By Daniel Mercer

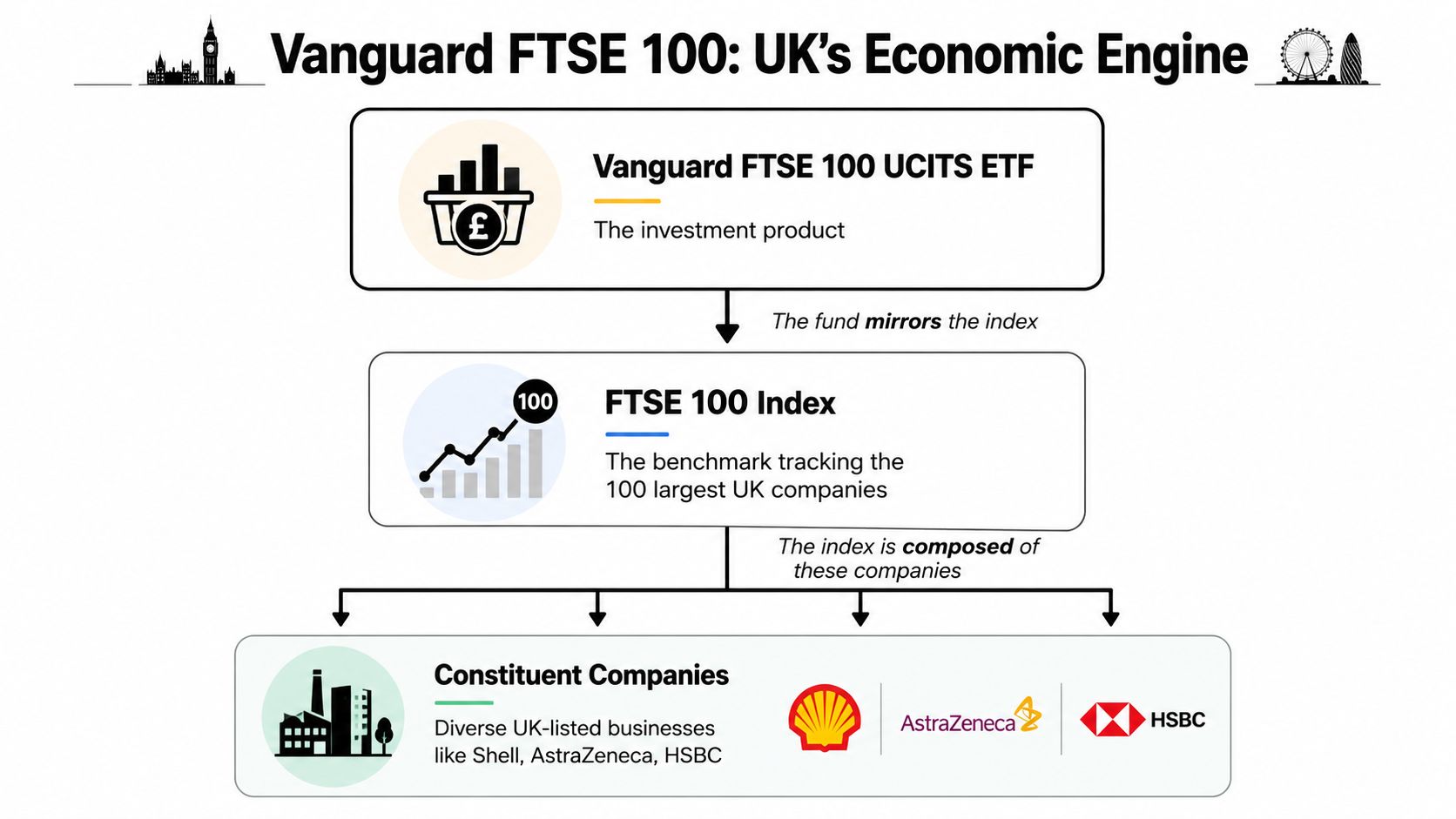

A fund can be passive in construction and still be powerful in consequence. That's the counterintuitive reality of the Vanguard FTSE 100. It is designed to track a benchmark, not to express a view on industrial strategy, climate governance or board accountability. Yet because it follows the FTSE 100 Index, which has been the UK's main blue-chip equity benchmark since its launch on 3 January 1984, it sits inside the ownership architecture of Britain's largest listed companies.

