commercial discipline. As noted earlier, the corporation's ownership has included a significant private-sector majority alongside a major holding by the Central Bank of Nigeria. That balance helps explain AFC's operating profile. Commercial shareholders tend to press for execution, returns, and balance-sheet prudence. A public anchor helps keep the institution aligned with development objectives and policy credibility across member states.

The result is a hybrid model with strategic implications. AFC can often act faster than larger multilateral lenders because its governance is closer to a development finance institution built for transactions than to a treaty-based bank built around extensive sovereign process. Yet that same agility creates a policy requirement for strong disclosure, clear board oversight, and disciplined risk management. Speed improves development outcomes only when investment standards remain consistent.

Institutional scale reinforces that point. Publicly available summaries indicate that AFC was established in 2007 with substantial authorised capital and has since built a balance sheet large enough to influence infrastructure financing decisions across multiple sectors and jurisdictions, as summarised in the Africa Finance Corporation entry. For external partners, scale at this level has two consequences. It is large enough to matter in project preparation and capital mobilisation. It is still concentrated enough that governance choices can materially affect portfolio quality and market confidence.

Membership growth as a governance signal

Membership expansion should be read as a political and institutional signal, not a clerical one. A wider member base suggests that more African governments view AFC as a legitimate channel for infrastructure finance and economic transformation. That strengthens its claim to represent continental priorities in discussions with external capital providers, export credit agencies, and multilateral partners.

It also raises the bar.

As membership broadens, AFC faces greater pressure to show that project selection, country exposure, environmental and social standards, and reporting practices are applied consistently across jurisdictions. For G7 and G20 stakeholders, this is the practical test of partnership quality. A larger membership base can improve pipeline access and policy reach, but it can also generate competing national expectations that strain governance unless rules and disclosure keep pace.

This broader institutional context is also visible in analysis of the African Investment Forum and African financial governance, where regionally anchored platforms are increasingly shaping how African priorities are presented to global investors.

Why credit ratings matter for public policy

Credit ratings are more than market labels. They influence funding costs, tenor, market access, and an institution's ability to maintain lending through periods of global financial stress. Publicly reported rating actions indicate that AFC has achieved investment-grade recognition from major agencies, which strengthens its standing with international investors and co-financiers.

For policymakers, the deeper implication is strategic. An African institution with credible market access can reduce dependence on more volatile or politically constrained financing channels. But ratings discipline also imposes limits. It encourages portfolio quality, liquidity management, and capital preservation, which can constrain appetite for projects with weaker revenue models or higher political risk. That tension matters for G20 engagement. Partners seeking to work with AFC need to structure collaboration in ways that preserve its credit strength rather than loading policy ambitions onto its balance sheet without appropriate risk-sharing.

The policy takeaway is straightforward. AFC's governance and membership trajectory suggest an institution moving toward greater continental legitimacy and greater global relevance. That creates a practical opening for G7 and G20 actors. They can use AFC as a partner for co-financing, pipeline formation, and standards coordination, but only if cooperation is designed around transparent governance, clear risk allocation, and respect for AFC's role as an African institution with its own strategic agency.

