Byline: Dr Eleanor Marsh

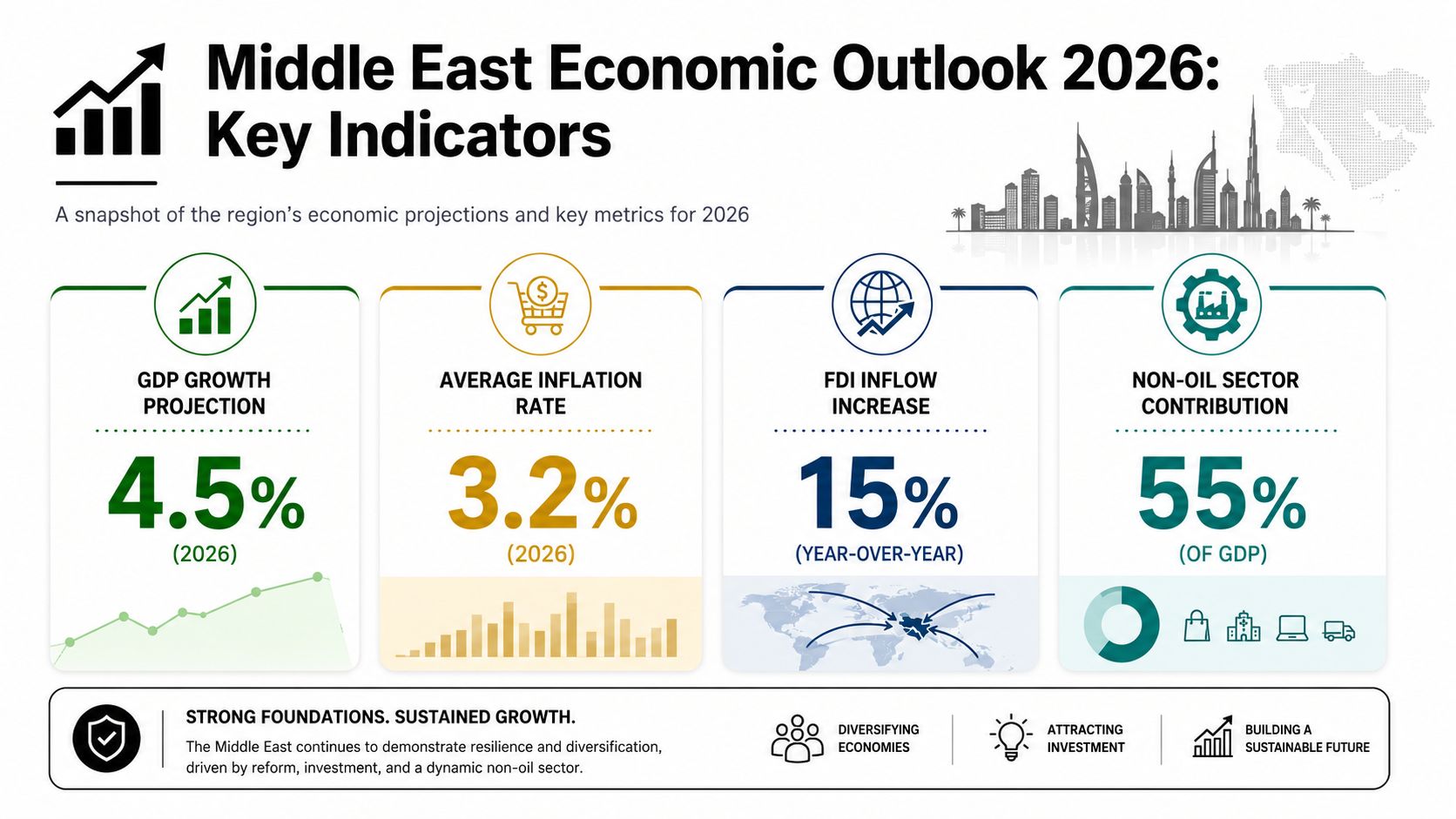

The most revealing number in Middle East markets isn't an oil price. It is USD 1,644.68 billion, the projected size of the Middle East retail market by 2034, up from USD 932.54 billion in 2026 according to Middle East retail market projections. That figure matters because it shifts the analytical frame. It points to household demand, distribution networks, digital payments, health spending, education demand, and imported consumer and business services.

