More than 1,300 of the UK's largest listed companies and financial institutions fell within the Financial Conduct Authority's climate disclosure regime in 2022. That scale matters because ESG reporting now sits inside core market infrastructure, where disclosure rules shape capital allocation, supervisory expectations, and competitive positioning across borders.

By Daniel Mercer

ESG reporting is the system companies use to disclose how their activities affect environmental, social, and governance issues, and how those issues in turn affect enterprise value, risk, and long-term performance. For boards, it has become part of market access and financing strategy. For investors, it improves the basis for pricing transition risk, labour practices, governance quality, and operational resilience. For governments, it is increasingly a policy instrument that influences investment flows, industrial strategy, and the terms of international economic cooperation.

The policy question is now larger than definition. It is whether major economies can produce enough interoperability between disclosure regimes to preserve comparability and trust, without giving up domestic priorities on climate, social outcomes, and corporate accountability.

That tension is most visible in the emerging divide between systems centred on investor-focused financial materiality and systems that also require reporting on a company's wider impacts on society and the environment. The practical consequence is not only higher compliance cost. It is the risk of fragmented reporting blocs, duplicated assurance demands, and weaker consistency in cross-border capital markets.

For G7 and G20 leaders, ESG reporting has therefore become a governance issue as much as a corporate one. The strategic challenge is to reduce unnecessary divergence between regimes such as the EU's CSRD and the UK's ISSB-aligned direction, while preserving enough flexibility for national policy choices. How that balance is handled will influence reporting burdens, investment comparability, and the broader credibility of global standards.

Table of Contents

- The Unstoppable Rise of ESG Reporting

- Beyond the Acronym The Core Purpose of ESG

- Navigating the Global Standards Maze

- What Companies Actually Report The E S and G Pillars

- The Engine Room Data Collection and Assurance

- Challenges and Geopolitical Fault Lines

- A Roadmap for Policymakers and Corporate Leaders

The Unstoppable Rise of ESG Reporting

More than 1,300 large UK companies and financial institutions were brought into mandatory TCFD-aligned reporting in 2022. That scale marks a structural change in how markets define acceptable disclosure.

ESG reporting now sits closer to financial reporting than to corporate communications. Once regulators require boards to publish decision-useful information on climate risk, governance, and resilience, sustainability stops being a side programme. It becomes part of the disclosure architecture that shapes access to capital, supervisory scrutiny, and corporate credibility.

ESG as disclosure, not branding

ESG reporting is the structured disclosure of how a company manages and performs on environmental, social, and governance issues. In practical terms, it gives investors, regulators, lenders, employees, customers, and counterparties a basis for judging whether management understands material risks, controls operational impacts, and governs the business with discipline.

The strategic significance is straightforward. ESG reporting converts broad commitments into a documented record that boards can be challenged on and regulators can test. It also creates a common reference point across firms, sectors, and jurisdictions, even when standards still differ.

ESG reporting has its greatest value when it links sustainability claims to strategy, controls, capital allocation, and board oversight.

Why the rise is now strategic

Two forces explain the speed of adoption. Capital markets want more consistent information on climate exposure, supply chain resilience, workforce practices, and governance quality. Regulators increasingly view sustainability disclosure as part of market integrity, prudential oversight, and economic stability.

That combination has consequences beyond compliance.

Companies now have to translate issues once handled through policy statements into reporting lines, internal controls, risk committee agendas, and assurance processes. For multinational groups, the task is harder still. They are not responding to one global rulebook, but to a fast-changing mix of national and regional regimes that only partly align.

The geopolitical dimension comes into play. The contest between more expansive systems such as the EU's CSRD and more investor-focused baseline approaches associated with ISSB is not only a technical debate about materiality. It is also a debate about who sets the terms of transparency in the global economy. Standards determine which risks become visible, which costs are internalised, and which business models face earlier pressure to adapt.

Why leaders should stop treating ESG as a silo

Corporate leaders often ask what ESG reporting requires. A more revealing question is what weak reporting capability signals about management quality. If a company cannot produce reliable sustainability data, reconcile it across functions, and defend it at board level, investors may reasonably question its grip on operational risk more broadly.

