By Daniel Mercer

The United Kingdom's latest climate finance pledge offers a sharp way to answer a deceptively simple question: what is climate finance? London has announced approximately £6 billion for 2024 to 2027, a commitment that Carbon Brief's analysis says is effectively half of the previous £11.6 billion pledge when inflation and reporting changes are taken into account. That isn't just a budget story. It shows that climate finance is a strategic instrument of statecraft, development policy and economic transition.

For G7 and G20 ministers, climate finance isn't a niche environmental topic. It is the machinery through which governments shape energy systems, resilience investment, industrial competitiveness and diplomatic credibility. The central policy question isn't whether finance matters. It's how to organise it so public money lowers risk, private capital scales deployment, and institutions can prove that commitments translate into real-world outcomes.

Table of Contents

- Defining the Scope of Climate Finance

- Public Versus Private Finance Flows

- The Policymakers Toolkit of Financial Instruments

- Key Institutions Shaping Global Capital Flows

- Tracking Finance and Measuring Real Impact

- Confronting the Finance Gap and Shifting Trends

- Mobilising Trillions for the G7 and G20 Agendas

Defining the Scope of Climate Finance

Climate finance is the deployment of capital toward activities that reduce emissions, strengthen resilience or support the institutions needed to do both. In policy terms, it sits at the centre of Paris alignment because it determines whether national ambition is backed by actual investment decisions. A pledge only matters if it changes what gets built, who bears risk, and how quickly economies can shift.

That definition is broader than many ministers use in practice. It includes not only headline international pledges, but also domestic public expenditure, development finance, lending structures, guarantees, and investment frameworks that direct private money into clean infrastructure and adaptation. It covers mitigation and adaptation, but also the less visible work of planning, data systems and implementation capacity.

Why the definition matters for ministers

Governments often treat climate finance as a reporting category. That's too narrow. It is better understood as an allocation system for scarce fiscal space, concessional resources and investor confidence. Once framed that way, the strategic choices become clearer.

- Public leaders decide priorities: They determine whether scarce concessional funding supports resilience, energy access, industrial upgrading or nature-related programmes.

- Financial institutions translate policy into instruments: They package risk and return in forms that projects can absorb.

- Private actors decide scale: They provide the depth of capital markets that public balance sheets can't match on their own.

Practical rule: If a climate commitment doesn't alter capital allocation, risk pricing or project viability, it isn't yet functioning as climate finance.

The UK's own policy architecture illustrates how climate finance evolves over time. Its International Climate Finance programme began in 2011, with ICF1 at £3.9 billion from 2011/12 to 2015/16, followed by ICF2 at £5.8 billion from 2016/17 to 2020/21, and ICF3 at £11.6 billion from 2021/22 to 2025/26, according to the Center for Global Development's review of UK climate finance results. That progression shows how climate finance becomes embedded in state budgeting and external policy, rather than remaining a one-off diplomatic commitment.

A second reason the definition matters is that it shapes the policy mix. Adaptation projects, for example, often need a different financing structure from revenue-generating renewable power assets. Ministers who want effective climate change mitigation strategies need to distinguish between projects that can attract commercial finance and those that will continue to require grants or concessional support.

Four questions that clarify what climate finance is

A useful ministerial test is to ask four questions:

- Who provides the money? Governments, development banks, national institutions, corporates and institutional investors all play different roles.

- What form does it take? Grants, loans, guarantees and bond issuance each solve a different problem.

- Who manages allocation? Institutions matter because governance shapes speed, access and credibility.

- How is impact measured? Tracking determines whether political promises survive contact with implementation.

Climate finance, then, is not just money for climate. It is the financial architecture through which climate goals become investable public policy.