For policymakers and investors, the region now has to be read as a multi-speed economic system rather than a single hydrocarbons story. Oil still shapes fiscal space, external balances, and geopolitical influence. But market opportunity is increasingly mediated through retail expansion, digital procurement, logistics capacity, analytics adoption, and jurisdiction-specific reform paths. Firms considering Gulf entry are already adapting capital structures and working capital planning to this reality, as seen in practical discussions of UAE business expansion financing.

That change also has a governance dimension. Economic transformation isn't just a commercial story. It is tied to social capacity, institutional reform, and public legitimacy, themes that sit behind wider debates on building stronger Arab societies through global governance. The central mistake in much commentary is to ask whether the Middle East is investable. The better question is which market, through which channel, under which regulatory assumptions, and with what exposure to energy and freight shocks.

Table of Contents

- An Introduction to the New Middle East Economy

- The Macroeconomic Landscape in 2026

- Key Sector Breakdowns and Transformations

- The Role of Capital Flows and Sovereign Wealth Funds

- Navigating Regulatory Frameworks and Governance

- Geopolitical and Climate Risk Transmission

- Strategic Recommendations for Decision-Makers

An Introduction to the New Middle East Economy

Middle East markets are often described with a vocabulary that is already out of date. The older frame treated the region as a commodity complex dominated by fiscal cycles and geopolitical risk. That frame still captures part of reality, but it no longer captures the whole of it.

The more useful starting point is structural duality. The region remains significantly shaped by hydrocarbons, yet it is also building demand in sectors that depend on urban consumption, services trade, and digital infrastructure. Historical trade structure helps explain this coexistence. The IMF notes that oil and oil-related products have historically represented about three quarters of Middle Eastern exports, while the region accounted for about 4% of world trade and 15% of global oil exports, with intra-regional trade at only about 8% of both exports and imports according to IMF analysis of MENA trade structure. That low level of intra-regional trade is strategically important. It means extra-regional partners continue to matter for finance, logistics, insurance, standards, and market access.

The region is diversifying, but not uniformly

Some jurisdictions are moving quickly into high-value services, data-intensive administration, and logistics intermediation. Others remain more exposed to administrative friction, fiscal dependence on energy, or weaker institutional capacity. Treating all of this as one “Middle East market” produces weak policy and weaker investment decisions.

Middle East markets should be segmented first by jurisdiction, then by sector, and only then by demand category.

A senior decision-maker should therefore read the region through three filters:

- External dependence: Several economies remain connected to global demand, capital, and imported regulatory expertise.

- Domestic consumption: Expanding retail and service demand signal where non-oil opportunities are broadening.

- Institutional variation: Reform depth, legal enforceability, and localisation requirements differ sharply.

Why 2026 looks different

The decisive shift is that opportunity now sits at the intersection of state capacity and market modernisation. A port project, a digital identity system, a cloud procurement programme, and a consumer import channel may all belong to the same growth story. That is why a narrow commodities lens misses what matters. It sees volatility, but not adaptation.

The Macroeconomic Landscape in 2026

Aggregate scale and uneven resilience

A region with output measured in the trillions can still transmit risk through a small number of channels. In 2026, the more useful question is not whether the Middle East is large enough to matter. It is which jurisdictions can absorb shocks from energy prices, tighter global financial conditions, and domestic reform fatigue without impairing investment returns.

That distinction matters because aggregate regional figures hide major differences in fiscal space, labour market structure, and external financing needs. Hydrocarbon exporters with strong sovereign balance sheets can cushion volatility for longer. More import-dependent economies face a narrower margin for policy error, especially where inflation, unemployment, or exchange-rate pressure feed directly into household demand and business costs.

For policymakers and investors, segmentation should start with macro buffers rather than headline growth. A jurisdiction with moderate expansion and predictable policy execution may offer a stronger operating environment than a faster-growing market with weak payment discipline, higher refinancing risk, or inconsistent administrative enforcement.

Tax policy illustrates the point. Gulf jurisdictions continue to attract attention for business-friendly regimes, and resources on understanding the UAE's zero tax strategy are relevant for market-entry planning. Yet tax efficiency is only one part of the decision. The stronger indicator is whether fiscal incentives sit inside a wider system of contract enforceability, logistics reliability, skilled labour access, and regulatory follow-through.

