By Dr Eleanor Whitfield, Senior Policy Analyst

NHS England recorded 267 medicine shortages in 2023, a fact that should change how ministers think about American pharma companies in allied markets, because it shifts the conversation from abstract pricing disputes to a harder question of national health security and supply resilience. The dominant US firms are not merely exporters selling into foreign health systems. They sit inside research networks, manufacturing footprints, reimbursement negotiations and access debates that now shape how quickly patients in countries such as the UK receive medicines, how reliably hospitals can source them, and how much power governments retain in moments of scarcity.

That makes American pharma companies a G7 and G20 issue, not just a domestic US industry story. Their influence reaches from profit allocation and launch sequencing to procurement strategy, industrial policy and the politics of global health equity. For ministers preparing for the next cycle of health and finance negotiations, the central challenge isn't whether these firms matter. It's how to govern their power without weakening innovation, supply continuity or cross-border research capacity.

Table of Contents

- The Unignorable Influence of American Pharmaceuticals

- Mapping the Titans of the US Pharmaceutical Sector

- The Engine Room of Innovation and Profit

- Shaping Global Health Agendas from Washington to Geneva

- Navigating IP, Pricing and Global Supply Chains

- Public-Private Partnerships and the Access Gap

- Policy Pathways for a Resilient and Equitable Future

The Unignorable Influence of American Pharmaceuticals

The United States remains the pharmaceutical sector's largest profit pool, and that financial depth gives American drugmakers an outsized ability to shape which medicines are launched, where supply is prioritised, and how aggressively firms bargain with public payers abroad. For ministers in the G7 and G20, the core issue is not only corporate scale. It is the conversion of domestic market power into cross-border influence over availability, affordability and negotiating power.

This matters most where allied health systems are already under strain. A launch sequence set in New York or New Jersey can delay access in the UK if companies prioritise markets that protect higher margins or faster uptake. A production decision for a single biologic ingredient can tighten supply across several countries at once, because many procurement systems still depend on concentrated manufacturing networks and limited backup capacity. The policy risk is therefore wider than the standard US pricing debate. American pharma strategy can transmit shortages, fiscal pressure and access disparities into partner countries that did not shape those original incentives.

Ministers should assess these companies as system actors whose choices affect industrial resilience, health budgets and foreign policy relationships at the same time.

The distinction between large pharmaceutical groups and the broader biotech field also matters. Biotech firms often specialise in narrower platforms or therapeutic modalities, while large pharma companies combine research, regulatory expertise, manufacturing scale and market access operations in ways that give them far greater influence over international diffusion. Policymakers seeking a concise reference point on that wider ecosystem may find Woolf Software's guide to biotech useful.

The domestic context helps explain the international pattern. The wider pressures described in the crises in US health care have reinforced a business model built around high returns in the US market. Those returns do more than reward shareholders. They help finance global portfolios, sustain long negotiation cycles abroad, and support a level of policy engagement that few foreign suppliers can match. For the UK and other allies, that creates a practical dilemma. They rely on American innovation, yet remain exposed when US-driven commercial incentives conflict with supply security or equitable access.