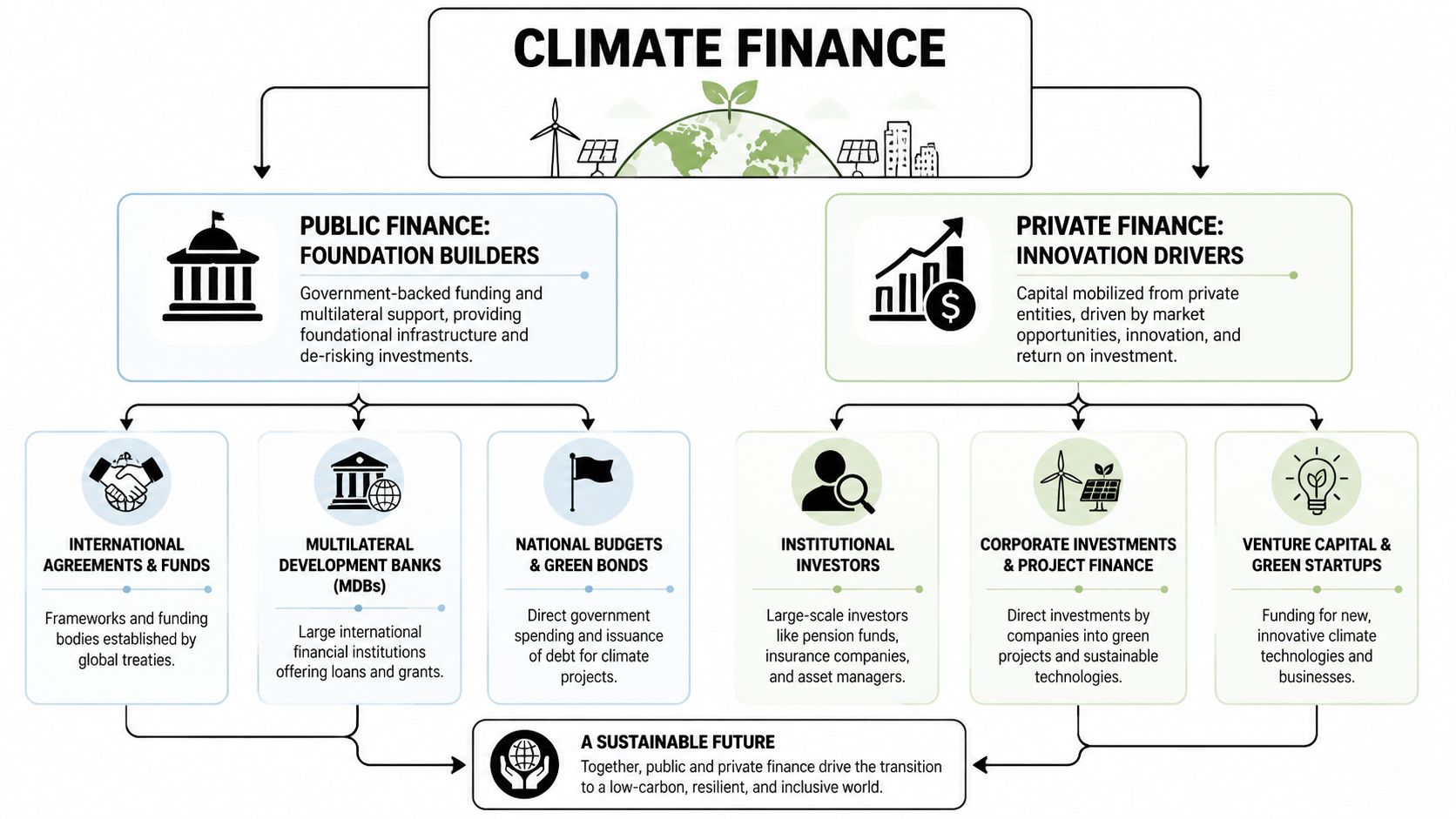

Public Versus Private Finance Flows

The most useful way to understand climate finance flows is to think of public finance as seed capital and private finance as growth capital. The first builds confidence, absorbs early risk and establishes rules. The second expands deployment once a project, technology or market can offer an acceptable risk-return profile.

What public finance actually does

Public climate finance is policy-driven. Governments and multilateral institutions use it to pursue outcomes that markets alone won't reliably deliver. That includes adaptation, capacity building, concessional infrastructure, first-loss positions and technical assistance.

In practical terms, public finance performs three jobs.

- It lowers risk: A guarantee, junior tranche or concessional loan can make a difficult project bankable.

- It creates markets: Public procurement, national development plans and regulatory reform can establish demand where none existed.

- It protects public goods: Resilience, ecosystem protection and community adaptation often generate social returns that commercial investors can't fully monetise.

