By Eleanor Voss, Senior Fiscal Analyst

When people ask, “Is Britain bankrupt?”, they usually mean something narrower and more urgent: has the UK reached a point where its debt burden sharply limits what government can do at home and abroad? That's the right question. The bankruptcy label sounds dramatic, but it collapses several different issues into one slogan and obscures the policy choices that matter.

For G7 finance ministers, the useful distinction isn't between panic and reassurance. It's between a country that has lost the basic capacity to finance itself and a country that still has market access but faces tightening constraints from debt service, refinancing risk, weak growth and political fatigue. Britain is in the second category. That is serious enough.

Table of Contents

- Framing the Question on UK Solvency

- Sovereign Default versus National Bankruptcy

- The UKs Fiscal Health A Data Snapshot

- Reading the Market Signals on UK Risk

- Historical Parallels Crises and Recoveries

- Future Scenarios and Difficult Policy Levers

- Conclusion Britains Constrained Role on the World Stage

Framing the Question on UK Solvency

The phrase “Britain bankrupt” imports a corporate and household concept into sovereign finance. It sounds intuitive, but it isn't analytically sound. A sovereign that borrows in its own currency doesn't enter bankruptcy in the same way a household, company or local authority might.

That doesn't mean the UK is comfortable. It means the relevant test is different. The questions that matter are whether fiscal policy is sustainable, whether debt service is crowding out public priorities, and whether market confidence can be maintained if growth remains weak.

For a G7 audience, this distinction matters because the UK isn't an isolated case. A large advanced economy with debt around the size of its annual output, a persistent deficit and heightened refinancing sensitivity can still function normally for long periods. But that same country can also lose room for manoeuvre in defence, industrial policy, energy security and crisis response well before any legal concept of insolvency enters the discussion.

Britain's core problem isn't bankruptcy. It's the narrowing of fiscal space in a more expensive interest-rate environment.

The political risk is that the wrong question produces the wrong debate. If ministers argue over whether the UK is “bankrupt”, they invite either melodrama or denial. If they ask instead how much policy capacity has already been eroded by debt service and weak trend growth, they move closer to a useful diagnosis.

Three practical implications follow.

- Language matters: “Bankrupt” suggests a cliff-edge event. Fiscal erosion usually works through cumulative pressure on budgets, confidence and policy credibility.

- Institutions matter: A country with a tax base, a domestic bond market and monetary sovereignty operates under a different constraint set from a debtor that depends on foreign-currency funding.

- Timing matters: Sovereign stress often becomes visible late. Before that point, it shows up as harder trade-offs, not missed pay cheques.

That is why the question “Is Britain bankrupt?” is best answered with a disciplined refusal to apply the term in its strictest sense, followed by a closer examination of solvency, liquidity and market tolerance.

