By Daniel Mercer

More than US$1 billion in financing has been enabled or optimised through the Entrepreneurial Finance Lab's work, according to Harvard's account of EFL. That figure matters not only because of scale, but because it points to a deeper institutional shift. Credit assessment no longer has to rely only on collateral, balance sheets, and formal borrowing histories.

For policymakers, that changes the frame. The central issue isn't whether one fintech tool can improve loan screening at the margin. It's whether governments, development finance institutions, and G20-aligned agencies are prepared to treat alternative underwriting as public-interest infrastructure for inclusive growth, especially where viable firms remain invisible to conventional banking systems.

The Entrepreneurial Finance Lab, usually referred to as EFL, deserves attention in that light. It is best understood not as a lender, and not merely as a start-up success story, but as an early and influential model for assessing entrepreneurial potential when standard credit files are thin or absent. That makes it relevant well beyond the markets where it first gained traction. For officials working on SME policy, financial inclusion, industrial strategy, or blended finance, EFL offers a practical example of how behavioural data can be translated into lending decisions without abandoning rigour.

This is also why EFL belongs in broader debates on state capacity and development delivery. The procurement of financial infrastructure, the design of public-private partnerships, and the setting of data governance standards all influence whether tools like this expand opportunity or remain isolated pilots. The strategic question is no longer whether alternative data exists. It's whether institutions can govern its use responsibly and at scale. That wider policy context sits at the heart of current debates on financing development strategies.

Table of Contents

- Introduction The Global Credit Gap and a New Frontier

- From Harvard Research to Global Impact

- The Science of Psychometric Credit Scoring

- Evidence of Impact and Global Case Studies

- Policy Implications for Global Governance

- Engagement and Evaluation Pathways

Introduction The Global Credit Gap and a New Frontier

The development challenge is often described as a shortage of capital. In practice, it is just as often a shortage of legible information. Banks can't lend confidently when they can't observe repayment signals, and many entrepreneurs can't generate those signals because they've never had access to formal finance in the first place.

That circular problem has defined SME finance for years. It has also encouraged a narrow view of risk, one that overweights documentation and underweights entrepreneurial capability. The result is not only exclusion. It is misallocation. Economies leave productive activity underfinanced because institutions cannot see it clearly enough to price it.

A methodological shift in credit assessment

EFL entered this gap with a different premise. Instead of treating the absence of credit history as the end of the underwriting conversation, it asked whether other indicators could help lenders distinguish between high-potential and high-risk borrowers. The answer, developed through research and later deployment, was psychometric credit scoring.

That concept matters because it moves underwriting closer to behaviour. Rather than relying solely on what an applicant already owns or has previously borrowed, the model looks at traits and responses that may signal repayment capacity and business discipline. For policymakers, the significance is strategic. A state that wants more inclusive enterprise finance needs methods that can work before a firm becomes fully documented, not only after.

Practical rule: When a market has many capable but undocumented borrowers, better underwriting is often more valuable than larger subsidy pools.

Why policymakers should care now

This is especially relevant for governments and multilaterals trying to make public finance catalytic rather than merely compensatory. If institutions can identify excluded but credible borrowers more effectively, guarantees, credit lines, and technical assistance become sharper tools. They can target market failures with more precision instead of absorbing risks that were poorly understood from the outset.

The Entrepreneurial Finance Lab also sits at the intersection of several policy agendas that are often treated separately:

- Financial inclusion: expanding access for borrowers without conventional credit files.

- SME development: improving capital allocation to firms that can generate jobs and resilience.

- Digital governance: setting standards for data use, accountability, and consent.

- State effectiveness: embedding better screening tools into publicly supported finance programmes.

The policy opportunity is therefore broader than fintech adoption. It is about whether public institutions can integrate non-traditional risk assessment into the architecture of development finance without compromising fairness or oversight.

From Harvard Research to Global Impact

Research institutions rarely produce tools that change credit operations across multiple markets. EFL did, and that origin matters for public decision-makers assessing whether it belongs inside development finance programmes or procurement pipelines.

