By Eleanor Ashcroft

London's housing correction is no longer a routine cyclical story. The signal that matters for finance ministers is this: private-sector housebuilding in London has fallen 84% since 2015, with only 5,547 new starts in 2025 against a need for 88,000 homes annually, according to BBC reporting on the construction slowdown. That turns a price adjustment into a strategic policy problem. A city can absorb softer valuations for a period. It can't absorb a deepening supply shock without consequences for inflation, labour mobility, fiscal planning, and urban competitiveness.

That's why the London house price fall deserves attention well beyond the UK property pages. London sits at the intersection of global capital, domestic household balance sheets, and public-sector revenue expectations. When prices weaken in such a market, the effects don't stay inside estate agency windows. They spill into development finance, local tax bases, infrastructure sequencing, and confidence in the wider growth model.

The more important point is that the correction isn't uniform. The headline conceals a two-tiered market. Prime central boroughs have come under sharper pressure than much of outer London, and that divergence matters for policy design. Treat the entire city as if it were in a single broad downturn, and ministers risk mispricing the problem. Ignore the supply consequences, and today's weakness becomes tomorrow's affordability crisis.

For housing operators trying to stabilise rental income while transaction markets remain uncertain, practical market responses such as guaranteed rent solutions for landlords help illustrate how private actors are adapting to volatility that public policy hasn't yet fully addressed.

Table of Contents

- An Unsettled Market in a Global City

- Defining the Contraction Magnitude Timing and Geography

- Diagnosing the Drivers of the Downturn

- Assessing the Economic and Fiscal Ripple Effects

- A Tale of Two Markets Prime Central vs Outer London

- Global Context and Forward-Looking Scenarios

- A Policy Roadmap for Resilience and Growth

An Unsettled Market in a Global City

The London house price fall should be read as a policy stress test for a global city, not as a localised correction in an expensive market. London combines three features that amplify risk. It is a major financial centre, a magnet for international wealth, and a labour market that depends on workers who are increasingly priced out of its housing system.

That mix creates a contradiction. Prime values can fall while the city remains structurally undersupplied. For ministers, that means lower prices don't automatically signal better access. In practice, a correction in high-value districts can coincide with weaker construction pipelines, slower mobility, and worsening barriers for the workforce that keeps the metropolitan economy functioning.

Why London matters beyond Britain

A weakening London market can influence broader expectations about the direction of high-value urban property in open economies. It also affects debates on taxation, cross-border capital, and the balance between housing as a consumption good and housing as a store of wealth.

London is useful to policymakers because it shows how a housing downturn can be narrow in geography, broad in consequences, and politically easy to misread.

The central analytical mistake is to treat all price declines alike. Some corrections reflect excess speculation unwinding. Others reveal financing strain. Others still are policy-driven reallocations within a city. London currently shows elements of all three, but in uneven proportions across boroughs and property types.

The strategic issue for ministers

A finance ministry looking only at average citywide prices would miss the core problem. The immediate fall is concentrated in segments that matter heavily for transaction taxes, investor sentiment, and development economics. The longer-run danger lies elsewhere. Fewer viable schemes today mean tighter supply tomorrow.

For G20 governments facing similar tensions between affordability, capital inflows, and construction viability, London offers a live case study in how a housing correction can produce opposite effects at the same time. It can cool asset values at the top while worsening scarcity for everyone else.