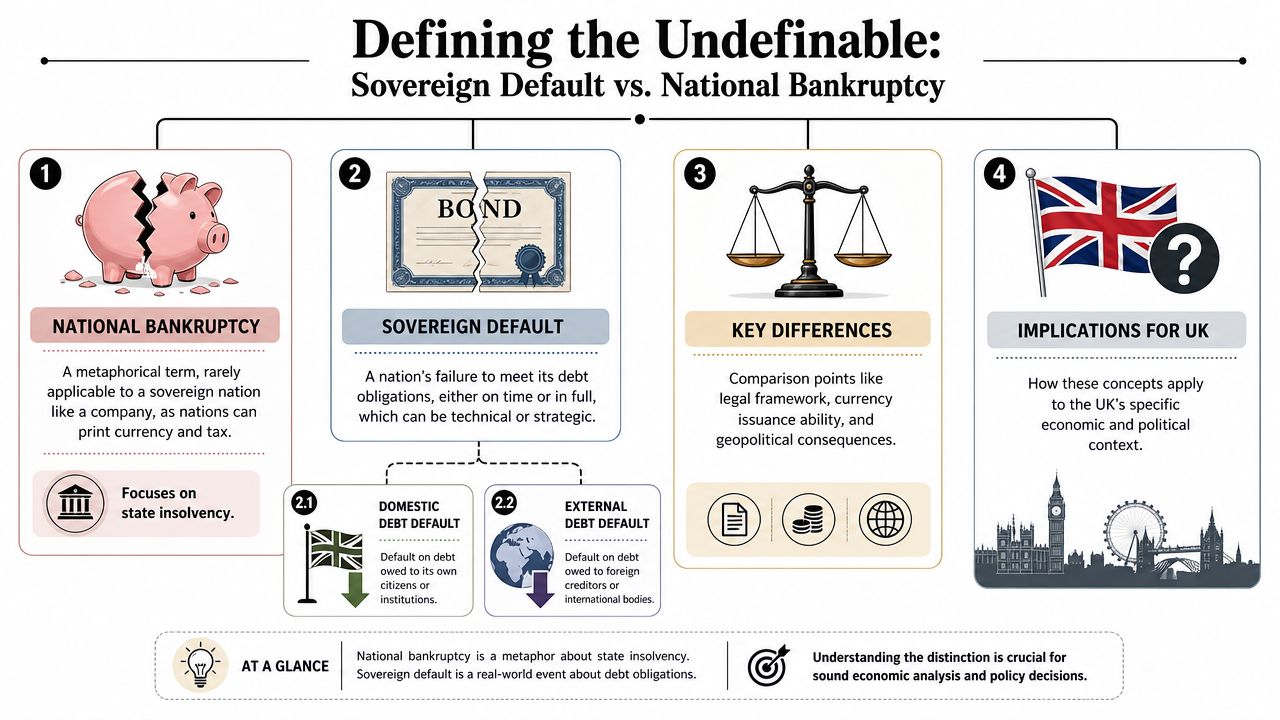

Sovereign Default versus National Bankruptcy

Why the headline misleads

A state doesn't pass through a standard bankruptcy court procedure. That is the first analytical error embedded in the headline. In England and Wales, insolvency is a defined legal process for individuals, not a template for sovereign finance. Official data show 651 bankruptcies in June 2024, and in the 12 months ending 30 June 2024 there was about one insolvency for every 457 adults, or 21.9 per 10,000 adults, according to the individual insolvency statistics commentary. The same release shows that bankruptcies were 7% of all individual insolvencies in the year to June 2024, while 57% were IVAs and 35% were DROs.

Those figures tell us something real about household financial distress and the legal routes people use to manage it. They do not tell us that the British state is bankrupt.

A country like the UK can tax, issue bonds and borrow in sterling. That gives policymakers options unavailable to a household. It doesn't remove constraints, but it changes their nature. For readers interested in how sovereign restructurings differ from corporate workouts, this analysis of managing sovereign debt restructuring is a useful companion.

The terms that matter

Three concepts matter more than “bankruptcy”.

| Term | What it means in practice | Why it matters for the UK |

|---|---|---|

| Default | Failure to meet debt obligations on time or in full | A sovereign can default without going through any standard bankruptcy process |

| Insolvency | A deeper inability to meet obligations over time | Hard to apply neatly to a currency-issuing sovereign |

| Illiquidity | A cash-flow or market-access strain | Often the more relevant near-term sovereign risk |

The UK's present debate sits at the boundary between fiscal strain and affordability risk, not at the endpoint of legal bankruptcy. The distinction is more than semantic.

Practical rule: When a sovereign borrows in its own currency, the immediate risk usually lies in inflationary finance, rising yields, political retrenchment or confidence loss before it lies in any textbook notion of bankruptcy.

That's why serious analysis asks whether the government can continue financing itself at tolerable cost, whether debt interest is squeezing choices elsewhere, and whether institutional credibility is strong enough to prevent a refinancing scare from becoming a broader macroeconomic event.

The UKs Fiscal Health A Data Snapshot

How strained are the UK's public finances if one sets aside the language of “bankruptcy” and looks at the balance sheet, cash flow, and refinancing calendar?