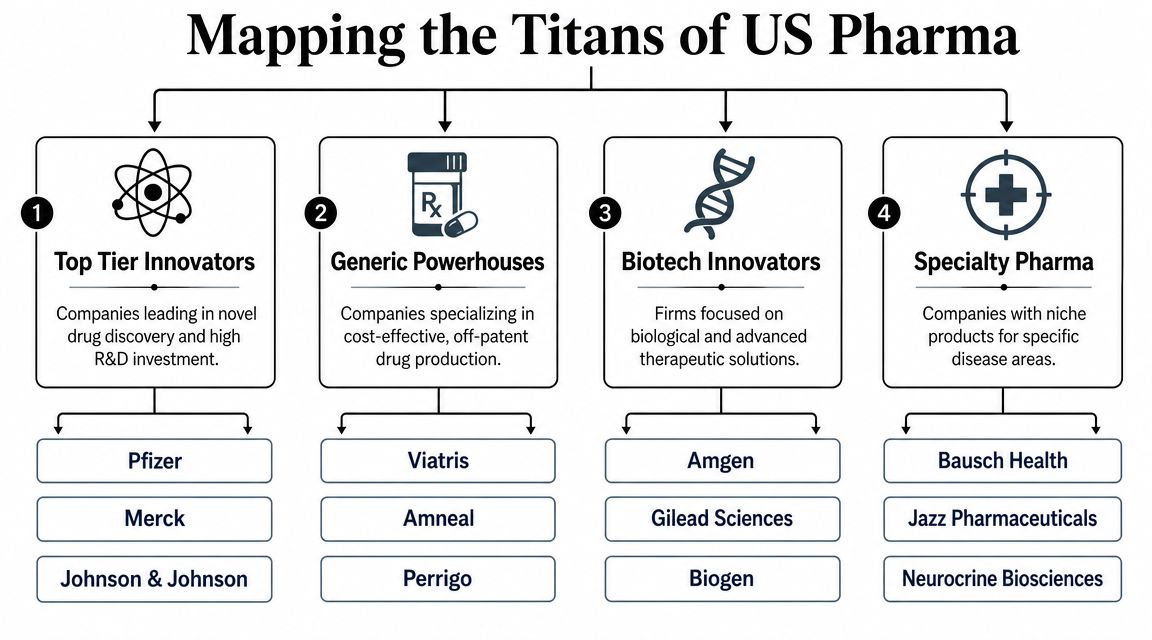

Mapping the Titans of the US Pharmaceutical Sector

For ministers, a list of company names isn't enough. The more useful approach is to group American pharma companies by strategic function, because different business models create different policy risks and opportunities in pricing, procurement and innovation diplomacy.

Four strategic archetypes matter most

Some firms operate as top-tier innovators. They build broad portfolios, maintain major discovery operations and tend to anchor international policy debates because governments depend on them for high-profile launches and ongoing pipeline credibility. Pfizer, Merck and Johnson & Johnson are the clearest examples of this group in public debate.

A second group consists of biotech-led innovators with strong positions in biological medicines and advanced therapeutic approaches. Their policy profile often differs from larger diversified companies because manufacturing complexity, evidence requirements and smaller initial patient populations can create sharper market access disputes. Biologics also tend to push regulators and payers into more specialised forms of assessment.

Then there are specialty pharma companies, which focus on narrower disease areas or specific treatment modalities. Their portfolios may be less diversified, but their advantage can still be substantial when they hold a leading product in an area with limited alternatives. In negotiations, these firms often behave differently from diversified giants because one or two assets can carry an outsized share of commercial value.

Finally, generic and off-patent producers matter for affordability and continuity. They usually receive less ministerial attention than brand-name innovators, yet the resilience of any health system depends on them. When shortages emerge, the failure point is often not the most visible blockbuster medicine but the less glamorous product category where margins are thinner and manufacturing concentration is harder to see.

Why the taxonomy matters for ministers

This categorisation isn't academic. It changes what policymakers should ask.

| Strategic group | Primary policy concern | Typical negotiating issue |

|---|---|---|

| Top-tier innovators | Market power across multiple products | Launch timing and pricing leverage |

| Biotech-led innovators | Complex production and evidence demands | Access conditions and regulatory readiness |

| Specialty pharma | Dependence on limited products | Single-product bargaining asymmetry |

| Generic producers | Fragile economics and supply concentration | Continuity of supply and shortage prevention |

A health ministry negotiating with a diversified innovator needs a different toolkit from one managing dependence on a specialist manufacturer. The same applies at multilateral level. If ministers want more resilient supply, they need to know whether they are confronting patent-driven exclusivity, biological production bottlenecks, or economically fragile generic markets.

The important distinction isn't simply who is largest. It's who controls the bottleneck that the health system can't easily replace.

That is why the term American pharma companies should never be used as though the sector were strategically uniform. Policy works better when governments identify which type of firm they are dealing with, what that firm values most, and where public influence is strongest.

