By Adrian Mercer

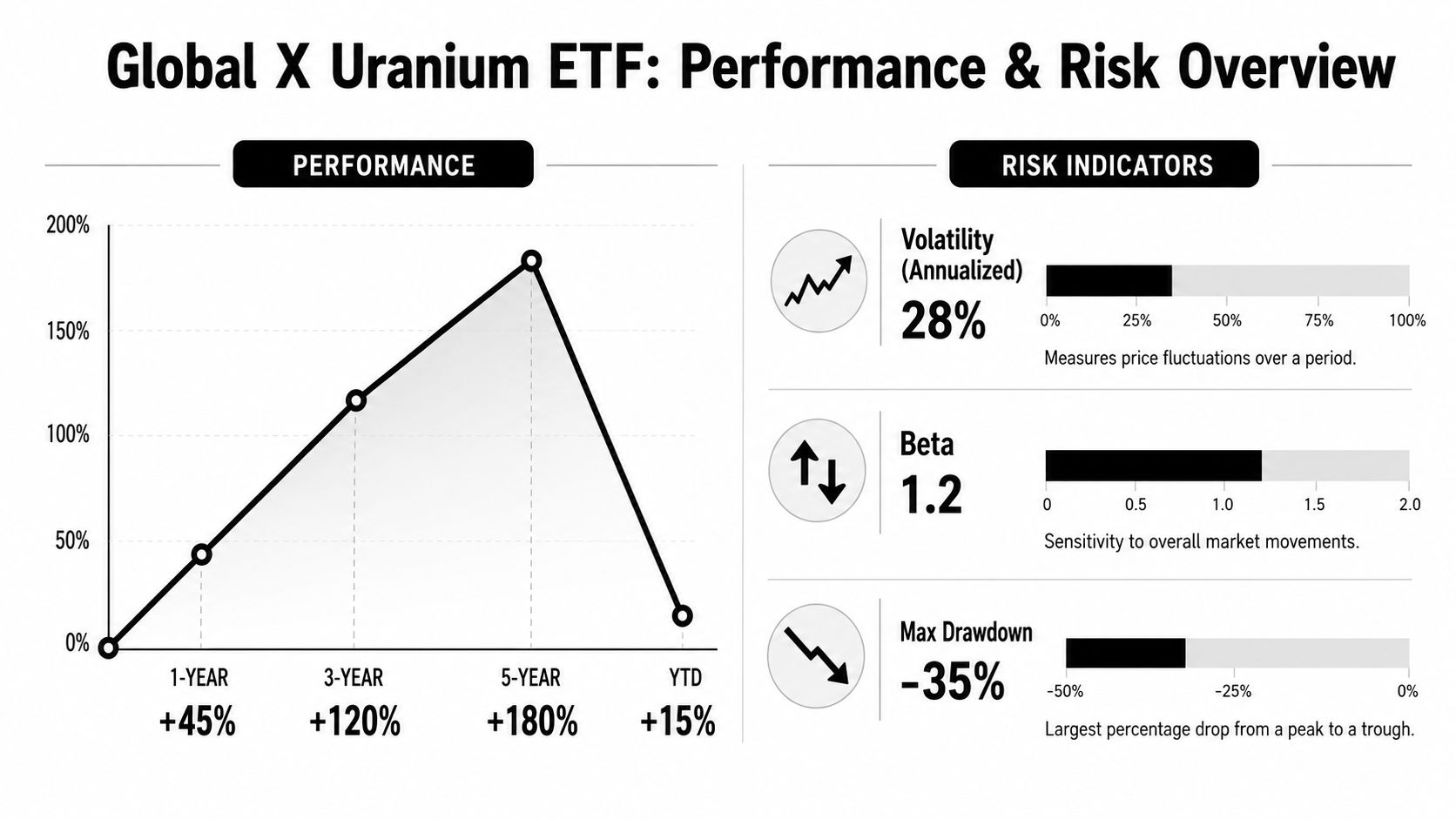

The most revealing number about the Global X Uranium ETF isn't a reactor count or a fuel price. It's the 28.69% one-year total return posted by the London-listed Global X Uranium UCITS ETF (URNG.L) as of mid-2026, alongside a £4.48 share price and a 0.65% ongoing charge, according to Hargreaves Lansdown's fund page for the ETF. That performance matters because it signals more than investor enthusiasm. It reflects how capital markets are pricing the strategic return of nuclear energy to the centre of energy security, industrial policy, and geopolitical competition.

