By Dr Eleanor Markham, Senior Policy Analyst

Population ageing is accelerating across every G7 and G20 economy, yet financing systems still treat medical treatment and long-term support as if they were administratively adjacent and fiscally interchangeable. They are not. The result is a policy gap that shifts costs to households, obscures public liabilities, and leaves ministers managing care needs through institutions built to pay for diagnosis, acute intervention, and episodic recovery.

For health ministers, the phrase care health insurance should signal a structural mismatch, not a product category. Health insurance is designed around insurable clinical events. Care needs are different. They are recurrent, labour-intensive, and often tied to functional decline rather than a discrete medical episode. That distinction matters for fiscal planning, labour markets, and entitlement design.

Where governments fail to separate these functions clearly, three predictable problems follow. Households assume that health cover includes sustained personal support. Insurers price products against risks they can limit, while excluding the risks families are most likely to face over time. Public systems then absorb the residual burden through hospitals, means-tested social care, and unpaid family labour. Our earlier analysis of why health and care policy is more than a family affair shows how quickly that burden becomes a macroeconomic issue, not just a welfare concern.

This disconnect now belongs on the G7 and G20 agenda. It affects workforce participation, public expenditure, gender equity, and the resilience of health systems under demographic pressure. The central policy question is not whether countries need more insurance products. It is whether their financing architecture matches the true economics of care.

Table of Contents

- The Widening Gap Between Health and Care

- Defining the Divide Between Health Insurance and Long-Term Care

- A Typology of Global Care Financing Models

- Global Examples and Systemic Pressures in the G20

- Key Regulatory and Financing Challenges

- Elevating Care on the G7 and G20 Agendas

- Actionable Policy Recommendations for 2026

The Widening Gap Between Health and Care

Across the G20, population ageing and the rise of chronic disease are increasing demand for support that health insurance was not designed to finance. That design mismatch now sits at the centre of a wider governance problem. Ministers have built payment systems around diagnosis and treatment, while the fastest-growing pressures often come after discharge, outside hospitals, and inside households.

The result is a structural gap between what health systems pay for and what people need to live with frailty, disability, cognitive decline, or long recovery periods. Acute medicine can stabilise patients and extend life. It does not, on its own, provide months or years of supervision, assistance with daily activities, respite for unpaid carers, or a sufficient paid care workforce.

This matters because insurance is a financing instrument, not a care system.

The phrase care health insurance often blurs that distinction. It suggests that a single product can absorb risks that are operational, labour-intensive, and only partly insurable. In practice, insurance can fund treatment episodes, specialist access, diagnostics, and some post-acute services. It does not automatically create home-care capacity, improve labour standards in the care economy, or protect families from the time costs of unpaid care.

Policy design follows those definitions. When governments classify care needs as an extension of medical treatment, they tend to overestimate what insurance markets can do and underestimate the need for public purchasing, workforce planning, and cash or in-kind support for households. That is one reason the same country can expand health coverage yet still leave older people and people with disabilities exposed to high out-of-pocket costs or heavy reliance on relatives.

The political economy is clear. Underfunded care does not disappear from the system. It is shifted to families, usually women, and then reappears as lower labour-force participation, financial strain, and avoidable hospital use. For ministers looking at sustainable reform, a broader analysis of why health and care are more than a family affair provides the right frame.

For the G7 and G20, the non-obvious conclusion is that the disconnect between health and care is not only a social policy failure. It is also a macro-fiscal and governance failure. Countries that insure treatment but leave care fragmented end up paying more elsewhere, through hospital bottlenecks, delayed discharge, caregiver burnout, and weaker workforce participation.