That matters because the benchmark itself is systemically large. By March 2026, the FTSE 100's aggregate market capitalisation was reported at about £2.436 trillion. A vehicle that mechanically channels savings into that market isn't just another consumer product. It is part of the institutional plumbing through which corporate power, voting rights and governance expectations are mediated.

Readers who usually approach passive funds through a portfolio-construction lens may find it helpful to contrast this with the US-centred questions in VTI vs VTSAX. The UK issue is narrower and sharper. When an index fund tracks the country's flagship equity benchmark, its significance extends beyond diversification or convenience and into the governance of nationally important firms. That wider policy context sits close to debates on capital markets development, where the line between market efficiency and public interest is often thinner than it appears.

Table of Contents

- Introduction The Vanguard FTSE 100 as a Policy Actor

- Deconstructing the UK's Economic Engine

- Concentration and Influence Top Holdings and Sector Biases

- The Efficiency Engine Fees Performance and Systemic Risk

- The Passive Ownership Governance Dilemma

- Implications for UK Economic Sovereignty and Global Policy

- Conclusion The Future of Indexing and Corporate Governance

Introduction The Vanguard FTSE 100 as a Policy Actor

The standard description of the Vanguard FTSE 100 is technically correct and politically incomplete. It is a fund that tracks a benchmark of large UK-listed companies. But once a product becomes a durable holder of the country's corporate flagship names, it stops being neutral in effect, even if it remains rules-based in design.

That's because ownership is never only financial. Ownership carries votes, engagement choices, escalation decisions and, in practice, a view on what boards can get away with. A passive fund doesn't choose which blue chips to own in the same way as an active manager. It does, however, choose how seriously to treat stewardship once those holdings are locked in by index methodology.

The key question isn't whether the Vanguard FTSE 100 is an active fund. It isn't. The real question is whether a passive owner can remain passive when regulation expects visible stewardship.

The policy challenge becomes sharper in the UK because the fund's influence is concentrated in nationally important companies rather than spread across a very broad global universe. That creates a direct line from index mechanics to boardroom incentives. It also creates a quiet accountability problem. Retail holders may think they are buying a low-maintenance market tracker. In reality, they are delegating part of the governance function over the UK corporate core.

Why policy officials should care

Three features make the Vanguard FTSE 100 relevant beyond asset management.

- It channels ownership into the UK corporate centre: the fund tracks the country's primary blue-chip benchmark rather than a peripheral market segment.

- It aggregates voting rights: those rights attach to shares whether the investment process is active or passive.

- It can shape governance indirectly: boards respond to their largest and most stable shareholders, even when those shareholders claim not to be making discretionary bets.

That combination turns an apparently simple product into a policy actor. Not because it seeks that role, but because the UK's largest listed companies can't be governed without regard to who owns them and how they use that ownership.

Deconstructing the UK's Economic Engine

The Vanguard FTSE 100 is not just a low-cost wrapper around British equities. It is a rules-based channel through which household savings, pension assets and international capital are converted into stable ownership stakes in the corporate core of the UK economy.

That distinction matters because the fund does not allocate capital across a broad or neutral slice of national output. It replicates a benchmark designed around the largest listed companies on the London market. In practice, that means the product directs capital toward firms that already sit closest to the centre of British corporate power. For readers tracking the wider ownership chain, our analysis of how capital flows through modern markets and institutions provides useful context.

Why the fund structure matters

The legal wrapper shapes the ownership pathway as much as the index does. This vehicle uses a UCITS structure domiciled outside the UK, while investing in companies that remain central to the UK's listed economy. That arrangement is ordinary in European asset management. Its policy implications are less ordinary.

A cross-border fund structure affects who can hold the product, which supervisory rules apply to the vehicle, how investor protections are standardised, and how voting rights over major UK issuers are organised through intermediated ownership chains. For a retail investor, that may feel administrative. For a policymaker, it goes directly to market access, supervisory coordination and the institutional location of shareholder power.

