By Dr Eleanor Markham

Global value chains account for about 70% of international trade, according to the OECD's overview of global value and supply chains. That single benchmark changes how G20 leaders should think about trade policy. The decisive question is no longer only what a country exports. It is where domestic firms sit inside cross-border production networks, which inputs they depend on, which services they contribute, and which chokepoints they can't control.

That shift matters because recent disruptions have exposed a hard truth. A state can appear well positioned in headline trade figures and still be strategically exposed if key components, logistics routes, finance, software, or processing stages sit elsewhere. Equally, a country can wield far more influence than its merchandise exports suggest if it controls design, standards, insurance, legal architecture, digital infrastructure, or specialised business services.

For G7 and G20 governments, a global value chain is now part of economic statecraft. It affects inflation, industrial capability, sanctions resilience, defence preparedness, climate transitions, and diplomatic influence. Policymakers who still read trade through the old lens of final goods will miss the true structure of power.

A broader geopolitical framing is already overdue, as argued in The global system taking stock. The challenge now is to convert that framing into practical decisions on resilience, diversification, and governance.

Table of Contents

- The Hidden Wiring of the World Economy

- From Supply Chain to Value Chain A Critical Distinction

- The New Geopolitical Map of Trade and Power

- Resilience and Vulnerability Three Case Studies

- Governing a System Without a Centre

- Strategic Policy Levers for G20 Decision-Makers

- Conclusion Forging a New Consensus on Global Trade

The Hidden Wiring of the World Economy

Global value chains are the hidden wiring of the world economy because they organise production across borders before goods or services ever reach a final buyer. A finished export often reflects design in one country, finance in another, components from several more, and logistics and compliance managed across multiple jurisdictions. What matters strategically is not the final shipment alone, but the sequence of value-adding activities behind it.

For the UK and other G20 economies, this is especially important because competitiveness often depends on combining imported services, parts, and raw materials with domestic strengths in design, logistics, advanced manufacturing, finance, and professional services. The OECD's treatment of global value chains makes this point clearly. Cross-border production networks shape trade outcomes, and disruptions in tariffs, shipping, exchange rates, or customs processes can hurt firms even when they are not direct exporters of final goods.

Why leaders should treat GVCs as strategic infrastructure

A global value chain isn't just an economic concept. It is a map of dependence.

When political tensions rise, when ports slow, or when a regulatory change interrupts intermediate goods, the impact spreads through production stages rather than stopping neatly at a border. That's why ministries of trade, industry, finance, energy, and foreign affairs increasingly confront the same problem from different angles. Each is trying to manage exposure within an interconnected production system.

Practical rule: If a government can't identify where domestic firms source critical inputs and where they add the highest-value functions, it can't judge its real economic resilience.

The strategic implication is straightforward. States that understand their role in a global value chain can protect critical nodes without retreating into blanket protectionism. States that don't will overreact to visible shortages while underestimating deeper structural risks.

The policy lens has changed

This is also why recent disruptions have had such political force. They have shown that economic openness without mapping, monitoring, and contingency planning creates fragility. But they have also shown that full self-sufficiency is rarely credible for complex economies.

A more serious agenda begins with a different question. Instead of asking how to bring everything home, governments should ask which functions must remain secure, which dependencies are tolerable, and which foreign links are sources of strength.