For policymakers, the stakes are larger than disclosure design. ESG reporting is becoming part of the institutional plumbing of cross-border commerce. Countries that promote clear, interoperable rules can reduce friction for issuers and investors. Countries that allow fragmentation to harden into competing blocs risk higher reporting costs, weaker comparability, and another channel through which economic governance becomes geopolitically divided.

Beyond the Acronym The Core Purpose of ESG

The core purpose of ESG reporting is to reduce opacity. Markets work poorly when major risks sit outside standard disclosure channels. ESG frameworks try to bring those risks into view.

That's why ESG has moved well beyond the older language of corporate responsibility. Traditional responsibility programmes often focused on intent, philanthropy, or brand positioning. ESG reporting demands evidence, governance, and comparability. It asks management teams to show how sustainability-related issues affect performance and how the business affects people, resources, and institutions around it.

Investor pressure changed the centre of gravity

Investor behaviour explains much of the shift. In the UK, 75% of investors actively consider ESG risks and opportunities when screening investment opportunities, according to PwC's sustainability reporting analysis. That figure tells us something larger than investor preference. It suggests ESG information is now part of capital allocation logic.

The same source shows where confidence still breaks down. 47% of investors cite ESG data coverage gaps as their biggest hurdle, 41% point to data quality issues, and 40% highlight inconsistencies in reported metrics. Those aren't side complaints. They are evidence that the market wants ESG information but still struggles to trust and compare it.

Regulation is filling the trust gap

Policy has moved in because voluntary disclosure left too much variation. In the UK, 72% of surveyed companies now experience regulatory pressure to report ESG information, as set out in KPMG's UK ESG assurance maturity report. The same reporting environment includes SECR obligations for quoted companies, large unquoted firms, and large LLPs reporting UK energy use above 40 MWh, greenhouse gas emissions, and at least one intensity ratio, with annual comparative figures.

Regulation isn't only forcing more disclosure; it is standardising what counts as relevant disclosure. This standardization creates a bridge between environmental and social issues on one hand, and financial governance on the other.

Practical rule: If a board treats ESG reporting as a communications product, it will usually underinvest in controls, ownership, and materiality analysis.

ESG reporting is about resilience

At its best, ESG reporting gives decision-makers a disciplined way to ask three questions:

- What can disrupt enterprise value: Climate exposure, supply chain labour risk, cyber governance failures, and weak oversight can all become financial issues.

- What can undermine legitimacy: Firms depend on public trust, regulatory licences, and social permission to operate.

- What can reveal strategic preparedness: A company that can map emissions, governance, and workforce risk usually understands its operating model better than one that can't.

That is why the actual purpose of ESG reporting isn't moral theatre. It is to improve visibility over risks and dependencies that conventional accounting alone doesn't fully capture.