The Entrepreneurial Finance Lab began as a Harvard Kennedy School research effort led by Asim Khwaja and Bailey Klinger. It was later formalised as a private company. The sequence is important. EFL was not created as a generic fintech product looking for a market. It was developed around a defined policy and banking problem: lenders needed a disciplined way to evaluate entrepreneurs who lacked the paperwork required by conventional underwriting.

That starting point gave EFL an unusual position in the field. Many financial technologies adapt an existing workflow to reduce cost or speed up approval times. EFL addressed a prior constraint. In large parts of the SME market, banks could not price risk well enough to lend at all. For ministries of finance, development banks, and multilateral agencies, that distinction has practical consequences. A tool that expands the assessable borrower pool can change how public credit lines, guarantee schemes, and SME facilities are designed, not just how fast applications move.

Its wider significance is institutional.

EFL helped establish that non-traditional borrower assessment could move from academic testing into bank practice without abandoning the discipline of credit screening. That made it relevant beyond the narrow question of one firm's growth. It offered an early proof point that inclusion and underwriting quality do not need to sit in opposition if the assessment method is built for operational use by lenders.

Three strategic lessons follow from that history:

- Procurement should focus on use case, not branding. Public institutions should treat EFL less as a startup success story and more as a validated underwriting approach that can be procured, adapted, or embedded within broader SME finance programmes.

- Partnership design matters as much as the scoring tool. The strongest applications are likely to come through arrangements that combine banks, DFIs, technical assistance providers, and regulators, rather than stand-alone software purchases.

- Policy integration determines development value. The biggest gains come when alternative screening is tied to public objectives such as women-owned business finance, first-loss guarantee targeting, agricultural SME lending, or post-crisis enterprise recovery.

This helps explain EFL's lasting influence on later debates about alternative underwriting. Its contribution was methodological and institutional. It showed that lenders and policymakers could treat previously excluded borrowers as assessable subjects of formal finance rather than residual cases for subsidy or informal lending channels.

For G20 governments and multilateral institutions, the forward-looking question is no longer whether psychometric underwriting was novel. It is whether tools in this category can be incorporated into public finance architecture with clear standards for procurement, validation, consumer protection, and accountability. EFL's trajectory matters because it provides an early model for doing exactly that.