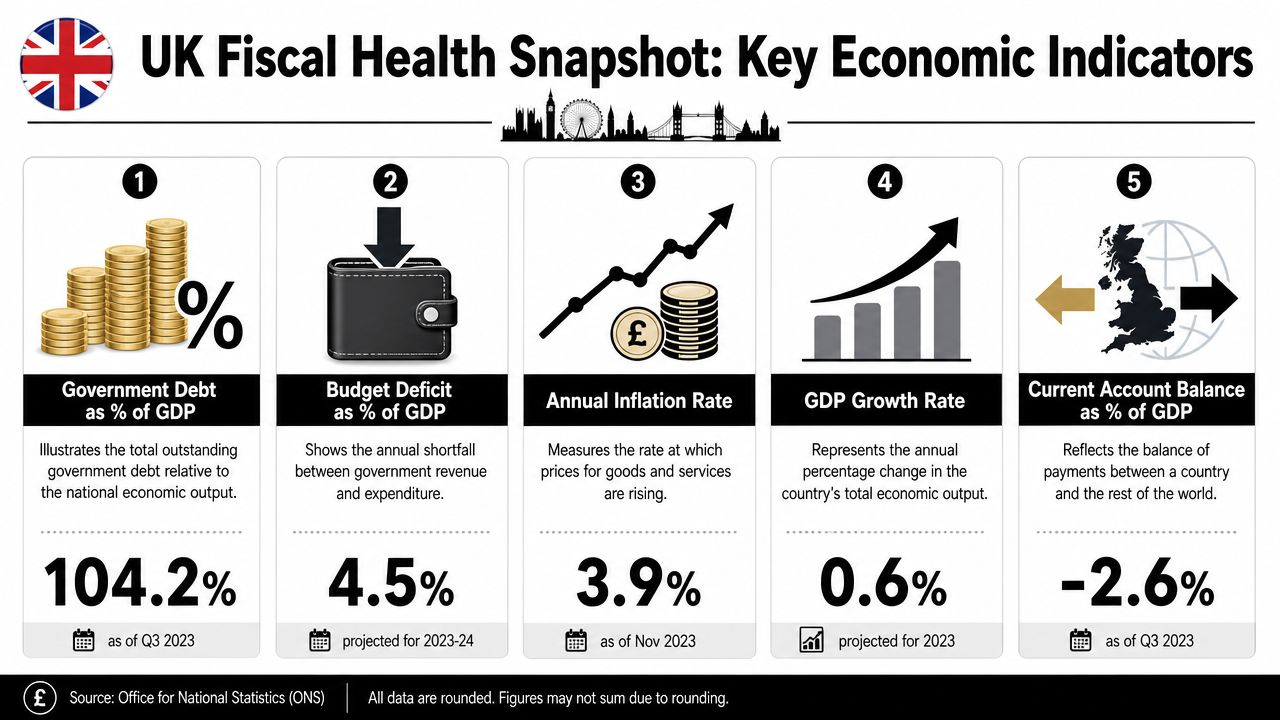

A useful starting point is the Office for National Statistics series on public sector net debt. The ONS reported that UK public sector net debt excluding public sector banks stood at £2,567.2 billion in June 2023, equivalent to 100.8% of GDP, the first time since 1961 that the ratio had exceeded 100% on that measure, according to the ONS public sector finances release. More recent cross-country monitoring from the IMF places UK general government gross debt near 100% of GDP and the fiscal deficit around 5% of GDP in 2024, as shown in the IMF Fiscal Monitor database.

What the debt numbers say

For ministers, the first implication is scale. Debt at around national income levels does not imply imminent default for a reserve-currency sovereign. It does mean that fiscal choices become more sensitive to interest rates, growth disappointments, and policy reversals. In a G7 context, that matters because the UK is large enough for fiscal stress to affect wider confidence, gilt market functioning, and the broader debate on stability in the financial system.

The second implication is persistence. A debt ratio above 100% of GDP can be managed over time, but it leaves less room for shocks. Ageing costs, weaker trend growth, and a higher global rate environment all raise the threshold for restoring fiscal space. The issue is no longer the stock of debt in isolation. It is the interaction between the stock, the cost of servicing it, and the volume that must be refinanced each year.

Why debt service matters more than rhetoric

The UK's exposure is clearest in debt interest. The Office for Budget Responsibility shows that debt interest spending has become far more volatile because a meaningful share of the gilt stock is index-linked and because refinancing now occurs at rates well above the levels that prevailed in the 2010s, as set out in the OBR fiscal risks and sustainability analysis. For policy, this is the operational constraint. Principal can be rolled over. Interest must be financed within each budget cycle.

That changes the nature of fiscal debate. A government with high debt and moderate borrowing costs retains room to absorb shocks. A government with high debt, large annual issuance needs, and increased servicing costs has less discretion even if market access remains intact. The UK is in the second category more often than many domestic debates acknowledge.