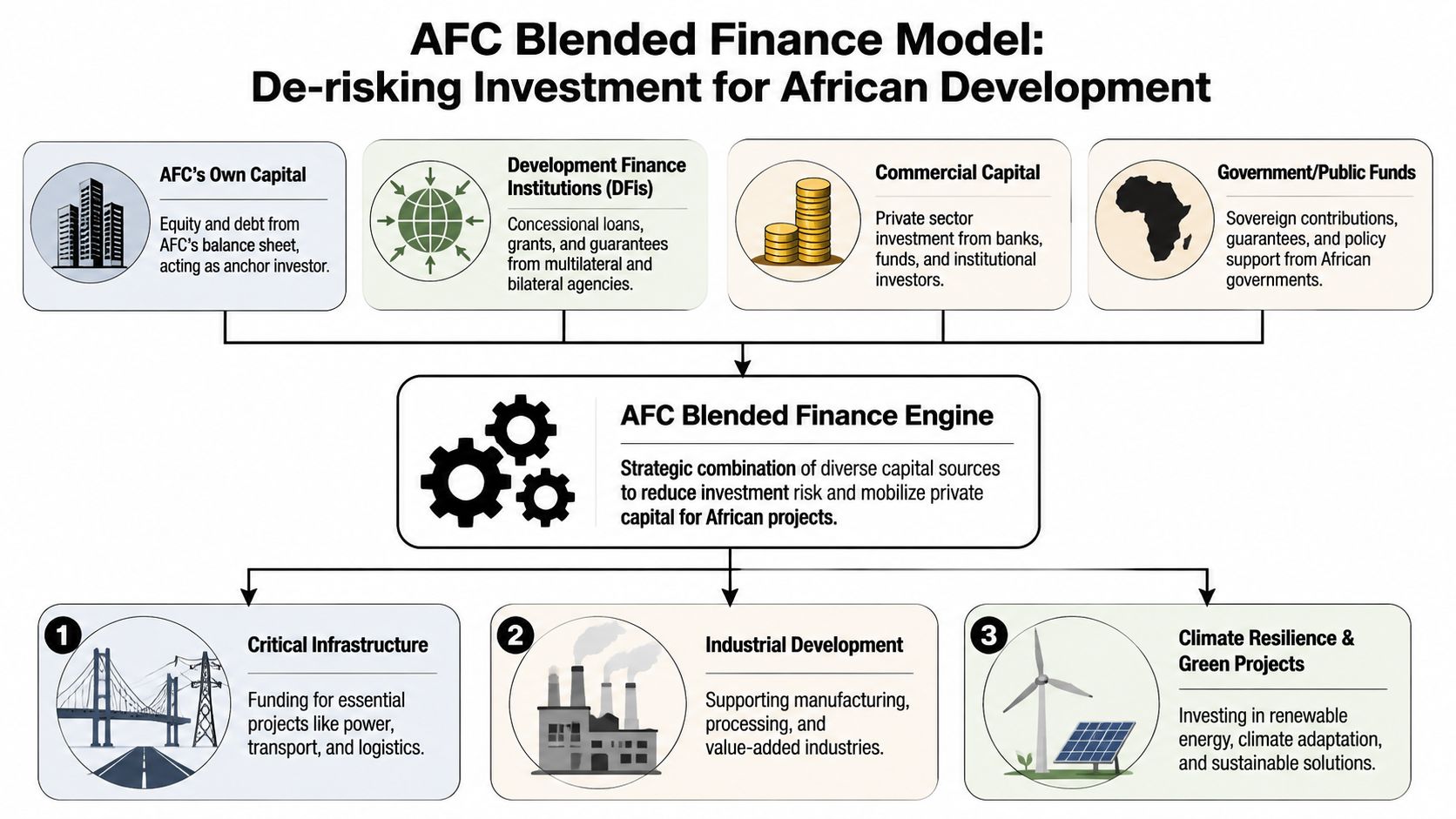

The Blended Finance Engine De-risking Investment

US$19 billion in direct disbursements and US$14 billion in mobilised capital indicate that AFC operates as more than a conventional project financier. Its model is built to change the risk profile of infrastructure transactions so that commercial lenders, institutional investors, and development partners can participate at scale, as documented in AFC's investment footprint reporting.

How AFC turns difficult projects into financeable ones

The central policy question is not whether capital exists. It is whether projects can be structured to meet the risk, return, and tenor requirements of different investor classes. AFC addresses that gap by combining project development, equity, debt, and advisory support in a single platform. That allows it to enter earlier than many commercial financiers and stay involved long enough to improve bankability, allocate risk more clearly, and prepare assets for refinancing or syndication.