From Supply Chain to Value Chain A Critical Distinction

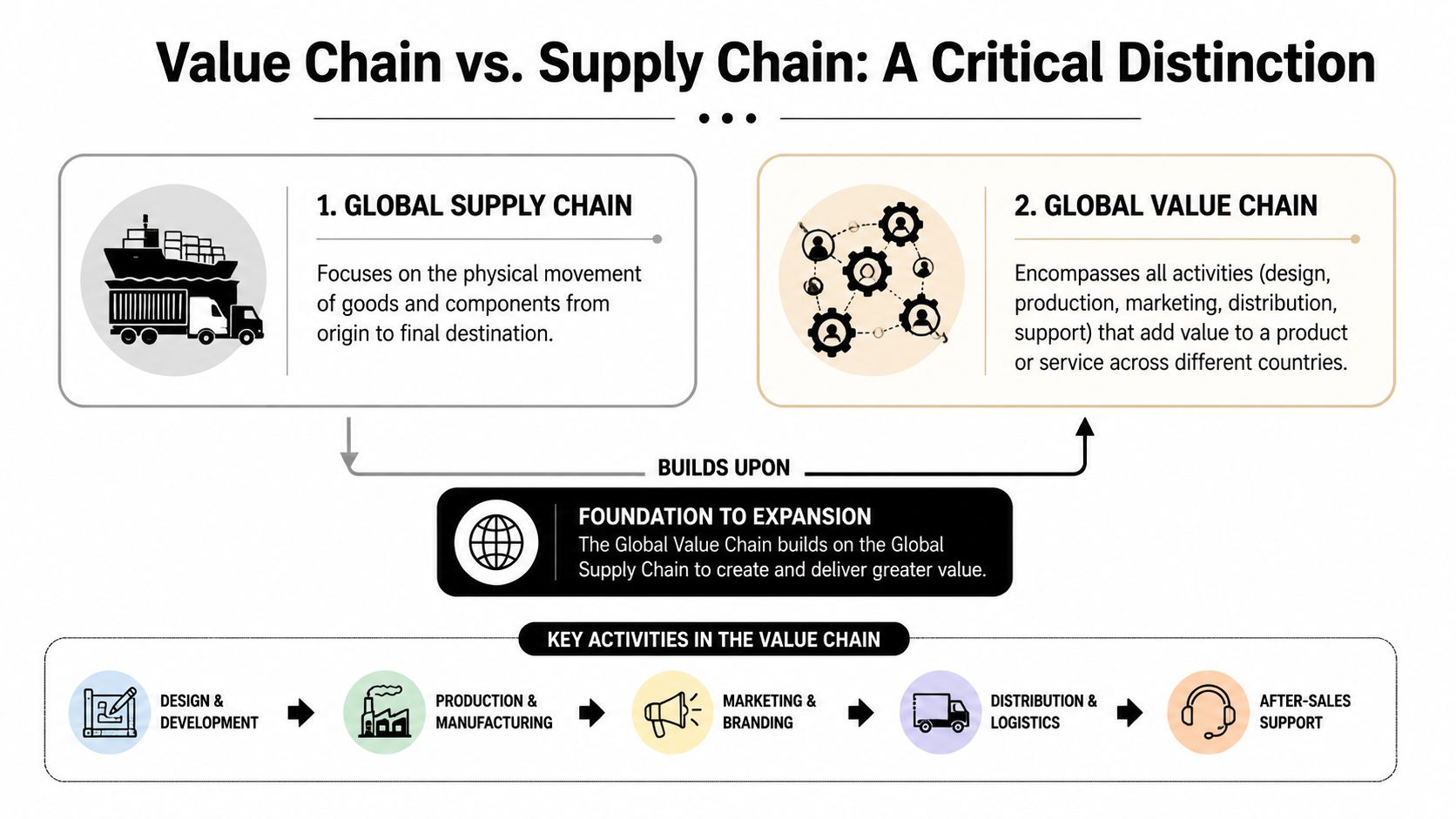

Most policymakers are more familiar with the phrase global supply chain than global value chain. That familiarity can mislead. A supply chain tracks the movement of goods and components from origin to destination. A value chain asks a more important question for public policy. Where is value created?

Take a complex consumer device such as a smartphone. One country may specialise in chip design. Another may produce precision components. Assembly may happen elsewhere. Branding, software, legal protection, finance, marketing, and after-sales services may sit in still other jurisdictions. The physical object moves through a supply chain. The economic gains are distributed through a value chain.

What the distinction changes in practice

This distinction changes industrial strategy.

A government focused only on supply chains tends to prioritise cargo movement, inventories, transport links, and customs speed. Those are important, but they are only part of the picture. A government focused on value chains asks whether domestic firms control high-value stages such as research and development, standards setting, software integration, financing, certification, or specialised services.

