By Daniel Mercer

In 2025, solar accounted for 54% of all new electricity-generating capacity added to the US grid, according to the SEIA Solar Market Insight 2025 Year in Review. That single figure changes how policymakers should read the Solar Energy Industries Association. SEIA is more than a sector lobby. It speaks for an industry that now sits near the centre of American power-sector expansion, capital formation, grid planning, and industrial policy.

For a G20 audience, that matters beyond Washington. When an association represents a market of that scale, its technical preferences, trade positions, and regulatory priorities can shape supply chains, investment signals, and policy language well outside the United States. SEIA's relevance therefore lies not only in what it wants from US lawmakers, but in how those demands ripple into standards, procurement choices, and diplomatic narratives across advanced and emerging economies.

A useful way to think about SEIA is as a strategic intermediary. It translates firm-level commercial interests into policy asks, then translates policy outcomes into industry-wide operating conditions. That role affects domestic deployment, but it also influences how governments elsewhere interpret the political economy of rapid solar scale-up. For officials assessing energy security, competitiveness, and climate implementation, SEIA is a case study in how trade associations become consequential actors in the energy transition.

For readers looking at the wider politics of decarbonisation, this analysis of solar's role in the path to net zero offers useful complementary context.

Table of Contents

- An Introduction to SEIA and Its Strategic Importance

- The Architecture of Influence History Structure and Funding

- SEIAs Core Policy Positions and Advocacy Priorities

- Quantifying the Impact SEIA and Solar Industry Growth

- SEIAs Influence on Global Energy and Climate Policy

- Navigating Tensions Criticisms and Future Challenges

- Policy Takeaways and Recommended Actions

An Introduction to SEIA and Its Strategic Importance

In the United States, solar has moved from a peripheral technology to a central component of new power investment. That shift helps explain why the Solar Energy Industries Association, or SEIA, now matters beyond Washington. It is the principal US trade body for solar and solar-plus-storage, and its interventions increasingly affect questions that extend well past domestic deployment, including product standards, supply-chain governance, trade compliance, and the policy vocabulary used in G7 and G20 energy discussions.

SEIA's strategic relevance lies in the market it helps organise and the policy channels it can access. In large power transitions, governments do not engage only with utilities and regulators. They also rely on industry associations that can consolidate commercial positions, identify implementation barriers, and translate technical concerns into legislative and administrative proposals. In the US case, that gives SEIA a role in debates over tax credits, permitting, interconnection, domestic manufacturing rules, and the treatment of storage within electricity market design.

For non-US policymakers, the wider significance is practical. Decisions shaped in the US solar sector often influence procurement norms, due-diligence expectations, and compliance frameworks elsewhere, especially where global manufacturers, project financiers, and equipment suppliers operate across multiple jurisdictions. A US trade association with sustained access to federal agencies, Congress, and standards-setting conversations can therefore affect the terms on which international firms compete. It can also shape which policy models are seen as credible in wider climate diplomacy.

Solar policy is no longer only an environmental file. It now sits at the intersection of industrial strategy, grid reform, resilience planning, and trade policy. The strategic case for solar in decarbonisation is already well established in wider policy debate, including in analyses of the role of solar power in getting closer to net zero. What deserves closer attention is the institutional layer beneath that transition. Trade bodies such as SEIA help determine how fast projects move, which standards gain acceptance, and how governments balance cost reduction against domestic production and supply-chain security.

A comparative lens is useful here. Mature energy sectors rarely scale through technology economics alone. They scale when industry representation becomes organised enough to reduce policy uncertainty and present officials with implementable options. SEIA should therefore be read not merely as a lobby group, but as a coordinating institution within the US clean energy economy, one whose domestic advocacy can carry international effects through standards, investment expectations, and cross-border supply chains.

For G20 delegations, the policy lesson is specific. SEIA does not represent the public interest as such, and its positions should be assessed accordingly. Yet any government seeking to understand how the US solar market may shape broader energy governance should treat SEIA as a relevant institutional actor, particularly where American policy choices influence global capital flows, manufacturing location decisions, and the practical terms of climate implementation.

