By Eleanor Markham

The Athens General Index reached 2,537 points in July 2026, its highest level since November 2009, according to Trading Economics on Greece's stock market. That single figure changes how policymakers should read the Athens stock market. It is no longer useful to treat Athens merely as a peripheral exchange recovering from a sovereign debt crisis. The market now functions as a visible test of whether Greek policy credibility, institutional reform, and European integration are translating into durable capital formation.

That matters well beyond portfolio allocation. In Greece, equity prices often compress several policy judgements into one signal: whether investors trust fiscal management, whether domestic firms can access market finance, and whether the country is moving from crisis repair to long-horizon investment. In the Eurozone, the same market offers a narrower but revealing window into how a member state rebuilds confidence inside a shared monetary and regulatory framework.

The Athens stock market is also distinctive because its recent strength sits beside a cautionary valuation signal. On 2 July 2026, the estimated Greek market P/E ratio was 11.44, above the 5-year average range of [7.56, 11.11], a reading that Trading Economics characterises as overvalued. Policymakers should pay attention to that tension. A rising market can validate reform, but it can also run ahead of economic delivery.

Table of Contents

- Introduction The Resurgence of the Athens Stock Market

- From Drachma to Euro A History of the Exchange

- Deconstructing the ATHEX Market Structure

- Navigating Trading Mechanics and Regulation

- Analysing Recent Performance and Economic Drivers

- Systemic Importance for Greece and the European Union

- Investor Considerations and Future Prospects

- Conclusion The Athens Market as a Policy Nexus

Introduction The Resurgence of the Athens Stock Market

The current story of the Athens stock market is not merely one of price appreciation. It is one of institutional re-entry. When an exchange that spent years associated with stress, restructuring, and compressed valuations returns to a level last seen before the long aftershocks of crisis, officials should ask what has changed beneath the surface.

The answer isn't just sentiment. The exchange now sits at the intersection of domestic reform, European market integration, and renewed investor willingness to place Greek assets back into strategic rather than purely tactical allocations. That is why the market's resurgence deserves to be read as an economic governance signal, not just a financial headline.

Three features stand out.

- Historical memory matters: Athens is judged against a long arc of instability and recovery, so renewed strength carries more policy content than a routine upswing elsewhere.

- Institutional design matters: The exchange's structure, technology, and supervision shape whether market gains can support productive investment rather than short-lived speculation.

- European integration matters: Greece's market story is now inseparable from how EU rules, capital mobility, and common credibility frameworks affect national recovery.

The most useful way to read the Athens stock market is as a transmission channel between policy choices and investor beliefs.

That framing alters the policy conversation. A stronger exchange can widen financing options for firms, improve the signalling environment for foreign capital, and reinforce the credibility of reform. But a market that rises too quickly can also create complacency. If officials mistake valuation expansion for structural transformation, they'll misread what equity markets can and can't deliver.

The deeper issue is state capacity. Stock exchanges reward governments indirectly. They don't applaud speeches or policy branding. They reward predictable rules, functioning oversight, investable companies, and a macroeconomic environment that lowers the penalty investors attach to uncertainty. Athens therefore offers a practical lesson for the wider Eurozone. Recovery becomes durable when institutions turn political commitments into credible market conditions.

From Drachma to Euro A History of the Exchange

Greece's shift into the euro changed far more than the currency in circulation. It changed how the Athens market was interpreted by investors, regulators, and policymakers across Europe. Once equity pricing was embedded in a monetary union, the exchange became a more direct referendum on Greece's policy credibility within a shared institutional framework.

That wider role has deep historical roots. The Athens exchange emerged alongside the modern Greek state and developed in an economy where public finance, banks, and private capital were closely connected. In that setting, the exchange had an unusually clear public role. It reflected corporate prospects, but it also reflected the state's capacity to sustain orderly finance, attract savings, and anchor expectations.