For G7 and G20 policymakers, the Global X Uranium ETF should be read less as a niche thematic product and more as a live market instrument that aggregates expectations about uranium supply security, reactor build-out, mining jurisdiction risk, and the durability of nuclear power within the low-carbon transition. In other words, this fund is a barometer. It measures where private capital believes the next phase of the energy transition is heading.

That matters in a policy environment where governments are trying to decarbonise without sacrificing grid stability, industrial resilience, or strategic autonomy. The market response to uranium exposure offers a useful signal about whether investors believe states are serious about long-horizon nuclear commitments, or merely talking about them.

Table of Contents

- The New Nuclear Nexus Finance and Energy Security

- Deconstructing the Global X Uranium ETF

- Performance Analysis and Inherent Risk Profile

- The Geopolitical Landscape of Uranium Supply

- Interpreting Investment for National Energy Strategy

- Navigating ESG and Complex Regulatory Frameworks

- A Policy Roadmap for a Nuclear Future

The New Nuclear Nexus Finance and Energy Security

Nuclear finance has moved out of the margins. The policy conversation now treats uranium exposure as a proxy for something larger: whether advanced economies can secure dependable low-carbon baseload power without deepening dependence on fragile supply chains.

The Global X Uranium ETF sits at that junction of finance and statecraft. It channels capital into a narrow but strategically charged segment of the energy system. That makes it relevant to ministries well beyond finance, including energy, trade, defence, and industrial strategy. A rise in demand for this vehicle isn't merely a vote on commodity prices. It's a market judgement on whether the nuclear fuel cycle will regain durable policy support across major economies.

A second-order effect follows. As more capital tracks uranium-linked equities, listed mining and fuel-cycle firms gain a stronger financing environment, and governments get a clearer signal about where private markets expect policy consistency. That's one reason nuclear has become harder to dismiss as a legacy technology. The political economy around it is changing.

For policymakers trying to understand why nuclear has re-entered strategic planning, this analysis of the power of nuclear is useful context. It helps explain why uranium-focused funds now function as more than portfolio tools. They've become indicators of whether markets believe governments will back nuclear through permitting, procurement, grid planning, and long-term supply agreements.

Private capital doesn't settle energy policy, but it does reveal which policies investors think will survive electoral cycles.