The Engine Room of Innovation and Profit

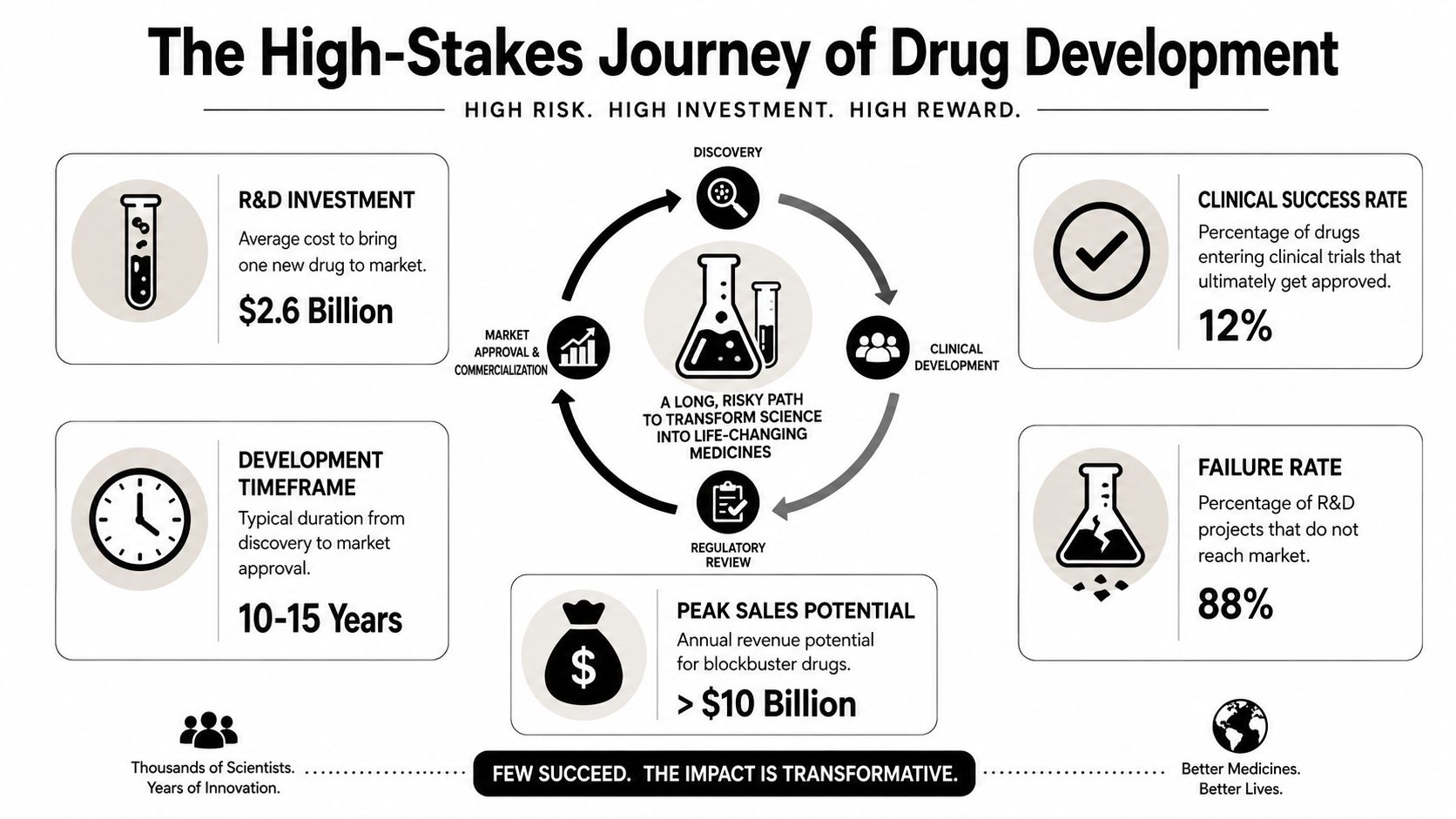

A small set of blockbuster products often determines whether a large pharmaceutical company outperforms or falls short in a given year. That concentration of returns helps explain why American pharma companies behave less like broad-based manufacturers and more like portfolio managers of high-value intellectual property.

Profit concentration shapes strategic behaviour

As noted earlier, profit levels at the top of the sector are unusually high by the standards of most manufacturing industries. The policy significance is not the headline number alone. It is the way those profits are concentrated in a limited number of products, therapeutic areas and launch markets, with the US market still carrying much of the commercial weight.

That structure produces predictable strategic choices. Firms protect patent life aggressively because a short extension on a major product can matter more than incremental gains across a wide portfolio. They sequence launches by expected net price and reimbursement certainty, not solely by clinical need. They also allocate management attention toward assets with the highest probability of sustaining margins over time.

For ministers outside the United States, including in the UK, this has practical consequences. A company may describe a medicine as globally important while still delaying launch in markets that offer lower prices, tighter health technology assessment, or less favourable commercial terms. The result is a health equity problem that is often misread as a purely national pricing dispute. In reality, it reflects a corporate model in which access decisions are filtered through portfolio economics set elsewhere.

Three implications follow.

- US earnings shape global risk tolerance: Strong returns in the domestic market let companies absorb slower uptake in allied countries while preserving research programmes and shareholder distributions.

- Launch decisions can widen access gaps among allies: Countries with disciplined reimbursement systems may wait longer for supply, even when they contributed to the science base, trial infrastructure or public purchasing commitments.