Defining the Divide Between Health Insurance and Long-Term Care

Two systems with different purposes

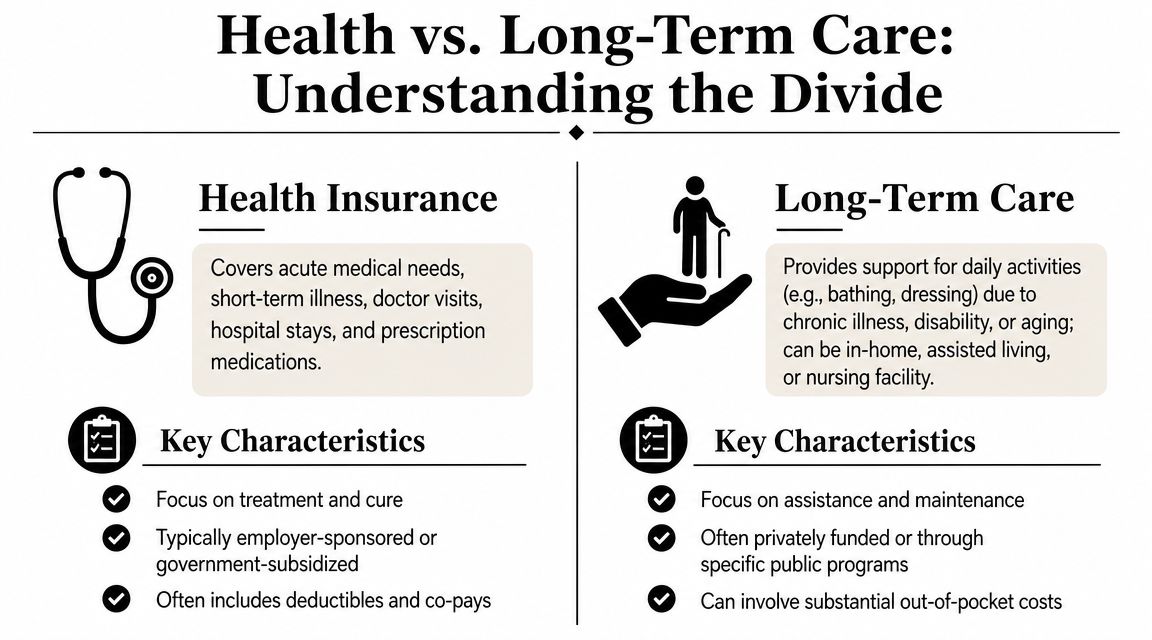

Health insurance and long-term care are often placed in the same political conversation because both involve illness, ageing, and cost. Functionally, though, they solve different problems.

A simple analogy helps. Health insurance is closer to car insurance after a crash. Long-term care is closer to ongoing support that keeps the vehicle usable day after day. One finances acute intervention. The other finances continuing assistance.

Health insurance usually centres on:

- Clinical treatment: doctor visits, hospital stays, diagnostics, procedures, and medicines.

- Acute events: illness, injury, flare-ups, and discrete episodes of medical need.

- Time-limited episodes: costs that rise around treatment and then fall when the event passes.

Long-term care usually centres on:

- Daily support: help with bathing, dressing, eating, supervision, or mobility.

- Chronic need: disability, cognitive decline, frailty, or conditions that don't resolve quickly.

- Persistent service demand: support delivered at home, in assisted settings, or in institutional care.

Why the distinction changes policy design

The financing logic diverges as well. Acute medical risk can often be pooled around uncertain but bounded episodes. Care risk is different. It can be prolonged, labour-intensive, and closely tied to age and dependency. That makes it harder to finance through a simple health insurance template without exclusions, co-payments, waiting periods, or narrow definitions of eligibility.

| Dimension | Health insurance | Long-term care |

|---|---|---|

| Core purpose | Treat illness and injury | Support daily functioning |

| Service profile | Clinical and episodic | Assistive and continuous |

| Main delivery setting | Clinics and hospitals | Home, community, residential settings |

| Policy challenge | Affordability of treatment | Sustainability of sustained support |

The term “care health insurance” only becomes useful when policymakers ask a sharper question: which part is financing treatment, and which part is financing dependency?

This distinction also explains persistent public confusion. Citizens facing delayed diagnosis or specialist referral may buy private health cover expecting a complete solution. They may then discover that insurance can accelerate some pathways while leaving broader care needs largely untouched. For ministers, the governance lesson is straightforward. Product design should never substitute for system design.