The Architecture of Influence History Structure and Funding

In large power markets, industry associations often shape implementation as much as legislation. Their importance rises once a technology moves from niche deployment to system relevance, because governments then need organised interlocutors on tariffs, interconnection, standards, workforce capacity, and finance. SEIA fits that pattern. Its significance lies in how it converts a fragmented commercial sector into a repeat participant in US rulemaking, with effects that can extend beyond the domestic market through procurement norms, trade debates, and manufacturing signals watched closely by G7 and G20 governments.

Why trade associations matter in power transitions

SEIA's development reflects a broader institutional sequence seen in renewable-energy markets. An industry body usually begins as a technical or representative forum for an emerging sector. As deployment expands, it becomes a coalition manager. Once the technology starts affecting grid planning, industrial policy, and trade exposure, the association becomes a system-level stakeholder that public authorities consult repeatedly.

| Stage | Character of the organisation | Strategic function |

|---|---|---|

| Early market phase | Specialist or technical advocate | Legitimises an emerging technology |

| Expansion phase | Broader industry coalition | Seeks market access and policy stability |

| Infrastructure phase | System-level stakeholder | Engages on grid, standards, finance, and integration |

This progression matters for non-US policymakers. When a US industry body reaches the infrastructure phase, its domestic positions can begin to influence international standard-setting discussions and supply-chain expectations, even without a formal global mandate.

Institutional continuity, structure and funding

The public record available here supports a cautious assessment rather than a detailed organisational map. What can be said with confidence is that SEIA's influence is likely rooted in features common to major trade associations. These include member coordination, formal governance, permanent policy staff, technical committees or working groups, and funding tied primarily to industry participation. That combination gives an association continuity across electoral cycles and regulatory shifts.

Continuity is the point.

A ministry can disregard a single campaign. It is harder to disregard an organisation that appears in successive consultations, submits technical comments, convenes firms across the value chain, and remains present when policy moves from headline law to administrative detail. In practice, much of the policy effect comes from repeated participation in tariff design, tax guidance, domestic-content rules, permitting debates, and standards development. For outside governments, this helps explain why a US trade body can matter in arenas that appear at first to be purely national.

Funding structure also shapes policy behaviour. Associations financed by member firms tend to prioritise bankability, regulatory clarity, and market access, because those are the issues around which a diverse membership can usually align. That incentive structure does not make their positions neutral, but it does make them legible. It also explains why questions such as solar energy tax credits for businesses become more than sectoral lobbying points. They become indicators of how the industry seeks to stabilise investment conditions, influence capital allocation, and frame clean-energy expansion as an industrial strategy rather than only an environmental one.

Associations such as SEIA lower transaction costs for policymakers by aggregating industry preferences into a form officials can engage with repeatedly.

For a G20 delegation, the strategic implication is straightforward. Engagement with SEIA should be treated as engagement with a structured commercial coalition whose domestic advocacy can affect international conversations on clean-energy trade, local content, and technology governance. Governments designing their own solar institutions should therefore pay close attention to governance, membership incentives, and funding sources, because those factors determine whether an industry body remains a narrow lobby or becomes a durable actor in energy and climate policy.

SEIAs Core Policy Positions and Advocacy Priorities

SEIA's policy agenda can be read as a response to three practical questions. How do solar projects become economically viable? How do supply chains remain workable under geopolitical pressure? How does a power system absorb more variable generation without slowing deployment? Those questions produce a recognisable advocacy pattern, even where this article avoids unsupported detail.

Tax policy as market design

The first pillar is fiscal certainty. Solar deployment depends heavily on whether investors can model expected returns over project lifetimes. Industry associations therefore tend to treat tax policy not as a side issue, but as part of market design itself. In the US context, that includes support for clean-energy tax incentives and clear implementation rules.

For officials comparing policy approaches, a practical reference on how these incentives are framed for commercial users is this guide to solar energy tax credits for businesses. It isn't a substitute for statute or regulation, but it helps illustrate why the tax treatment of projects often determines whether deployment happens at pace or stalls in development pipelines.