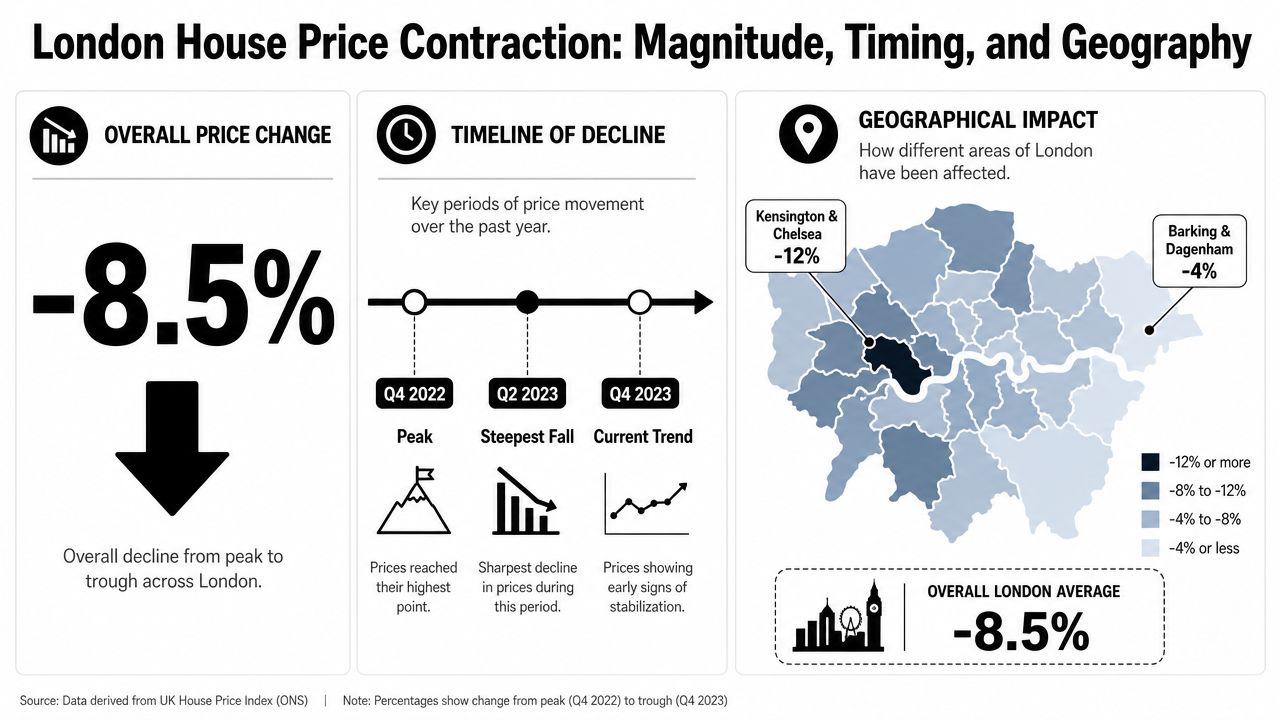

Defining the Contraction Magnitude Timing and Geography

By early 2024, the average London house price had fallen to £556,000, down 1.7% on the year, according to the official ONS figure cited in the verified dataset. That headline number matters less than its distribution. The correction is not uniform across the capital, and treating it as a single-city decline obscures where underlying stress is accumulating.

From post-pandemic peak to correction

London's pricing cycle turned after the late summer 2022 peak. As noted earlier, values in 2023 posted the city's sharpest annual fall since 2009 and sat about 4.5% below that recent high. The scale is material, but the timing is more instructive for policymakers. What began as a rate-driven slowdown developed into a segmented repricing, with weaker liquidity appearing first in the parts of the market most exposed to financing costs, tax sensitivity, and discretionary international demand.

The six-month run of declines into January 2024 shows that this was not a brief adjustment. It was a sustained loss of momentum.

That distinction matters for fiscal planning. A short correction mainly affects sentiment. A prolonged one starts to weigh on transactions, valuation benchmarks, and the pipeline assumptions used by developers, lenders, and local authorities.

Geography matters more than the citywide average

The citywide figure conceals a two-tiered correction. Prime central boroughs are repricing for structural reasons linked to tax, global capital flows, and thinner buyer depth at high price points. Much of outer London faces a different problem. Prices have been more resilient in relative terms, but households there remain highly exposed to borrowing costs and the long-term risk of restricted new supply.

Property type reinforces that split. The verified dataset shows London flats and terraced houses recorded a 2.1% annual drop. Because flats account for a larger share of London's stock than in most UK regions, weakness in that segment carries disproportionate weight in the aggregate index. Analysts who rely only on the average city figure risk overstating the breadth of the decline while understating its strategic concentration.

A concise view is below:

| Segment | Verified movement | Why it matters |

|---|---|---|

| London overall in 2023 | Annual decline | Marked the city's weakest year since 2009 |

| Distance from late summer 2022 peak | About -4.5% | Confirms a clear reversal from the post-pandemic high |

| Average London price to January 2024 | -1.7% to £556,000 | Shows the correction extended into 2024 |

| London flats and terraced houses | -2.1% | Important in a city where flats carry greater index weight |

The policy implication is straightforward. London is not experiencing one housing downturn. It is experiencing a high-value correction in prime central districts and a separate affordability and supply strain elsewhere. Those are different problems and require different responses.

At transaction level, this fragmentation also widens the range between asking prices, mortgage-backed valuations, and achieved sale prices. For buyers and advisers, post-survey negotiation strategies become more relevant when comparable evidence diverges sharply by borough and property type.