The exchange through regime shifts

The drachma period gave the market a strongly national character. Exchange-rate risk, inflation expectations, and domestic political cycles shaped valuation more directly. Entry into the euro altered those mechanics. The cost of capital began to depend less on currency credibility alone and more on Greece's fit with Eurozone rules, supervisory standards, and the discipline imposed by cross-border investors.

That change carried an important implication. The market was no longer just a venue for Greek securities. It became part of the EU's broader allocation of capital, where Greek firms were judged against peers operating under the same monetary regime but often under stronger domestic institutions.

The sovereign debt crisis exposed that gap with unusual force. Equity prices did not fall only because earnings expectations deteriorated. They also reflected doubts about policy execution, banking-system stability, and Greece's position inside the monetary union. For officials in Athens and Brussels, the lesson was clear. A national stock market inside the euro can act as an early indicator of whether reform commitments are viewed as credible by private investors.

Historical lesson: In Athens, episodes of market stress have usually reflected wider institutional weakness rather than a standalone market malfunction.

The post-crisis period therefore involved more than reopening risk appetite. It required rebuilding trust in legal predictability, supervision, bank balance sheets, and the continuity of Greece's European policy orientation. Read in that context, the exchange's later integration into Euronext is not a branding exercise. It is part of a longer shift from a domestically bounded market toward infrastructure aligned with European standards and cross-border capital flows.

Why history still shapes current pricing

Investors do not treat Greek assets as if history has been erased. Crisis memory remains part of the valuation process, which raises the market's sensitivity to policy signals. Improvements in governance, fiscal discipline, or supervisory quality can therefore have a stronger effect on sentiment than in larger Eurozone markets where institutional credibility is taken for granted.

The reverse is also true.

Because Greece has already experienced a severe break in confidence, investors are quick to react to signs of policy drift, administrative delay, or weaker reform follow-through. That is why the Athens market matters for more than portfolio allocation. It functions as both a barometer of confidence in Greek economic management and an instrument through which EU integration affects domestic financing conditions. In Greece's case, market history is not background context. It remains part of the mechanism through which policy is priced.