That difference explains why two countries can appear connected to the same product and derive very different benefits from it.

| Lens | Core question | Policy implication |

|---|---|---|

| Supply chain | How does the product move? | Improve logistics, border processes, storage, transport reliability |

| Value chain | Where is value added? | Strengthen high-value capabilities, services, innovation, standards, finance |

Why services matter more than many trade debates admit

Traditional debates often err by treating manufacturing as the whole story and services as peripheral. In reality, many of the most defensible and profitable stages in a global value chain sit outside factory floors. Design, software, insurance, legal structuring, management, and financing can determine who captures value even when production is geographically dispersed.

A country can lose an assembly contract and still retain strategic influence if it controls the architecture around the product.

For economies with strong business services, higher education, digital capabilities, or advanced research ecosystems, the aim shouldn't be to replicate every stage of production. It should be to secure the stages that anchor wider domestic value creation and make the economy harder to bypass.

That is why the phrase global value chain is more useful than supply chain for ministers making long-term decisions. It directs attention to where national capability sits, where dependence is rising, and which functions are worth defending.

The New Geopolitical Map of Trade and Power

The old trade map highlighted exporters and importers. The new one highlights nodes, chokepoints, and dependencies. Power now lies not only in market size or tariff policy, but in control over strategic stages of production. A government that hosts a critical node in a global value chain can shape outcomes far beyond its share of final goods exports.

That is why geoeconomics has become more granular. The key issue is no longer only whether countries trade. It is whether they can weaponise interdependence by influencing a narrow but indispensable stage in finance, technology, logistics, standards, or production. This is the practical backdrop to current debates on de-risking, friend-shoring, export controls, and strategic autonomy, including the wider challenge examined in confronting the US China split in the world trading system.

Why position matters more than volume

The most useful analytical tools here are upstreamness and downstreamness. As explained in the CEPR discussion of global value chain positioning, these indicators help policymakers identify where an economy sits in global production sequences. A changing position can reveal whether a country is moving toward higher-value knowledge hubs or toward lower-margin, trade-sensitive assembly segments.

The significance is that position often determines bargaining power.

- Upstream roles often include research, design, specialised inputs, software, finance, and enabling services.

- Downstream roles often sit closer to assembly, distribution, or final delivery.

- Mixed positions can be economically successful, but they require clear awareness of where dependence is concentrated.

A country that dominates a small but essential upstream function may hold more strategic advantage than one that exports larger gross volumes from easily replaceable downstream activity. Gross trade statistics don't always reveal that distinction.

The central policy mistake is to treat all trade exposure as equal. It isn't. Exposure to a substitutable supplier is different from exposure to a chokepoint.

De-risking is a structural response

Governments are now adjusting to that reality. They're reassessing whether efficiency alone should determine sourcing decisions, especially in sectors linked to health security, advanced technology, energy transition, and defence capability. Firms are doing the same, often by shortening chains, adding inventory buffers, qualifying alternative suppliers, or regionalising some stages.

This short explainer is useful background for decision-makers weighing those trade-offs:

These shifts are not simple reversals of globalisation. They are a redesign of exposure. In practice, de-risking means preserving cross-border production where it creates value, while reducing dependence on single points of failure that can be disrupted by conflict, coercion, sanctions, or natural shocks.

For G20 leaders, the policy test is whether interventions improve resilience without degrading the productive complexity that makes economies competitive in the first place.