- Supply resilience can become secondary to asset optimisation: Management teams focused on protecting high-margin franchises have weaker incentives to maintain redundant manufacturing capacity for lower-return products.

This last point deserves more attention in G7 discussions. The same firm that invests heavily in a frontier therapy may still rely on concentrated production networks, single-source inputs, or tightly managed inventory systems that leave partner countries exposed during disruptions. For the UK and other allied health systems, the issue is not only what a medicine costs. It is whether commercial incentives support dependable supply once a product becomes clinically indispensable.

Why public research still matters

Private returns rest on a larger public foundation. Universities, publicly funded laboratories and government-backed research agencies absorb a meaningful share of early scientific risk, long before a product reaches the stage where commercial exclusivity becomes valuable. Debates over funding for the NIH therefore matter well beyond the United States. They affect the upstream discovery pipeline that many multinational pharmaceutical strategies depend on.

That creates a clearer policy test for ministers. If public institutions finance a significant share of early uncertainty, governments have grounds to ask for more than eventual product availability. They can ask for evidence standards that reflect real-world use, supply commitments that reduce shortage risk, and access terms that recognise public contribution to invention.

Profitability does not undermine the case for innovation. It does, however, strengthen the case for reciprocal obligations, especially where allied countries help fund science, host trials, provide skilled manufacturing capacity and still face delayed access or fragile supply.

Shaping Global Health Agendas from Washington to Geneva

American pharma companies influence global health agendas because governments need them, often urgently, while also trying to constrain their influence. That dual role makes them indispensable partners and persistent political challengers at the same time.

The UK as a policy lever not just a market

The UK illustrates this clearly. According to the Association of the British Pharmaceutical Industry's industry data, the UK biopharmaceutical sector includes around 73,000 employees in pharmaceutical manufacturing and the industry invested £9.6 billion in research and development in 2023. For American firms, that means the UK isn't a peripheral export destination. It's a strategically valuable base for research, trials, manufacturing and European policy positioning.

That location within a high-value ecosystem gives companies influence that extends beyond direct sales. A firm with research partnerships, production assets and clinical presence in the UK speaks to government not merely as a vendor but as an investor, employer and participant in national innovation strategy. Ministers know this. Companies know that ministers know it.

Governments rarely negotiate with pharmaceutical multinationals on price alone. They negotiate across investment, jobs, research credibility and the optics of patient access.

Corporate strategy becomes governance strategy

Corporate decisions spill into international governance. A company deciding where to place trials, where to manufacture, or which market to launch into first is also shaping the priorities of regulators, treasury officials and multilateral institutions. In forums such as the G7 and G20, that influence appears indirectly. It surfaces in discussions about pandemic preparedness, antimicrobial resistance, industrial resilience, life-sciences competitiveness and the rules attached to public-private collaboration.

Three policy effects deserve close attention:

Agenda setting through indispensability

When governments depend on a small set of firms for critical products and future pipelines, those firms gain a voice in defining what “realistic” policy looks like.Norm shaping through technical expertise

Regulators and ministries often need company data, manufacturing insight and trial evidence. Technical dependence can become normative influence.Cross-border bargaining power

A firm with a strong presence in the UK and the US can translate national negotiations into broader regional and multilateral influence.

This isn't an argument for hostility. It is an argument for realism. Ministers should assume that large American pharmaceutical groups are active participants in governance outcomes, even when they aren't formally seated at the negotiating table.