Stable incentive design doesn't simply lower cost. It tells lenders, developers, and manufacturers that government intends the market to persist.

Trade and grid policy as strategic bottlenecks

The second pillar is trade. Solar isn't deployed through domestic policy alone. Modules, components, equipment, and upstream materials move through global supply chains that are politically exposed. When SEIA weighs in on trade questions, it is often doing more than defending firm interests. It is shaping the balance between industrial policy, import dependence, resilience, and cost.

The third pillar is grid integration. Here the politics become less visible but more consequential. Once a solar market reaches scale, the main constraint often shifts away from public enthusiasm and towards planning, interconnection, storage, and system flexibility. That's why mature solar policy increasingly turns to the institutional plumbing of electricity systems.

A concise summary of SEIA's likely policy playbook looks like this:

| Policy Pillar | Objective | Example Initiative |

|---|---|---|

| Tax incentives | Preserve long-term project bankability | Advocacy for durable clean-energy tax treatment |

| Trade policy | Avoid supply disruptions while managing geopolitical risk | Engagement on import rules and supply-chain conditions |

| Grid modernisation | Enable faster connection of new projects | Support for interconnection and system-integration reform |

| Storage integration | Improve flexibility and dispatch value | Advocacy for policies that treat solar and storage as linked assets |

| Technical certainty | Reduce development and compliance friction | Promotion of standardised design and quality approaches |

SEIA holds particular relevance for non-US governments. Many countries focus on deployment targets while underestimating the policy detail required to turn those targets into connected assets. Industry associations often understand that detail before governments do, because their members encounter the frictions first.

Quantifying the Impact SEIA and Solar Industry Growth

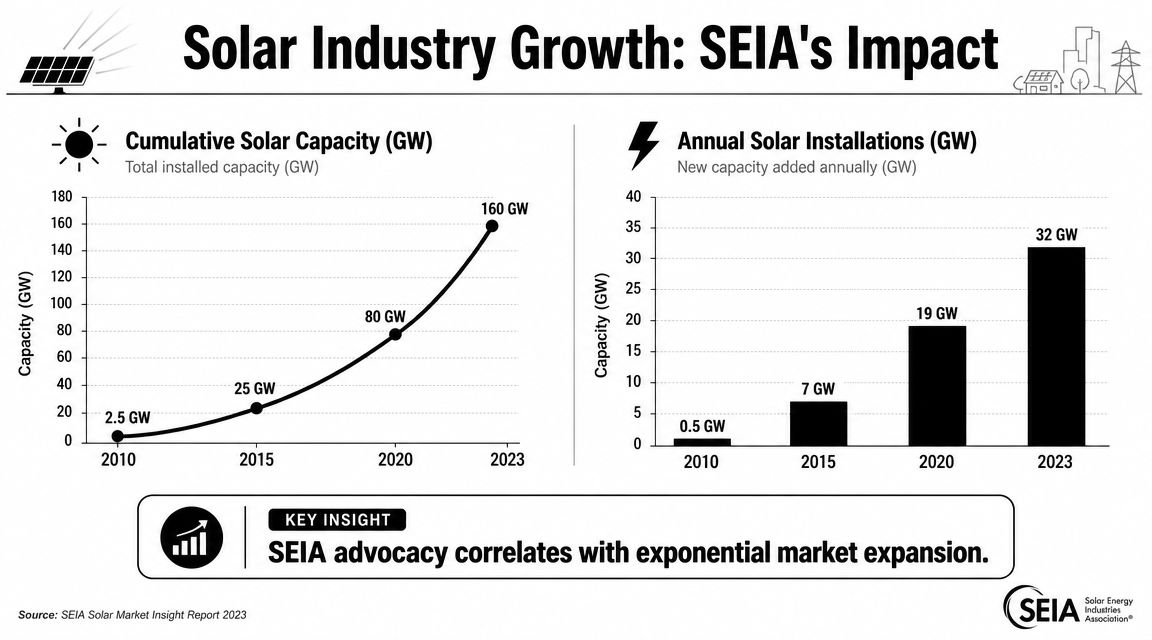

More than half of new US electricity-generating capacity added in 2025 came from solar. As noted earlier, annual installations fell from the previous year, yet solar still held the largest share of new capacity additions. For policymakers, that combination matters more than the year-on-year decline. It indicates that solar has moved from policy-supported growth into system-defining scale within the US power sector.