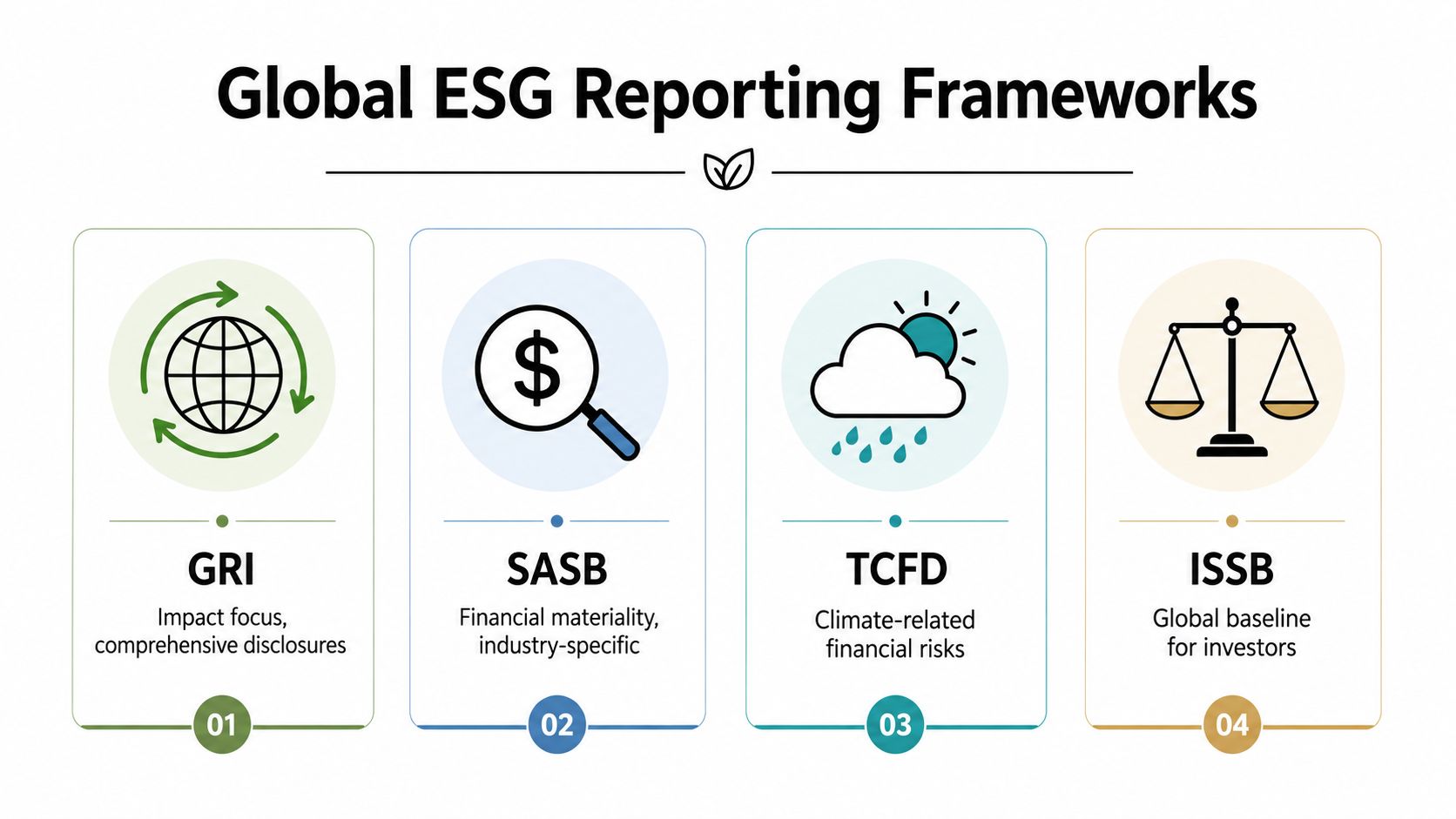

Navigating the Global Standards Maze

More than one major ESG reporting architecture now shapes global capital flows, regulatory access, and board oversight. The result is not just technical complexity. It is a policy question about whether the world is converging on a common disclosure baseline or splitting into regional blocs with different theories of corporate accountability.

Why frameworks exist at all

The main frameworks were designed for different decision-makers, so they ask different questions.

GRI supports impact reporting. It helps organisations explain how their operations affect workers, communities, and the environment.

SASB, now incorporated into the ISSB system, was built around financially material, sector-specific metrics for investors.

TCFD gave climate disclosure a durable structure through four pillars: governance, strategy, risk management, and metrics and targets. Regulators and standard setters reused that structure because it translated climate risk into board and finance language.

ISSB seeks to establish a global investor-oriented baseline through IFRS S1 and IFRS S2. Its strategic significance is larger than standard-setting alone. If widely adopted, it can lower reporting fragmentation across markets without requiring every jurisdiction to agree on a single model of stakeholder accountability.

That last point matters for G7 and G20 policymakers. Standard setting is becoming part of economic diplomacy. A jurisdiction that defines materiality, assurance, and comparability also shapes how capital judges corporate risk.

Where the UK now sits

The UK has moved toward ISSB alignment. The UK Sustainability Reporting Standards, endorsed in June 2025 and based on IFRS S1 and IFRS S2, are described by Tetra Tech's explanation of the UK SRS as integrating sustainability disclosures with general-purpose financial reporting, requiring assurance over Scopes 1 and 2 greenhouse gas inventories, setting a roadmap for Scope 3, and linking materiality assessments to cash-flow effects. That source indicates voluntary adoption begins in 2026 and that mandatory compliance for qualifying entities is expected to follow, with the first mandatory reporting periods expected to start on or after 1 January 2027.

Another account of the same direction appears in Watershed's guide to UK SRS adoption, which says the UK government had formally adopted the UK SRS by 25 February 2026, aligned them with ISSB standards, and expected the first mandatory UK SRS-aligned reports in 2028 covering FY2027 data. The precise timetable may still evolve. The strategic message is already clear. The UK is positioning sustainability disclosure inside the logic of mainstream financial reporting and closer to the information needs of global investors.