Operational rule: Citywide averages are a weak guide to pricing power in a segmented correction. Borough mix, property type, and transaction liquidity matter more.

Diagnosing the Drivers of the Downturn

The causes of the London house price fall are not singular. They interact. Financing pressure narrows demand. Tax changes alter behaviour at the top end. Lower liquidity then weakens pricing benchmarks and slows transaction chains.

Why prime central London is leading the fall

The strongest evidence points to a structural prime-central divergence rather than a citywide collapse. ONS data showed Kensington & Chelsea fell 11.3% and Westminster 14.4% in the year to September 2024, with the drag concentrated in properties above £2m and partly driven by a new mansion tax with annual fees starting at £2,500. London became the only English region with an annual decline while the UK average rose 2.5%, according to Bloomberg's reporting on the prime borough correction.

That pattern matters because prime central London isn't just another local submarket. It carries disproportionate weight in perceptions of London wealth, overseas demand, and high-value transaction activity. When that segment reprices, the political narrative often overshoots. Policymakers start talking about a broad collapse when the evidence points to a concentrated shock.

A feedback loop between pricing and liquidity

Higher mortgage costs have also tightened effective demand, especially where absolute loan sizes are large. Even when the initial fall begins in the prime segment, financing conditions can spread caution across adjacent markets. Sellers hold back, buyers wait, and developers struggle to underwrite future values.

A qualitative comparison with wider investor commentary is useful here. Broader analyses such as the 2026 UK property market outlook help situate London within a national investment debate, but London's current weakness is more tax-sensitive and segment-specific than many national narratives imply.

Three forces are interacting:

- Tax sensitivity at the top end: High-value assets respond quickly to changes in recurring holding costs and political signalling.

- Financing constraints: Higher borrowing costs reduce affordability most sharply where baseline prices are already high.

- Liquidity withdrawal: Fewer confident transactions mean weaker price discovery, and weaker price discovery feeds caution.

Prime-central corrections often begin as valuation stories, but they become supply stories when developers and lenders stop believing in exit prices.