What the headline market data actually show

The strategic point is straightforward. Once a technology supplies the majority of new capacity in a major economy, trade, standards, grid access, and financing rules around that technology begin to shape wider market behaviour. In practice, SEIA's importance follows from representing an industry that is now large enough to affect utility planning, capital allocation, and industrial policy in one of the world's most consequential energy markets.

Classification also matters. The 221114 solar electric power generation framework is useful because industries gain political and financial visibility through the way governments, lenders, and analysts count them. That visibility affects tax treatment, procurement design, and the comparability of solar with other infrastructure classes.

The investment dimension deserves separate attention. Solar deployment at this scale depends not only on equipment costs but also on the ability of public and private institutions to fund pipelines of bankable projects. That is why the broader debate about growing the pipeline of energy transition investments has direct relevance to SEIA's policy role. Associations that reduce uncertainty for developers and financiers can influence build rates even without formal regulatory authority.

Why standards matter to finance and delivery

SEIA's effect is not captured by deployment totals alone. It also appears in technical standard-setting. Its standards programme includes a technical standard for 250 kW to 5 MW utility-interactive PV, storage, and PV-plus-storage systems on commercial and industrial properties, covering the PV array, balance of system, microgrids, contractor qualifications, quality control, and inspection processes, as set out in the SEIA 251 draft standard.

That project band has outsized policy relevance. Commercial and industrial installations sit between rooftop diffusion and utility-scale procurement. They often expose actual sources of delay in mature markets, especially permitting, inspection consistency, insurance requirements, and lender due diligence. A clearer technical baseline can reduce transaction costs across all four.

For G20 delegations, the broader implication is easy to overlook. US industry standards often travel indirectly through insurers, engineering firms, multinational buyers, and supply-chain contracts. A standard advanced by a US trade association can therefore influence expectations well beyond the United States, particularly in markets seeking to attract international capital while keeping project risk within acceptable limits.

Operational lesson: Technical standards affect the speed of approvals, the cost of capital, and the confidence of institutional investors. They are part of industrial policy, not just engineering guidance.

SEIAs Influence on Global Energy and Climate Policy

SEIA's global significance lies in spillover effects. A US industry association doesn't need a formal diplomatic mandate to influence international outcomes. If it affects domestic trade rules, technical expectations, and supply-chain positioning in one of the world's largest clean-energy markets, other governments will feel the consequences through prices, procurement choices, investment timing, and policy imitation.

From domestic advocacy to international signalling

Consider the strategic message sent by the scale of mature markets. In the UK, installed solar capacity has surpassed 15 GW, and generation reached record levels above 2 TWh in peak months, according to the Solar Market Insight Q2 2025 reference. That matters because the policy questions facing mature markets converge. Once deployment reaches infrastructure scale, debates shift from whether solar is viable to how it is integrated.

That is where SEIA's domestic agenda becomes internationally relevant. If the US policy debate, shaped in part by SEIA, emphasises supply-chain resilience, storage pairing, technical standardisation, and grid reform, those priorities can influence what becomes legible and legitimate in wider energy diplomacy. The result is indirect harmonisation. Not full alignment, but a narrowing of the policy menu that governments consider realistic.

A related diplomatic frame appears in broader discussions about strengthening solar and clean energy at the UN's COP29, where deployment, finance, and implementation increasingly sit in the same conversation.

Why non-US governments should pay attention

For non-US policymakers, SEIA matters for three reasons:

- Norm setting: US industry positions can shape expectations around what counts as responsible sourcing, investable project design, and credible market reform.