That alignment also has implications for market trust and supervisory coordination. This analysis of IOSCO's role in building trust in capital markets for sustainability reporting treats international coordination as a prerequisite for cross-border credibility, not as a secondary implementation issue.

Key ESG Reporting Frameworks at a Glance

| Framework | Primary Focus | Materiality Lens | Primary Audience |

|---|---|---|---|

| GRI | Broad sustainability impacts | Impact-oriented | Stakeholders beyond investors |

| SASB | Industry-specific financially relevant issues | Financial materiality | Investors and analysts |

| TCFD | Climate-related financial risk disclosure | Financial risk lens | Investors, regulators, lenders |

| ISSB | Global baseline for investor-grade sustainability reporting | Financial materiality | Global capital markets |

| CSRD and ESRS | Impact and financial sustainability reporting in the EU | Double materiality | Regulators, investors, civil society, wider stakeholders |

The sharpest divergence now sits between systems built around investor materiality and systems built around double materiality. The EU's CSRD and ESRS ask companies to report both how sustainability issues affect enterprise value and how the company affects society and the environment. The UK's direction of travel, by contrast, is more closely tied to the ISSB model and its capital-markets baseline.

For multinational companies, this is less a choice between standards than an exercise in system design. They need reporting architecture that can translate one underlying data set into multiple regulatory outputs, while preserving consistency across filings, investor communications, and board reporting.

For governments, the stakes are broader. If interoperability improves, ESG reporting can support more comparable capital allocation across borders. If divergence hardens, disclosure standards may become another channel through which geopolitical competition is expressed in financial regulation.