A short video overview can help place the current debate in wider context.

This pressure also reaches households through pensions, savings allocation, and the pricing of long-dated assets. Readers tracking that transmission into personal finance may find these pension insights for savers useful alongside the fiscal data.

- Debt stock: high enough to limit room for policy error.

- Deficit flow: persistent enough to keep annual borrowing needs high.

- Interest bill: large enough to absorb resources that could otherwise support public investment or shock response.

- Refinancing risk: manageable in normal conditions, but more sensitive to shifts in market confidence than the term “bankrupt” implies.

The central point is straightforward. Britain remains financeable, but its fiscal space has narrowed. For a G7 sovereign with a large financial sector and an outsized role in global capital markets, that is not only a domestic budgeting problem. It is a question of resilience, credibility, and policy capacity under stress.

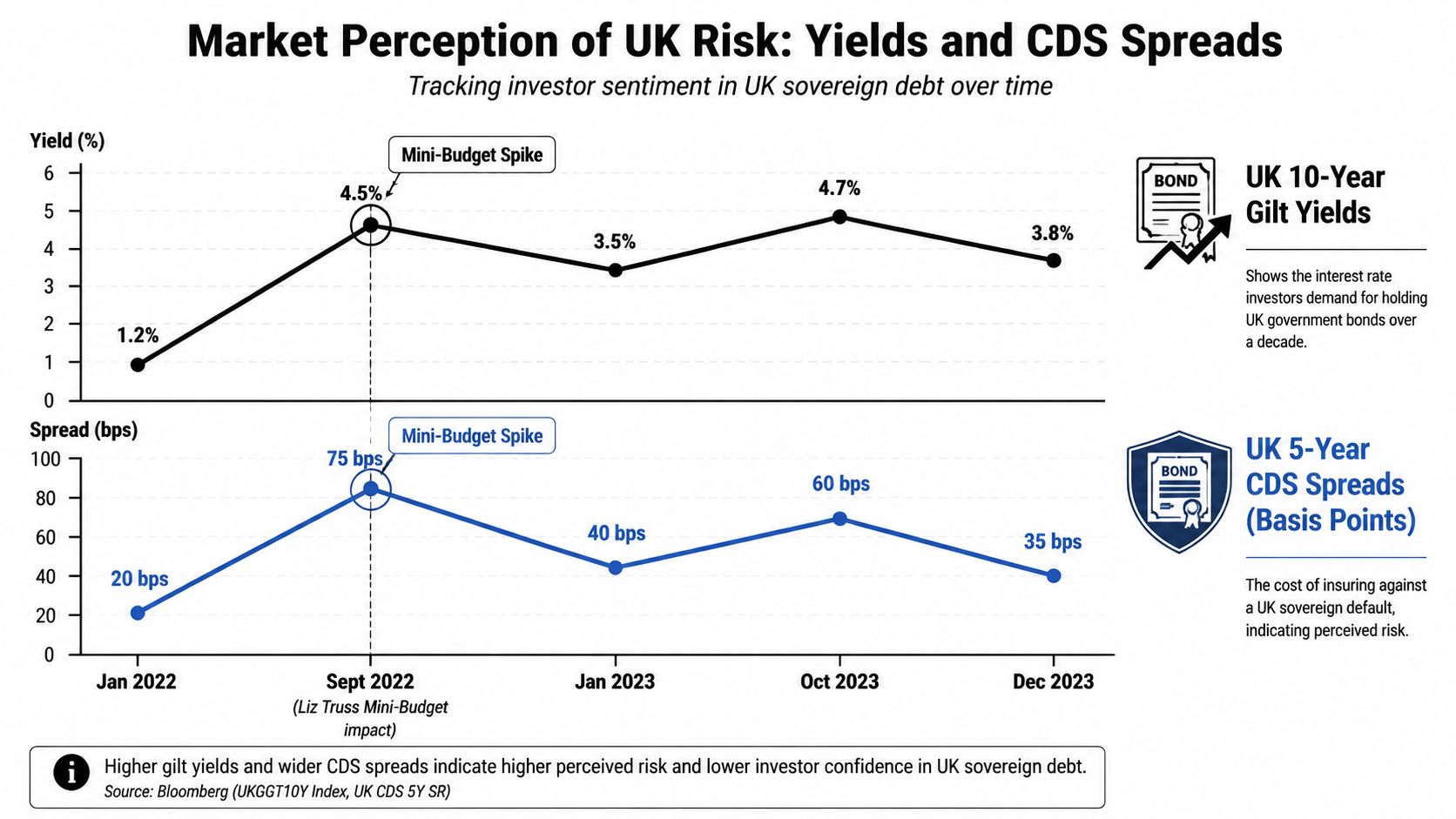

Reading the Market Signals on UK Risk

Fiscal numbers describe the stock and flow of public finances. Markets judge whether those numbers are credible, financeable and politically manageable. That judgement often turns before headline economic narratives catch up.

What markets punish first

Markets don't wait for legal default. They react to shifts in confidence, policy inconsistency and signs that the state may be relying on optimistic assumptions about growth or future consolidation. In the UK case, the key vulnerability isn't that investors think the state will suddenly cease to exist as a borrower. It's that they may demand a higher premium for holding its debt if policy choices look unstable.

The language of solvency and liquidity becomes relevant. UK-specific commentary has stressed that the sovereign cannot be forced into a classic foreign-currency default because it borrows in pounds, but that doesn't settle the more relevant issue. The more relevant issue is whether debt dynamics are becoming politically or macroeconomically unsustainable. That concern has been sharpened by warnings that UK public finances are in a “relatively vulnerable position”, as discussed in this analysis of the UK's fiscal risk debate.

If growth disappoints while refinancing costs stay high, investors don't need to believe in literal bankruptcy to change pricing. They only need to conclude that future budgets will be harder to stabilise.

Risk pricing is a policy signal

For ministers, the market signal should be read as a discipline mechanism, not as a referendum on national viability. The UK still benefits from deep institutions, a domestic investor base and monetary sovereignty. But those strengths don't grant immunity from repricing.

Three signals deserve attention.

- Consistency of fiscal plans. Markets are more tolerant of high debt than of erratic policy.

- Composition of borrowing. Greater reliance on short-term funding increases sensitivity to rate conditions.