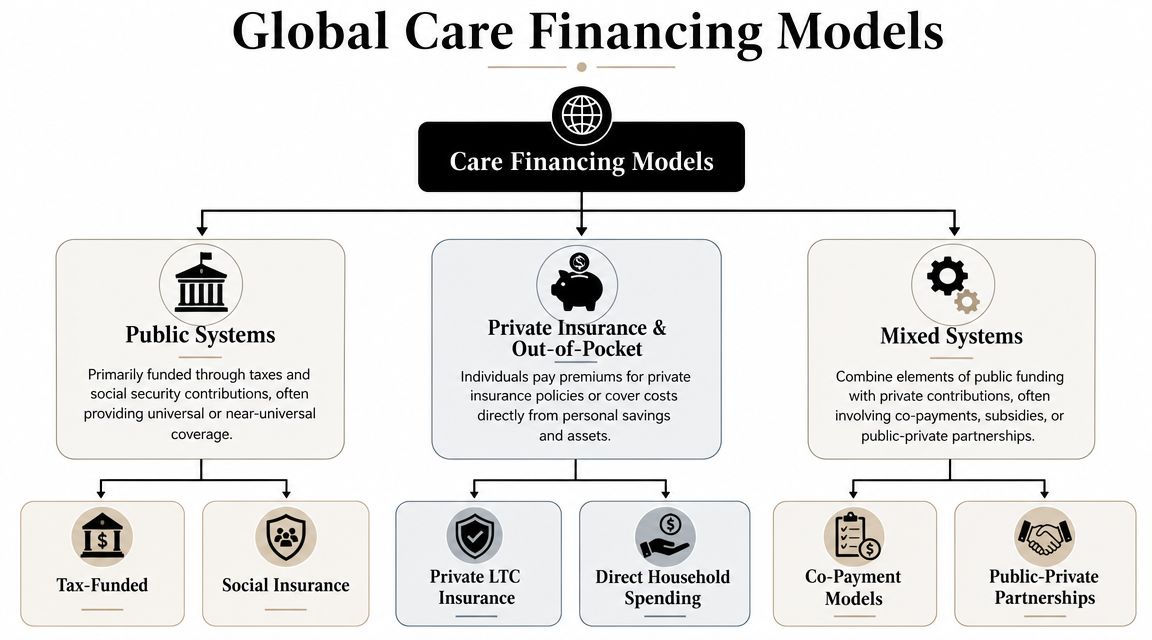

A Typology of Global Care Financing Models

Across the G20, the central policy problem is not whether countries finance health and care. It is that they often finance them through different institutional logics, with weak coordination between the two. That disconnect shapes who gets support, when costs shift to families, and how quickly demographic pressure turns into fiscal strain.

Three broad financing models recur internationally. Few countries fit neatly into one category, but the typology is still useful because it shows where risk sits and where systems fail.

Public systems

Public or social insurance models pool care risk through taxation, payroll contributions, or both. Their policy strength is straightforward. They treat dependency as a collective risk rather than a private misfortune, which improves equity and can spread costs across generations.

The harder question is operational. A legal entitlement to long-term care does not by itself produce workers, home-care capacity, or consistent local delivery. In several advanced economies, that gap between statutory coverage and actual access has become the defining weakness of public systems.

This matters for the G7 and G20 because ageing is no longer a future issue. It is already testing budget design, intergovernmental transfers, and labour supply, as seen in wider G20 performance on ageing populations.

Private insurance and out-of-pocket systems

Private models place more responsibility on individual premiums, savings, household assets, and employer-sponsored benefits. They can widen choice for higher-income households and create faster channels into selected services. They also tend to define benefits more narrowly, because insurers must limit exposure to long-duration and uncertain care needs.

That is the structural constraint. Private insurance works more easily for discrete medical episodes than for open-ended dependency. As noted earlier, supplementary private medical cover can expand even inside a universal health system. That growth does not resolve the underlying care financing problem, because long-term support remains difficult to insure on equal and affordable terms.

Where out-of-pocket spending plays a large role, the system often relies on an implicit buffer. Family labour, especially unpaid care by women. Ministers should treat that as a financing mechanism, not a cultural residual, because it conceals the true economic cost of underfunded formal care.

Mixed systems

Mixed systems combine public funding with private payment, co-payments, employer benefits, or private provision. In practice, this is the dominant model across high-income and middle-income economies. It reflects political reality. Governments fund a baseline, then households cover gaps in access, intensity, or quality.