The Science of Psychometric Credit Scoring

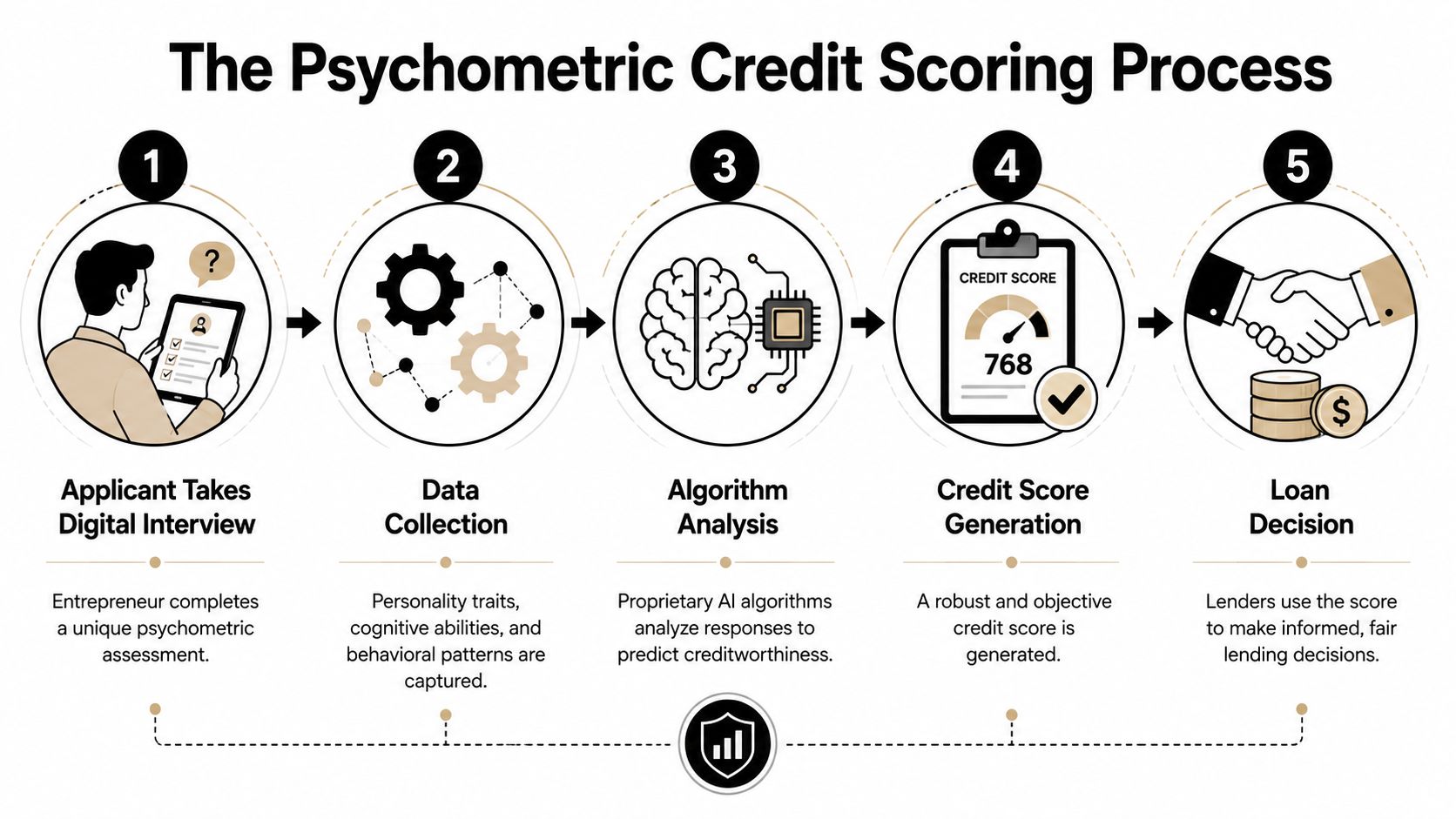

Psychometric credit scoring sounds abstract until you translate it into operational terms. A useful way to think about it is as a structured digital interview designed to reveal borrower characteristics that ordinary financial documents may miss.

Instead of asking only what assets an entrepreneur owns or what formal loans they have repaid, the system asks whether measurable behavioural traits can help predict repayment. That is the conceptual leap. It doesn't eliminate finance. It supplements finance where data scarcity would otherwise force lenders to reject applicants wholesale.

What EFL actually measures

Harvard's description of EFL states that the primary innovation is the use of psychometric tests measuring traits such as ethics, character, intelligence, attitudes, and beliefs to predict loan repayment, as noted in Harvard's discussion of EFL's approach. For a policymaker, the key point is that these are not random personal details gathered for curiosity. They are inputs intended to improve risk assessment where standard files are absent or weak.

The Entrepreneurial Finance Lab differs from many later conversations about “alternative data”. Some alternative-data models focus heavily on digital exhaust, such as transaction traces or platform activity. EFL's model is more deliberately behavioural. It seeks evidence about the applicant as an entrepreneurial actor, not only as a data subject.

A simplified process looks like this:

- Assessment completion: the entrepreneur answers a structured digital questionnaire.

- Trait capture: the system records patterns related to decision-making, consistency, and behavioural indicators.

- Analytical interpretation: algorithmic tools analyse response patterns to estimate likely repayment performance.

- Score generation: lenders receive an output that can inform approval, rejection, or further review.

A short overview of the concept is embedded below.

Why this matters for lenders and regulators

Harvard's account also notes that the approach has been implemented in dozens of countries to expand credit access to many thousands of entrepreneurs who might otherwise have been excluded from formal finance. It further notes that EFL's tools were designed to help banks in developing markets score business-loan applicants. That combination is important. It tells policymakers that the innovation sits inside institutional lending workflows rather than outside them.