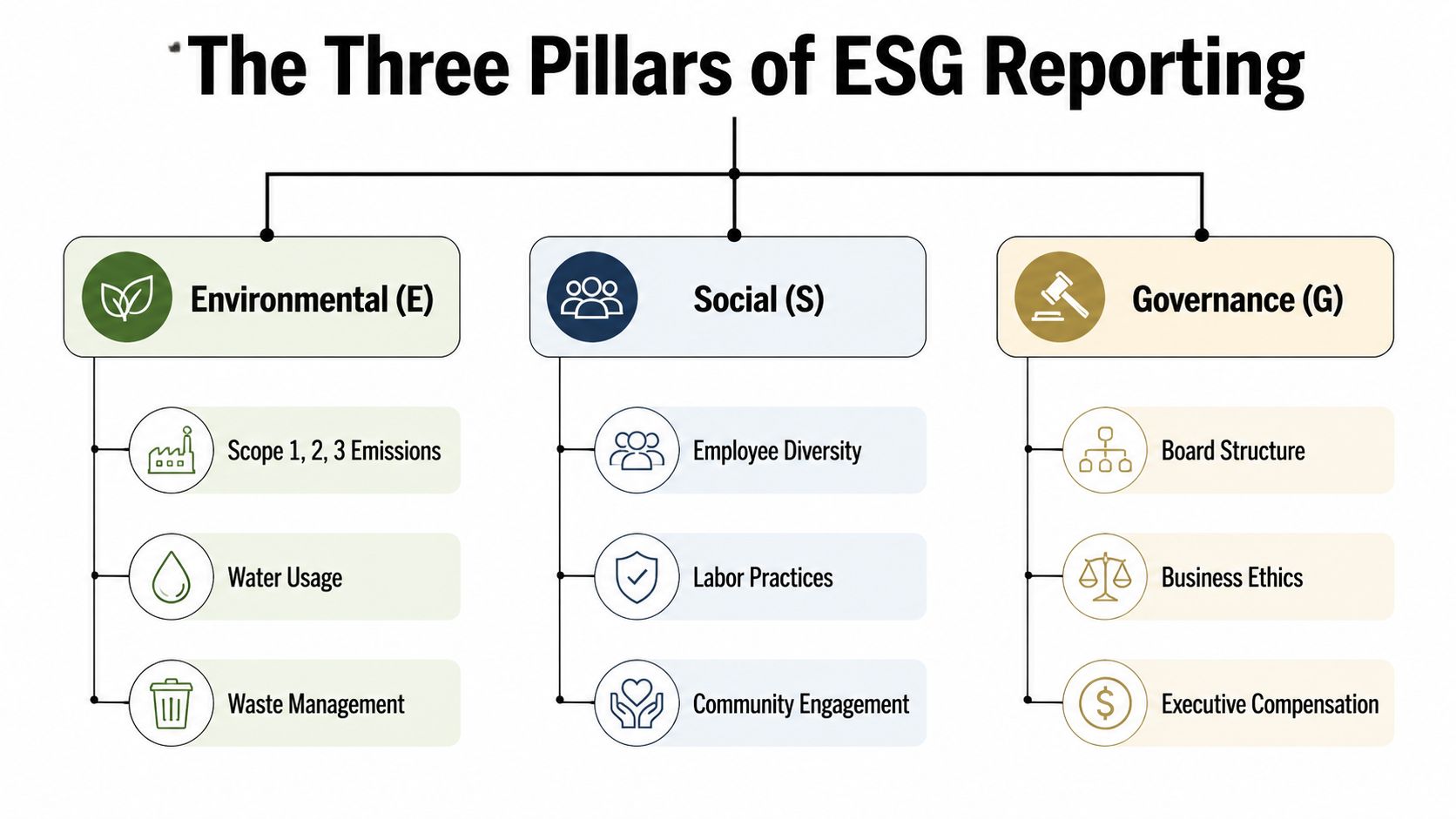

What Companies Actually Report The E S and G Pillars

The content of an ESG report becomes clearer once the acronym is broken into operating categories. The strongest reports don't treat the three pillars as separate public relations themes. They show how environmental exposure, workforce practices, and governance quality connect to risk and performance.

A useful visual summary sits below.

Environmental disclosures

Environmental reporting often starts with energy use and greenhouse gas emissions. In the UK context, mandatory ESG reporting under SECR and TCFD-aligned climate disclosure requires certain large companies and LLPs, including those with over £500M turnover or 500+ employees, to disclose energy consumption, Scopes 1 and 2 emissions, and climate-related risks across the four TCFD pillars within the NFSI statement of the strategic report, as outlined by Saffery's guide to UK ESG reporting requirements.

But high-quality environmental reporting doesn't stop there. Companies often also discuss water use, waste management, physical climate exposure, transition planning, and where relevant, biodiversity or nature dependencies.

A related discussion of how firms are directing investment sits in this analysis of corporate capital allocation towards climate action.

Social disclosures

Social reporting asks how the company treats people across its workforce, value chain, and customer base. Common topics include labour practices, diversity and inclusion, health and safety, supplier standards, training, community relationships, and data privacy.

The point isn't to generate a long list of human resources indicators. It's to identify where social practices affect continuity, legitimacy, and legal exposure. For a manufacturer, labour conditions in the supply chain may dominate. For a technology company, data security and workforce retention may be more central.

A concise explainer can help anchor these categories in practice.

Governance disclosures

Governance is often the decisive pillar because it determines whether the rest can be trusted. Investors and regulators look for signs that oversight is real rather than symbolic.

Typical governance disclosures include:

- Board structure: Who oversees sustainability, risk, and audit functions.

- Business ethics: Anti-bribery controls, whistleblowing arrangements, and compliance policies.

- Executive incentives: Whether leadership remuneration is connected to long-term strategic priorities.

- Decision rights: How management escalates climate, social, and operational risks to the board.

Good ESG reporting usually reads less like a manifesto and more like a controlled account of how decisions are made.

