By Dr Eleanor Hart, Senior Policy Analyst

An emerging markets index began life as a narrow investment benchmark. It now operates much closer to critical financial infrastructure. The clearest proof is historical scale. The MSCI Emerging Markets Index launched in 1988 with stocks from 10 countries and represented less than 1% of the world's investable equity market capitalisation. By late 2020, that share had risen to approximately 13% of the global stock market, according to Morningstar's analysis of the index's evolution.

For G7 and G20 finance ministers, that change matters because benchmarks no longer merely describe markets. They organise capital, steer reform incentives, amplify stress, and influence which countries sit at the centre of global portfolio construction. A committee decision at a private index provider can alter the financing conditions facing sovereigns, banks, exporters, and pension systems across multiple jurisdictions.

That is why the emerging markets index deserves to be read as an instrument of economic statecraft. It shapes who receives capital, under what governance assumptions, and with what exposure to currency, technology, and trade risk. When policymakers treat indices as technical market plumbing, they miss the larger reality. These benchmarks now sit at the junction of public regulation and private capital allocation.

The policy question is no longer whether ministers should understand index mechanics. It's whether they can afford not to.

Table of Contents

- Introduction The Trillion-Dollar Benchmarks Shaping Global Growth

- Decoding the Emerging Markets Index

- The Architecture of Influence Index Construction Rules

- Comparing the Gatekeepers MSCI vs FTSE vs S&P

- The Index Effect How Benchmarks Drive Capital and Policy

- Modern Challenges Governance and Measurement Dilemmas

- A Roadmap for G7 and G20 Policymakers

Introduction The Trillion-Dollar Benchmarks Shaping Global Growth

Finance ministries often discuss emerging markets through the lenses of growth, debt, commodities, or geopolitical alignment. The emerging markets index cuts across all four. It compresses many national stories into a single investable signal, then transmits that signal into portfolio mandates, ETF allocations, pension rebalancing, and sovereign risk perception.

That makes the benchmark unusually powerful. It doesn't legislate, yet countries adapt policy to remain investable. It doesn't negotiate trade terms, yet it influences the cost and stability of capital that supports trade expansion. It doesn't regulate corporate conduct, yet its sector composition can clash directly with national sustainability rules.

The benchmark as a policy transmission channel

A useful way to think about an emerging markets index is as a private rulebook with public consequences. Inclusion standards, liquidity screens, free-float tests, and market accessibility judgements determine whether a national market is visible and investable to global institutions. When those institutions act at scale, benchmark design becomes a transmission channel for cross-border financial conditions.

Practical rule: If a benchmark can trigger automatic buying or selling, it has systemic importance whether or not it has formal regulatory status.

For ministers, that insight changes the agenda. Emerging market benchmarks shouldn't be left only to portfolio managers and index specialists. They belong in conversations about financial stability, capital flow resilience, trade diversification, and sustainable development.

Why this matters now

The policy stakes are sharper because today's benchmark is more concentrated and more entangled with technology supply chains, ESG regulation, and currency volatility than earlier versions were. The result is a new class of risk. A benchmark change can now affect not just investor returns, but also export earnings, domestic political pressure for market reform, and the coherence of multilateral standards.

An emerging markets index is therefore not just a scorecard of developing economies. It is part of the machinery through which globalisation is currently governed.

Decoding the Emerging Markets Index

By 2021, roughly three quarters of the main emerging markets benchmark was concentrated in four economies in Asia, according to the Morningstar analysis cited earlier. That concentration explains why finance ministries should treat these indices as more than portfolio tools. They shape where international capital can move at scale, which countries gain valuation support, and where market stress can spread fastest.

An emerging markets index functions as a rules-based basket of listed companies from countries classified as emerging by a benchmark provider. Its influence comes less from the label than from the filters behind it. Country eligibility, investability, company size, liquidity, and free-float all determine what global investors are permitted to own in benchmark-aware portfolios.

Those mechanics matter because benchmark inclusion creates demand that is partly automatic. Passive funds must replicate the index. Active managers are often judged against it and tend to stay close to its composition to control tracking error. For a government seeking stable foreign portfolio participation, entry into a major benchmark can therefore matter almost as much as a sovereign rating upgrade.

The evolution of the MSCI benchmark illustrates the scale of that shift. Morningstar's review notes that the index began in 1988 with 10 countries and less than 1 percent of world investable equity market capitalisation. By late 2020, emerging markets accounted for about 13 percent of the global stock market, and over the 2001 to 2020 period the benchmark delivered higher annualised returns than MSCI World, alongside materially higher volatility and deeper drawdowns.