This has two implications.

First, psychometric scoring should be understood as complementary underwriting. It is most valuable where collateral records, audited statements, and bureau data are missing or partial. Regulators don't have to treat it as a replacement for every existing method. They can treat it as an additional instrument in a broader risk toolkit. That makes policy integration easier.

Second, the governance challenge isn't whether such tools are legitimate in principle. It is whether authorities can set the rules that make them trustworthy in practice. That includes consent standards, bias testing, appeals processes, and supervision of model use. These are issues that belong within wider debates about fintech and digital opportunities beyond finance, especially as governments build digital public infrastructure and rethink how data contributes to development outcomes.

Psychometric scoring works best when institutions define clearly where it fits. It should inform judgement, not replace accountability.

Evidence of Impact and Global Case Studies

More than US$1 billion in financing has been enabled or optimised through EFL's model, according to Harvard's summary of Entrepreneurial Finance Lab. For policymakers, that figure matters less as a headline than as evidence that psychometric underwriting moved beyond academic promise into bank and market practice.

The strongest case for EFL is cumulative adoption. Harvard's account links the model to use across dozens of countries and to expanded credit access for many thousands of entrepreneurs. That combination suggests operational relevance in varied institutional settings, which is a higher bar than a successful pilot inside a single lender. For G20 governments, multilateral development banks, and DFIs, the strategic question is not whether one fintech tool produced an eye-catching result. It is whether a method can be procured, governed, and adapted across jurisdictions with very different data constraints.

What the evidence supports, and what it does not

The available record supports three conclusions with confidence.

First, EFL achieved scale that public institutions should notice. The financing volume associated with the model indicates that lenders used it in real credit allocation, not only in controlled tests.

Second, the model proved exportable. Use across many countries points to a form of institutional portability, which is especially relevant for multilaterals that need tools capable of fitting multiple banking systems and supervisory environments.

Third, the impact claim is strongest at the system level. The evidence shows that EFL helped widen the set of borrowers who could be assessed by formal lenders.

The record is thinner on a different question. It does not provide a standardised, lender-by-lender archive of outcomes that would allow policymakers to compare delinquency, approval, and profitability across every deployment. That limitation should shape how ministries and development institutions use the evidence. EFL should be treated as a credible market-building instrument with demonstrated adoption, not as a universal template that can bypass local evaluation.

The policy value lies in repeatable institutional use across markets, not in a single celebrated case.

Traditional vs EFL psychometric credit scoring

A direct comparison clarifies why this matters for development finance strategy.

| Criterion | Traditional Credit Scoring | EFL Psychometric Scoring |

|---|---|---|

| Primary inputs | Formal credit history, collateral records, financial statements | Psychometric assessments of ethics, character, intelligence, attitudes, and beliefs |

| Best suited to | Applicants with established formal financial footprints | Applicants with limited or no conventional credit history |

| Institutional role | Core tool of mainstream underwriting | Complementary tool for thin-file or excluded borrowers |

| Policy value | Supports mature credit markets | Expands the assessable borrower pool in under-documented markets |

| Strategic limitation | Can exclude viable firms that lack records | Requires governance around fairness, transparency, and proper use |

The comparison has a practical implication for public procurement. Institutions should not buy this category of tool as a generic innovation product. They should procure it against a defined policy problem, such as SME lending in thin-file markets, state-backed credit programmes targeting informal firms, or DFI-supported bank transformation efforts. That framing changes the evaluation criteria. Interoperability with existing underwriting, auditability, and supervisory comfort become as important as predictive performance.

What global case experience means for DFIs and G20 policymakers

EFL's documented spread across markets carries a lesson that goes beyond the company itself. In development finance, capability constraints inside lenders often matter as much as funding shortages. A guarantee facility or credit line cannot reach intended firms if banks lack a credible way to assess them. Psychometric scoring addressed that bottleneck in settings where conventional data were weak.