The 2026 test is transmission, not size

The central macro question for 2026 is how quickly external shocks pass through to domestic demand, credit conditions, and public spending. In some markets, lower energy revenues would first affect state-led investment, then supplier payments, then employment. In others, the first transmission channel is imported inflation, which weakens real consumption and raises pressure on subsidy systems or public wages.

This is why “Middle East markets” should be treated as a portfolio of different macro regimes. The Gulf is not interchangeable with the Levant. Large consumer markets are not interchangeable with logistics hubs. Reform announcements are not interchangeable with administrative capacity.

A practical screening framework is to separate jurisdictions into three groups: balance-sheet strong states that can finance transition over multiple years, reforming middle-income markets where execution risk is the main variable, and fragile economies where political or fiscal stress can quickly override commercial fundamentals. That approach produces better policy prioritisation and better capital allocation than a single regional thesis.

Domestic demand remains the cleaner signal

Consumer activity still matters, but less as a headline growth story than as evidence of institutional quality. Where domestic demand broadens in a durable way, it usually reflects functioning import channels, payments infrastructure, urban transport, warehousing, licensing systems, and dispute resolution. Those are the mechanics that turn income into investable demand.

This has a direct implication for 2026 strategy. Analysts should track whether demand is supported by productivity and employment gains, or by temporary fiscal stimulus and imported liquidity. The first case supports long-duration investment. The second can inflate valuations while leaving firms exposed to abrupt policy tightening or weaker household balance sheets.

For officials comparing opportunities across jurisdictions, relative screening tools are more useful than aggregate regional narratives. Benchmarks such as the country risk and reform comparisons in the Emerging Markets Index can help frame where institutional change is strengthening the macro setting, and where headline optimism still runs ahead of implementation.