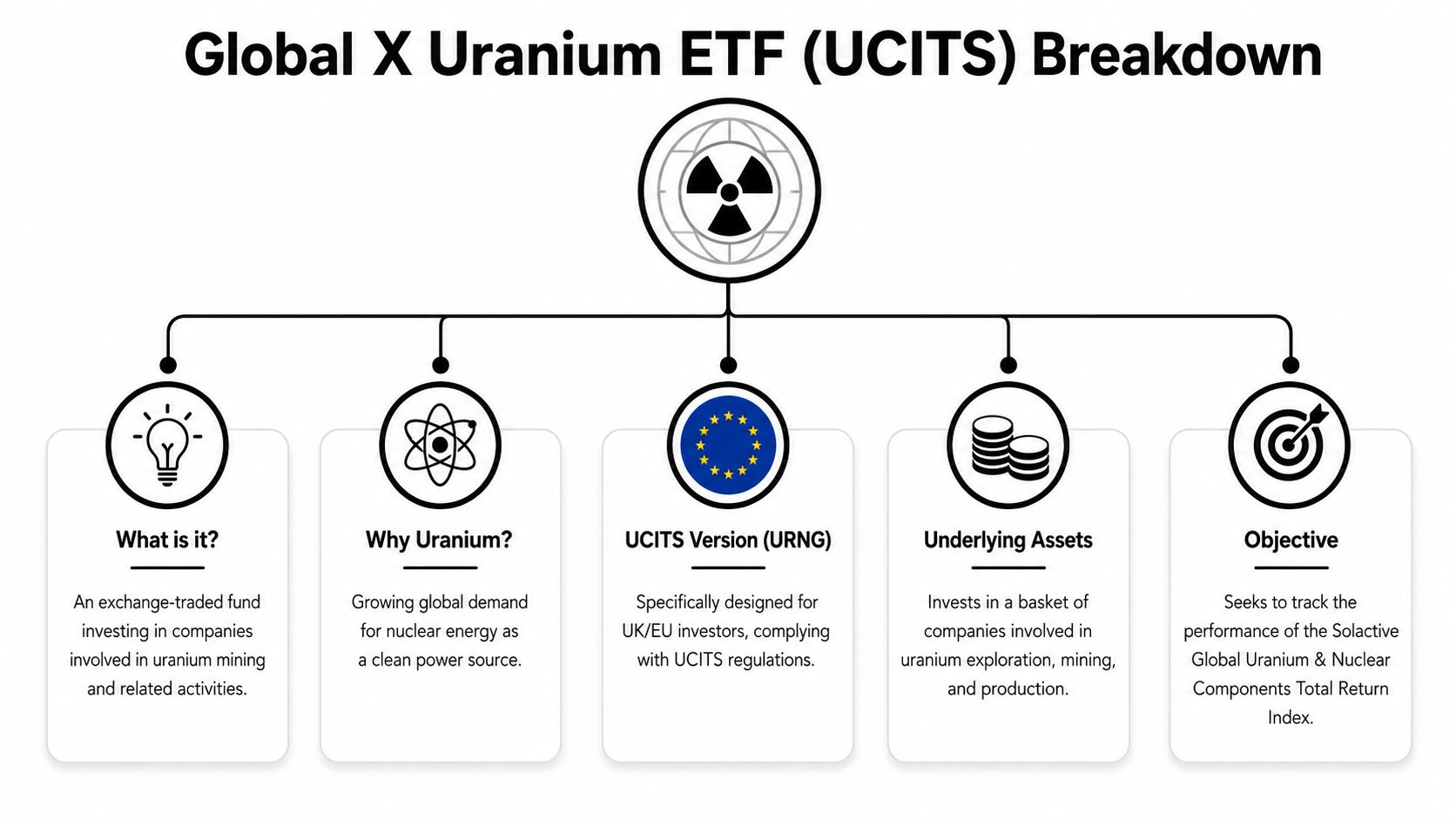

Deconstructing the Global X Uranium ETF

A uranium ETF is never just a portfolio wrapper. In practice, it is a tradable view on reactor buildouts, fuel-cycle resilience, mining finance, and the durability of pro-nuclear policy across advanced economies.

The phrase Global X Uranium ETF covers more than one product, but for UK and European institutions the strategically relevant vehicle is the Global X Uranium UCITS ETF USD Accumulating, listed in London under URNG. That distinction matters because policymakers assessing capital flows into the nuclear value chain need to know which regulatory regime governs the instrument, which investor base can access it easily, and how closely its structure maps onto European market rules.

Why the UCITS structure matters

As outlined in justETF's profile for IE000NDWFGA5, the fund is domiciled in Ireland, listed on the London Stock Exchange under ticker URNG, holds substantial assets under management, charges a 0.65% total expense ratio, follows an accumulating dividend policy, and uses full replication to track the Solactive Global Uranium & Nuclear Components Index.

Those design choices shape who uses the fund and what signal the fund sends. A UCITS wrapper places the vehicle inside a familiar compliance framework for European pension funds, wealth platforms, and cross-border allocators. The Irish domicile also matters operationally because it sits within a legal and tax structure many institutional investors already use for regional ETF exposure.

The accumulating share class has a separate policy implication. By reinvesting income rather than distributing it, the fund is structured for investors seeking long-duration exposure to uranium and nuclear-related equities, not for income-sensitive buyers. That can reinforce persistent capital allocation to the sector when the policy outlook for nuclear improves.

What full replication means in practice

Full replication deserves more attention than it usually gets. If a uranium fund holds each benchmark constituent directly, shifts in investor demand transmit more cleanly into the underlying equities than they would through a sampled or synthetic structure.