Mixed systems can be stable if the public tier clearly defines what is guaranteed and if private spending sits above, rather than instead of, that floor. They become unstable when governments underfund core services and leave families to absorb residual risk without transparent rules. The result is often hidden rationing through waiting times, regional variation, asset depletion, or caregiver burnout.

For ministers, three tests matter more than the label attached to any model:

- What risk is pooled? Acute treatment, functional dependency, or a limited subset of both.

- Who absorbs costs when needs become prolonged? The treasury, social insurance funds, employers, insurers, or households.

- How is scarcity managed in practice? Through price, waiting, strict eligibility, workforce shortages, or uneven local supply.

The policy implication is broader than product design. “Care health insurance” is best understood as a sign of institutional ambiguity. It usually appears where states have built financing systems for treatment more clearly than for dependency, and where the boundary between the two is still being contested rather than governed.

Global Examples and Systemic Pressures in the G20

The UK access problem

Millions of people in England are waiting for NHS treatment. That fact matters beyond service management. It shows how quickly a system with universal entitlement can generate demand for supplementary cover when access becomes uncertain in practice.

The policy issue is not merely whether insurance exists. The issue is what insurance is being asked to solve. In the UK, private cover often operates as a mechanism for faster entry into diagnosis or elective treatment, while long-term care remains governed through a different and far more fragmented set of local authority rules, means tests, and household payments. That split is the governance problem. One financing channel responds to medical delay. Another leaves dependency risk only partly pooled.

As noted earlier, long waits have increased political interest in private cover. Ministers should read that trend carefully. Rising take-up of supplementary insurance does not show that the underlying settlement between health and care is coherent. It shows that households and employers are searching for workarounds when the public system cannot convert legal coverage into timely use.

This distinction has wider G20 relevance. Countries can preserve universal health insurance on paper while still shifting the operational burden of prolonged illness, disability, and frailty onto families. The result is a two-stage system. Acute care is nationally protected. Ongoing support is locally rationed, privately purchased, or informally provided.

For a broader demographic context, this analysis of G20 performance on ageing populations helps explain why these pressures are intensifying across advanced and emerging economies alike.

India and product adaptation

India presents a different policy pattern. The central pressure is not waiting times inside a mature universal system. It is the construction of risk pooling in a heterogeneous market where public provision, household spending, and private insurance all carry substantial weight.

That setting encourages insurers to design broad, modular product portfolios rather than a single care-specific line. From a policy perspective, that is a rational response to fragmented demand. Households may need protection against hospitalisation costs, catastrophic episodes, accident risk, or income shocks associated with illness, but that still does not create a clear financing architecture for long-term support needs such as supervision, daily living assistance, or extended home-based care.

The governance lesson is easy to miss. Product innovation can widen enrolment and segment risk more finely, especially across age bands and family structures. It does not resolve the deeper boundary problem between health insurance and care financing. If anything, it can obscure it. A market can offer more insurance products while still leaving dependency risk underfunded, poorly regulated, or dependent on unpaid family labour.

India therefore illustrates a broader G20 dilemma. In high-income systems, pressure appears through queues and supplementary cover. In middle-income systems, pressure appears through patchy pooling, uneven product design, and sharp differences in what households can buy. In both cases, the phrase "care health insurance" signals institutional ambiguity rather than policy clarity.

For G20 ministers, the comparative conclusion is straightforward. The core challenge is not choosing between public and private finance in the abstract. It is defining which needs are insured, which are tax-financed, which remain means-tested, and which are left to families by default. Where that boundary remains unclear, markets expand around the gap instead of closing it.

Key Regulatory and Financing Challenges

A persistent policy error runs through both advanced and emerging economies. Ministers insure episodes of illness, then leave dependency risk to fragmented local budgets, means tests, or unpaid family care. That design failure creates fiscal pressure long before it appears in insurance claims.

Fiscal and workforce strain

The binding constraint is often delivery capacity rather than formal coverage. Long-term care requires a large workforce, stable provider payment, inspection, and clear rules for transitions from hospital to home or residential support. If those institutions are weak, expanding insurance products changes who pays first, not whether care is available.