This is why G20 debates about fiscal constraints matter so much. When public budgets tighten, the pipeline of bankable climate investment can weaken long before private investors visibly step back.

What private finance looks for

Private climate finance is commercially driven. Investors, banks, insurers and asset managers assess whether expected returns compensate for policy risk, technology risk, currency exposure and execution risk. If those factors remain unresolved, capital stays on the sidelines.

That doesn't make private actors reluctant participants. It means their participation is conditional on policy credibility. Ministers who want to accelerate mobilisation need to design environments where investors can price risk with confidence. That is the logic behind efforts focused on facilitating private sector investment.

Public money works best when it is disciplined, targeted and temporary. It should crowd capital in, not permanently substitute for it where commercial models can function.

The strategic relationship between the two

The public-private distinction is often framed as a contest. In reality, it is a sequencing problem. Public capital goes first where uncertainty is highest. Private capital scales once project structures become investable.

A ministerial view of the relationship looks like this:

| Flow type | Core motivation | Best suited to | Main policy challenge |

|---|---|---|---|

| Public finance | Development, resilience and treaty commitments | Early-stage markets, adaptation, de-risking, public goods | Limited fiscal space and competing priorities |

| Private finance | Risk-adjusted return | Mature technologies, scalable infrastructure, operating assets | Unclear pipelines, unstable regulation, currency and policy risk |

Expecting private finance to do the work of public finance is a policy error. Investors can scale assets. They can't replace governments in funding fragile public goods or underwriting political uncertainty. G7 and G20 strategies need both engines working in tandem.

The Policymakers Toolkit of Financial Instruments

Ministers rarely need more slogans about mobilisation. They need to know which instrument solves which problem. Climate finance packages fail when governments apply the wrong financial tool to the wrong policy objective.

Grants and concessional loans

Grants are the purest form of concessional support. They are most effective where a project delivers strong social or resilience benefits but weak direct cash flow. That makes them suitable for adaptation planning, institutional capacity, community resilience and preparation work that enables larger downstream investments.

Concessional loans sit one step closer to commercial finance. They still reduce financing pressure, but they preserve some expectation of repayment and financial discipline. For many sovereign and sub-sovereign borrowers, concessional loans can support infrastructure that has long-term value but doesn't yet attract affordable market borrowing.

A practical distinction helps. Use grants when the priority is public benefit without revenue certainty. Use concessional loans when the project has an economic rationale but still needs softer terms to proceed.

Guarantees and risk-sharing tools

Guarantees matter because many climate projects fail long before construction, not because the asset is uneconomic, but because someone cannot absorb the relevant risk. That could be policy instability, payment uncertainty or counterparty weakness.

A guarantee doesn't directly pay for the entire project. It changes who bears selected risks. That can be enough to enable senior debt, attract institutional investors or improve terms for local lenders.

For ministers, guarantees are among the most underused tools in the climate finance arsenal because they preserve fiscal resources while expanding confidence. They work best when policy teams clearly identify the binding risk and target the guarantee narrowly.

The question isn't whether a project needs support. The question is which specific risk is stopping capital from moving.

Green bonds and structured finance

Green bonds give governments, development banks and companies a way to raise debt linked to eligible environmental uses. Their policy value lies in signalling and market development as much as in volume. A credible green bond framework can standardise project pipelines, improve reporting discipline and widen the investor base.

Structured finance matters when policymakers need to combine instruments. A blended package may use grants for preparation, concessional debt for construction and guarantees for political or payment risk. This is often the difference between an announced priority and an executable project.

The policy lesson is straightforward. Climate finance isn't one instrument. It is a portfolio approach in which each tool absorbs a different part of the problem.

Comparison of Key Climate Finance Instruments

| Instrument | Primary Purpose | Typical Use Case | Leverage Potential |

|---|---|---|---|

| Grant | Fund public goods and early-stage capacity where repayment is unrealistic | Adaptation planning, technical assistance, community resilience, project preparation | Indirect but important, especially in building pipelines |

| Concessional loan | Reduce financing costs for projects with economic value but limited commercial bankability | Public infrastructure, transition investments, long-horizon assets | Moderate, especially when paired with policy reform |

| Guarantee | Shift specific risks away from private lenders or investors | Projects facing political, payment or counterparty risk | High when risk is clearly defined |

| Green bond | Raise debt for climate-aligned investment under an identifiable framework | Sovereign programmes, public agencies, corporate clean investment portfolios | Strong for market deepening and scaling repeat issuance |

The most effective climate finance ministries don't ask which instrument is best in the abstract. They ask which instrument best matches the project's cash flow profile, developmental value and risk distribution. That same logic sits behind proposals for an SDR bond for climate finance, where the central challenge is not solely volume, but how to convert official resources into scalable and credible structures.