Why index design becomes a governance mechanism

Market-cap weighting is often described as a technical choice. It is better understood as a constitutional rule for capital allocation. The largest listed firms receive the largest share of incoming passive money because the methodology assigns them the largest weights. No portfolio manager needs to endorse those firms one by one. The benchmark embeds the preference.

That has consequences well beyond portfolio construction. Size attracts more passive capital. More passive capital can reinforce shareholder stability. Stable ownership can increase the influence of large fund groups in routine governance matters such as director elections, remuneration policies and climate disclosures. The fund therefore mirrors the structure of the market and helps reproduce it.

| Mechanic | Governance implication |

|---|---|

| Larger firms carry larger index weights | Voting power concentrates in a small group of nationally significant issuers |

| Rebalancing follows index rules | Ownership shifts track benchmark methodology rather than case-by-case judgement about management quality |

| Inclusion depends on listed size and market status | Incumbent corporate champions remain deeply embedded in passive ownership chains |

The policy point is narrower and more important than a standard product description suggests. The Vanguard FTSE 100 does not merely offer exposure to British equities. It helps determine how ownership, voting rights and stewardship attention are distributed across Britain's most powerful listed companies.

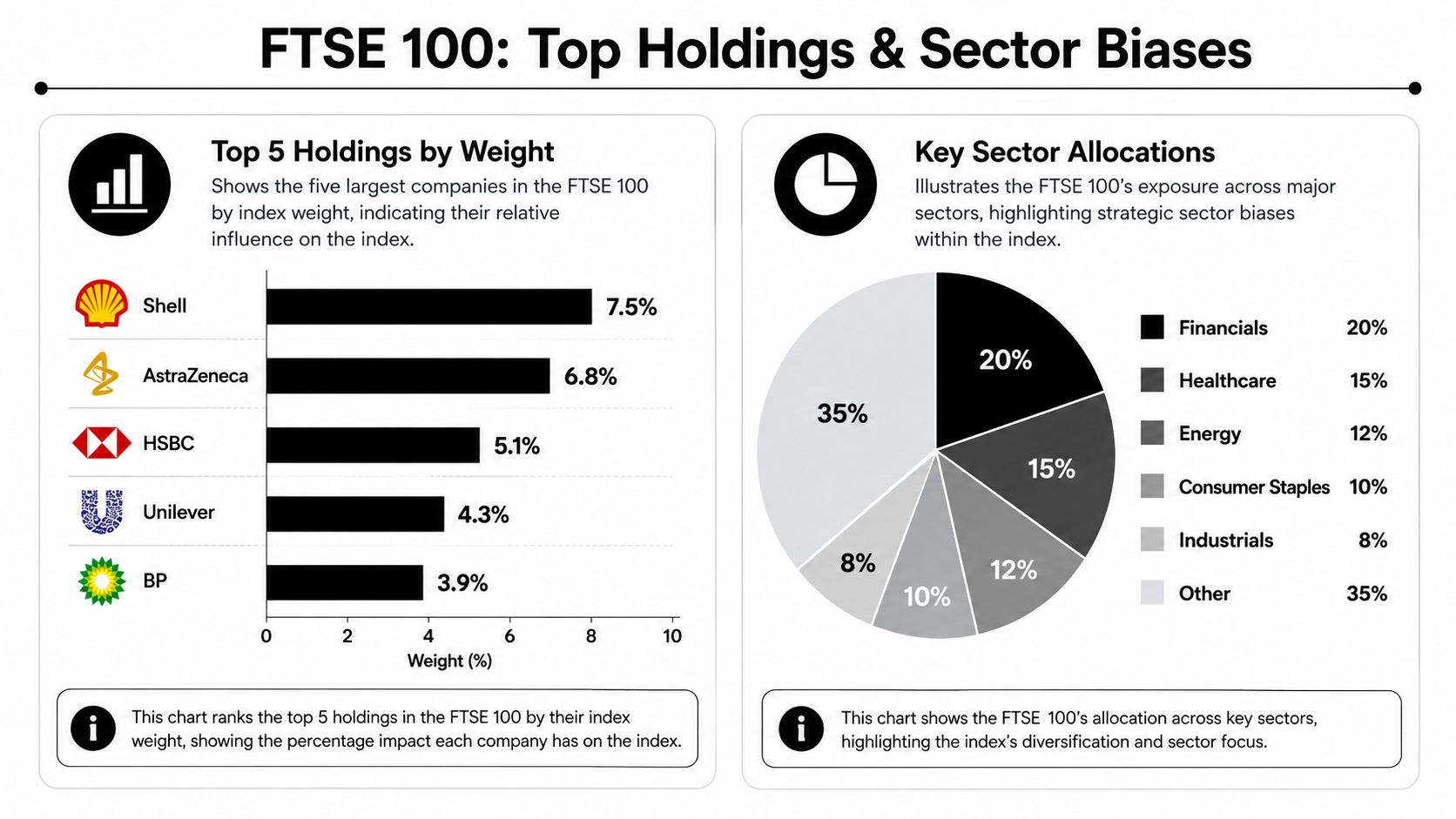

Concentration and Influence Top Holdings and Sector Biases

A hundred stocks sounds diversified until you look at how the weights are distributed. The FTSE 100 is a narrow governing mechanism disguised as a broad market index. The benchmark has just 100 constituents, and the top 10 weight is 48.57%, compared with 23.71% for the FTSE All-World, according to the FTSE Russell factsheet for UKX.

That single comparison tells policymakers something important. This isn't simple equity exposure to Britain. It is concentrated exposure to a small cluster of corporate giants. The return stream, the voting bloc and the stewardship challenge are all disproportionately tied to that cluster.

A narrow index can still dominate attention

Market-cap weighting amplifies incumbency. Large companies attract larger passive allocations because they are large already. That tends to reinforce the centre of gravity in the UK market rather than challenge it.

For an investor, that may look efficient. For a policymaker, it raises harder questions about how the ownership system interacts with industrial composition. If the largest listed issuers sit in sectors with outsized importance to energy security, pharmaceuticals, banking or consumer staples, a tracking fund becomes a stable owner of strategic assets almost by accident.