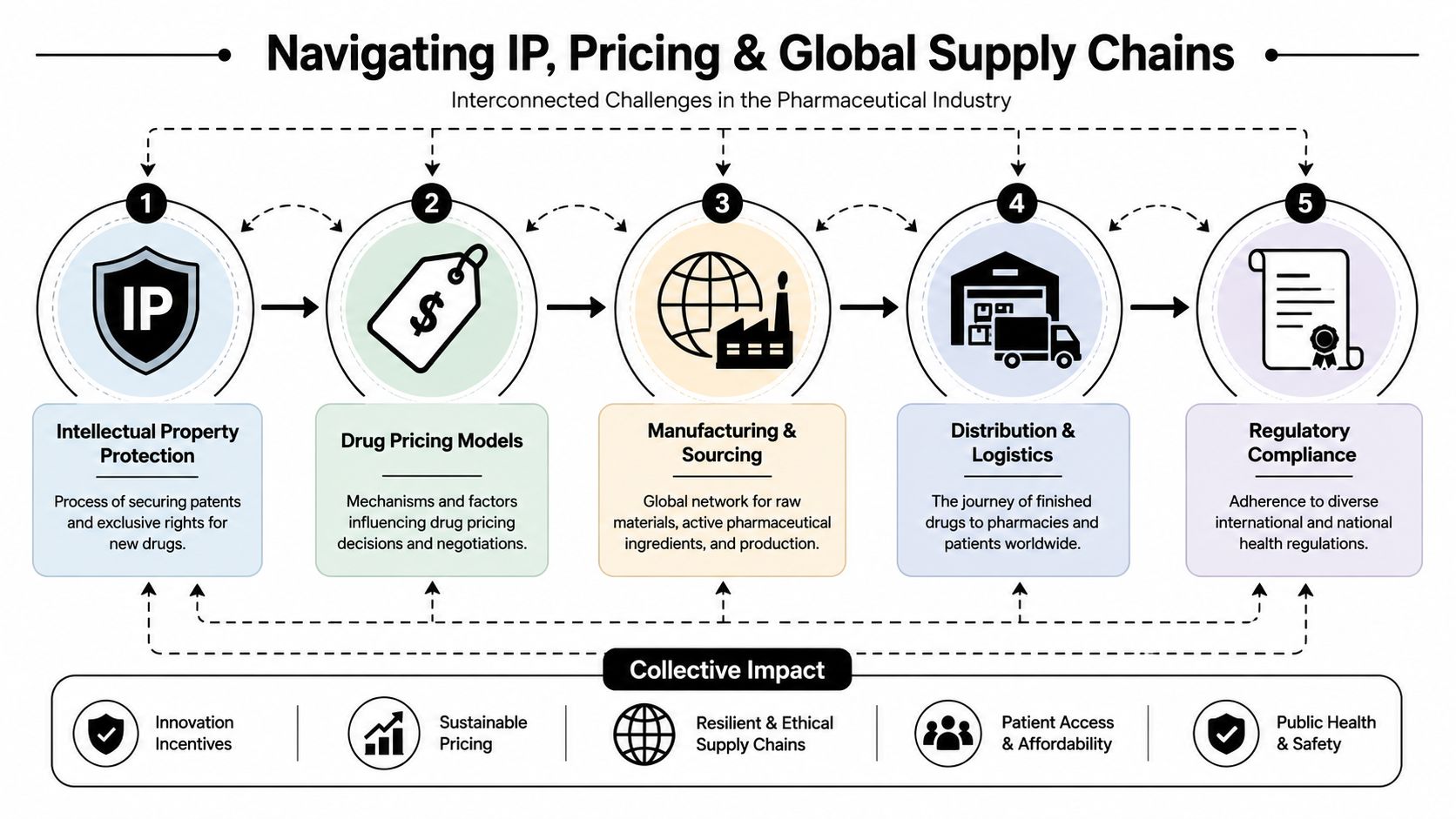

Navigating IP, Pricing and Global Supply Chains

The standard argument says strong intellectual property drives innovation, and lower prices improve access. That framing is too narrow for current conditions. It misses the operational middle where real-world supply can fail even when products are approved, clinically valuable and formally available on paper.

Shortages expose the limits of the pricing debate

In the UK, this tension is visible in hard system stress. The Access to Medicine Foundation material notes that NHS England recorded 267 medicine shortages in 2023, making the supply behaviour of large US-headquartered firms a live policy issue in a market already adjusting branded medicine spending rules, as referenced in the Access to Medicine Foundation discussion of shortages and access pressures.

That fact changes the policy emphasis. A medicine can be reimbursed in principle and still be difficult to access in practice if production is concentrated, release processes are delayed, packaging is market-specific, or firms direct inventory toward more commercially attractive settings. Anyone looking for a concise patient-facing explanation of the wider causes of medication supply issues will recognise that shortages rarely come from one cause alone. They emerge from cumulative weak points across manufacturing, logistics and incentives.

The operational consequences are easier to grasp when seen as a chain:

- IP determines who can legally produce

- Pricing shapes whether firms want to supply

- Manufacturing concentration determines how fragile output becomes

- Distribution and market-specific compliance determine whether stock reaches patients on time

To illustrate the wider system challenge, this briefing is also worth viewing:

What ministers should scrutinise in supply decisions

The policy mistake is to focus only on the final negotiated price. Governments also need visibility into how firms organise release hubs, secondary packaging, stock buffers and market sequencing. The logic for that scrutiny is reinforced by analysis in a Global Governance Media essay on licensing for equity and access to medicines, which highlights why legal access frameworks and practical supply arrangements must be considered together.