This is why the case matters for multilateral institutions. It points to a partnership model in which public actors do more than subsidise risk. They can also strengthen underwriting infrastructure through technical assistance, results-based procurement, and common standards for testing fairness and performance. For G20 members shaping international financial inclusion agendas, that is the more consequential insight. Credit innovation should be integrated into financial sector policy as operational capacity, not treated only as startup experimentation.

The absence of flashy case storytelling is also instructive. Policymakers are often presented with vendor claims built around one bank, one country, and one short time horizon. EFL's history suggests a better screening test for public adoption. Officials should ask whether a model can survive institutional reality, fit procurement rules, and generate enough confidence for repeated use across different markets. Those are the conditions under which a private innovation becomes relevant to development strategy.

Policy Implications for Global Governance

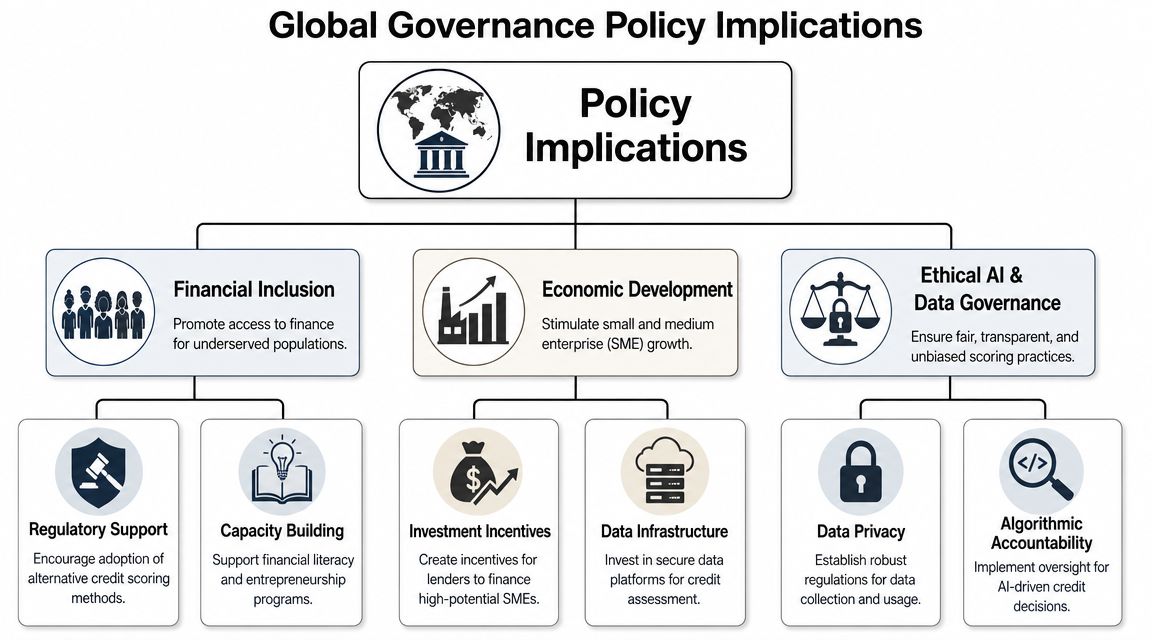

If EFL were only a niche fintech product, it would sit mainly with bank innovation teams. It does not. It has implications for sovereign financial inclusion strategies, DFI portfolio design, and multilateral approaches to private-sector development.

The reason is simple. Credit assessment is a gatekeeping function. Whoever defines bankable risk influences which firms grow, which communities remain underfinanced, and how effectively public money mobilises private capital. Methods that widen the set of assessable borrowers therefore carry governance consequences, not just commercial ones.

Why multilateral institutions should treat this as infrastructure

Multilateral institutions often focus on the visible parts of SME finance, such as lines of credit, guarantees, and investment vehicles. Those matter, but they depend on a quieter layer underneath. Lenders need tools to sort applicants intelligently. Without that layer, public finance either fails to reach intended firms or overcompensates through blunt de-risking.

An EFL-type model can help institutions think more strategically about market-building. The question becomes not only “how much liquidity should we provide?” but also “what underwriting capability does the market lack?” In many settings, that capability gap is exactly where public intervention can be catalytic.