For G20 policymakers, that operating model matters because it addresses a recurring failure in infrastructure finance. Public actors often focus on the volume of available funds, while investors focus on construction risk, revenue uncertainty, contract enforcement, currency mismatch, and exit options. AFC's role sits between those positions. It helps convert policy intent into structures the market can price. The broader debate on mobilising investments for sustainable infrastructure amid global crises turns on precisely this intermediary function.

Why the financing mechanism matters to G20 agendas

Three elements of AFC's approach merit attention.

Early-stage risk allocation

AFC can commit capital and structuring capacity before a project reaches the point where mainstream lenders are prepared to enter. That can reduce uncertainty around due diligence, counterparties, and transaction design.Capital mobilisation as a performance test

The institution's effectiveness should be judged not only by what it lends from its own balance sheet, but by whether its participation draws in other sources of finance. On that measure, AFC's mobilisation record is a material part of its development case.Transmission of lower funding costs

Lower-cost funding can improve project viability, particularly in sectors with long payback periods such as power, transport, and industrial infrastructure. The policy issue, however, is whether those benefits are passed through to end users and host economies, or absorbed by weak contractual design and sovereign-related risks.

This creates a more demanding view of blended finance than the term usually receives in international forums. A blended structure works only if concessional, catalytic, and commercial capital are assigned to risks they are suited to bear. If public capital is used to subsidise projects that remain poorly prepared, the result is not market creation. It is deferred failure.

The policy lesson on crowding in

For G7 and G20 stakeholders, the practical implication is clear. Partnership with AFC is likely to be most effective where external actors contribute first-loss capital, guarantees, local currency solutions, or project preparation support that complements AFC's balance sheet rather than duplicating it. That approach can expand the pool of investable transactions without weakening AFC's financial discipline.

There is also a risk that deserves more attention. Successful de-risking institutions can become vehicles for shifting excessive political or policy objectives onto a relatively disciplined intermediary. If shareholders and partners expect AFC to absorb risks that should sit with governments, donors, or guarantee providers, they may dilute the very features that make it useful to markets.

The strategic conclusion for G20 delegates is straightforward. Africa's infrastructure financing gap is not only a problem of capital supply. It is a problem of institutions that can convert fragmented risk appetite into investable structures. AFC shows one route to doing that. The next policy task is to decide how international partners can reinforce that function without crowding out private discipline or socialising losses that should remain explicit.

Flagship Projects and Sectoral Portfolios

AFC operates across five infrastructure-linked sectors. That matters for G20 policymakers because the development impact of African infrastructure depends less on any single asset than on whether power, transport, digital networks, industrial capacity, and resource processing are financed in the right sequence.

AFC Flagship Project Portfolio Highlights

| Sector | Illustrative portfolio role | Why it matters for policy and partnerships |

|---|---|---|

| Power | Generation, transmission, and related energy infrastructure that expands available electricity and supports industrial users | Power finance has the highest system-wide spillovers. It affects manufacturing competitiveness, logistics reliability, and the bankability of downstream investments. For external partners, this makes energy a logical entry point for guarantees, local currency support, and project preparation facilities. |

| Transport and logistics | Ports, rail, corridors, and freight-enabling assets that reduce physical trade frictions | Transport assets shape whether regional trade agreements translate into actual market integration. Co-financing in this segment can produce wider returns if corridor projects are linked to customs reform, border management, and industrial clusters rather than treated as stand-alone construction finance. |

| Telecommunications | Digital backbone and connectivity infrastructure that lowers information and transaction costs across firms and public systems | Telecoms sit at the intersection of productivity and state capacity. Better connectivity improves payment systems, logistics coordination, and service delivery. For G7 and G20 actors, digital infrastructure partnerships need to address cybersecurity, data governance, and affordability alongside capital provision. |

| Natural resources | Infrastructure tied to extraction, processing, and movement of resource-based outputs | This segment can either reinforce enclave models or support domestic value addition. The policy distinction is whether financing is attached to processing capacity, energy access, and transport links that keep more value on the continent. |

| Heavy industries | Industrial platforms and productive assets that use infrastructure as a base for manufacturing and processing | Heavy industry pushes AFC beyond basic service provision into structural transformation. These projects can deepen domestic supply chains, but they also require careful assessment of off-take risk, power availability, and trade competitiveness. |

Reading the portfolio strategically

The core point is portfolio design.