For ministers and regulators, this is relevant because the ETF becomes a clearer market barometer. If capital enters or exits the vehicle, the effect is tied more directly to listed companies involved in uranium mining, processing, and nuclear components. In a sector shaped by permitting delays, state-backed procurement, export controls, and sanctions risk, that directness gives policymakers a more readable indicator of how private capital is pricing the future of the fuel cycle.

The architecture is easier to assess through four features:

| Feature | Strategic interpretation |

|---|---|

| UCITS structure | Accessible within a regulatory format widely used by UK and European institutions |

| Full replication | Investor flows map more directly onto the underlying nuclear and uranium equity basket |

| Accumulating share class | Supports reinvestment and longer-horizon thematic exposure rather than income distribution |

| Sector-specific index | Concentrates capital in a narrow industrial chain with direct relevance to energy security |

This concentration is the main analytical point. URNG is not a broad clean-energy allocation, and it is not a generic commodities fund. It is a targeted financial instrument tied to a sensitive segment of the nuclear supply chain. As a result, changes in assets, trading volumes, and valuation multiples can reflect more than investor enthusiasm. They can also reflect expectations about reactor approvals, Western supply diversification away from Russia-linked fuel services, and the willingness of governments to treat nuclear power as part of energy security policy rather than as a residual climate option.

Policy reading: The structure of a uranium ETF affects how accurately it mirrors market conviction about nuclear strategy, supply-chain security, and long-term state support.

Performance Analysis and Inherent Risk Profile

A near 29% one-year gain in a uranium ETF matters because it shows how quickly capital can reprice a sector once energy security, industrial policy, and decarbonisation begin to align.

What recent performance is signalling

As noted earlier, the London-listed Global X Uranium UCITS ETF (URNG.L) has posted strong recent returns, with a share price of £4.48 and a 0.65% ongoing charge and management fee as of mid-2026. Those figures matter less as a retail scorecard than as a policy signal. Investors have been willing to pay for exposure to the nuclear fuel chain at a time when governments are reassessing baseload power, strategic stockpiles, and dependence on politically exposed suppliers.

That repricing carries a broader implication. Equity markets are assigning higher value to firms linked to uranium mining, fuel services, and reactor supply chains because policy risk has shifted direction. For much of the past decade, nuclear faced uncertainty from public opposition, slow approvals, and weak investor sponsorship. Recent performance suggests part of that discount has narrowed.

The result is not a referendum on nuclear technology alone. It is also a market judgment on whether governments can convert pledges on energy resilience into bankable projects, procurement commitments, and permitting decisions.

Where the risk sits

URNG remains a high-conviction, high-volatility instrument. Its risk profile is shaped by three forces that policymakers should read carefully.

- Sensitivity to uranium price expectations: The fund holds equities, but those companies are still valued partly on assumptions about future uranium pricing, contract terms, and reactor build timelines.

- Narrow thematic concentration: A specialised index can rise quickly when sentiment improves and fall just as quickly when cost inflation, project delays, or policy reversals weaken the investment case.

- Political and regulatory exposure: Holdings operate across jurisdictions where export controls, mine licensing, sanctions, indigenous consultation requirements, and state intervention can materially change earnings prospects.

This makes the ETF useful as a market-based indicator, but unreliable as proof of durable sector strength. A sharp rally can reflect expected supply tightness as much as confidence in new nuclear deployment. A reversal can signal doubts about execution rather than rejection of nuclear power itself.

For G7 and G20 officials, that distinction matters. Capital can finance uranium and nuclear-adjacent firms faster than governments can permit mines, convert reactors from Russian-linked fuel services, or build enrichment capacity in allied jurisdictions. The gap between market enthusiasm and state capacity is where future volatility is likely to emerge.

That gap also connects uranium finance to the wider problem of critical mineral resilience. The policy challenge is not limited to attracting private capital. It is about building processing, conversion, transport, and recycling systems that reduce exposure to single-point geopolitical risk, a point developed in this analysis of global partnerships and circularity for resilient critical minerals systems.