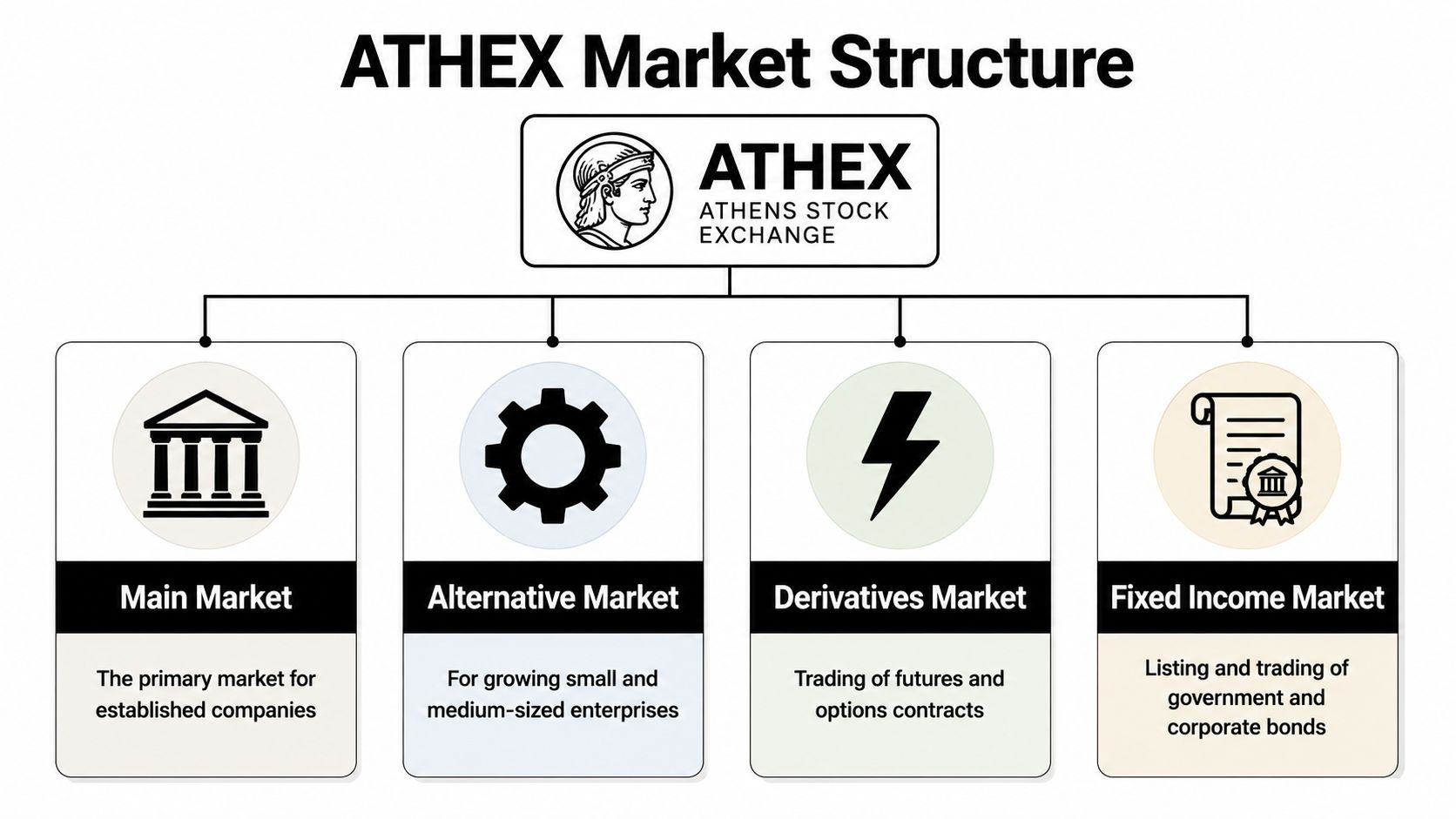

Deconstructing the ATHEX Market Structure

The Athens Stock Exchange is often described as if it were a single venue. It isn't. It is a layered market system designed to channel different forms of risk, capital, and disclosure into different segments. According to the Athens Stock Exchange overview, the exchange currently lists 172 stocks representing 166 companies across five markets: regulated securities, regulated derivatives, alternative, carbon (for EUAs), and OTC markets. It also operates from Athinon Avenue 110, Athens, Greece and remains a member of the Federation of Euro-Asian Stock Exchanges.

The exchange as a layered financing system

Think of ATHEX as a public financing ecosystem with distinct rooms rather than one trading floor.

The regulated securities market is the central room. It is where established listed companies access public equity capital under the highest level of formal listing discipline within the exchange structure. For policymakers, this segment matters because it offers the clearest window into how domestic corporate champions are valued by the market.

The regulated derivatives market serves a different function. It allows participants to hedge exposure, manage risk, and express views on future price movements. A derivatives venue can improve the efficiency of the broader market by allowing risk transfer rather than forcing all adjustment through spot selling.

The alternative market widens the funnel. It gives smaller or growing enterprises a pathway into public market financing that may be less burdensome than the main regulated segment. In practical policy terms, this matters for business scaling. A country that relies only on bank lending often constrains innovation and succession planning. A more varied market structure supports broader capital access, which is why debates on capital markets development should include secondary exchanges, not just headline indices.

A short way to read the remaining segments is this:

| Market segment | Policy relevance |

|---|---|

| Carbon market | Connects Greek market infrastructure to EU climate compliance mechanisms through EUAs |

| OTC market | Provides a venue for transactions that don't fit standard listed market channels |

Why structure matters for policy

A diversified exchange structure does more than organise trading. It allocates institutional attention. Different companies, instruments, and compliance obligations can be matched to different market environments rather than being forced into one model.

That has three policy implications.

- Capital formation becomes more flexible: Governments that want firms to rely less exclusively on bank credit need multiple market entry points.

- Risk management improves: Derivatives and OTC channels can absorb complexity that would otherwise destabilise cash-market pricing.