Key Institutions Shaping Global Capital Flows

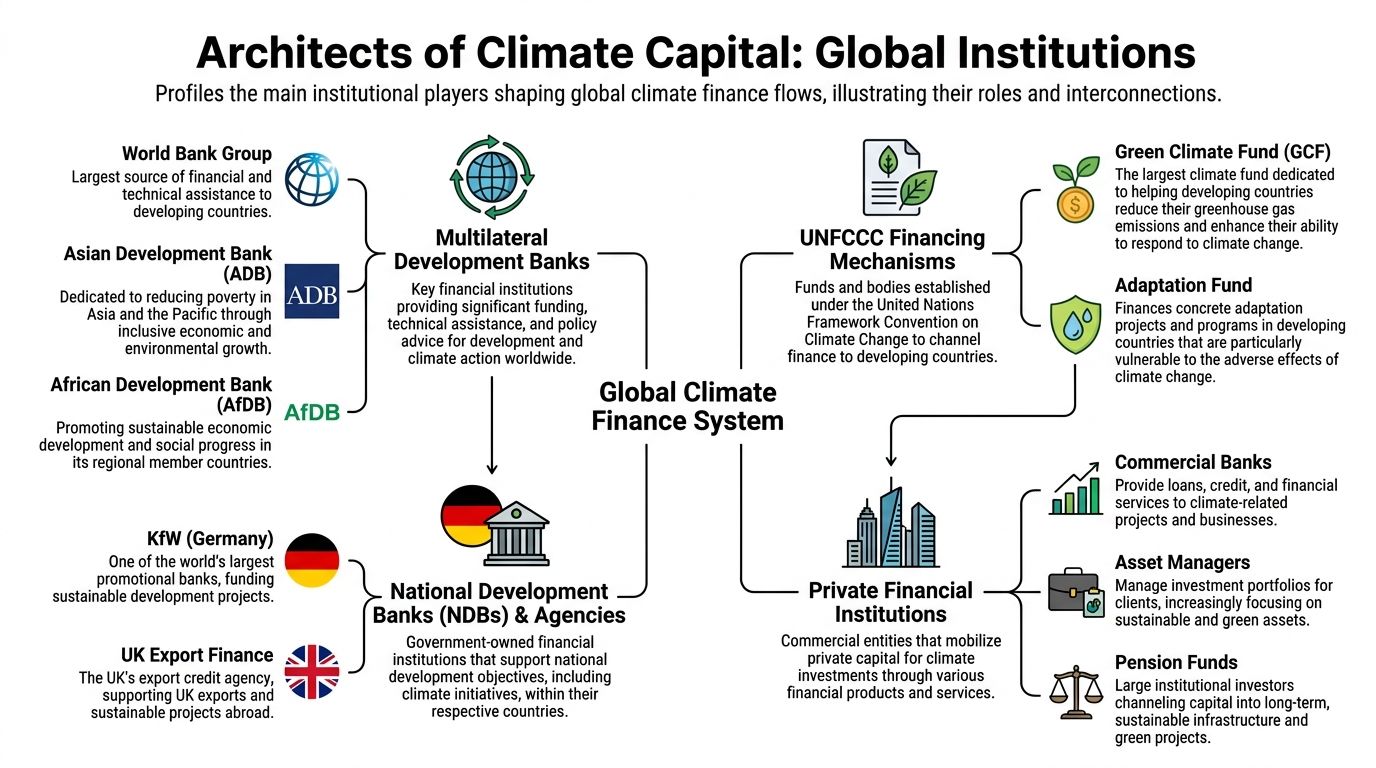

Public international finance still shapes the terms on which much larger pools of capital move. For G7 and G20 ministers, that makes institutional design a macroeconomic and geopolitical question, not an administrative one.