Assessing the Economic and Fiscal Ripple Effects

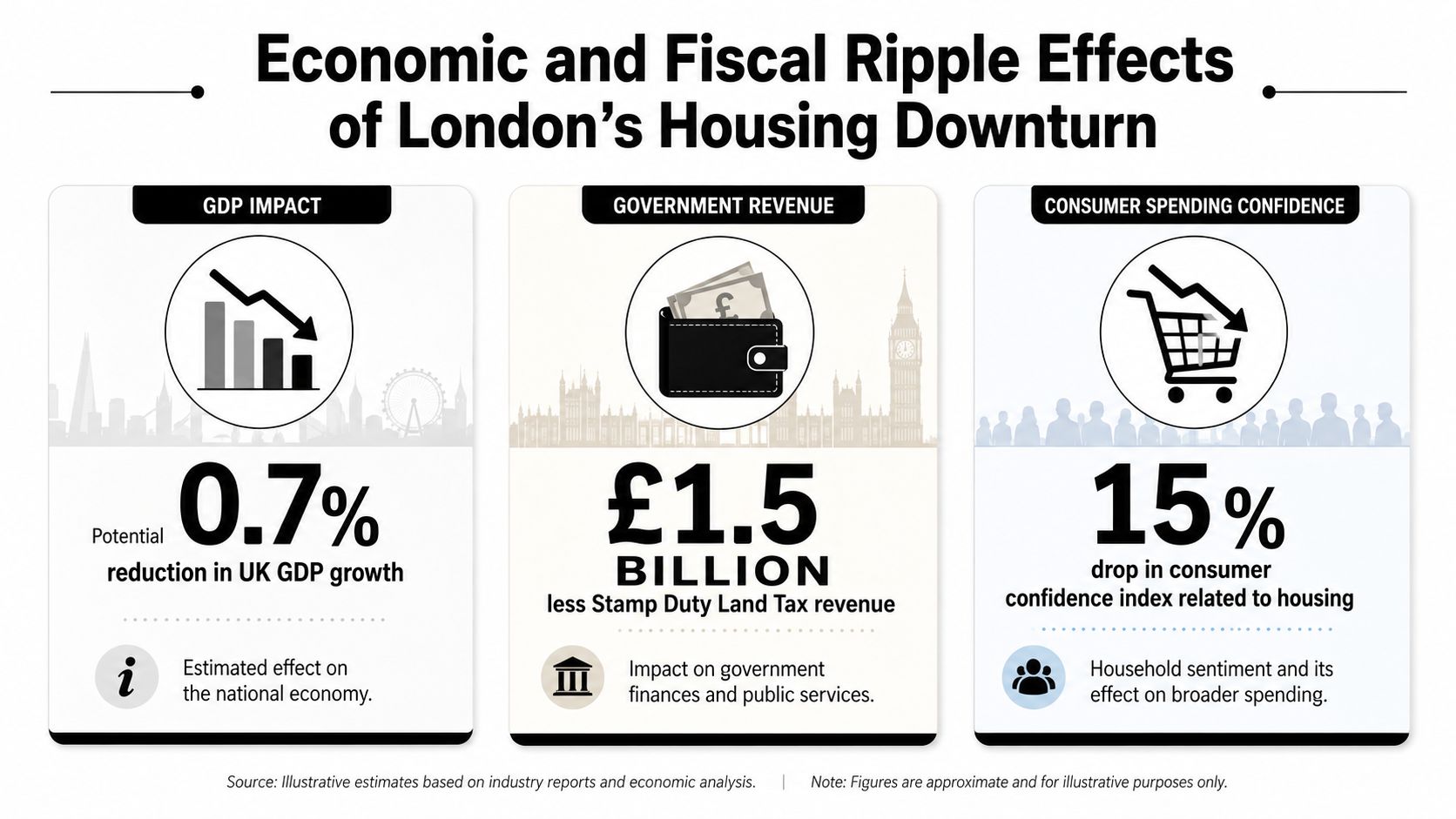

An 84% fall in private-sector housebuilding since 2015 matters more for London's medium-term economy than a moderate decline in headline prices. For finance ministries, the main question is no longer whether valuations are cooling. It is whether the correction is now suppressing future supply, weakening tax receipts, and raising longer-run housing costs for the wider workforce.

Construction is now the main macroeconomic transmission channel

As noted earlier, London's development pipeline has deteriorated sharply. That matters because construction links the housing market to employment, local investment, infrastructure delivery, and future rental pressure. Once projects are delayed or cancelled, the effects persist well beyond the initial price adjustment.

The fiscal implications are immediate. Fewer viable schemes mean weaker fee income for local authorities, slower build-out around planned transport and social infrastructure, and reduced confidence among lenders and institutional capital. The correction therefore shifts from an asset-price event into a supply-side constraint.

That distinction should shape policy.

A two-tiered market correction sharpens the risk. Weakness concentrated in prime central London can still generate citywide consequences if high-value transactions no longer support land values, developer margins, and cross-subsidy models used to bring forward mixed-tenure schemes. In that setting, a fall at the top end does not stay at the top end. It lowers the probability that new homes are built across the system.

The affordability effect is delayed, but more damaging

Short-term price softness can look helpful in public debate. For many households, however, affordability is determined less by a temporary adjustment in valuations than by the long-run balance between supply, rents, and wage growth. If the pipeline contracts, the eventual outcome is straightforward. Scarcity intensifies, rents remain high, and access to home ownership deteriorates for workers outside prime-income brackets.

The burden is unevenly distributed. Owners of expensive assets absorb nominal losses first. Renters, younger households, and key workers then absorb the larger structural cost through tighter availability and higher housing outgoings.

That is why the case for inclusive planning and housing for a better world is not social policy rhetoric. It is an economic stabilisation issue tied to labour mobility, productivity, and the cost base of a global city.

Four channels merit close Treasury monitoring

Development finance stress

Lower expected sale values and weaker transaction depth make lenders more cautious, particularly on projects that rely on premium-unit absorption to support overall viability.Public revenue exposure

A thinner high-value market can reduce receipts tied to transactions and development activity, even before any broader slowdown appears in aggregate output.Labour market pressure

If fewer homes are completed, employers face a more expensive housing environment for staff, which can intensify recruitment and retention problems in essential services.Balance-sheet restraint

Households, investors, and developers tend to defer spending when price discovery weakens and future valuations become less certain.

The policy mistake would be to read lower prices as a self-correcting affordability solution. In London's current market, the larger systemic risk is that a prime-led correction is choking off supply, and that the fiscal and social costs will emerge after the headlines about falling prices have faded.