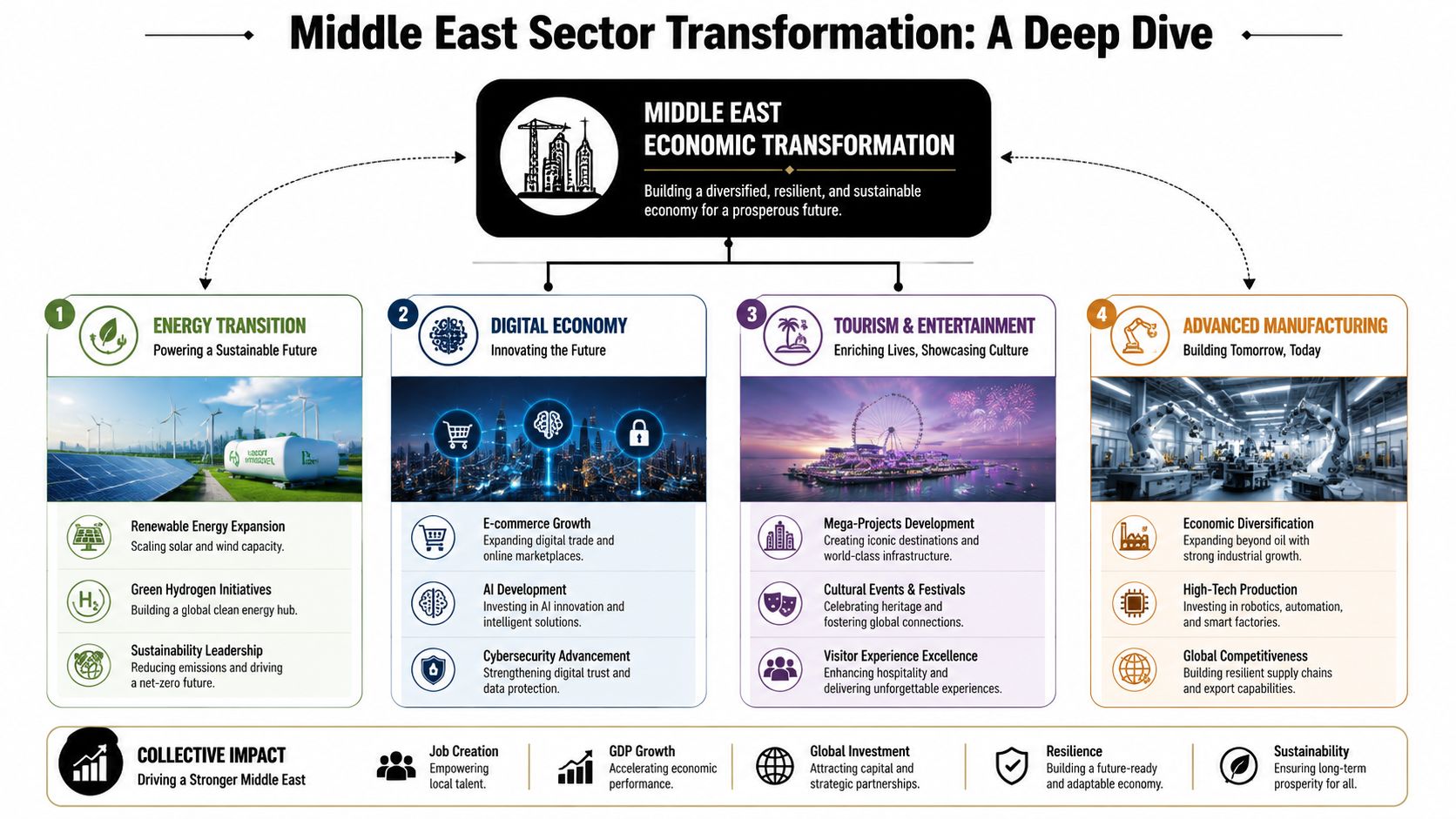

Key Sector Breakdowns and Transformations

Energy still anchors the system

Any serious reading of middle east markets begins with energy, but it shouldn't end there. Hydrocarbons still determine fiscal flexibility, sovereign liquidity, and external financial capacity in much of the region. They also shape how governments sequence diversification. A state with stronger energy revenues can fund infrastructure, absorb reform costs, and support strategic sectors for longer.

Yet the relevant analytical shift is from “oil versus non-oil” to “oil financing non-oil transition”. That's why energy should be read as a balance-sheet enabler as much as an export category. It is also why urban sustainability experiments matter. Projects associated with low-carbon urban systems, industrial efficiency, and clean technology signal how some jurisdictions are trying to convert resource rents into future capability. The policy logic behind that shift is visible in discussions around Masdar City and sustainable urban innovation.

Digital capability is becoming a procurement signal

The clearest quantified sector signal in the region is analytics demand. Data analytics spending in the Middle East and Africa is forecast to increase from USD 5,938.5 million in 2024 to USD 15,714.4 million by 2030, implying a 16.8% CAGR, according to Middle East and Africa data analytics market forecasts. That is economically significant because analytics budgets usually arrive with adjacent demand for cloud services, compliance architecture, software localisation, cybersecurity, and sector-specific decision tools.

This shifts how exporters should think about entry. A public-sector buyer or regulated industry in the Gulf may not be looking for software in isolation. It may be buying a bundle that includes reporting, localisation, interoperability, and governance assurance.

Three practical conclusions follow:

- Professional services are strengthening their position: Advisory, implementation, and managed-service providers can sell into digital modernisation if they understand localisation and sector regulation.

- Compliance is part of the product: In many procurements, reporting capability and data governance aren't add-ons. They shape whether a solution is credible.

- Demand quality matters more than hype: Markets with active analytics spending often provide stronger signals than markets with louder rhetoric around innovation.

Trade and finance are converging

Trade in the region increasingly depends on platform efficiency. Import demand, warehousing, payments, customs systems, and re-export logistics are becoming more tightly integrated. This rewards firms that can combine supply chain management with financing and regulatory intelligence.

A useful way to read sectoral transformation is through operational combinations rather than isolated industries:

| Sectoral node | What matters most |

|---|---|

| Energy-linked industry | Cost pass-through, state financing, long-cycle procurement |

| Consumer and retail systems | Distribution, import standards, brand localisation |

| Digital and analytics | Data governance, cloud readiness, public procurement fit |

| Trade and logistics | Port access, documentation speed, financing and insurance |

The strongest opportunities often sit where sectors overlap. Logistics plus finance. Retail plus data. Energy plus industrial services.