A practical framework for multilateral use would include:

- Procurement of scoring capability: selecting tools that can integrate with local lenders rather than creating parallel channels.

- Partnership design: pairing technology providers with banks, guarantee agencies, and technical assistance facilities.

- Standards setting: requiring clear rules on consent, explainability, and recourse.

- Learning systems: funding evaluations that examine not just disbursement, but portfolio composition and inclusion effects.

Where G20 governments can act now

For G20 governments, the relevance is somewhat different. Many already have developed financial sectors. Their challenge is often policy integration. How should ministries, regulators, and public development banks incorporate alternative underwriting into national growth strategies without weakening consumer protection or supervisory discipline?

A sensible answer has four parts.

First, recognise alternative underwriting as economic infrastructure. If SME growth is a priority, then the systems that identify viable firms deserve policy attention just as much as guarantee schemes or public credit registries.

Second, embed these tools in public programmes carefully. State-backed SME facilities and development banks can test psychometric approaches in segments where conventional files are especially weak, while maintaining human review and documented appeal mechanisms.

Third, use procurement to shape market quality. Public contracts can require transparency about model governance, local implementation support, and evidence that the tool complements formal finance rather than substituting for responsible underwriting.

Fourth, align with ethical AI governance. Alternative scoring enters politically sensitive territory because it affects access to opportunity. Regulators should insist on oversight structures that examine discrimination risks, data minimisation, and institutional accountability.

The strategic value of an underwriting innovation depends as much on governance as on analytics.

For global governance forums, that means EFL is best treated as an early example of a wider category: tools that convert non-traditional information into formal economic participation. Such tools can help advance inclusive growth agendas, but only if public institutions decide that underwriting quality is a development priority in its own right.

Engagement and Evaluation Pathways

Public officials don't need to start with a national rollout. They need a disciplined entry point. The best approach is usually a bounded partnership with clear governance terms, a defined target segment, and an evaluation plan agreed before implementation begins.

Procurement choices that shape outcomes

A DFI or ministry considering an EFL-inspired solution should begin with procurement design, not technology enthusiasm. The most important choices are institutional.

- Define the use case first: Is the priority microenterprise lending, early-stage SME finance, or underserved borrower segments within existing bank portfolios?

- Select implementation partners carefully: Banks, public development banks, guarantee entities, and technology providers should each have explicit responsibilities.

- Write governance into the contract: Requirements should cover consent, data handling, audit access, model monitoring, and decision review processes.

- Insist on operational fit: A scoring tool must work inside lending workflows. If staff can't use it, pilot results won't translate into durable capability.

Officials looking at entrepreneurship systems more broadly should also connect underwriting reform with wider policies that support firm creation and growth, including the ecosystem questions discussed in facilitating entrepreneurship.

How to evaluate beyond loan volume

Loan volume is the weakest single measure of success. A programme can disburse aggressively and still fail on inclusion, portfolio quality, or institutional learning. Evaluation should ask a better set of questions.

- Who entered the pipeline? Did the programme identify borrowers who would otherwise have been screened out?

- How did lenders use the score? Was it decisive, advisory, or ignored in practice?

- Did institutional behaviour change? Did partner banks adapt their underwriting frameworks or treat the tool as a temporary pilot?

- Were safeguards credible? Could borrowers understand the process and challenge adverse decisions where appropriate?

- What capability remained after the pilot? Lasting value often lies in improved underwriting systems, not only in the first round of approvals.

A useful pilot therefore does two things at once. It expands access for real firms and generates operational evidence that ministries, DFIs, and regulators can use in future policy design. That is the threshold leaders should set. The purpose isn't to buy innovation theatre. It's to build financing systems that can recognise entrepreneurial potential earlier, more fairly, and with greater confidence.

Explore more policy analysis, expert commentary, and practical multilateral insights with Global Governance Media. If your institution is rethinking SME finance, digital governance, or inclusive growth strategy, use this moment to assess where alternative underwriting can strengthen your next programme, partnership, or procurement decision.