AFC's sector spread suggests an operating model built around bottlenecks between sectors, not only financing gaps within them. That is a different proposition from narrowly themed funds that can support one class of asset well but have limited ability to address why adjacent constraints continue to depress returns. For public and private partners, the implication is practical. Cooperation with AFC is likely to work best when external capital reinforces these interconnections rather than carving them back into silos.

This also sharpens project selection. A transport corridor has greater development value if reliable power, telecoms coverage, and industrial users are present around it. An energy asset is more likely to sustain revenues if logistics and productive demand are developing alongside it. AFC's multi-sector platform gives it a better chance of identifying those complementarities at origination stage.

For readers seeking wider context on the financing environment, analysis of mobilising investment for sustainable infrastructure amid global crises sets out the broader constraints facing long-horizon infrastructure capital.

From assets to economic systems

This portfolio composition has direct implications for global governance. It positions AFC as more than a lender to discrete projects. It is an intermediary that can influence how infrastructure, industrial policy, and regional integration interact in practice.

For G7 and G20 stakeholders, that creates clear opportunities and clear risks.

The opportunity is better coordination. Partners can use AFC as a platform for co-financing projects where commercial discipline and development objectives overlap, especially where cross-sector sequencing is central to success. The risk is that breadth can obscure trade-offs. A wide mandate can pull an institution toward politically attractive projects, resource nationalism, or industrial strategies that lack competitive foundations.

The strategic test, then, is not whether AFC finances many sectors. It is whether that breadth translates into disciplined portfolio construction, stronger regional value chains, and projects that remain commercially credible after concessional support recedes. That is the standard international partners should use when deciding where AFC fits within a broader infrastructure and development agenda.

Driving Climate Action and Regional Integration

African infrastructure choices will shape emissions trajectories for decades. They will also determine whether the African Continental Free Trade Area is supported by functioning power pools, transport links, and data networks or constrained by fragmented national systems. AFC matters in this context because it finances assets that sit at the intersection of both agendas.

Climate relevance beyond green labelling

The strongest climate contribution from institutions such as AFC is often not a narrowly defined green transaction. It is the financing of systems that change the carbon intensity, reliability, and economic geography of growth. Power generation, transmission, transport logistics, and industrial inputs all affect whether firms invest in cleaner production or remain tied to costly, carbon-intensive alternatives.

That gives AFC a policy role that is larger than project appraisal. Its model can influence how African countries sequence electrification, industrial expansion, and trade connectivity. For G7 and G20 governments, that matters because climate cooperation in Africa will be more credible when mitigation is linked to energy access, productive capacity, and fiscal realism.

A useful framework for that broader challenge appears in this analysis of the climate finance gap and emissions alignment.

Regional integration as an investment discipline

Regional integration is often discussed as a trade policy objective. In practice, it depends on infrastructure with cross-border utility and on financiers willing to absorb long construction periods, regulatory inconsistency, and coordination failures between states. AFC's operating model gives it a natural position in that space because it can work across jurisdictions and sectors rather than treating each asset as a stand-alone transaction.

That distinction matters. A port expansion without inland logistics, transmission capacity without industrial demand, or fibre investment without reliable power can leave countries with underused assets and weak development returns. An institution that finances connected systems, rather than isolated projects, can improve the odds that regional corridors function as economic networks.

Strategic implication: G20 actors should treat selected infrastructure financiers as practical instruments of trade integration and climate policy, provided project selection remains disciplined and commercially credible.

Why this matters for external partners

External partners often separate climate, trade, and development finance into different policy channels. AFC's portfolio logic suggests that this division can be counterproductive in African markets, where the same asset may affect emissions, export capacity, grid stability, and regional resilience at once.

The following video offers additional institutional context.