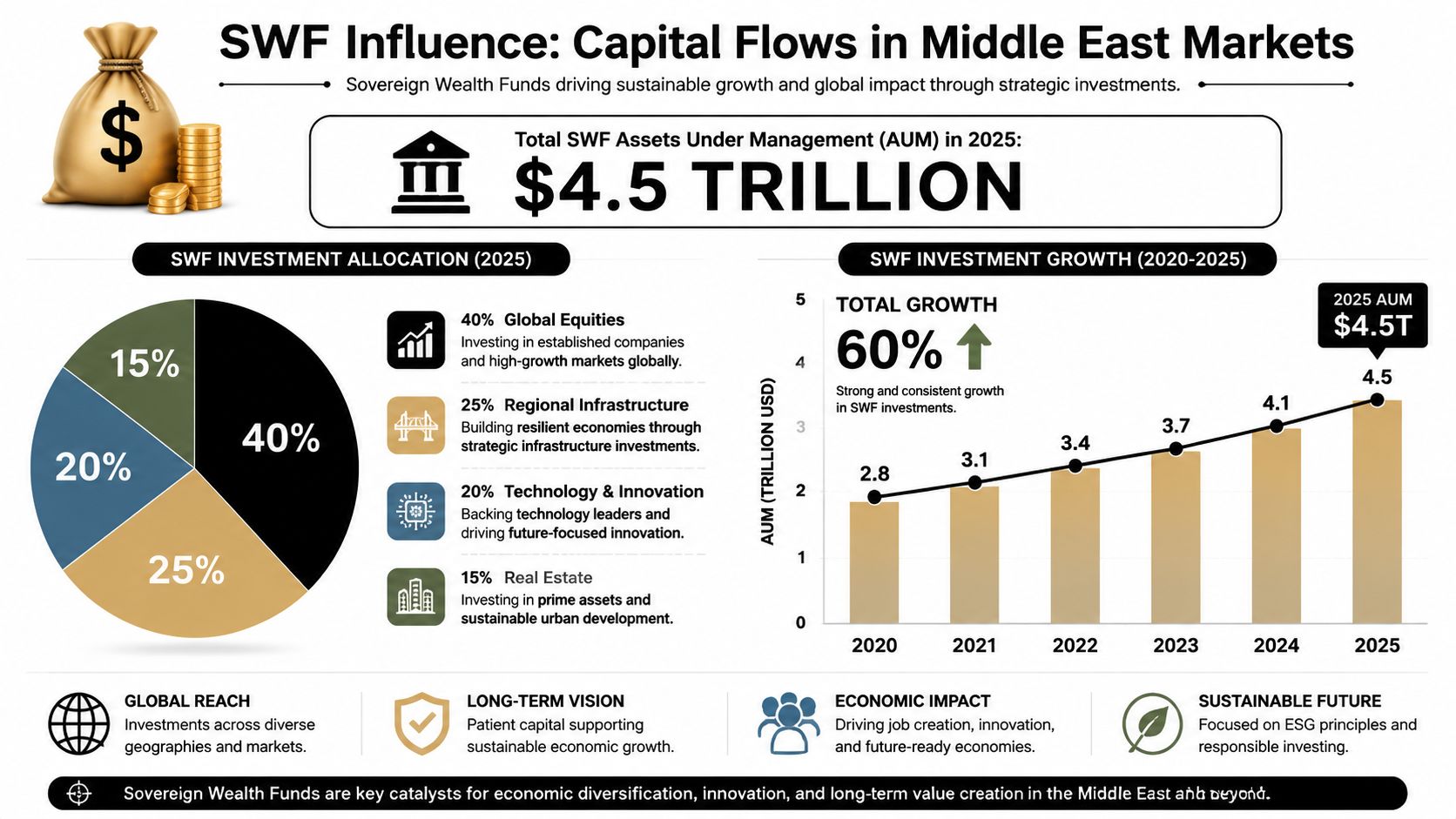

The Role of Capital Flows and Sovereign Wealth Funds

A small number of state-backed investors now influence capital allocation across energy, logistics, technology, real estate, and global financial markets. That concentration matters because it changes how shocks travel through the region and how opportunities should be assessed by jurisdiction.