- EU policy transmission becomes more concrete: The presence of a carbon market shows how European climate architecture can be embedded inside domestic financial infrastructure.

ATHEX's structure also clarifies what the Athens stock market is not. It is not merely a scoreboard for listed shares. It is a national platform where financing, hedging, climate compliance, and private negotiation coexist under one institutional umbrella. That breadth is easy to overlook, but it is central to understanding why Athens matters for economic policy.

Navigating Trading Mechanics and Regulation

The strength of a stock exchange depends partly on what investors can see and partly on what they can't. Trading protocols, data distribution, and supervisory enforcement rarely dominate public discussion, yet they shape whether the market is investable for serious institutions.

Why market plumbing now matters more

According to Twelve Data's exchange profile for ASE, the exchange uses the Fast-FIX protocol for real-time data dissemination, offering latency significantly lower than the legacy IOCP feed through UDP Multicast transmission. The same reference notes the Europe/Athens timezone (EET, UTC+02:00) and the main trading window of 10:30–17:20. It also states that technical anomaly studies confirm price momentum strategies yield statistically significant returns in this market.

That information tells policymakers something important. Athens is no longer operating as a slow, secondary venue tolerated by long-only investors alone. Its technical design recognises that modern participation depends on reliable, low-latency information. For institutions running algorithmic strategies across European markets, feed quality and timing discipline are not side issues. They are part of market access.

A market can't broaden participation if its information architecture lags behind the practices of contemporary investors.

This doesn't mean policymakers should optimise the exchange for high-frequency activity above all else. It means they should understand that strong market infrastructure supports price discovery, liquidity provision, and cross-border integration. The debate on strengthening financial regulation for stability should therefore include market plumbing alongside capital rules and conduct oversight.

Regulation as a confidence technology

Regulation matters in Athens because history has made credibility expensive. The Hellenic Capital Market Commission sits at the centre of that credibility architecture. Its practical role is to protect investor confidence by enforcing transparency, market integrity, and orderly conduct across the trading environment.

A useful way to think about supervision in Greece is not as a brake on market development but as a precondition for it. In a market with crisis memory, investors won't separate growth stories from governance questions. If disclosure quality weakens, if enforcement appears selective, or if political signals cloud institutional independence, the penalty can be immediate.

For policymakers, the challenge is balance.

- Too little supervision undermines trust and raises the discount investors demand.

- Too much procedural friction can reduce market dynamism and discourage listings.

- Too much uncertainty about rules is worst of all, because it suppresses participation without delivering visible safeguards.

Athens therefore offers a clear lesson. Trading technology attracts attention because it improves execution. Regulation sustains confidence because it defines the fairness of that execution. A market needs both.