If a country can only secure access after a long reimbursement process, and the same product is more profitable elsewhere, supply vulnerability stops being a technical problem. It becomes a governance problem.

Allied markets have more common cause than they often admit. The UK case shows that even advanced health systems can face exposure when global production is concentrated and launch economics are uneven. G7 coordination on supply resilience shouldn't be framed only around emergency stockpiles. It should include aligned expectations on transparency, continuity planning and market service obligations for critical medicines.

Public-Private Partnerships and the Access Gap

Public-private partnerships remain one of the most durable tools in global health. They can mobilise technical expertise quickly, share risk across institutions and create delivery channels that states alone might struggle to assemble. For ministers, the key question isn't whether partnerships have value. It's when they produce public value that can be measured independently.

Where partnerships work

At their best, partnerships align complementary strengths. Governments and multilaterals can provide legitimacy, pooled financing and convening power. Companies contribute development capacity, manufacturing know-how and regulatory experience. In crisis settings or neglected disease areas, that combination can move faster than either side acting alone.

A useful way to judge partnership quality is to ask whether each party is doing something it couldn't do as effectively on its own. If the answer is yes, the model has merit. If the arrangement mainly repackages company commitments that would likely have happened anyway, the public case is weaker.

Where access claims need harder testing

The harder issue is what happens after announcements. The Access to Medicine Foundation findings discussed in November 2024 show that while pharma companies are expanding access commitments, many populations in low-income countries remain largely overlooked. The same analysis cautions that company-reported reach can be difficult to interpret because access metrics may combine product delivery with non-product initiatives.

That matters for a G7 and G20 audience because corporate rhetoric often travels faster than comparable outcome data. A pledge can be global in tone while remaining narrow in operational reach. A programme can look impressive in communications but still leave major patient groups outside effective coverage.

A more disciplined evaluation framework would compare partnerships across three questions:

| Test | What ministers should ask |

|---|---|

| Patient reach | Who actually received the medicine or service? |

| Market coverage | Which countries and populations were excluded? |

| Verifiability | Can outcomes be checked independently? |

Partnership design should start from accountability, not gratitude. Public institutions are entitled to ask what was delivered, where it was delivered, and who was left out.

This isn't a critique of collaboration as such. It is a reminder that access claims need clearer baselines, cleaner definitions and stronger external verification. Without that, public-private partnerships can become vehicles for reputational gain more readily than instruments of equitable health delivery.

Policy Pathways for a Resilient and Equitable Future

The most effective policy response isn't to weaken American pharma companies indiscriminately or to defer to them out of fear of losing innovation. It is to employ public influence more intelligently, especially in allied markets where regulators, payers and industrial policymakers already shape the conditions of market entry.

A practical agenda for G7 and G20 health ministers

The UK offers a useful negotiating template. Analysis published in the study on pharmaceutical market access and UK regulatory constraints shows that the UK's value-based reimbursement environment, governed by NICE and the MHRA, creates distinct commercial constraints for American firms, requiring careful alignment of evidence packages and supply chains. That means policymakers already possess more influence than conventional industry narratives suggest.

Ministers should use that power in four ways.

- Tie access to supply reliability: Reimbursement and procurement discussions should include explicit expectations on continuity planning, release readiness and market servicing for critical products.

- Demand clearer evidence packages: If firms want rapid uptake, they should present data in formats that fit local health technology assessment requirements rather than relying on pressure for exceptional treatment.

- Coordinate among allied markets: G7 members should compare launch sequencing, shortage patterns and supply dependencies more systematically so companies can't exploit fragmented negotiations.

- Raise the bar for partnership accountability: Public support, concessional finance and political endorsement should come with clearer disclosure of who benefits and who doesn't.

The deeper lesson is that resilience and equity aren't separate agendas. They intersect in the same set of decisions about where medicines are launched, how they are priced, where they are produced and which patients are ultimately prioritised. American pharma companies will remain central to solving major health challenges. But governments don't have to choose between dependence and confrontation. They can choose structured reciprocity.

That should be the operating principle for the next round of G7 and G20 health diplomacy: if public systems sustain the conditions for innovation, then private actors must accept stronger obligations on access, transparency and supply security.

Global Governance Media convenes the policymakers, analysts and sector leaders shaping these debates across the G7 and G20. For more evidence-based briefings on global health, industrial policy and multilateral governance, visit Global Governance Media.