Capital as industrial policy

In several Middle Eastern economies, the state acts as owner, allocator, borrower, and market maker at the same time. Sovereign wealth funds, development vehicles, and other state-linked investors therefore do more than pursue financial returns. They help determine which sectors scale, which supply chains localise, and which foreign firms gain access to long-cycle demand.

That requires a different reading of investment announcements. A large allocation into ports, downstream industry, tourism, digital infrastructure, or advanced manufacturing should be treated as a signal about future procurement depth, regulatory attention, and ecosystem formation in a specific market. The investable question is not whether the region is attracting capital. It is which jurisdiction is using capital to build durable productive capacity, and which is relying on spending cycles that may fade if fiscal conditions tighten.

This distinction is easy to miss. A hydrocarbon exporter with large external surpluses and a globally active sovereign fund presents a different risk profile from a market where capital inflows depend more heavily on debt rollover, external support, or politically sensitive portfolio flows. Grouping both under a single “Middle East markets” label obscures the transmission channels that matter most to investors and policymakers.

A short discussion of capital intermediation is useful here:

A framework for reading capital flows

Three questions help separate durable opportunity from headline noise.

First, what is the source of capital. Domestically anchored sovereign balance sheets usually provide more policy continuity than short-term portfolio inflows. Second, where does the capital go. Investment into tradable sectors, logistics, and industrial capability tends to have wider multiplier effects than prestige assets alone. Third, how does the capital move through the economy. Direct state procurement, public-private partnerships, domestic bank lending, and offshore listing activity each create different entry points and different vulnerabilities.

This framework also clarifies risk transmission. A decline in oil prices does not affect all jurisdictions in the same way. In one economy, it may slow sovereign deployment but leave reserves strong. In another, it can tighten banking liquidity, delay contractor payments, widen spreads, and weaken import demand. The practical implication is straightforward. Capital-flow analysis should begin with fiscal buffers, external accounts, and institutional channels, not with regional sentiment.

Why the UK connection remains strategic

The UK remains tied to these capital flows through trade finance, insurance, legal services, asset management, project advisory, and procurement exposure. That connection is not only about export volumes. It reflects the role of London-based institutions in structuring, insuring, financing, and intermediating regional investment.

For UK decision-makers, the policy relevance is twofold. Strong Gulf balance sheets can support outward investment, imports of high-value goods and services, and cross-border deal activity. The same channels can transmit volatility quickly when energy prices fall, shipping security deteriorates, or sovereign funding costs rise. Firms assessing exposure to Iran-related trade constraints should also distinguish between regional capital hubs and sanctioned markets. Coreties' guide to Iran exports is a useful reference point for that narrower operational question.

The broader conclusion is that capital flows in the Middle East should be read as a map of state capacity, external vulnerability, and sector formation. Investors who segment the region by balance-sheet strength, institutional depth, and transmission channels will make better decisions than those relying on a single geopolitical narrative.

Navigating Regulatory Frameworks and Governance

Jurisdiction comes before strategy

The first operational rule is simple. Don't enter “the Middle East”. Enter a specific jurisdiction for a specific reason. Effective market entry requires treating the region as a set of distinct country-level opportunities, each with its own regulatory environment and risk profile, as emphasised in market entry guidance for the Middle East and Africa.

That sounds obvious, but firms still get this wrong. They infer regional accessibility from one Gulf success story, or they extrapolate one difficult market experience across the whole region. Both errors produce bad allocation decisions.

A jurisdiction-first approach means asking different questions in different places. In one market, foreign ownership rules may matter most. In another, public procurement access or dispute resolution may decide viability. Elsewhere, sanctions, customs treatment, or the mechanics of trade documentation may dominate.

A practical screening method

Decision-makers need a compact screening tool before committing management time or political capital. A useful sequence is:

- Define the commercial function. Are you selling consumer products, public-sector services, industrial inputs, or digital systems?

- Test legal fit. Can your ownership, licensing, and contracting model operate lawfully and predictably in the jurisdiction?

- Assess counterpart quality. Which local partner, distributor, sponsor, or procurement channel is credible?

- Map friction points. Where could customs, payments, localisation, certification, or dispute risk interrupt the business case?

For firms dealing with harder trade corridors, granular operational knowledge matters more than generic regional advice. In specialised contexts, practical resources such as Coreties' guide to Iran exports can be useful because they focus on actual export mechanics rather than broad market optimism.