- Supply-chain signalling: Large-market advocacy influences commercial decisions by manufacturers, developers, and investors serving multiple jurisdictions.

- Negotiation framing: G7 and G20 debates on energy security often borrow language first tested in domestic industrial policy contests.

This doesn't mean governments should import US frameworks wholesale. In fact, they shouldn't. Institutional conditions differ. Grid structure differs. Housing stock differs. Capital costs differ. But ignoring US industry coalitions would also be a mistake, because they often prefigure the next set of political and operational issues that other markets will confront as they scale.

Navigating Tensions Criticisms and Future Challenges

Rapid growth doesn't settle the hardest policy questions. It often exposes them. The most important challenge facing SEIA and comparable industry bodies is that more solar doesn't automatically produce more equitable outcomes. A key criticism of rapid solar expansion is that benefits may not reliably reach low-income households, and the policy challenge is structuring incentives so communities with limited financial resources and inefficient housing can participate, as discussed in the US Department of Energy primer on equity-focused energy finance.

Growth and equity are not the same policy outcome

This is a serious issue for G20 policymakers because it affects political durability. If solar policy is perceived to favour asset owners, creditworthy households, or large project developers while excluding renters, low-income households, and communities in inefficient housing, public support can weaken even when deployment succeeds.

The core tension is straightforward. Industry associations are designed to support market expansion. Equity policy requires asking who can access that market, on what terms, and with what financing structure. Those aren't always the same objective.

Solar policy should be judged by distribution as well as volume. A system that adds capacity without broadening access can still deepen inequality.

A more demanding policy test would ask whether rebates, finance tools, community engagement, and project models are designed for people who cannot use standard credit-based rooftop pathways.

Representation tensions inside a broad industry coalition

SEIA also faces the familiar challenge of representing a broad commercial coalition. Utility-scale developers, distributed generation providers, storage firms, manufacturers, and service companies don't always have identical interests. A policy that accelerates one business model may inconvenience another. A supply-chain rule that benefits one segment may raise costs for another.

That doesn't invalidate the association's role. It means governments should read its positions as negotiated industry settlements rather than neutral technical truths.

For officials, two practical cautions follow:

- Separate industry efficiency from public interest. They often overlap, but not always.

- Interrogate who is absent. Renters, low-income households, and weakly financed communities usually don't sit inside trade associations with the same voice as capitalised market actors.

- Look beyond deployment metrics. Planning, access, grid connection, and affordability determine whether scale becomes legitimacy.

The next phase of solar politics will probably be less about proving that solar can grow and more about proving that solar can grow fairly, reliably, and with lower institutional friction.