Analysing Recent Performance and Economic Drivers

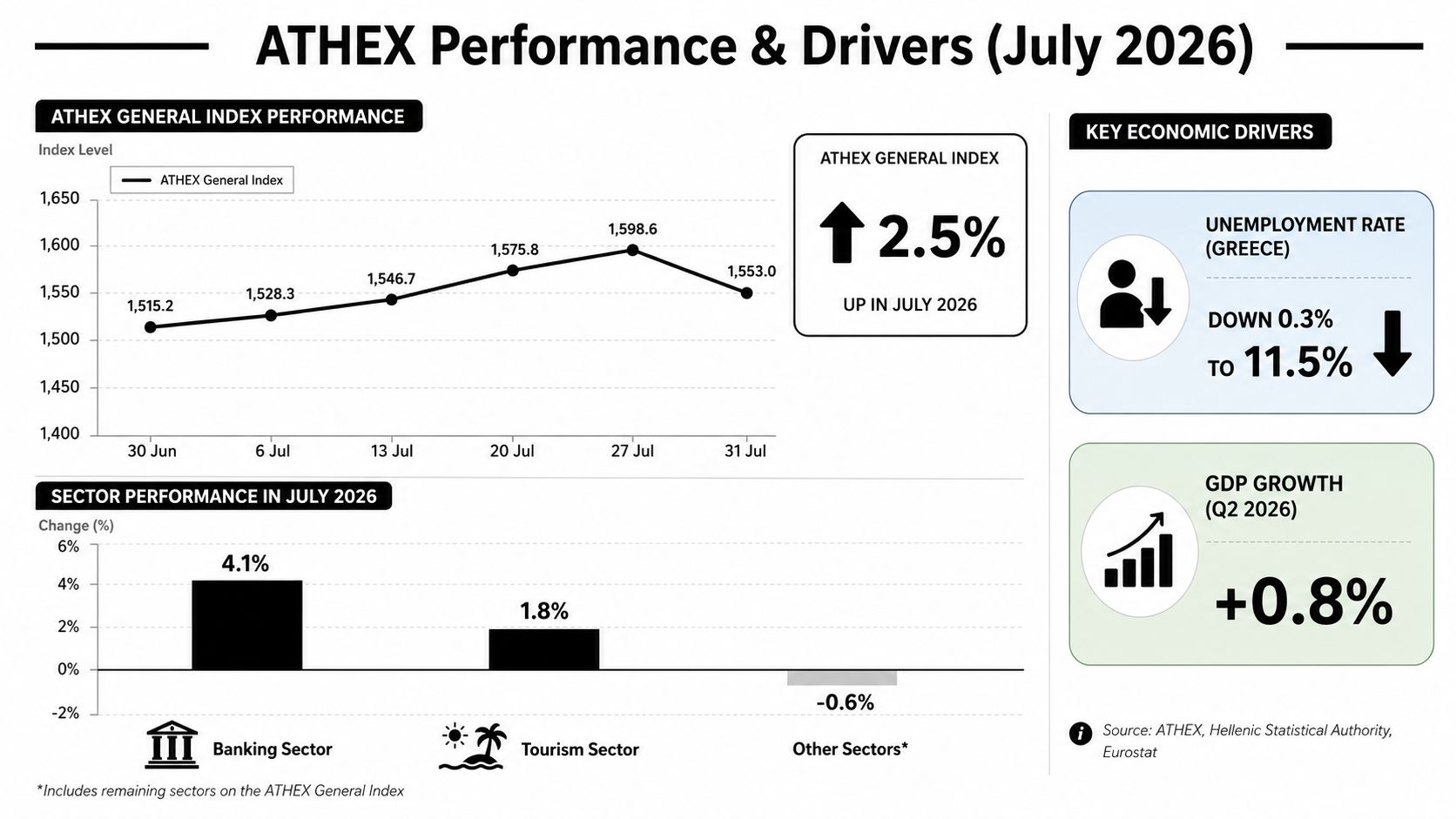

A return to the highest index level since 2009 is not a routine market move. As noted earlier, data from Trading Economics shows the Athens General Index reached 2,537 points in July 2026. For policymakers, that matters less as a headline than as a signal that investors are attaching a smaller discount to Greek assets than they did for much of the post-crisis period.

What the July 2026 rally signals

The strongest interpretation of the rally is not that Greece has completed its economic convergence with the Eurozone. It is that the market is pricing a lower probability of policy reversal, financial stress, and institutional fragility. Equity investors are effectively reassessing the interaction between domestic reform, corporate earnings capacity, and Greece's position inside the EU policy framework.

That repricing has macroeconomic consequences. A stronger equity market can improve firms' ability to raise capital, support balance-sheet repair, and reduce the reputational penalty that Greek issuers have long faced in international markets. In a bank-centered financial system, that shift is especially important because it broadens financing channels rather than relying only on credit expansion.

The more interesting point is political economy. When Athens trades closer to other European markets in valuation terms, the exchange begins to function as both a barometer and an instrument of policy integration. It rewards credible reform with lower perceived risk, but it also raises the cost of inconsistency. Governments then face a clearer transmission mechanism from fiscal discipline, regulatory quality, and investment policy into market pricing.

This video provides additional context on the Greek market.