Resilience and Vulnerability Three Case Studies

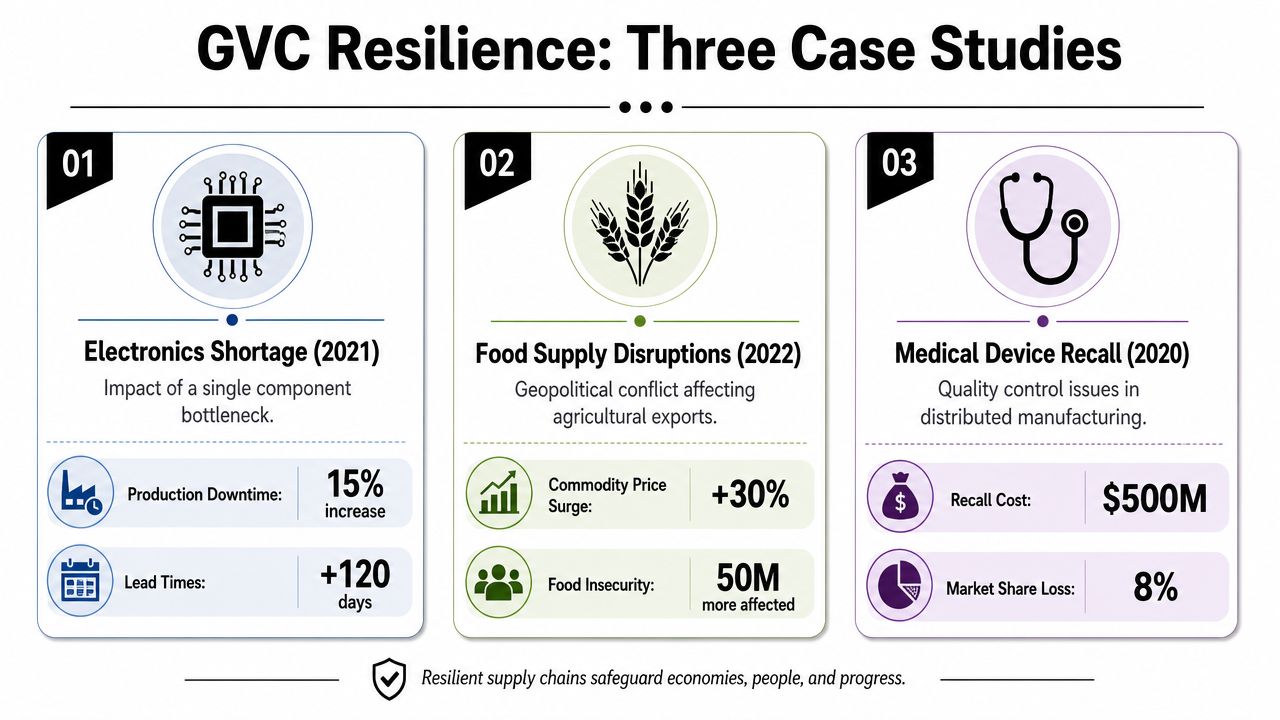

General principles become clearer when governments confront concrete failures. Three recent areas illustrate how a global value chain can become a source of resilience or vulnerability depending on concentration, substitutability, and state capacity.

PPE and the politics of concentration

The scramble for personal protective equipment during the pandemic exposed a basic problem. Many governments had procurement systems designed for cost efficiency, not emergency stress. When demand surged and borders tightened, buyers discovered that nominal market access did not guarantee physical access.

The lesson wasn't that all medical production should be repatriated. It was that public authorities need visibility into supplier concentration, surge capacity, and emergency substitution. In sectors tied directly to public safety, resilience requires more than a contract and a warehouse. It requires pre-agreed alternatives, domestic conversion capacity, and procurement rules that value continuity as well as price.

A second lesson is political. During crisis conditions, governments prioritise domestic needs. That makes dependency on a narrow set of foreign producers especially risky when the product is essential and time-sensitive.

Semiconductors and strategic choke points

The semiconductor industry shows a different form of vulnerability. Here the issue is not just shortage. It is the concentration of highly specialised capabilities in a small number of locations and firms. Production depends on intricately interlinked stages, from design and intellectual property to fabrication, testing, packaging, equipment, materials, and software.

That structure makes semiconductors a textbook case of geostrategic dependence.

- Capability is layered. Different countries and firms control distinct steps that are not easily replaced.

- Time matters. When disruption hits, rebuilding capacity is slow because tacit knowledge, equipment ecosystems, and trusted supplier relationships can't be recreated quickly.

- Policy spillovers are large. Export controls, investment screening, and industrial subsidies in one jurisdiction affect firms and governments far beyond that jurisdiction.