Legal openness and commercial usability are not the same thing. A market can be formally accessible and still be operationally difficult.

Governance analysis should therefore distinguish between reform signalling and execution quality. That distinction is where many entry models succeed or fail.

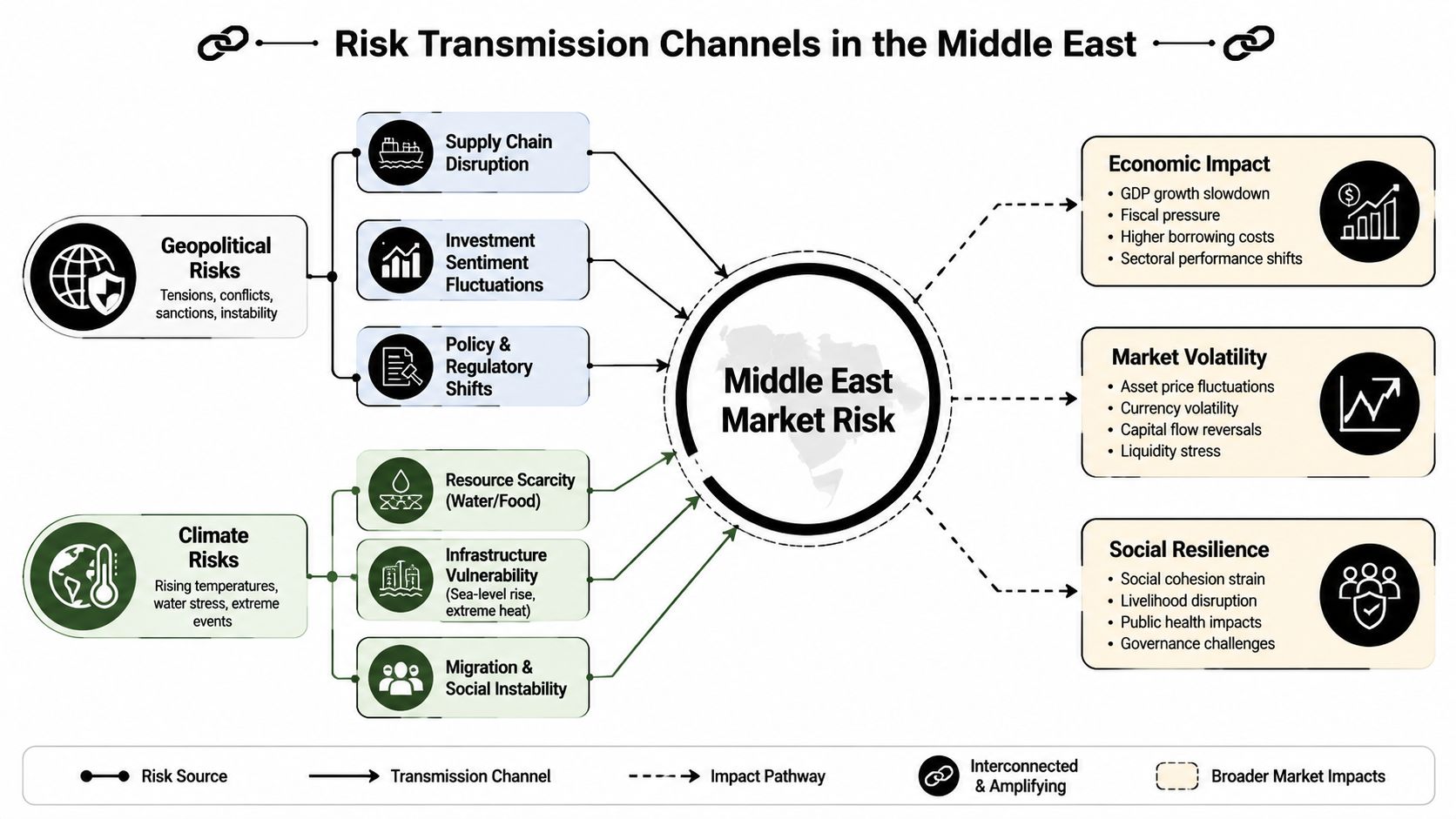

Geopolitical and Climate Risk Transmission

The relevant question is transmission, not headlines

Most geopolitical commentary on middle east markets is descriptively correct and analytically incomplete. It tells readers that conflict matters, but not how the impact travels through prices, contracts, shipping decisions, and inflation expectations.