Strong recent performance in a uranium ETF should be read as concentrated market conviction about state follow-through, supply discipline, and fuel security. It should not be mistaken for reduced strategic risk.

URNG therefore works less like a passive thematic allocation and more like a live barometer of whether nuclear policy is becoming investable at scale. For policymakers, its value lies in what it reveals about confidence, bottlenecks, and the credibility of national energy strategy.

The Geopolitical Landscape of Uranium Supply

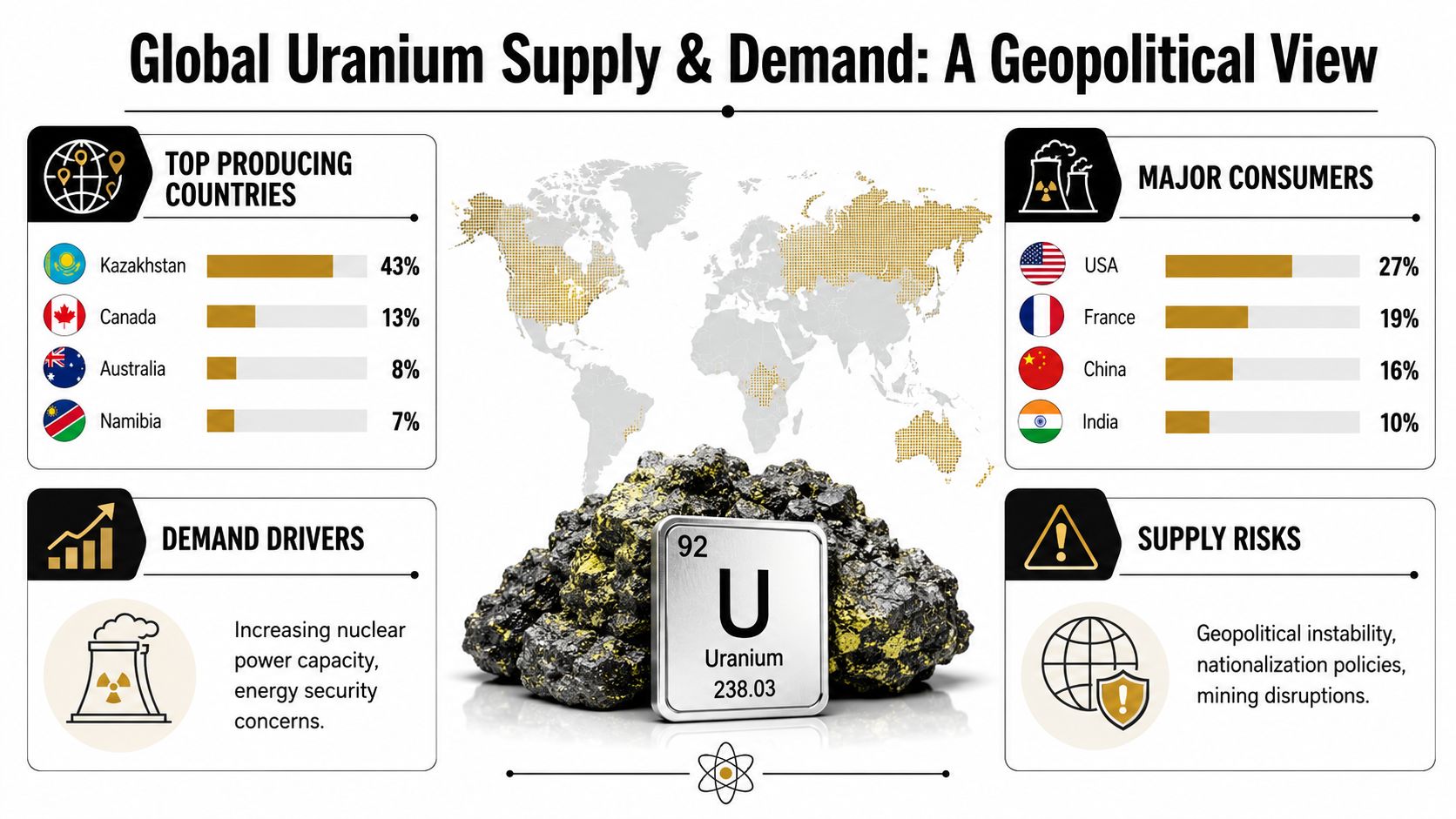

The strategic value of the Global X Uranium ETF comes into focus when you look at what sits underneath it. This isn't an abstract clean-energy allocation. It's a portfolio linked to a geographically uneven and politically exposed supply chain.