For policymakers, the conclusion is straightforward. These indices combine growth exposure with transmission risk.

That combination makes them instruments of economic statecraft. A country's presence in the index affects its cost of capital, the visibility of its corporate sector, and the pressure it faces to align market infrastructure with global norms on access, settlement, disclosure, and governance. The benchmark also reveals where the world's institutional investors are structurally exposed. Heavy weights in China, Taiwan, Korea, and India mean that an emerging markets allocation is also a position on Asian technology manufacturing, supply-chain resilience, and regional geopolitical stability.

A short primer helps frame the mechanics in visual terms.

The benchmark no longer tracks growth alone. It channels capital toward markets that private index providers judge accessible, investable, and scalable for global institutions.

The Architecture of Influence Index Construction Rules

An emerging markets index doesn't arise naturally from economic growth alone. It is built through explicit construction rules. Those rules decide not only which markets appear in the benchmark, but also how concentrated the final product becomes.

Weighting decides concentration

Most flagship benchmarks use market-capitalisation weighting. In practice, that means larger listed companies and larger accessible markets receive greater weight. This gives the index efficiency and replicability, but it also channels capital towards the largest incumbents rather than towards the broadest set of economies.

Three construction choices usually do the most work:

- Market-cap weighting: Larger firms dominate because the benchmark reflects size, not developmental importance.

- Free-float adjustment: Providers focus on the shares that are available to public investors, which reduces the role of tightly held companies or state-controlled structures.

- Liquidity screening: A company may be large on paper but still fail inclusion if investors can't trade it efficiently.

For ministers, those rules create a policy dilemma. A country can improve macroeconomic performance and still fail to gain weight if foreign investors face frictions in access, conversion, custody, disclosure, or settlement.

Classification is policy by other means

Country classification is where private methodology meets public policy most directly. Providers assess a mix of qualitative and quantitative factors. The exact formulations differ, but the policy-relevant questions are consistent. Can foreign investors enter and exit predictably? Are currency arrangements workable? Are custody and settlement systems dependable? Do market rules protect minority shareholders and support orderly trading?

That means governments often end up reforming market plumbing, not just macroeconomic fundamentals, to secure benchmark status. The benchmark becomes a scoreboard for operational credibility.

A concise way to read the architecture is this:

| Construction lever | What it tests | Why policymakers should care |

|---|---|---|

| Market size and weighting | Scalable investability | Determines whether reforms translate into global allocation |

| Free-float rules | Actual availability to investors | Limits headline size if ownership is concentrated |

| Liquidity and access | Ease of entry, exit, and trading | Influences whether capital is stable or episodic |

| Classification review | Institutional operability | Signals international confidence in market governance |

Benchmarks reward not just growth, but governability in a form that portfolio managers can operationalise.

That is why index rules should be read as the hidden constitution of international equity allocation.