For G20 leaders, the semiconductor lesson isn't that everyone should build the full stack. That would be economically wasteful for most countries. The lesson is that strategic sectors require realistic mapping of what can be substituted, what must be stockpiled, what can be allied, and what domestic capability is indispensable for national resilience.

Decision test: Don't ask whether your country participates in a critical sector. Ask whether it participates in a way that can still function under stress.

Renewables and the next dependency cycle

The renewable energy transition is creating new production networks with their own strategic pressures. Clean technology deployment depends on minerals, processing, component manufacturing, engineering, finance, grid integration, and long-term maintenance. The transition reduces some dependencies while creating others.

That has major implications for industrial policy.

A country can appear to advance decarbonisation while deepening external dependence if it relies heavily on imported processed inputs, specialised components, or foreign-controlled processing stages. Conversely, a country may strengthen its strategic position by specialising in grid software, project finance, materials processing, precision engineering, or standards and certification rather than only in final assembly.

The renewable case also shows why governments need a whole-chain view. Mining policy alone won't secure resilience. Neither will a narrow focus on final products. The more serious task is to identify where value, control, environmental risk, and political influence sit across the chain.

A useful way to organise those judgements is to compare sectors against four criteria:

| Criterion | PPE | Semiconductors | Renewables |

|---|---|---|---|

| Urgency of disruption | Immediate public health impact | Fast industrial and security impact | Slower but system-wide impact |

| Ease of substitution | Sometimes possible, often limited in crisis | Often very difficult | Varies by material and component |

| Role of state planning | High | Very high | High |

| Best policy posture | Preparedness and surge capacity | Allied coordination and selective capability building | Diversification and long-horizon industrial strategy |

These cases point to the same conclusion. Resilience doesn't come from eliminating interdependence. It comes from understanding which interdependence is manageable, which is dangerous, and which can be turned into strategic advantage.

Governing a System Without a Centre

Global value chains are highly organised in practice but weakly governed in aggregate. Firms coordinate contracts, standards, finance, logistics, and compliance across borders every day. Public governance remains fragmented by national jurisdiction, sectoral silos, and outdated trade categories.

That mismatch matters because the rules were largely built for a world in which trade meant shipping final goods across borders. Today, production is split across many jurisdictions and often bundled with services, data, intellectual property, and financing. Governance still struggles to see the whole system, let alone steer it.

Why measurement is a governance issue

One of the most important governance advances has been statistical, not diplomatic. The UN Statistics Division's Global Value Chains initiative was created to improve measurement of trade in value added because traditional gross trade statistics can misrepresent the true economic contribution of services-heavy economies such as the UK.

This is not a technical footnote. It changes the policy baseline.

If governments rely only on gross trade data, they may overestimate the importance of final assembly and underestimate the role of domestic services, research, management, and other high-value functions embedded in exports. They may also miss where imported content is essential to domestic competitiveness. Better measurement therefore shapes better decisions on industrial strategy, border policy, and resilience planning.

Rules still lag behind production reality

Even with better data, governance remains incomplete. A typical global value chain cuts across trade law, investment policy, competition rules, labour standards, digital regulation, customs administration, security screening, and environmental governance. No single institution governs all of that coherently.

Three gaps are especially significant:

- Fragmented rule-making: Trade ministries may liberalise flows that security agencies later restrict, while industrial subsidies create tensions with competition and fiscal objectives.

- Uneven treatment of services and data: Many high-value functions in a global value chain rely on digital coordination, software, design, and business services that don't fit neatly into goods-centred frameworks.

- Weak chain-level accountability: Environmental and labour harms often occur at lower-visibility stages where legal responsibility is diffuse and enforcement capacity varies.

Better governance starts with a more honest premise. States are not regulating isolated imports and exports. They are regulating slices of shared production systems.

For G20 leaders, the implication is practical. They need institutions that can join trade, security, industrial, and statistical analysis rather than treating them as separate policy worlds. Without that integration, governments will continue to govern interconnected production through disconnected tools.