Why holdings matter more than branding

The underlying Solactive Global Uranium & Nuclear Components index recorded a 27.59% gain over the past year and a 135.84% cumulative increase over three years, while top-weighted holdings include Cameco, Uranium Energy Corp, and Kazatomprom, according to CMC Markets' overview of the Global X Uranium ETF. Those names matter because they tie the fund directly to Canada, the United States, and Kazakhstan, three jurisdictions that carry very different policy and geopolitical profiles.

That geographic spread creates both resilience and fragility. On one hand, it means the ETF isn't captive to a single domestic market. On the other, it means investors are effectively underwriting a transnational supply system exposed to diplomatic shocks, transport constraints, national resource policy, and shifting alliance structures.

A strategic reading of uranium concentration

For G7 and G20 governments, the lesson is clear. A uranium ETF may look like a financial wrapper, but in strategic terms it maps exposure to a chain that includes extraction, refinement, logistics, and political access. That's why uranium should increasingly be discussed alongside other critical minerals rather than as an isolated energy commodity.

Several implications follow:

- Canada's role is stabilising but finite: Exposure to Cameco gives the fund a link to a politically dependable producer, but not a substitute for broader supply diversity.

- Kazakhstan remains central: Exposure to Kazatomprom means any disruption in Central Asian political risk perceptions can travel quickly into listed uranium valuations.

- The US role is partially industrial, partially strategic: Uranium Energy Corp reflects not only market exposure but the wider policy push for domestic and allied supply resilience.

Critical-minerals strategy becomes inseparable from nuclear policy. Governments can't credibly support reactor expansion while leaving uranium supply security to fragmented market responses alone. A more durable approach requires alliances, recycling where feasible, and cross-border financing structures that reduce single-jurisdiction dependency. This argument for G7 critical-minerals partnerships and circularity is directly relevant to uranium because it reframes supply resilience as a coordinated system problem rather than a procurement problem.

Uranium security doesn't begin at the reactor gate. It begins in mining law, trade diplomacy, and transport access.

Interpreting Investment for National Energy Strategy

A uranium fund becomes strategically important when governments set nuclear targets that require sustained fuel access, industrial capacity, and policy credibility. At that point, the fund stops being merely descriptive. It starts becoming diagnostic.

The UK case

The UK offers a sharp example of the gap between capital market enthusiasm and strategic policy clarity. InvestEngine's discussion of URNG notes that the UK is aiming to increase nuclear capacity to 24GW by 2050, a projection said to require 1.5 million tonnes of uranium annually. The same source also notes investor questions about whether the ETF's 736.93M net asset base includes sufficient exposure to UK supply chain partners such as Rolls-Royce and AMEC, while concluding that the absence of UK-specific sectoral breakdowns means policymakers can't evaluate whether the ETF supports domestic energy sovereignty.

That point deserves more attention than it usually gets. An ETF can show strong confidence in the global uranium complex while still offering little visibility into whether private capital is reinforcing a specific national industrial strategy. For the UK, that raises an uncomfortable possibility: public ambition for nuclear expansion may be advancing faster than the market tools available to assess domestic supply-chain alignment.

Three policy questions follow from that gap:

- Does market exposure support national capability? If a fund captures global miners but not local engineering or fuel-cycle enablers, it may validate the nuclear thesis without strengthening domestic sovereignty.

- Can states monitor strategic dependence early enough? By the time governments discover that capital has concentrated abroad, industrial catch-up may already be expensive and slow.

- Are financial products reflecting policy goals or merely reacting to commodity momentum? Those are not the same thing.

The wider implication is that ministers shouldn't read inflows into uranium-linked equities as proof that national strategy is coherent. They should read them as a prompt to ask where financing is landing.