- Credibility of medium-term growth. Without a believable growth path, consolidation becomes politically harsher and financially less convincing.

Readers following downside scenarios may want to compare this debate with a broader 2026 UK recession forecast, particularly for its discussion of how weak activity can reinforce fiscal pressure. For a wider institutional lens on contagion and confidence channels, this article on stability in the financial system is also relevant.

Markets rarely ask whether a G7 sovereign is “bankrupt”. They ask whether policy remains coherent enough to keep refinancing risk contained.

That's a stricter and more useful test.

Historical Parallels Crises and Recoveries

British fiscal history is less a sequence of bankruptcies than a record of recurring constraint. The pattern is consistent. Pressure builds when markets begin to doubt whether the policy mix can reconcile growth, inflation control, and debt financing at the same time.

The 1976 IMF episode remains the clearest case of external discipline overriding domestic discretion. Sterling weakness, high inflation, and doubts about fiscal management combined to limit the government's room for manoeuvre. The point for today is not that the UK faced insolvency in a corporate sense. It is that policy autonomy can shrink quickly when credibility erodes.

The ERM crisis of 1992 was a different type of failure, but it belongs in the same analytical frame. Britain was not overwhelmed by public debt dynamics. It was trapped in a policy commitment that markets judged unsustainable. Once that judgment hardened, official resolve was expensive to defend and ultimately ineffective. The lesson is broader than exchange-rate management. Governments lose room to act when policy frameworks ask markets to believe two incompatible things at once.

The 2008 financial crisis showed the opposite side of sovereign power. The British state could mobilise its balance sheet to stabilise banks and support the wider economy. That capacity mattered, and it helped prevent a much deeper collapse. But it also left a more difficult inheritance. Crisis intervention protected the system in the short run while reducing fiscal space for later shocks, a trade-off that matters for any G7 economy operating in an era of repeated disruptions.

That is why the 2022 mini-budget turmoil deserves attention as more than a domestic political error. The UK retained monetary sovereignty, deep capital markets, and a long institutional record. Even so, a sharp loss of confidence produced an abrupt repricing in government debt and exposed vulnerabilities in liability-driven investment strategies. For G7 and G20 policymakers, the episode was a reminder that credibility shocks can spill through pension funds, gilt markets, and currency channels with speed. The wider context is a world of financial risks shaped by geopolitical uncertainty, where advanced economies are no longer insulated by reputation alone.