Multilateral and UN-linked institutions

Multilateral development banks sit at the centre of cross-border climate capital flows because they combine three functions few others can perform together. They provide long-tenor finance, shape policy reform through country dialogue, and set due diligence standards that private investors often treat as a market signal. For ministers, MDBs matter because they can turn political commitments made in G7 and G20 communiques into investable national programmes.

Their influence extends beyond their own balance sheets. An MDB-backed power sector reform, city transport programme, or transmission package can reduce policy uncertainty for years. That changes the risk-return profile faced by pension funds, insurers, and commercial banks. In practice, institutions that appear technical often determine whether private capital enters early, late, or not at all.

UNFCCC-linked funds, including the Green Climate Fund and the Adaptation Fund, play a different role. They channel climate-specific resources with stronger treaty legitimacy and a clearer focus on vulnerable countries, adaptation, and concessionality. That function is politically important. It helps preserve trust in the international climate regime, especially where recipient governments judge mainstream development finance to be too slow, too debt-creating, or insufficiently responsive to loss, vulnerability, and local access constraints.

National institutions and bilateral programmes

National development banks and bilateral agencies convert broad international pledges into country and sector decisions. They can align climate finance with industrial policy, export strategy, technology partnerships, and diplomatic priorities more directly than large multilateral platforms.

The UK's International Climate Finance programme illustrates the scale and reporting logic of a bilateral platform. The UK government reports programme results across adaptation, clean energy access, emissions reductions, and mobilised private finance through its official results publications on UK International Climate Finance results. For policymakers, the institutional lesson is not only that bilateral channels can produce measurable outcomes over multiple spending cycles. It is that bilateral programmes can be used to test models, build sector pipelines, and prepare projects that larger institutions or private financiers can later expand.

That is also why results systems matter. Officials designing climate finance vehicles increasingly need fluency in delivery frameworks, indicators, and attribution rules. For teams building that capability, understanding RBM for MDB careers helps explain how multilateral institutions assess performance and implementation credibility.

Why institutional design affects outcomes

Institutional choice affects speed, concessionality, risk allocation, and political ownership. Those differences shape outcomes as much as the volume of money committed.

- MDBs suit large infrastructure, policy reform, and transactions that need sovereign engagement, procurement discipline, and repeated co-financing.

- UN-linked climate funds suit areas where grant intensity, adaptation focus, and legitimacy in the UN process carry greater weight.

- Bilateral programmes suit strategic sectors, first-loss experimentation, and country partnerships linked to wider economic or foreign policy objectives.

- Private financial institutions matter most where regulation, contract enforcement, and project pipelines already support repeatable investment at scale.

The strategic implication for the G20 is clear. Climate finance architecture should be organised around functional complementarity rather than institutional competition. Ministers should ask which institution is best placed to absorb early risk, which can finance scale-up, and which can standardise reporting and safeguards across borders.

That approach has direct relevance to current G7 and G20 agendas. Energy security, supply-chain resilience, adaptation, debt sustainability, and industrial competitiveness now intersect in the same financing decisions. Countries that treat climate finance institutions as instruments of economic strategy will shape standards, technology markets, and political alliances more effectively than countries that treat them as a narrow development silo.

Tracking Finance and Measuring Real Impact

Climate finance becomes politically contentious when counting rules are unclear. Ministers know this from every negotiation over fulfilment, comparability and burden-sharing. The challenge isn't only moving money. It is proving what the money is, where it went and what it changed.

Following the money

At the domestic level, tracking frameworks provide a baseline for accountability. The UK's Overview of Climate Finance framework offers a useful example because it provides a technical specification for tracking public and private investment flows toward emissions-reducing technologies and aligns with OECD monitoring of the global USD $100 billion goal, as set out in the Frontier Economics summary report. That matters because ministers need a way to compare policy intent with actual capital deployment.

The same source notes that unit cost estimates for most subsectors are only available from 2018 onward, which limits historical trend analysis. That detail is important. It reminds policymakers that measurement systems are always partial, and that methodological limitations can shape the political narrative as much as the spending itself.

What robust measurement needs

A strong tracking system usually requires three disciplines working together:

- Classification: Governments need clear rules on what qualifies as climate-relevant spending or investment.