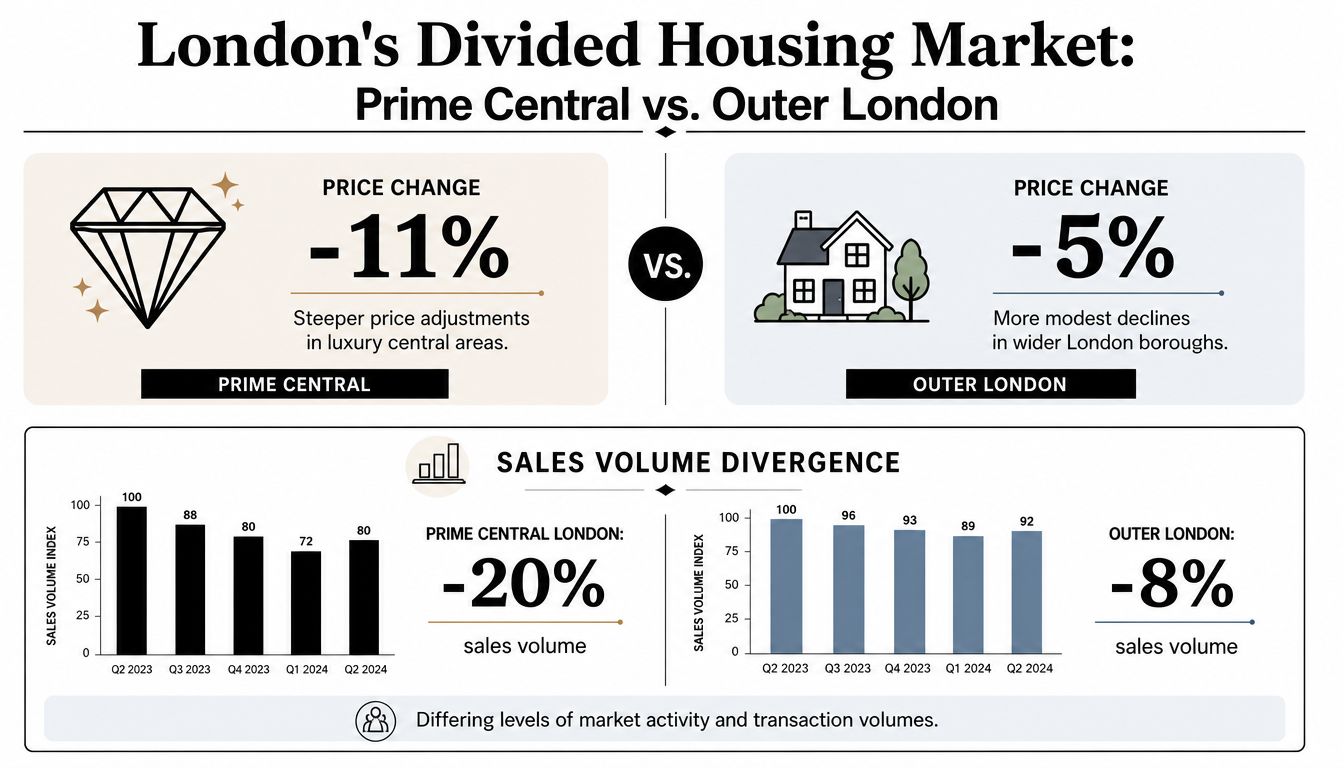

A Tale of Two Markets Prime Central vs Outer London

The headline “London is falling” is too blunt to guide policy. The city is splitting into at least two distinct markets, and their policy needs are different.

Prime boroughs are carrying the drag

The clearest example is Kensington and Chelsea, where average house prices fell 8.4% year on year by April 2026, dropping from £1,390,000 in April 2025 to £1,273,000 in April 2026. That is a £117,000 fall in a single year, according to the ONS local housing price visualisation for Kensington and Chelsea.

The same verified dataset shows how broad-based that local correction was inside the borough. First-time buyers paid an average of £1,094,000 in April 2026 compared with £1,191,000 a year earlier, an 8.1% fall. Mortgage-backed transactions fell from £1,415,000 to £1,299,000, an 8.2% decline. Cash buyer averages dropped from £1,360,000 to £1,243,000, an 8.6% decline.

That pattern is analytically important. It suggests the borough-level correction isn't limited to one financing channel. It is visible across buyer categories, which strengthens the case for viewing prime central London as the epicentre of the downturn.