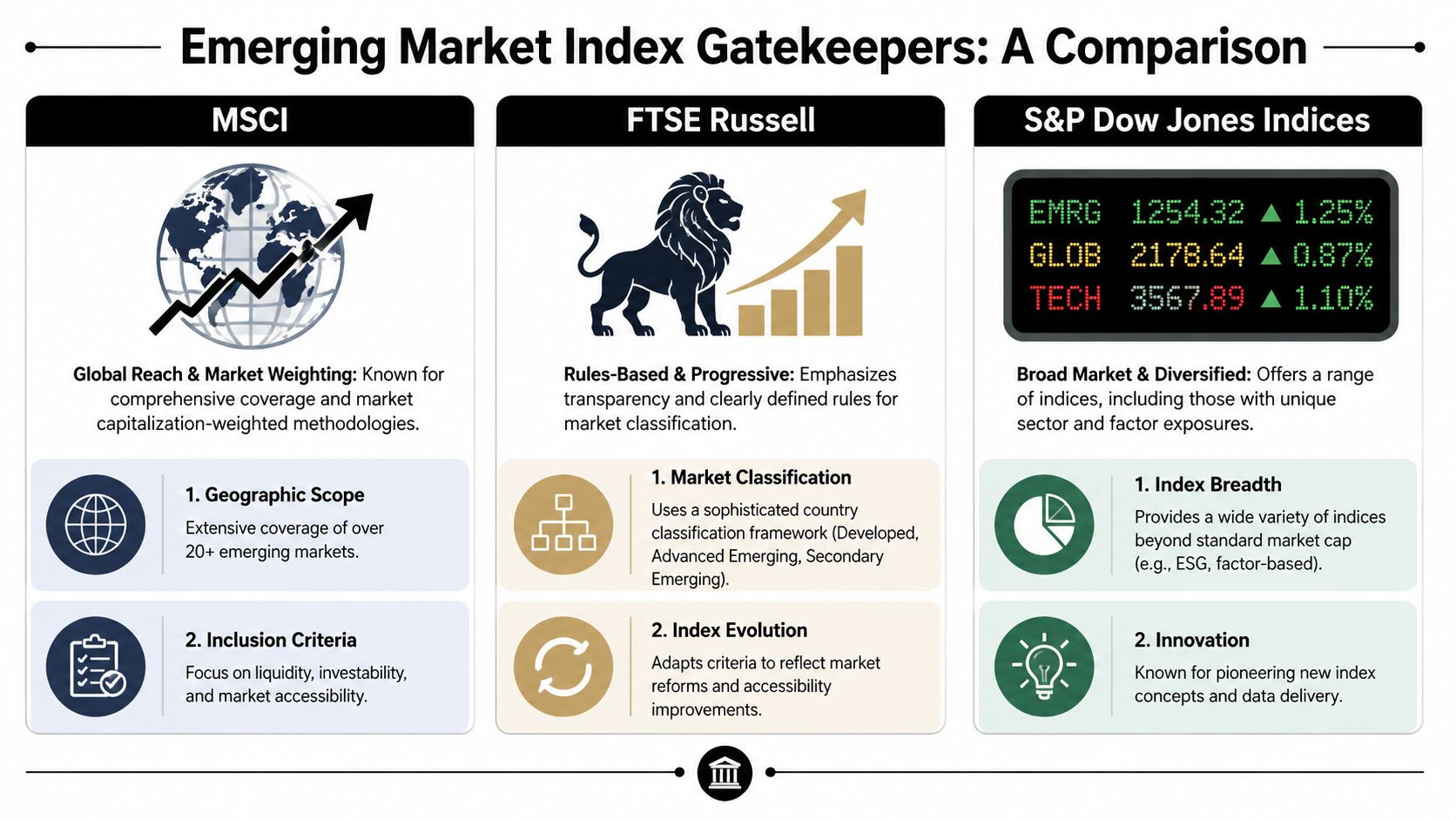

Comparing the Gatekeepers MSCI vs FTSE vs S&P

A country can be investable to global institutions and still be treated differently by the three firms that define much of the benchmark universe. For G7 and G20 ministers, that is not a technical curiosity. It shapes capital allocation, reform incentives, and the transmission of financial stress across borders.

MSCI, FTSE Russell, and S&P Dow Jones Indices each convert market access, liquidity, and governance conditions into index membership. Yet they do not translate those conditions in the same way. Their methodologies reflect different judgments about what counts as sufficiently open, sufficiently tradable, and sufficiently reliable for international investors.

Three providers, three policy signals

MSCI is widely treated as the reference point for global emerging market equity exposure, particularly among cross-border asset managers. FTSE Russell carries weight with institutions that track its country classification process closely, including many investors with long-standing links to UK and European portfolio mandates. S&P Dow Jones Indices offers another influential framework, often used by investors seeking broader segmentation across regional, style, or strategy-based index families.

Those differences matter because benchmark providers do more than measure markets. They assign operational credibility. A market that clears one provider's threshold may still fall short under another provider's test for accessibility, foreign ownership treatment, or trading infrastructure. The result is a fragmented external verdict on the same national reform story.

| Provider | Flagship Index | Distinctive emphasis in country classification | Policy implication |

|---|---|---|---|

| MSCI | MSCI Emerging Markets Index | Strong focus on market accessibility and investability for international institutions | Reforms that improve entry, exit, and foreign investor treatment can have outsized benchmark consequences |

| FTSE Russell | FTSE Emerging Index family | Tiered classification system with clearly differentiated market-status categories | Governments often face a more staged path, where partial reform can change perception before full reclassification |

| S&P Dow Jones Indices | S&P emerging market index family | Hybrid approach to market structure, accessibility, and index design across multiple families | Policymakers may encounter a less uniform external signal, especially when investors track different S&P benchmark variants |

The practical conclusion is straightforward. There is no single authoritative map of the emerging market universe.