For G7 and G20 stakeholders, the practical question is not whether africa finance corporation can support climate action in principle. It is whether partnerships are designed around regional systems, policy coordination, and bankable transition pathways rather than around climate-labelled deals alone. That approach offers a larger opportunity, but it also requires tighter standards on governance, project preparation, and cross-border execution.

Policy Implications and Risks for G7/G20 Stakeholders

For G7 and G20 policymakers, the central question is strategic allocation. AFC has shown that an African-led institution can originate, structure, and finance infrastructure transactions that many external actors struggle to advance on their own. That makes it relevant not only as a source of capital, but as an operating partner in sectors where project preparation, execution discipline, and local market knowledge determine whether public policy goals become bankable assets.

The policy significance is larger than AFC's balance sheet. Its model links commercial discipline with developmental objectives in a way that speaks directly to current G20 constraints: limited fiscal space, pressure to mobilise private capital, and growing demand for energy, logistics, and industrial infrastructure that can support both growth and decarbonisation. For external stakeholders, that creates a practical opportunity to use AFC as a channel for co-financing and risk sharing rather than treating Africa policy, climate policy, and trade policy as separate agendas.

That opportunity comes with clear conditions.

What G20 stakeholders should take from AFC's model

AFC offers three lessons with direct relevance for G7 and G20 ministries, development finance institutions, and export credit agencies.

First, institution building matters as much as transaction volume. AFC's value lies partly in its ability to move from project development to financing and syndication within one platform. Many public institutions support only one stage of that chain. The result is fragmentation, slower execution, and weaker mobilisation.

Second, partner diversification has geopolitical value. An institution with African ownership and market credibility gives external governments a wider set of credible counterparts. That can reduce excessive dependence on a narrow group of bilateral lenders or multilateral channels, while improving alignment with host-country priorities.

Third, the model has limits that external partners should acknowledge early. AFC operates in markets where regulatory uncertainty, currency pressure, and sovereign stress can quickly alter project economics. A high-functioning origination platform improves project flow. It does not remove country risk.

Strong institutional performance should be read as a capacity signal, not as a substitute for sovereign, regulatory, or project-level due diligence.

Where the main risks sit

The most material policy risk is not that AFC works in difficult markets. That is part of its comparative advantage. The risk is that external partners may treat institutional credibility as a proxy for low exposure, and then underprice concentration risk by country, sector, or counterparty.

AFC's own description of its model emphasises close work with governments and a focus on infrastructure solutions across African markets, as set out on AFC's overview of the solutions it delivers. That operating model can produce strong development impact and better project origination. It also means sovereign relationships remain central to execution. Delays in approvals, tariff adjustments, foreign exchange shortages, or contract disputes can weaken otherwise sound projects even when the institution itself remains financially stable.

This distinction matters for G20 risk frameworks. Credit ratings and institutional resilience indicators speak to AFC's capacity to absorb shocks. They do not eliminate the need for granular assessment of country exposure, refinancing profiles, and dependence on public counterparties in fragile settings.

A practical framework for partnership decisions

G7 and G20 stakeholders should assess engagement with AFC against three tests.

Additionality

Use AFC where it has a demonstrated advantage in origination, structuring, or local execution, not where external public finance can already act effectively on its own.Transparency

Request clearer disclosure on portfolio concentration, sovereign-linked exposure, and risk transfer arrangements before scaling co-financing commitments.Policy coherence

Align climate, trade, industrial, and development objectives at the transaction design stage. Projects tied to regional power, transport, or industrial systems often fail when each policy instrument is applied in isolation.

The policy conclusion is straightforward. AFC is most useful to G7 and G20 actors when it is treated as a specialist implementation partner with strong regional knowledge, not as a substitute for public governance standards or disciplined risk allocation.

Why this balance matters for global governance

There is a wider governance implication. If G20 members want more private capital in African infrastructure, they will need institutions that can convert broad policy intent into investable structures under difficult operating conditions. AFC has shown that this can be done. Yet the same features that make such institutions effective also require stronger partnership disciplines from external actors.