A short video summary helps illustrate how this divergence is being interpreted in public discussion:

Why one-size-fits-all policy will misfire

Outer London doesn't map neatly onto prime central weakness. The broader city has shown softer movement than the steep repricing in elite boroughs, and some non-prime areas have been comparatively resilient in qualitative terms. That's why citywide rescue policies can be poorly targeted.

A better policy lens is comparative:

| Market layer | Dominant pressure | Policy risk if misread |

|---|---|---|

| Prime central | Tax sensitivity, investor caution, high absolute financing costs | Overreacting with broad market support |

| Outer London | Structural supply shortage, affordability strain, slower turnover | Underreacting on delivery and planning |

This distinction changes what ministers should do. If the shock is concentrated at the top, then broad demand stimulus may reflate better-defended segments without solving access problems elsewhere. Conversely, if supply in outer and middle-market London is constrained, then delivery tools matter more than market-wide price support.

Global Context and Forward-Looking Scenarios

London's housing trajectory matters internationally because it is diverging not only from parts of the UK, but from the political assumption that expensive gateway cities either always outperform or always crash in unison. Neither is true.

London's divergence within the UK matters globally

A useful benchmark comes from Halifax. London house prices fell 1.3% year on year as of December 2025, while Northern Ireland recorded 7.5% growth. Halifax also projected a further -3% annual house price change for the UK in 2026, according to Reuters coverage of the Halifax data.

For global policymakers, the significance lies in the contrast. London can weaken even when other regions are growing. That tells us this is not just a national macro cycle. It is also a city-specific repricing of expensive urban property under tighter financing and changing tax conditions.

A broader policy benchmark is available in comparative work on G20 performance on housing, which helps frame London as part of a larger challenge facing major economies: balancing affordability, investment stability, and sustainable urban growth without mistaking asset-price moves for structural reform.

Three plausible policy scenarios

The next phase depends less on headlines about nominal prices and more on whether supply recovers.

Stagnation scenario

Prices remain under pressure in high-value segments while development stays weak. This would prolong uncertainty and deepen future shortages.Selective recovery scenario

Prime central values stabilise, but only after the market absorbs tax and financing changes. Outer London still faces affordability stress because supply remains too thin.Supply-led stabilisation scenario

Governments focus on planning, delivery, and development viability. Under this path, weaker short-term prices needn't translate into a more exclusionary city later.

The medium-term outlook for London depends less on whether prices fall a bit further and more on whether housing production restarts.

A Policy Roadmap for Resilience and Growth

A credible response to the London house price fall must separate asset repricing, which can be tolerated, from supply destruction, which cannot. The first is a market adjustment. The second is a public policy failure.

What national government should do now

National authorities should avoid blunt market-wide stimulus. London doesn't need a generic attempt to push all prices back up. It needs targeted action that restores development viability where homes are most needed.

Three levers stand out:

Recalibrate supply-side support

Focus fiscal tools on enabling stalled schemes, especially where projects are commercially marginal but socially valuable.Review high-value tax design

If recurring taxes are creating abrupt dislocations in narrow segments, ministers should test whether the structure is producing avoidable volatility without delivering broader housing gains.Align housing and productivity policy

Treat housing delivery as economic infrastructure. Labour markets can't function efficiently when workers can't live within reach of jobs.

What London government and the G20 should prioritise

City and borough leaders should use differentiated policy rather than citywide averages. Prime borough corrections don't justify inaction on delivery elsewhere. Planning reform, sequencing of transport-linked sites, and clearer viability frameworks are more useful than broad commentary about a “buyer's market”.

Multilateral forums also have a role. G20 finance ministers should treat major-city housing systems as part of macro resilience, not as a side issue. Tax coordination, capital-flow transparency, and urban supply capacity all intersect here.

A practical framework would include:

- For London government: unblock suspended sites, accelerate planning decisions where infrastructure already exists, and focus on homes that support workforce participation.

- For national treasuries: integrate housing delivery into growth and inflation planning rather than treating it as a siloed social-policy question.

- For the G20: compare how major cities handle tax shocks, investment flows, and supply constraints, then standardise better practice.

The strategic objective isn't to prevent all price declines. It is to prevent a segmented correction from hardening into a long-run shortage economy. That requires better data discipline, narrower policy targeting, and faster intervention when construction pipelines seize up.

A stronger international conversation on positive action in housing would help governments move from reactive market watching to active resilience planning.

For more data-led analysis on housing, economic resilience, and policy choices shaping the G7 and G20 agenda, visit Global Governance Media.