A useful way to think about this is through the lens of following the money in corporate systems. Capital doesn't just finance firms. It allocates attention, legitimacy and negotiating power inside the economy.

Why concentration becomes a policy issue

Concentration changes what stewardship has to do. A broad global tracker can plausibly treat company-specific engagement as one task among many. A national flagship tracker with a high top-end concentration has less room for that abstraction.

Three implications follow.

- Board influence is centralised: when the same handful of firms drive a large share of index behaviour, voting decisions around those issuers carry disproportionate system effects.

- Sector shocks transmit quickly: if large weights sit in globally exposed sectors, passive owners import those risks directly into household and institutional portfolios.

- Governance failures have index consequences: a problem at a major constituent isn't just an idiosyncratic event. It can affect perceptions of the benchmark itself.

A concentrated passive fund doesn't choose concentration. But once concentration exists, it inherits responsibility for what that concentration means.

The Vanguard FTSE 100 becomes more than an access product. It becomes a standing owner in a market where ownership is highly uneven. That unevenness is the beginning of its policy relevance.

The Efficiency Engine Fees Performance and Systemic Risk

Low fees are often treated as an unqualified public good. In a concentrated national equity market, they also change how ownership power is organised.

The Vanguard FTSE 100 matters because it lowers the cost of holding the UK's largest listed companies through a standardised product that can sit inside retail accounts, advised portfolios and institutional allocations. As noted earlier, that access has been built through multiple fund wrappers over time. The result is operational efficiency, broad distribution and a shareholder base that can become more stable than price commentary suggests.

That stability has policy consequences. A fund that is easy to buy and inexpensive to hold is more likely to become part of default savings behaviour. Capital then reaches major issuers through routine portfolio processes rather than repeated company-level judgments. For households, that can improve diversification and reduce cost drag. For the market, it can also mean that a larger share of ownership is less sensitive to managerial underperformance unless stewardship and voting mechanisms compensate for the absence of an exit response.

Fees are central to this model. Low-cost index replication leaves little room for labour-intensive, issuer-by-issuer intervention across every governance dispute. The economic logic is straightforward. Investors choose the product partly because it strips out discretionary stock selection and the higher operating costs that usually accompany it. Yet the legal and economic rights attached to the shares remain active. Voting rights, engagement expectations and scrutiny of disclosure quality do not disappear because the portfolio is rules-based.