The core transmission channel remains energy. Because the Middle East supplies roughly a third of global crude oil, regional instability can materially affect global oil prices, with lagged pass-through into UK inflation through transport, manufacturing, and utility costs, according to IMF-linked analysis on oil and inflation transmission. The point for decision-makers is not just that oil prices move. It is that the economic effect arrives with lags and through multiple cost layers.

That has immediate operational consequences:

- For finance ministries: watch inflation persistence, not only the initial energy move.

- For central banks: monitor the pass-through into producer costs and regulated utilities.

- For importers: track freight risk, insurance pricing, and delivery delays alongside commodity benchmarks.

- For investors: focus on episodic repricing in shipping, energy, and hedging costs rather than assuming a uniform equity response.

Markets often absorb the first shock in price. The harder problem is the second-round effect through contracts, transport costs, and policy response.

Climate risk compounds economic concentration

Climate risk interacts with these channels rather than sitting apart from them. Heat stress, water pressure, and infrastructure vulnerability can raise the cost of doing business, complicate food systems, and intensify social and fiscal pressure in already uneven economies. In a region where some states have substantial buffers and others do not, climate shocks won't produce a single regional outcome.

This means geopolitical and climate risks should be analysed together in strategic planning. A logistics corridor exposed to conflict risk may also be exposed to climate-related disruption. A food import model may be vulnerable to both freight dislocation and domestic resource stress. The policy advantage goes to institutions that monitor interaction effects rather than isolated risks.

Strategic Recommendations for Decision-Makers

Priorities for policymakers

Policymakers should begin by abandoning the “regional average” approach. It is too blunt for trade strategy, investment diplomacy, and resilience planning. A more effective framework has four parts.

- Segment by jurisdiction: Country-specific market mapping should precede trade missions, export finance priorities, or investment promotion.

- Build transmission monitoring: Energy shocks should be tracked through inflation, shipping, insurance, and industrial input channels, not just through spot price movements.

- Align commercial diplomacy with capability: Support should focus on sectors where outside firms can supply more than products, including standards, finance, analytics, compliance, and public-service delivery tools.

- Treat resilience as economic policy: Climate adaptation, logistics security, and energy contingency planning belong inside market strategy.

Public authorities in the UK and other external partners should also recognise that ties with the region are not purely commercial. They sit at the intersection of energy security, inflation management, industrial competitiveness, and foreign policy.

Priorities for firms and investors

Executives should use a stricter filter than “high-growth region”. Opportunity in middle east markets is real, but it is highly conditional. The best-performing strategies usually have three features.

First, they choose a jurisdiction before choosing a narrative. A firm should know why it is entering one market rather than another, and what legal and operational assumptions justify that choice.

Second, they build around execution, not presentation. In practice that means local partnerships, contract enforceability, localisation capacity, and working capital discipline. Boards should ask whether the business can still function if freight costs rise, a licence takes longer than expected, or a partner underperforms.

Third, they hedge transmission risk. That doesn't only mean commodity exposure. It means reviewing shipping routes, insurance assumptions, inventory strategy, contractual pass-through clauses, and financing flexibility.

A concise decision framework is useful:

| Decision area | Better question |

|---|---|

| Market selection | Which jurisdiction fits our sector and risk tolerance? |

| Operating model | What local structure makes enforcement and delivery credible? |

| Risk management | Which shocks would impair margins, timelines, or compliance? |

| Growth thesis | Is demand being driven by consumption, state procurement, or digital modernisation? |

The broad conclusion is clear. The region shouldn't be approached as a single bet on geopolitics or oil. It should be approached as a set of differentiated markets linked by capital, trade corridors, digital adoption, and shared exposure to external shocks. Decision-makers who segment carefully will find more opportunity than the headlines imply. Those who do not will misread both the upside and the risk.

For more policy-focused analysis on international trade, energy, governance, and the strategic choices shaping global markets, explore Global Governance Media. It's a valuable resource for decision-makers who need concise, evidence-led perspectives on complex cross-border risks and opportunities.