History also argues against simple threshold thinking. Britain has carried very high public debt in earlier eras and avoided default. What mattered was not a single debt ratio. What mattered was the interaction between interest costs, nominal growth, institutional credibility, and the state's ability to sustain political consent for adjustment.

Two conclusions follow.

- The UK has repeatedly retained market access under stress. That reflects institutional depth, central bank credibility, and a large domestic investor base.

- Recovery has usually required policy correction and clearer fiscal anchors. Confidence returned when governments aligned commitments with economic reality, not when they tried to outtalk the market.

The useful historical parallel is therefore not a replay of 1976, 1992, 2008, or 2022. It is the recurring British pattern in which formal default remains unlikely, but fiscal space can erode far enough to constrain national choices and, by extension, complicate stability across the wider advanced-economy system.

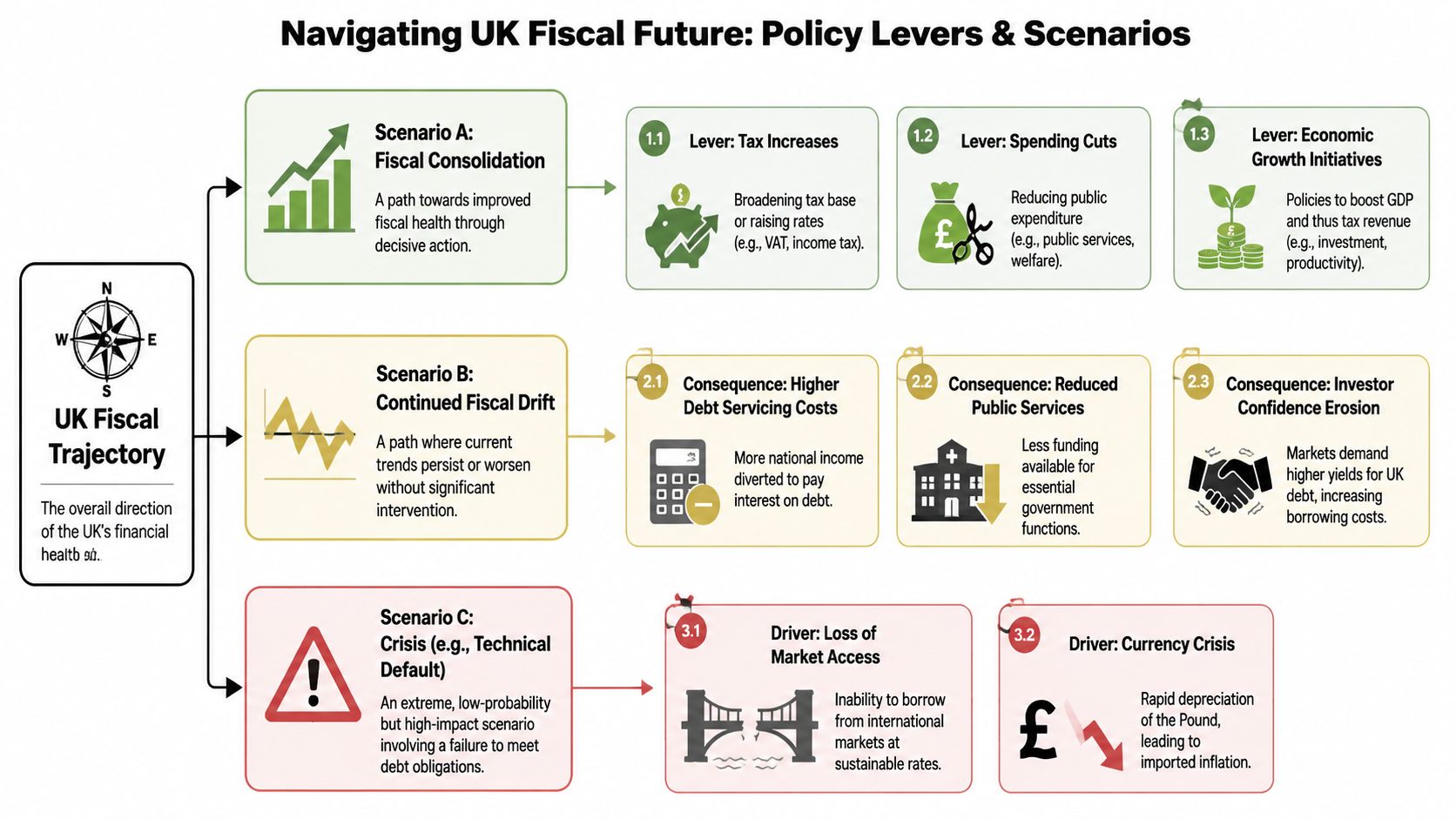

Future Scenarios and Difficult Policy Levers

The UK's policy problem can be summarised as a trilemma. Ministers want stronger growth, stable public services and credible debt reduction. In a constrained fiscal environment, they won't fully achieve all three at once.

The trilemma in plain terms

One path is fiscal consolidation. That can improve confidence if it is credible and sustained. But if it leans too heavily on cuts or poorly designed tax rises, it can also weaken growth and provoke resistance from households already under pressure.

A second path is fiscal drift. Government avoids the hardest choices, rolls debt forward and hopes growth or falling rates ease the burden. This path often looks politically convenient in the short run. It usually increases sensitivity to the next external shock.

A third path relies more heavily on monetary and financial conditions to absorb the strain. For a sovereign that borrows in its own currency, this can buy time. It can also create new tensions around inflation, market confidence and the distributional effects of higher borrowing costs.

None of these levers is clean. That is why the useful policy question isn't whether Britain is bankrupt. It's which combination of trade-offs ministers are willing to own, and whether they can do so before markets impose harsher ones.

For a broader view of how fiscal stress interacts with international fragmentation, energy shocks and strategic rivalry, this analysis of financial risks and geopolitical uncertainty provides a wider frame.

Why corporate distress matters for sovereign risk