Markets usually move before the full macroeconomic effects appear in national accounts data. That creates a useful but imperfect signal. Share prices can anticipate stronger investment and profitability, yet they can also reflect optimism that still depends on steady policy execution and favorable external conditions.

Why overvaluation warnings shouldn't be ignored

The same dataset points to a constraint. The estimated P/E ratio was 11.44 on 2 July 2026, above the 5-year average range of 7.56 to 11.11, a level Trading Economics characterizes as overvaluation. In practical terms, the market is no longer only rewarding recovery. It is pricing continued delivery.

That distinction matters because valuation expansion changes the policy stakes. If expectations are higher, setbacks carry a larger penalty. Slower reform implementation, weaker Eurozone growth, tighter financial conditions, or renewed domestic political uncertainty would affect an expensive market more quickly than a cheap one.

Strong market performance helps most when it supports investment, productivity, and reform credibility. It helps less when rising valuations create the impression that structural vulnerabilities have disappeared.

For Greece, the relevant question is therefore not whether the rally is justified in a narrow trading sense. The more important question is whether market gains are being converted into stronger capital formation, better corporate funding conditions, and more durable integration with European financial markets. If that conversion occurs, the Athens stock market becomes more than a recovery story. It becomes a measurable channel through which Greek policy credibility is tested and, at times, reinforced.

Systemic Importance for Greece and the European Union

The Athens stock market matters because it converts national policy choices into externally visible prices. That gives it systemic importance beyond its size. In Greece, the exchange helps determine whether businesses can raise capital outside the banking system, whether international investors view the policy environment as investable, and whether domestic reform is being rewarded with lower perceived risk. In the European Union, Athens serves as a practical test case for whether post-crisis governance can rebuild confidence inside a member state without fragmenting the wider financial order.

A domestic policy barometer

For Greek policymakers, the exchange is one of the clearest public scoreboards available. Bond markets often speak first about sovereign credibility. Equity markets add something different. They judge whether the corporate sector can grow under the policy framework the state provides.

That makes the exchange a policy barometer in at least three ways.

- Capital formation: When firms can tap equity markets credibly, they are less dependent on bank intermediation alone. That broadens the financing base for investment, expansion, and corporate restructuring.

- Reform validation: Rising market confidence can indicate that investors believe institutional reforms are durable rather than temporary responses to crisis pressure.

- Foreign capital signalling: International investors often interpret a functioning domestic equity market as evidence that legal, regulatory, and reporting systems are usable at scale.

These channels matter in a country where crisis management once overshadowed long-term allocation. Athens now has the potential to support a different model, one in which growth relies more on investable firms and less on recurrent emergency narratives.

Greece's exchange is most useful when it becomes boring in the best possible way: predictable, supervised, and trusted enough to support ordinary capital raising.

There is also a fiscal policy angle. A credible market doesn't directly solve sovereign vulnerabilities, but it can reduce the degree to which all national economic risk is concentrated in public balance sheet perceptions. The more investors can differentiate among Greek corporates, sectors, and business models, the less the entire economy is priced as one sovereign trade.

A Eurozone governance signal

For the European Union, Athens offers a narrower but strategically important lesson. Monetary union without convergent confidence is unstable. The Greek crisis exposed that reality starkly. The rebuilding of the Athens stock market suggests that institutional repair inside the Eurozone can, over time, restore private risk-taking where public distrust once dominated.

That has implications for European policy design. It reinforces the importance of consistent supervision, transparent markets, and cross-border capital participation. It also suggests that successful adjustment in one member state can strengthen the credibility of the wider union, especially when recovery takes place within common rules rather than outside them.

The sovereign dimension remains relevant here, particularly in any discussion of managing sovereign debt restructuring. Greece's market history shows that sovereign stress and equity market function can't be analysed separately for long. When state credibility weakens, the exchange suffers. When institutional confidence returns, the exchange can become one of the first domestic channels through which normalisation is priced.

This is why Athens should interest Eurozone policymakers even if they never invest in Greek equities. The exchange reveals whether European integration is operating as a theory or as a usable system. When a previously distressed member state can rebuild market credibility within the union's framework, that is not just a national success. It is evidence that common institutions can sustain recovery without erasing national market identity.