Why these distinctions matter for economic statecraft

For finance ministries, central banks, and market regulators, cross-provider divergence creates a coordination problem. Domestic reforms may be rational and internationally credible, yet still fail to produce a unified portfolio response if major benchmark houses interpret progress differently. That weakens the assumption that market-opening measures will automatically translate into lower funding costs or more stable foreign participation.

It also changes how countries should assess progress in capital markets development. The relevant question is not only whether a reform passes domestic legislation or wins praise from investors at roadshows. The harder test is whether multiple index gatekeepers judge the market to be operationally dependable at scale.

This has systemic implications. If benchmark providers classify the same market differently, passive and benchmark-aware active funds can hold structurally different exposures to the same country. In periods of stress, that divergence can amplify price dislocation, complicate official communication, and blur the signal policymakers think they are sending to international capital.

Index providers are not neutral observers of market development. Their rulebooks help define which reforms convert into allocatable capital, and which remain politically visible but financially discounted.

Ministers should therefore monitor all three provider families, not just the benchmark most commonly cited in investor presentations. A single-provider strategy is too narrow for a world in which private index methodology influences sovereign financing conditions, external vulnerability, and the distribution of global growth capital.

The Index Effect How Benchmarks Drive Capital and Policy

The most important policy feature of an emerging markets index is the index effect. Benchmark decisions don't stay on paper. They trigger portfolio adjustments by funds that are designed to track, approximate, or stay close to the index. That creates a chain reaction from methodology to money.

From benchmark change to market pressure

The sequence is straightforward. A provider changes inclusion, exclusion, or weighting rules. Passive vehicles rebalance. Active managers who are measured against the benchmark often respond as well. Liquidity concentrates around the rebalance window. Local asset prices, currencies, and hedging costs can all move in response.

That creates an underappreciated fact of modern finance. Countries do not compete for foreign investment through growth narratives or summit diplomacy alone. They also compete through index eligibility, investor access, and benchmark weight preservation.

For policymakers concerned with capital-market development, the core issue is not whether benchmarking exists. It's whether governments understand how benchmark-linked flows interact with domestic financial resilience. A broader discussion of that institutional challenge appears in this analysis of capital markets development and policy design.

Why the UK channel matters systemically

The UK case illustrates how benchmark-linked flows can become a macro-financial transmission mechanism. FTSE Russell data indicates that UK-based institutional investors manage over 40% of global EM assets, and Bank of England stress tests show that a 10% EM drawdown can trigger £150bn in UK portfolio outflows, directly depressing the index by 1.5-2% through forced liquidations, according to the cited Marketscreener summary of the benchmark's market dynamics.

That isn't just a UK portfolio story. It implies a feedback loop in which benchmark losses, institutional mandates, and liquidity pressure reinforce each other across borders. The benchmark becomes both the map and the mechanism of contagion.

Two policy conclusions follow:

- Central banks need benchmark awareness: Stress testing should examine not only direct exposures but also rule-driven rebalancing channels.

- Finance ministries need coordination tools: FX liquidity arrangements and supervisory dialogue matter when concentrated investor bases can transmit stress internationally.

A benchmark can accelerate outflows even when no country-specific fundamental shock has changed. The trigger can be portfolio mechanics alone.

Modern Challenges Governance and Measurement Dilemmas

Emerging market benchmarks now sit at the intersection of market efficiency, industrial policy, and financial stability. For ministers, the central question is no longer whether these indices represent growth. It is whether their design still serves as a credible public reference point when private rules shape sovereign financing conditions, capital access, and external vulnerability.

Sector concentration is now a governance problem

A benchmark marketed as broad exposure can, in practice, become highly dependent on a narrow set of sectors and issuers. As noted earlier, major emerging market indices are heavily tilted toward technology and financials. That concentration matters because it imports policy conflict directly into passive allocation. Export controls, semiconductor restrictions, data governance rules, and sustainability screens all start to affect index usability, even when the benchmark methodology has not changed.

This creates a statecraft problem as much as a portfolio problem.

If a country's weight in a benchmark rests heavily on firms exposed to strategic technology competition, then index inclusion stops being a neutral market label. It becomes part of a wider geopolitical sorting process. A benchmark review, or a shift in institutional screening standards, can alter capital costs for affected markets without any corresponding change in domestic macro fundamentals.