This matters for macro-fiscal planning. Care needs rise with population ageing, lower household size, and higher female labour-force participation, yet many public finance frameworks still treat care as a residual welfare function rather than core social infrastructure. The result is predictable. Hospitals retain patients who are medically fit for discharge, families reduce paid work to fill gaps, and insurers design around unclear public entitlements instead of complementing them.

A financing debate framed only around medical risk pooling misses that institutional problem. A stronger discussion of financing universal health coverage and care obligations has to specify who funds daily living support, supervision, respite, and post-acute recovery once clinical treatment ends.

Fragmented regulation and unequal access

Regulatory fragmentation then magnifies inequity. In the UK, private medical insurance coverage is disproportionately concentrated among higher-income households, a pattern documented by the Institute for Fiscal Studies in its analysis of NHS waiting times and private healthcare. The policy significance goes beyond distributional fairness. It shows how supplementary markets can expand fastest where public bottlenecks are most visible, even if those markets do little to solve underlying care deficits.

Three regulatory problems follow.

- Benefit ambiguity: Households often face unclear boundaries between medical treatment, rehabilitation, personal care, and long-term support. Products marketed around health security may exclude the services that matter most once functional limitations begin.

- Risk segmentation: Employer-sponsored and higher-income purchasers gain faster access to diagnostics or elective treatment, while lower-income households remain exposed to waiting lists, out-of-pocket care costs, and unpaid caregiving burdens.

- Siloed oversight: Health insurers, long-term care providers, and local social care authorities are frequently regulated through separate statutes, budgets, and reporting systems. That weakens accountability for outcomes that sit between sectors.

Policy test: If supplementary insurance grows while baseline care capacity, eligibility rules, and workforce supply remain unchanged, access stratification will deepen and public systems will absorb the hardest cases.

For G7 and G20 governments, the regulatory task is therefore sharper than standard insurance reform. They need a common classification of care benefits, a transparent allocation of financial responsibility across ministries and levels of government, and reporting systems that record unmet need rather than burying it in household labour. Without those levers, the phrase "care health insurance" will continue to describe an institutional gap more than a coherent financing solution.

Elevating Care on the G7 and G20 Agendas

Why leaders should treat care as macroeconomic policy

Across the G7 and G20, population ageing, lower fertility, and rising chronic disease are increasing demand for long-term support faster than many financing systems can adapt. That gap is no longer a narrow social policy issue. It affects labour supply, fiscal sustainability, household consumption, and political confidence in the state.

The core governance problem is the persistent mismatch between the word "care" and the institutions attached to "health insurance." Insurance systems are generally designed to finance episodic, clinically defined interventions. Care needs are different. They are continuous, labour-intensive, and often linked to functional decline rather than a discrete medical event. As a result, governments frequently insure treatment while underfunding support with daily living, rehabilitation, and extended assistance outside hospitals.

That distinction matters for macroeconomic performance. Where formal care systems are thin, families absorb the shock through unpaid work, reduced working hours, and delayed labour-force re-entry, especially for women in mid-life. Health ministers therefore have a direct interest in care financing even when social care sits in another ministry's portfolio.

Private insurers can widen options for higher-income households and reduce some short-term pressure on public systems. They cannot resolve the structural financing problem on their own. Voluntary products pool risk imperfectly for long-duration dependency, and insurers have limited incentives to cover open-ended care obligations without clear public rules on eligibility, benefits, and cost sharing. The result is a familiar policy failure. Governments tolerate fragmentation, markets fill selected gaps, and households remain exposed to the most expensive and persistent risks.

What international cooperation can add

G7 and G20 cooperation can improve policy discipline in three areas.

First, leaders can establish a shared policy vocabulary. Many countries still classify the same service differently across health insurance, disability support, elder care, and local government assistance. That prevents meaningful comparison of spending, coverage, and unmet need. A common taxonomy would help ministers identify whether systems are financing medical recovery, long-term assistance, or household substitution for missing public services.