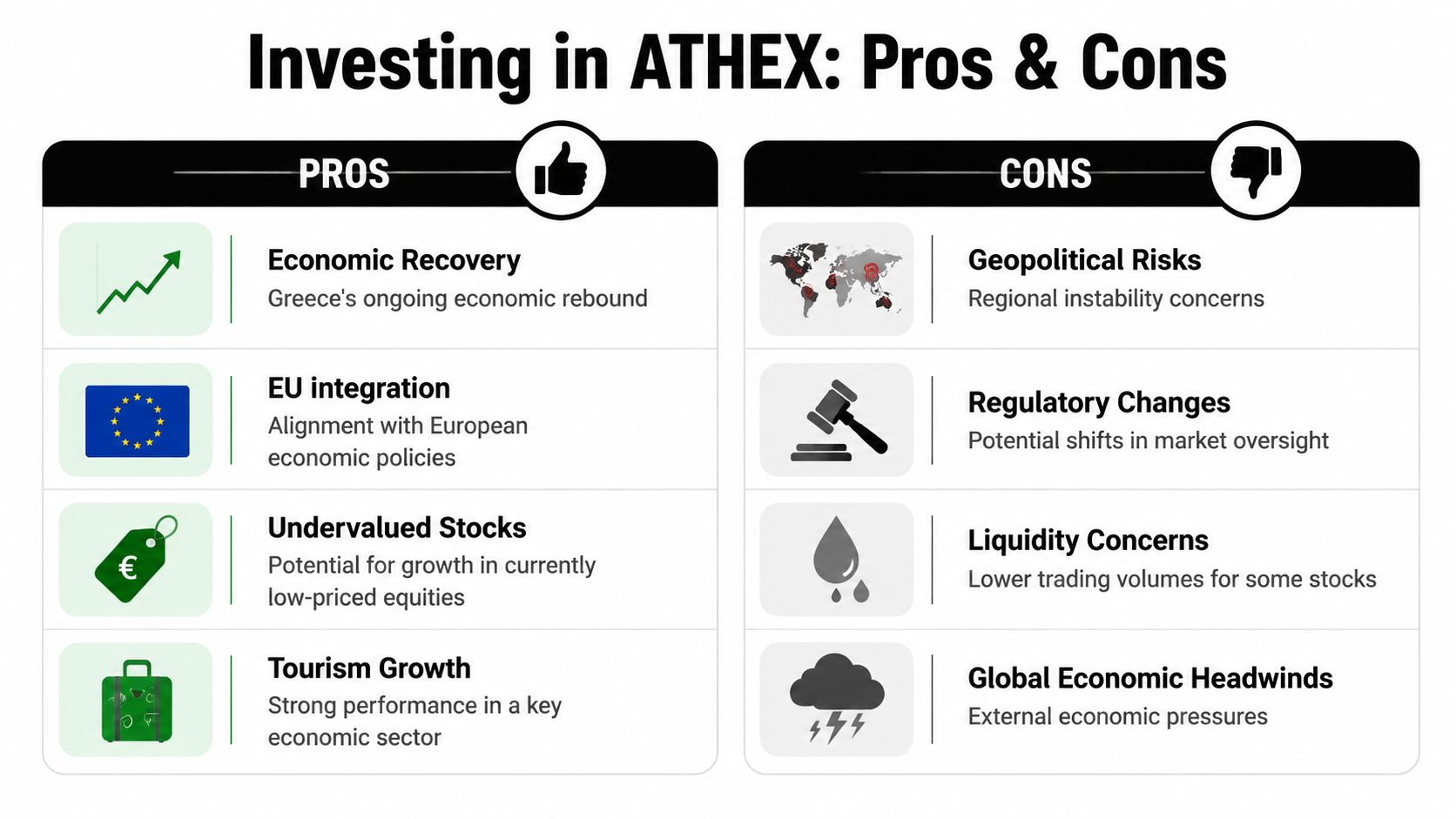

Investor Considerations and Future Prospects

Investor interest in Athens rests on a policy question as much as a valuation one. The exchange offers exposure to listed companies, but it also offers a real-time test of whether Greece can sustain growth, preserve fiscal and regulatory credibility, and translate EU membership into lower financing frictions for firms.