A sovereign balance sheet doesn't deteriorate in isolation. It deteriorates through transmission channels in the wider economy. One such channel is company failure. Trading Economics reports UK corporate bankruptcies at 2,085 companies in April 2026, up from 2,037 in March 2026, in this UK bankruptcies series. As a forward-dated indicator cited by that source, it should be read as a stress signal in the corporate sector, not as proof of sovereign insolvency.

The policy relevance is straightforward.

- Higher borrowing costs hit firms first: debt-heavy businesses lose margin and investment capacity.

- Corporate distress feeds the budget: weaker profits and payrolls can soften tax receipts while raising pressure on welfare spending.

- The state then inherits fragility indirectly: public finances worsen not through one dramatic event, but through repeated losses in the tax base.

If ministers focus only on the sovereign balance sheet, they can miss the real-economy deterioration that later returns as fiscal stress.

That is the hidden weakness in much of the public debate. Sovereign risk in an advanced economy often arrives through affordability, growth disappointment and institutional fatigue, not through a single failed debt payment.

Conclusion Britains Constrained Role on the World Stage

Britain is not technically bankrupt. That conclusion follows from the nature of sovereign finance, the UK's ability to borrow in its own currency and the absence of anything like a standard national bankruptcy process. But that shouldn't be mistaken for comfort.

The sharper conclusion is that the UK's room for action is narrower than many domestic debates admit. Debt around the scale of annual output, a persistent deficit and interest costs that absorb a meaningful share of national income leave less fiscal space for defence, industrial strategy, climate investment, development finance and emergency response. For a G7 country, that matters well beyond Westminster.

A constrained UK is still a major actor. It is a less agile one. It has fewer options when geopolitical shocks arrive, less capacity to fund long-horizon priorities, and less tolerance for policy mistakes that unsettle markets. That makes Britain's fiscal trajectory a multilateral issue as much as a national one.

The right response isn't alarmist language. It is institutional seriousness. Ministers need a credible path that improves growth, protects confidence and contains debt-service pressure over time. Without that, the question “Is Britain bankrupt?” will keep returning, not because it is technically accurate, but because it captures a public intuition that the state's freedom to act is being steadily reduced.

For more policy analysis on fiscal resilience, sovereign risk and the choices facing G7 and G20 governments, visit Global Governance Media and follow its coverage of the world economy, summit agendas and long-term pathways for sustainable growth.