What policymakers should ask of uranium funds

Before making strategic use of products like the Global X Uranium ETF, governments and public institutions should test them against a harder set of questions:

- Holdings transparency. Can the fund's composition be mapped to allied supply, domestic industry, and critical chokepoints?

- Policy congruence. Does the investment universe reinforce announced nuclear, industrial, and resilience objectives?

- System exposure. Which parts of the fuel and component chain remain underrepresented, and what does that imply for security planning?

A broader public discussion of nuclear strategy benefits from practical context, and the following briefing adds that perspective:

Markets can price a narrative quickly. States still have to build the infrastructure, procurement rules, and allied partnerships that make the narrative real.

Navigating ESG and Complex Regulatory Frameworks

Nuclear investment doesn't fit neatly into a binary ESG framework. It has a strong claim to relevance in low-carbon power systems, yet it also carries persistent questions around waste, safety, community consent, and strategic dependency. Serious institutional analysis has to hold those tensions together rather than forcing them into a simplistic green-versus-brown label.

Nuclear doesn't fit simple ESG labels

For investors operating in UK and European markets, one of the least understood issues isn't the abstract ESG debate. It's the institutional plumbing around tax, wrappers, and eligibility. Simply Wall St's discussion of URA and URNG points to a persistent information gap around the UK-specific tax and regulatory treatment of the UCITS version versus the US-domiciled counterpart, including Stamp Duty Reserve Tax, dividend withholding, and UCITS eligibility for UK pension schemes. The same source notes that no UK source clearly explains how the UCITS wrapper avoids the 15% US dividend withholding tax associated with non-UCITS US-listed ETFs.

That gap has governance implications. Boards and investment committees can't treat structure as secondary when regulation, reporting obligations, and fiduciary standards increasingly demand precision on how vehicles operate.

The pressure is rising. Under the UK's Corporate Governance Code, boards now have to make a formal declaration on the effectiveness of material internal controls, including narrative and ESG reporting controls under Provision 29. At the same time, institutions communicating publicly about energy and sustainability claims need to be conscious of broader UK expectations around evidence, public-interest framing, and local relevance, themes that also connect with clearer explanations of what ESG reporting involves.

Why structure and governance matter as much as thesis

The deeper risk is political economy. When regulation is opaque, specialised sectors often attract lobbying that favours particular structures, exemptions, or tax outcomes without improving strategic resilience. That's why Unitism's insights on rent seeking are useful here. They provide a framework for distinguishing between value created through genuine supply-chain strengthening and value captured through rules that privilege one market channel over another.

A disciplined ESG approach to uranium should therefore ask:

- Environmental: Does the investment support credible low-carbon generation pathways without obscuring waste and lifecycle accountability?

- Social: Who bears the local costs of mining, transport, and siting decisions?

- Governance: Is the chosen fund structure transparent, regulatorily coherent, and suitable for the institution's reporting obligations?

A uranium allocation can support climate resilience and still fail a governance test if the structure, disclosures, or policy assumptions are weak.

A Policy Roadmap for a Nuclear Future

The Global X Uranium ETF deserves attention because it translates a strategic argument into a market signal. It captures where private capital sees credibility in the nuclear fuel cycle, where it perceives supply risk, and where it expects governments to sustain support for atomic energy within the broader clean-power transition.

For G7 and G20 policymakers, that signal is useful but incomplete. Strong uranium-linked performance doesn't prove that national strategy is working. It shows that investors believe parts of the nuclear chain will matter more. The policy task is to determine whether those capital flows reinforce allied resilience, domestic industrial capacity, and effective governance, or whether they deepen exposure to external dependencies.

Institutional investors should treat the fund as a prompt for deeper due diligence on holdings, jurisdictional risk, tax structure, and alignment with public-energy objectives. Governments should treat it as an early-warning indicator of where supply pressure, financing concentration, and strategic bottlenecks may emerge next.

Nuclear power is becoming harder to separate from energy security, industrial policy, and geopolitical competition. Reading instruments like the Global X Uranium ETF carefully is no longer optional for serious energy governance.

For deeper analysis on energy security, critical minerals, ESG governance, and G7 and G20 policy strategy, explore Global Governance Media.