The case for opportunity

The opportunity case is strongest when Athens is viewed within the wider European policy framework. A market that spent years trading under sovereign stress is now being assessed more on corporate earnings, sector structure, bank balance-sheet repair, and investment execution. That shift matters because it changes how capital is priced. As macro risk premiums fall, company-level differentiation starts to matter more.

Three factors support that reading.

- Policy continuity: Investors tend to assign higher confidence to markets where tax, banking, and regulatory policy appear more predictable across electoral cycles.

- EU institutional anchoring: Membership in the Eurozone and the EU gives investors a rules-based framework for supervision, disclosure, and market access that is materially different from a standalone small market.

- Scope for company repricing: In a market that was long dominated by top-down risk, improving conditions can create room for stronger firms to attract attention on their own fundamentals.

For readers who want a practical primer on market basics before approaching smaller European exchanges, it's worth taking time to learn with Colibri Trader, particularly on how to think about risk management and entry discipline.

The case for caution

The main constraint is market depth. Athens can offer compelling stories, but thinner liquidity in parts of the market can distort price discovery, widen bid-ask spreads, and magnify short-term moves when international sentiment shifts. That makes position sizing, time horizon, and execution discipline more important than in larger Eurozone exchanges.

There is also a policy dimension to the risk. If reform momentum weakens, or if public policy becomes less predictable, the market can reprice quickly because foreign participation often reacts faster than domestic capital can offset it. This issue extends beyond portfolio allocation. It affects the cost of equity for Greek firms and, by extension, the economy's capacity to finance investment through private markets rather than bank credit alone.

A balanced comparison is set out below.

| Consideration | Opportunity reading | Risk reading |

|---|---|---|

| Valuation backdrop | Recovery can support further rerating if earnings and reforms hold | Higher expectations can amplify any disappointment |

| Policy environment | Continued institutional credibility can attract broader participation | Political or regulatory shifts can alter investor assumptions quickly |

| Regional setting | Greece's position in the Eastern Mediterranean can support long-term relevance | Geopolitical tension can raise the risk premium abruptly |

| Market depth | Focused investors may find under-researched companies | Lower liquidity can widen moves in both directions |

The medium-term outlook depends less on a single catalyst than on cumulative institutional performance. The central questions are whether Greece can maintain policy consistency, whether listed firms can convert improved sentiment into durable earnings and investment, and whether the exchange can broaden participation while preserving confidence in supervision.

For policymakers, that makes the Athens market more than a venue for equity trading. It is one channel through which Greece's integration into the European financial system is tested in practice.

Conclusion The Athens Market as a Policy Nexus

The Athens stock market now stands at a point where finance, national strategy, and European integration meet. Its recent strength signals renewed confidence, but its deeper significance lies elsewhere. It shows how a market shaped by crisis can become a working instrument of economic normalisation when institutions improve, trading infrastructure modernises, and investors believe policy commitments will endure.

Athens should therefore be read neither as a simple comeback story nor as a narrow specialist market. It is a policy nexus. It reflects whether Greece can sustain a transition from adjustment to investment, and whether the Eurozone can support recovery in a way that restores private confidence rather than merely containing public risk.

The next phase will be more demanding than the rally itself. Expectations are higher. Valuation discipline matters more. Supervisory credibility remains essential. If Greece manages that balance, the Athens stock market could become not just a symbol of recovery, but a durable mechanism for capital formation inside the European project.

For more analysis at the intersection of markets, public policy, and international cooperation, read and subscribe to Global Governance Media. It's a valuable resource for policymakers, analysts, and business leaders who need clear, evidence-based insight on the world economy and the institutions shaping it.