- Attribution: Institutions must avoid counting the same flow multiple times across public and private mobilisation chains.

- Results management: Policymakers need indicators that link spending to outputs and longer-term outcomes.

Officials working at or with development finance institutions often find that the hardest part isn't reporting the disbursement. It's connecting finance to operational results in a credible way. For practitioners interested in that implementation layer, understanding RBM for MDB careers is a useful primer on how results-based management shapes planning, monitoring and evaluation in multilateral settings.

Good climate finance reporting does two things at once. It protects political credibility and improves future capital allocation.

Why this matters for G20 agendas

Poor tracking weakens trust between providers and recipients. It also undermines domestic finance ministries, which need evidence to justify continued budget allocations. The benefit of strong measurement goes beyond public relations. It is better decision-making.

When governments can identify which instruments mobilise co-finance, which sectors stall at preparation stage, and which programmes consistently underdeliver, they can reallocate scarce concessional resources more effectively. That is how reporting becomes strategy.

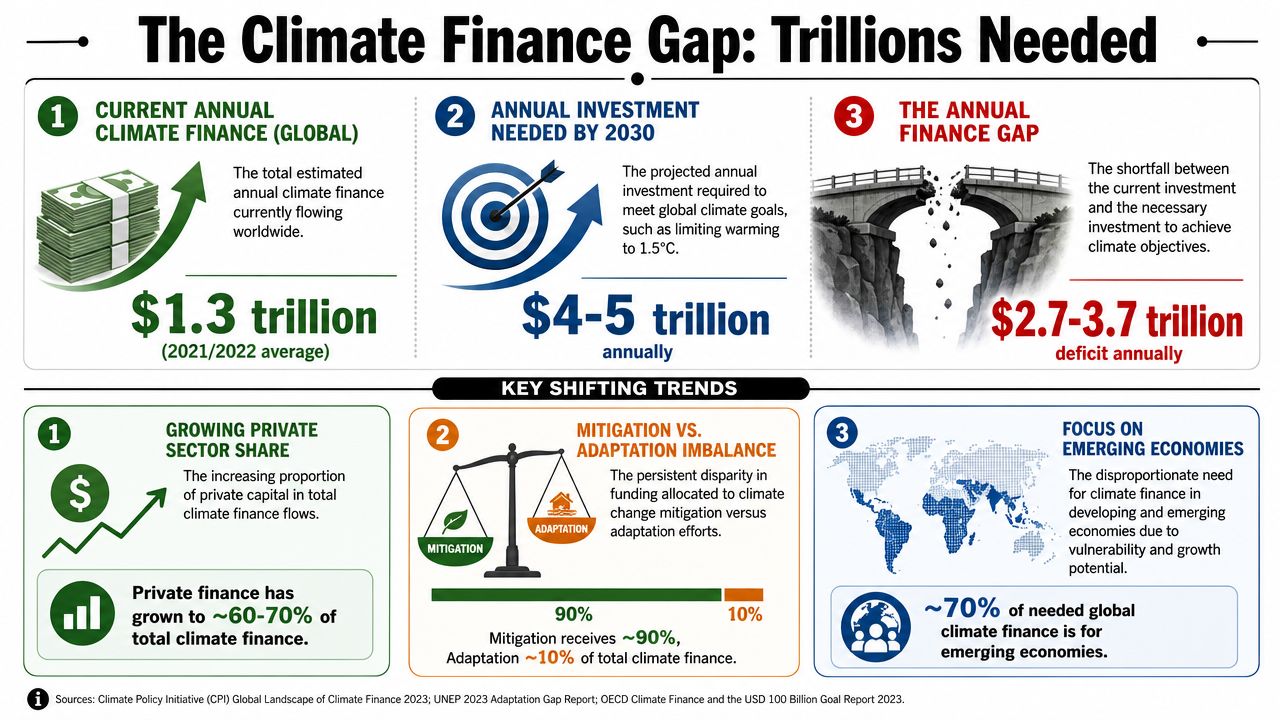

Confronting the Finance Gap and Shifting Trends

Climate finance needs are rising faster than political commitments are holding. That mismatch now matters as much for macroeconomic stability and geopolitical influence as it does for climate policy.