Disclosure standards make this worse. Where investors cannot compare governance quality, related-party exposure, or state influence across issuers, benchmark construction starts to reward scale and liquidity more than institutional credibility. That weakens the signalling value of the index itself, and it reinforces concerns raised in wider debates on corporate transparency and regulatory credibility.

Currency risk has become a policy coordination problem

Currency exposure is often treated as a technical feature of benchmark investing. For G7 and G20 policymakers, it is better understood as a transmission channel between global portfolios and domestic policy constraints. Local-currency weakness can reduce returns for foreign investors, raise hedging demand, and intensify outflow pressure at the same moment that emerging market central banks are trying to preserve policy space.

The policy tension is straightforward. Trade ministries often want deeper commercial integration with high-growth emerging economies. Financial regulators are more likely to focus on volatility transmitted through funds, derivatives, and collateral markets. Pension supervisors want benchmark-relative discipline. Sustainability authorities may push investors away from benchmark-heavy sectors or issuers. These objectives are individually rational, but they can pull in opposite directions when index design remains largely outside the policy conversation.

The result is a measurement dilemma. Benchmarks are still used as shorthand for country opportunity, yet they often capture only the investable slice that meets foreign ownership, liquidity, and custody thresholds. That makes them useful for asset allocation, but incomplete for public strategy. Ministers relying on benchmark performance alone may overestimate resilience, underestimate concentration, and miss how quickly private index rules can amplify external shocks.

The policy conclusion is clear. Emerging market indices should be monitored not only as investment tools, but as market infrastructure with distributional and systemic consequences.

A Roadmap for G7 and G20 Policymakers

Roughly a tenth of global equity assets are benchmarked to emerging market indices. That gives a small group of private rulebooks outsized influence over capital allocation, currency pressure, and reform incentives across economies that account for a much larger share of global growth.

For G7 and G20 finance ministers, the policy question is no longer whether these benchmarks matter. It is how to treat them as part of the international financial architecture. Indices shape portfolio mandates, determine which markets are considered investable at scale, and can accelerate repricing when market access, governance, or settlement conditions change. In practice, that makes them instruments of economic statecraft as much as tools of investment management.

Treat index infrastructure as a policy domain

A credible agenda starts with transparency. Ministers should establish routine dialogue with major index providers on review processes, accessibility criteria, consultation practices, and the operational triggers that can lead to inclusion, exclusion, or reclassification. Public authorities do not need to direct index weights. They do need a clearer view of how private benchmark decisions interact with sovereign funding conditions, reserve management, and domestic reform sequencing.

Standards alignment should come next. Fragmented ESG, disclosure, and market-operability rules create avoidable inconsistencies between what governments are asking markets to reward and what benchmark methodologies are built to measure. Greater comparability across jurisdictions would improve capital market signalling and reduce the risk that policy reforms fail to attract flows because they do not map cleanly onto index construction rules.

Stress testing also needs to catch up. Central banks, debt managers, and financial regulators should incorporate benchmark-linked flows into scenario analysis, especially in jurisdictions where passive investment, derivatives hedging, and concentrated custody networks can magnify cross-border movements.

Build coordination before the next shock

The trade dimension deserves closer scrutiny. As noted in the previous section, currency-driven volatility in benchmarked portfolios does not stay inside capital markets. It can alter exporter earnings, complicate hedging decisions, and tighten the link between external financing conditions and trade resilience. That matters for G20 ministers trying to reduce fragmentation while preserving macroeconomic stability.

A practical ministerial agenda would include:

- Structured benchmark dialogues: Regular exchanges among index providers, finance ministries, central banks, and securities regulators on methodology changes and market-access assessments.

- Cross-border liquidity planning: Coordination on swap lines, collateral practices, and market-functioning tools that can limit disorderly spillovers during index-driven rebalancing episodes.

- Data standard harmonisation: Better comparability on disclosure, foreign ownership limits, settlement systems, and sustainability reporting.

- Development strategy integration: Closer alignment between capital-market reform and long-term public investment priorities, including broader work on financing development strategies.

The broader implication is straightforward. Emerging market indices now influence how shocks travel, how reforms are rewarded, and which countries gain durable access to global savings. Ministers who monitor them as policy infrastructure, rather than as a niche market indicator, will be better positioned to contain instability and support more inclusive growth.

Global policymakers, analysts, and institutional leaders can follow more data-led coverage of financial stability, trade resilience, and multilateral economic strategy at Global Governance Media.