That argues for conditional engagement built on better disclosure, clearer risk sharing, and tighter coordination between development banks, export credit agencies, climate funds, and institutional investors. For G7 and G20 stakeholders, the policy objective should be to back AFC where it expands financing capacity and regional delivery, while avoiding a familiar error in development finance: counting mobilisation gains without pricing political and sovereign fragility with enough realism.

Pathways for Partnership and Strategic Engagement

For G7 and G20 governments, the practical question is not whether AFC can finance infrastructure. Its record already shows that it can. The harder policy question is how to work with AFC in ways that improve project delivery, preserve public accountability, and direct scarce concessional and guarantee instruments to the points of highest additionality.

That requires a partnership model built around function, not rhetoric.

Where partnership could move fastest

The clearest opening is earlier coordination at pipeline stage. By the time many infrastructure transactions reach formal fundraising, the central policy choices have already been made: currency denomination, offtake structure, sovereign support, local content assumptions, and the division of construction and political risk. External partners that join only at the end often add capital without changing the terms that determine bankability or development impact.

AFC is better suited to a different role in the G20 toolkit. It can serve as an originating and structuring partner for projects that need regional market knowledge, commercial discipline, and execution capacity across difficult operating environments. For G7 and G20 stakeholders, that points to a more selective form of engagement. The objective should be to use public instruments where they change risk allocation or lower the cost of capital, rather than where they merely increase headline financing volumes.

Transparency still matters, but the priority is operational disclosure that improves coordination. Comparable reporting on sovereign exposure, guarantee structures, refinancing assumptions, and climate-related performance would make it easier for development banks, export credit agencies, and institutional investors to judge where AFC participation adds value and where risks remain too concentrated.

A practical agenda for G7 and G20 actors

Co-develop pipelines before financial structuring is fixed

Governments, DFIs, and climate finance vehicles should engage AFC at origination stage. That is the point at which guarantees, technical assistance, foreign exchange support, and policy reform can still change project design.Build platform-based partnerships in priority sectors

Isolated transactions rarely solve the coordination failures that hold back African infrastructure. Joint platforms in power transmission, digital infrastructure, transport logistics, and industrial processing can produce repeatable structures, lower transaction costs, and create a clearer route for private co-investment.Set disclosure standards as a condition of scaled cooperation

Partnership should include agreed reporting on portfolio concentration, contingent liabilities, procurement approach, and development outcomes. That would improve comparability across institutions and help shareholder governments defend participation on policy as well as financial grounds.Align trade, climate, and development instruments around the same assets

Export credit agencies, climate funds, and development finance institutions often support adjacent objectives through separate channels. AFC offers a credible counterparty for integrating those tools around projects that advance energy security, adaptation, industrial capacity, and regional connectivity at the same time.

The deeper opportunity

The strategic case is larger than individual deals. AFC gives external partners a route to support African infrastructure through an institution with regional knowledge and an established execution model, while avoiding the fragmentation that has weakened many bilateral initiatives. That has implications for speed, legitimacy, and policy coherence.

It also changes the politics of partnership. Programmes are more likely to gain traction when African institutions shape project selection and financing architecture, rather than receiving externally designed packages after priorities have already been set.

For G20 delegates, the implication is clear. AFC should be treated as a partner for disciplined co-financing and implementation, with clear safeguards and disclosure expectations, not as a proxy for public governance or a vehicle for indiscriminate risk transfer. Used well, it can help connect global capital, development policy, and African infrastructure demand in ways that are more credible than fragmented pledges and more durable than one-off transactions.

Global Governance Media provides the kind of decision-focused analysis that policymakers and institutional leaders need when issues like AFC move from technical finance into strategic governance. If you're tracking G7 and G20 priorities on infrastructure, climate finance, trade, and multilateral reform, follow Global Governance Media for authoritative briefings, expert commentary, and practical insights that support better policy choices.