The recent UK pledge illustrates the problem. As noted earlier, Carbon Brief's analysis found that the government's commitment of approximately £6 billion over 2024 to 2027 represents a reduction against the previous £11.6 billion pledge once inflation and reporting changes are taken into account. For G7 and G20 ministers, the significance is larger than one donor's budget line. A major economy can maintain strong rhetoric while reducing the effective purchasing power of its external climate support.

Three policy conclusions follow.

Fiscal politics still determines delivery

International climate finance is negotiated in multiyear frameworks, but funded through annual domestic budget processes. That creates a structural weakness. Commitments made at COPs, G7 summits, or G20 leaders' meetings remain exposed to fiscal consolidation, changes in political leadership, and shifts in accounting treatment.

This has direct strategic consequences. Recipient governments build investment plans, adaptation programmes, and co-financing structures around expected flows. If those flows become less predictable, project pipelines slow, counterpart ministries become more cautious, and private investors apply a higher risk premium to markets already seen as difficult.

The central problem is credibility, not only volume

Headline totals matter, but ministers should focus just as closely on predictability, concessionality, and transparency. A pledge that is hard to interpret or vulnerable to later revision has less policy value than a smaller commitment backed by clear rules and stable appropriations.

That credibility question now sits at the centre of climate diplomacy.

For developing countries, uncertain finance disrupts planning. For multilateral institutions, it complicates portfolio design and weakens confidence in replenishment cycles. For private capital, it reduces the catalytic effect that public finance is supposed to provide in first-loss positions, guarantees, and blended structures.

Shifting trends are changing the politics of leadership

The direction of travel is uneven. Some advanced economies continue to present climate finance as a pillar of international leadership while tightening real fiscal effort. Others rely more heavily on balance-sheet presentation and reporting adjustments. The immediate effect is mistrust. The broader effect is strategic drift across the system.

If developed economies want influence in climate diplomacy, they need consistency in financial delivery.

For the G20, this is not a marginal issue. Climate finance now shapes relations with vulnerable states, affects the credibility of Just Energy Transition Partnerships, and influences whether emerging markets view advanced economies as reliable partners in industrial transformation. In that sense, climate finance is no longer only a burden-sharing debate. It is a test of whether major economies can align fiscal policy, development strategy, and foreign policy around a common transition objective.

Mobilising Trillions for the G7 and G20 Agendas

Climate finance now sits at the centre of G7 and G20 economic strategy. It shapes energy security, industrial competitiveness, resilience, debt trajectories, and geopolitical alignment. For ministers, the policy question is no longer whether climate finance matters. It is whether national and multilateral financial systems can direct capital at the speed and scale required for climate-compatible growth.

Three priorities follow.

First, reform MDB operating models. Boards and shareholders should expect more from existing balance sheets, guarantee capacity, and co-financing platforms, especially in sectors and markets where commercial investors still see policy, currency, or technology risks as too high. Success should be measured not only by commitments approved, but by whether MDB intervention changes project economics, extends tenor, lowers the cost of capital, and brings in institutional investors that would otherwise stay out.

Second, strengthen domestic investment conditions. G7 and G20 ministers control many of the variables that determine whether capital moves: regulatory predictability, credible transition plans, procurement quality, utility reform, and project preparation capacity. In this context, high-level summit language often fails. Investors do not allocate against declarations alone. They allocate against pipelines, contracts, and policy consistency.

Third, deploy concessional finance with sharper discipline. Limited public resources should be directed to adaptation, early-stage preparation, and specific risk tranches that prevent commercially viable projects from reaching financial close. Used well, concessional capital can improve market creation rather than substitute for it. Used poorly, it crowds out private finance, masks weak policy settings, and spreads scarce fiscal support too thinly across too many objectives.

The strategic implication is clear. Climate finance has become a test of state capacity and international credibility. Countries that can connect public finance, development institutions, and private capital to a coherent transition strategy will shape supply chains, standards, and alliances. Countries that cannot will face higher transition costs, weaker influence in climate diplomacy, and less room to steer the terms of global industrial change.

Global Governance Media brings together the policymakers, multilateral leaders and analysts shaping the G7 and G20 agenda. Explore more expert coverage, data-led analysis and forward-looking commentary on climate, energy and global economic governance at Global Governance Media.