Strategic Policy Levers for G20 Decision-Makers

The right objective isn't self-sufficiency. It is resilience through diversification. That means preserving the gains from cross-border production while reducing the chance that one disrupted node can impair an entire sector. G20 governments have enough market weight to shift business incentives if they act with precision.

The case for active policy is strengthened by a simple fact. Modern trade is built around cross-border production networks, not only final-goods exchange. That is why practical reform matters more than abstract declarations, a point that sits close to the wider trade agenda explored in dynamic policies to reshape trade.

Build resilience through diversification

The first lever is visibility. Governments can't manage vulnerabilities they can't see.

That requires public-private mechanisms that map critical inputs beyond first-tier suppliers. In many sectors, the visible contractor is not the actual point of fragility. The weak link sits several tiers deeper in a processor, software vendor, logistics service, or specialised materials producer. Ministries should build standing capabilities to identify those bottlenecks and test them under stress scenarios.

The second lever is diversification. This doesn't always mean moving production home. Often it means ensuring firms qualify multiple suppliers across jurisdictions, support alternative transport routes, and avoid procurement systems that reward the cheapest concentrated option.

Use industrial policy with discipline

Industrial policy is now back at the centre of G20 strategy. Used well, it can support capability in sectors where market incentives alone underprovide resilience, innovation spillovers, or security. Used badly, it becomes a subsidy contest that fragments production and wastes fiscal capacity.

A disciplined approach has four features:

- Target functions, not slogans. Support should focus on clearly identified bottlenecks, enabling technologies, or strategic services rather than broad claims of national champions.

- Tie support to ecosystem development. Skills, testing capacity, infrastructure, regulatory clarity, and finance often matter more than the headline subsidy.

- Build review mechanisms. Programmes should be reassessed against resilience, competitiveness, and spillover effects, not left on autopilot.

- Coordinate with allies where possible. In highly specialised sectors, shared capability is often more credible than duplication.

Modernise multilateral cooperation around production networks

The third lever is international. Since global value chains span multiple jurisdictions, no major economy can secure them alone.

A practical G20 agenda should include:

- Common approaches to transparency: Shared risk monitoring for critical sectors, using compatible classifications and reporting where possible.

- Faster customs and regulatory coordination: Intermediate inputs lose value when delays are unpredictable, even if tariffs are low.

- Sector-specific cooperation: Governments should use targeted agreements where they reduce friction in strategic chains without creating incompatible rulebooks.

- Better integration of services into trade policy: High-value services are often the glue that holds a chain together.

None of this requires a return to naive hyperglobalisation. It requires competence. Governments should distinguish between legitimate resilience measures and blunt restrictions that raise costs without reducing strategic vulnerability.

Smart GVC policy narrows dangerous dependencies while preserving productive interdependence.

For decision-makers, the standard should be clear. Every intervention should answer three questions. Does it reduce exposure to a genuine choke point? Does it preserve or strengthen domestic value creation? Can it work in concert with partners rather than against them?

Conclusion Forging a New Consensus on Global Trade

A global value chain is no longer a specialist trade concept. It is a working map of economic power. It shows where value is created, where risks are concentrated, and where governments retain or lose strategic room for manoeuvre.

That is why G20 leaders need to move beyond the old debate between openness and protection. The actual task is finer grained. They must identify which cross-border links increase capability, which create dangerous concentration, and which rules no longer fit the structure of production. Better measurement, targeted diversification, disciplined industrial policy, and more coherent international coordination all follow from that diagnosis.

The stakes are larger than trade performance alone. Global value chains now shape health security, digital capability, energy transition, inflation resilience, and geopolitical influence. Managing them well has become a core test of state capacity.

The next G20 cycle should treat this as a governing priority. Not because interdependence can be unwound, but because it must be managed with far more realism and discipline than in the past.

Global Governance Media helps policymakers, business leaders, and analysts track the ideas shaping G7 and G20 decisions on trade, resilience, climate, health, and economic governance. If you want sharper briefings and summit-focused analysis on issues like the global value chain, follow Global Governance Media.