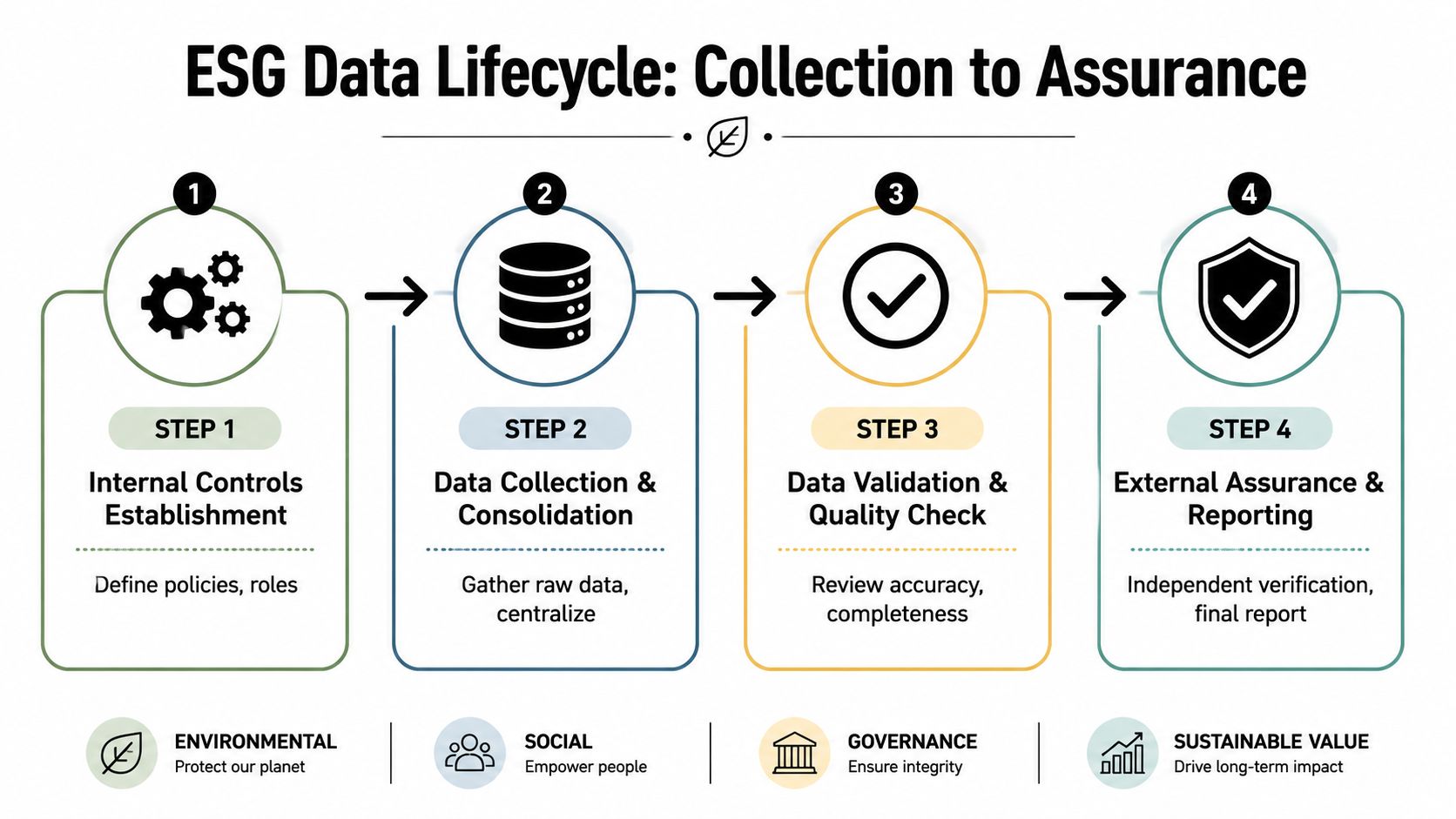

The Engine Room Data Collection and Assurance

Most ESG reporting failures aren't caused by bad intentions. They come from weak systems. Finance data usually has established controls, ownership, and testing. ESG data is often scattered across utility invoices, procurement systems, HR platforms, legal records, and supplier questionnaires.

That is why data collection and assurance are becoming the decisive test of credibility.

From source systems to board reporting

A credible ESG reporting process usually starts with internal controls. Companies need defined owners for each metric, agreed boundaries for reporting entities, clear calculation methods, and documented sign-off procedures.

The operational workflow often looks like this:

- Control design: Assign roles across finance, sustainability, legal, operations, and internal audit.

- Data consolidation: Pull information from source systems rather than relying on disconnected spreadsheets.

- Validation: Reconcile assumptions, check completeness, and test whether narrative claims match the data.

- Escalation: Bring unresolved issues to management committees before publication.

Many companies discover that ESG reporting is really a governance exercise disguised as a disclosure exercise.

Why assurance is moving to the centre

A major UK signal comes from this commentary on UK sustainability reporting and assurance, which notes that a June 2025 government consultation proposed an assurance provider regime, that 72% of UK ESG disclosures remain unassured in a 2025 FRC update, and that the FCA's March 2026 consultation on amended Listing Rules will likely mandate third-party assurance for climate data. The same source says only 12% of UK firms have prepared internal audit trails, citing Deloitte's 2024 maturity assessment.