Policy Takeaways and Recommended Actions

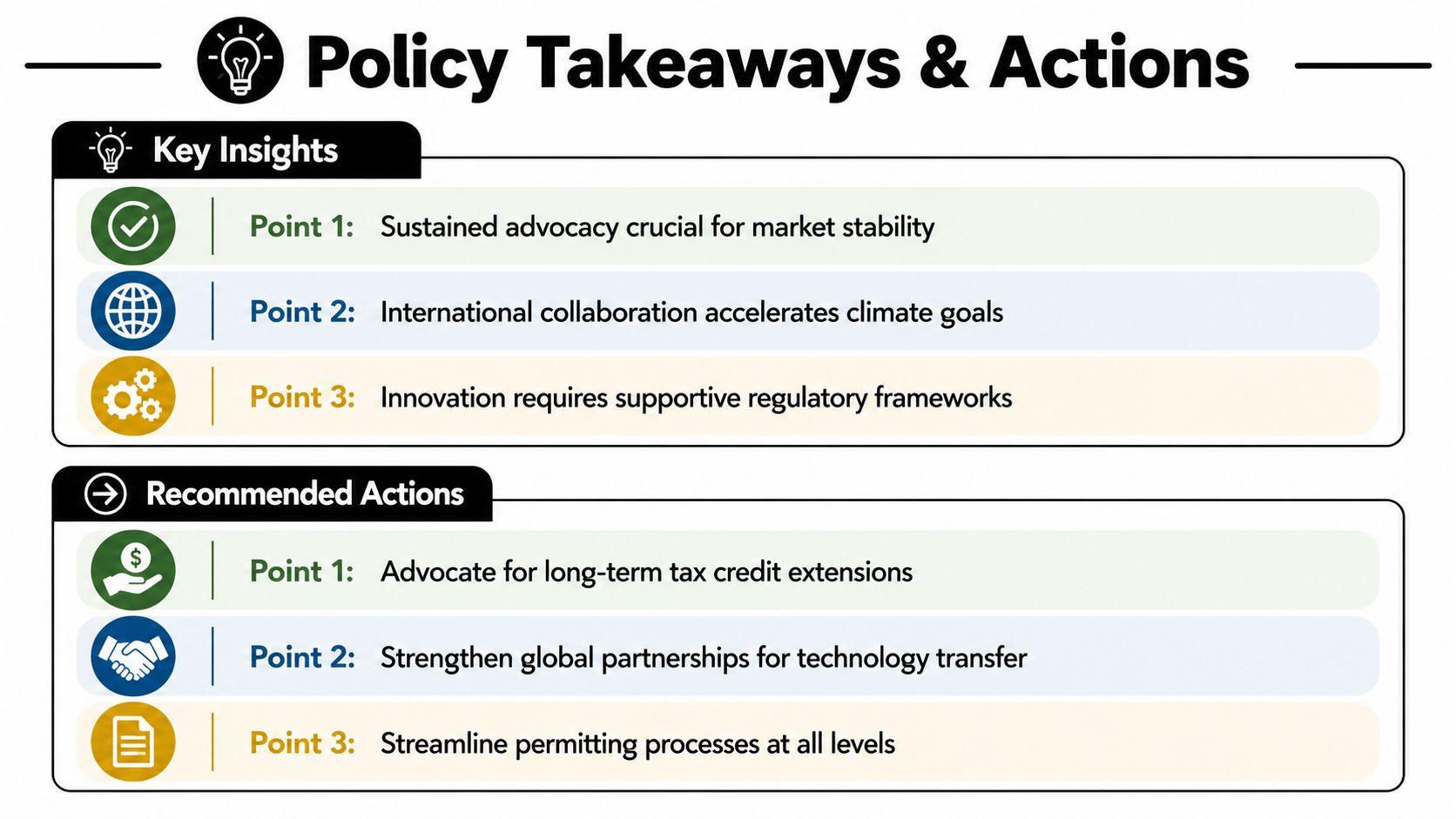

For a G20 delegation, the strategic lesson is clear. SEIA should be treated neither as a narrow lobby to ignore nor as a neutral authority to follow uncritically. It is a consequential market actor whose positions can help governments understand where solar deployment succeeds, where it stalls, and where the political economy becomes contested.

A practical agenda for governments and multilateral actors

A disciplined response would include the following actions:

- Engage, but preserve policy independence: Use industry bodies for technical intelligence and implementation feedback, while testing their proposals against affordability, equity, and system-wide resilience.

- Watch standards as closely as subsidies: Incentives attract projects, but standards and interconnection rules determine whether projects can move from announcement to operation.

- Prepare for spillovers from US policy: Trade measures, sourcing expectations, and industrial-policy shifts in the United States can alter commercial conditions in third markets.

- Build domestic institutional capacity: Countries need their own durable channels for structured dialogue between regulators, grid operators, financiers, and the solar sector.

- Treat equity as a design variable: If low-income households and hard-to-finance communities are left outside the transition, deployment success may become politically fragile.

SEIA's broader significance is that it demonstrates how an industry association can become part of energy governance itself. This is the core policy story. Not just advocacy, but the organised translation of commercial scale into public rules, technical norms, and political influence.

For more rigorous analysis on climate, energy, and international cooperation, follow Global Governance Media and bring these questions into your ministry, delegation, or boardroom. The solar transition is no longer just about capacity. It's about governance, standards, equity, and strategic coordination across borders.