Second, summit processes can move care from a residual welfare topic into the core economic agenda. Finance ministries tend to see care spending as a cost line, even though inadequate care provision suppresses employment, weakens tax capacity, and shifts expenses into hospitals and emergency settings. A G7 or G20 statement that treats care infrastructure as part of productive capacity would change domestic budget debates.

Third, multilateral forums can improve accountability. Countries report extensively on health expenditure, insurance enrolment, and hospital capacity. They report far less consistently on unpaid caregiving, waiting times for long-term support, workforce shortages in home and community care, or the share of household spending devoted to non-medical assistance. What is not measured is routinely left unfunded.

A recent summit conversation captures the scale of the agenda:

For G7 and G20 health ministers, the strategic task is clear. Treat care financing as a cross-government economic reform, not as a marginal extension of health insurance. Countries that fail to make that shift will continue to insure episodes of illness while leaving the longer arc of dependency to families, local authorities, and overstretched providers.

Actionable Policy Recommendations for 2026

Ageing is increasing demand for care in every G7 and G20 economy, yet many financing systems still treat extended support with daily living, supervision, and long-duration dependency as outside the main insurance architecture. The 2026 policy task is therefore institutional, fiscal, and regulatory at the same time. Health ministers need to close the gap between medical coverage and care provision before demographic pressure turns a design flaw into a broader failure of state capacity.

National policy levers

The first priority is to define responsibilities with precision. Where health insurance stops and long-term care obligations begin, the law should say so clearly, and budget systems should reflect that boundary. Ambiguity looks politically convenient in the short term, but it usually produces hidden rationing, uneven local access, and rising household exposure to costs that were never transparently assigned.

A credible national reform package should include:

- Create integrated care financing strategies. Give health, social care, labour, and treasury ministries a joint mandate, shared expenditure reporting, and a timetable for reform. This makes cost-shifting easier to detect and harder to defend.

- Set minimum care entitlements in statute or regulation. Citizens need a clear statement of what public systems cover, what is means-tested, what remains voluntary, and when co-payments apply.

- Regulate private insurance as a supplement, not a substitute. Private products can cover gaps, but they should not become the default mechanism for financing predictable age-related care needs that public systems have chosen not to define.

- Review benefit design and pricing tools through an equity lens. As noted earlier, some insurance products use age-linked cost sharing and waiver structures to manage risk. Policymakers should study these mechanisms for their distributional effects, especially whether they shift more cost onto older adults precisely when need is rising.

- Build data systems around care dependency, not only medical use. Hospital admissions are measured closely. Hours of home support, waiting periods for assessment, unpaid caregiving intensity, and provider exit rates are often not. That reporting gap distorts policy.

Sequencing matters. Countries that begin with product regulation but avoid entitlement reform usually end up managing symptoms rather than correcting the financing model underneath them.

Multilateral actions

The G7, G20, WHO, and development banks should treat care financing as a shared governance problem with macroeconomic consequences. Fragmented national definitions have made cross-country learning harder than it should be. Ministers are often comparing systems that use the same terms for very different benefits, funding sources, and eligibility rules.

Three multilateral actions would improve policy traction in 2026.

- Adopt a common taxonomy for care financing. Distinguish acute medical insurance, post-acute rehabilitation, long-term care, disability support, and household cash benefits in a way that allows valid comparison.

- Create a joint health-finance working group under the G20. Care reform fails when finance ministries enter late and only to contain spending. A formal process should assess labour market effects, fiscal sustainability, and the hospital costs generated by underfunded care systems.

- Support implementation capacity in middle-income systems. Technical assistance should cover eligibility assessment, purchasing models, workforce planning, consumer protection, and local government accountability.

- Publish operational casebooks, not just summit communiqués. Ministers need examples of how countries assigned responsibilities, financed transitions, and limited cost-shifting across sectors.

The strategic error for 2026 is to leave care in the policy margin while insuring only episodes of illness. Governments that continue to separate the two will face the same pattern repeatedly. Hospital pressure rises, families absorb unpaid burdens, private spending fills gaps unevenly, and public dissatisfaction grows because formal coverage does not match lived need.

For more evidence-based analysis on global health financing, G7 and G20 priorities, and the policy choices shaping international cooperation, follow Global Governance Media.