Those figures point to a structural risk. Companies may be producing more sustainability information while lacking the evidence chain needed to defend it. That gap creates vulnerability to regulatory challenge, investor scepticism, and accusations of greenwashing.

For policymakers, the lesson is equally important. If disclosure expands faster than assurance capacity, reporting quality will be uneven and enforcement credibility will weaken.

Further perspective on the policy value of transparency appears in this discussion of green finance and climate action.

Assurance is no longer a technical add-on. It is becoming the mechanism that separates decision-useful disclosure from unsupported assertion.

Challenges and Geopolitical Fault Lines

The hardest part of ESG reporting isn't defining metrics. It's reconciling different regulatory philosophies without fragmenting global commerce.

The materiality divide

The most consequential divide today sits between single materiality and double materiality.

Single materiality asks how sustainability issues affect the company's financial position and enterprise value. That lens is central to ISSB-style reporting and now strongly influences the UK framework.

Double materiality asks two questions at once. How do sustainability issues affect the company, and how does the company affect society and the environment. That approach is central to the EU's CSRD and ESRS architecture.

The distinction sounds technical. It isn't. It changes what firms measure, what they disclose, and what boards are accountable for.

A concrete warning comes from Grant Thornton's practical guide to sustainability reporting. It states that 68% of UK-listed firms surveyed in 2025 failed to distinguish between single and double materiality in their 2024 reports, leading to regulatory warnings. The same source notes that UK SRS allows omission of Scope 3 if not material, while CSRD requires Scope 3 reporting when material.

That gap matters because companies operating across the UK and EU can easily produce disclosures that satisfy one regime while falling short in another. The problem isn't just compliance cost. It's strategic incoherence.

Why this matters for G20 coordination

For G20 policymakers, ESG standards now raise a familiar multilateral challenge. Every jurisdiction wants disclosure rules that reflect domestic priorities. Yet global investors and multinational firms need enough comparability to evaluate risks across borders.

Three fault lines are emerging:

- Regulatory sovereignty: Governments want to preserve domestic control over disclosure requirements.

- Capital market interoperability: Investors want a common baseline that reduces friction and duplication.

- Developmental fairness: Emerging economies need standards that improve transparency without creating prohibitive compliance burdens.

The deeper risk is geopolitical fragmentation. If the EU, UK, and other major markets harden around different concepts of materiality, reporting becomes a trade and investment friction point. Boards then spend more time translating frameworks than improving performance.

The long-term contest isn't over whether ESG reporting survives. It's over whose definition of relevance becomes globally dominant.

A Roadmap for Policymakers and Corporate Leaders

Policymakers should treat ESG reporting as part of financial architecture, not a specialist sustainability annex. The priority for G7 and G20 governments is to support interoperability between major standards, strengthen assurance regimes, and build supervisory capacity so disclosure quality improves alongside disclosure volume. Alignment won't require identical rules. It will require common concepts, clearer crosswalks, and credible oversight.

Corporate leaders need a different but parallel discipline. Boards should place ESG reporting under the same governance expectations as financial reporting. That means clear ownership, formal materiality assessment, legal review, internal audit involvement, and a documented path to assurance. Firms operating across jurisdictions should build one underlying data system capable of serving multiple frameworks rather than producing separate reports for separate regulators.

The immediate agenda is practical:

- For boards: Tie ESG oversight to audit, risk, and strategy committees rather than isolating it in corporate affairs.

- For executives: Build reporting processes around source data, controls, and sign-off, not late-stage drafting.

- For policymakers: Reduce unnecessary divergence between standards while preserving room for legitimate policy ambition.

- For multinational groups: Map where ISSB-style financial materiality and CSRD-style double materiality produce different disclosure outcomes, especially on value chain issues.

The broader conclusion is clear. ESG reporting has become a test of whether governance systems can adapt to a world where climate risk, supply chain conduct, and institutional trust are no longer externalities. They are part of economic statecraft.

For more policy analysis on climate governance, capital markets, and the strategic choices facing G7 and G20 leaders, read more from Global Governance Media. If this issue is on your agenda, follow the platform for ongoing coverage of sustainability standards, corporate governance, and the future of international economic cooperation.