That creates a structural tension, not a temporary one.

- Cost efficiency depends on standardisation: portfolio management, trading and stewardship processes are designed to work at scale.

- Governance failures are company-specific: audit weakness, transition-plan credibility, board oversight and remuneration design need granular judgment.

- Index funds retain owner responsibilities: a passive mandate limits security selection, but it does not limit the need to vote, engage and monitor.

The systemic risk follows from that mismatch. It is a governance transmission problem. If a significant block of the shareholder register is organised around low-cost permanence, boards may face weaker market discipline between index reviews, especially when the company is too large to lose market relevance quickly. In that setting, weaknesses in disclosure become more consequential because passive ownership relies heavily on reported information to prioritise engagement. Problems of corporate transparency failure in major listed firms therefore affect not only valuation accuracy, but also the quality of stewardship across the index.

There is also a legal and accountability dimension. Low fees do not remove the possibility of disputes over fiduciary conduct, disclosures or investor treatment. The existence of external scrutiny, including discussion of investor rights against Vanguard, is a reminder that scale and passivity do not place a fund outside the wider architecture of market accountability.

The broader conclusion is easy to miss. The efficiency engine does more than reduce costs for end investors. It reallocates how monitoring is performed across the UK corporate system, shifting weight from trading decisions toward stewardship quality, disclosure integrity and regulation. In a market where a small number of companies carry large economic and political significance, that shift is not a technical footnote. It is a question of how corporate power is supervised when ownership is permanent, dispersed among savers, and exercised through an intermediary built to be cheap.

The Passive Ownership Governance Dilemma

The strongest case for the Vanguard FTSE 100 is also the source of its hardest policy problem. It offers disciplined, rules-based exposure to the UK blue-chip market through physical ownership of securities. That means it is not merely using synthetic exposure or abstract benchmark representation. It owns shares and inherits the obligations that come with them.

A passive mandate still produces active obligations

The unresolved issue is how that ownership model fits the UK's evolving governance framework. A notable gap in the public debate is the lack of UK-specific analysis on how the fund's passive indexing approach interacts with post-2023 corporate governance reforms, including biodiversity and climate disclosure expectations linked to active shareholder engagement. According to the cited product discussion, there was a 35% increase in 2024 shareholder engagement cases reported by the FCA, while existing coverage has focused more on tracking mechanics and NAV information than on whether a 102-stock portfolio held through physical acquisition is meeting new responsible-ownership expectations, as discussed on Vanguard Investor's FTSE 100 UCITS ETF page.

That gap matters because modern UK governance increasingly expects shareholders to do more than register discontent privately. They are expected to scrutinise transition plans, disclosure quality, biodiversity impacts and board accountability with more consistency and more evidence.

A passive manager can reply that stewardship and indexing are compatible. In principle, that's true. In practice, the challenge is scale. A single voting policy applied across many issuers may not be enough where company-level problems are distinct, politically salient and tied to domestic regulatory reforms.

Where the policy gap sits

The policy concern isn't that passive ownership is illegitimate. It's that passive ownership can become governance-light unless regulators, trustees and asset managers define clearer expectations for what serious stewardship looks like.

A useful comparison is legal accountability from the investor side. Readers interested in how disputes over fund oversight and investor protection are framed in practice may find the discussion of investor rights against Vanguard useful as a contrast point. It doesn't answer the UK stewardship question directly, but it shows how governance disputes around large asset managers rarely stay confined to portfolio performance alone.

The core governance risk can be stated plainly:

| Issue | Why it matters for a passive FTSE 100 vehicle |

|---|---|

| Mandatory engagement expectations | The fund can't rely only on holding shares and tracking well |

| Physical ownership of securities | Voting and escalation duties attach to real holdings |

| National governance reforms | UK-specific standards may require more than global boilerplate stewardship policies |

Questions of corporate transparency failure become especially relevant here. If disclosure quality weakens at a major constituent, a passive owner cannot credibly say the issue is peripheral. The whole premise of the product is that the constituent is central.

A short explainer is useful before the final point.

Stewardship is where passive finance becomes active governance. If that function is weak, the market gets low-cost ownership but discounted accountability.

That is the dilemma in its cleanest form. The fund's mandate is passive. Its civic footprint is not.

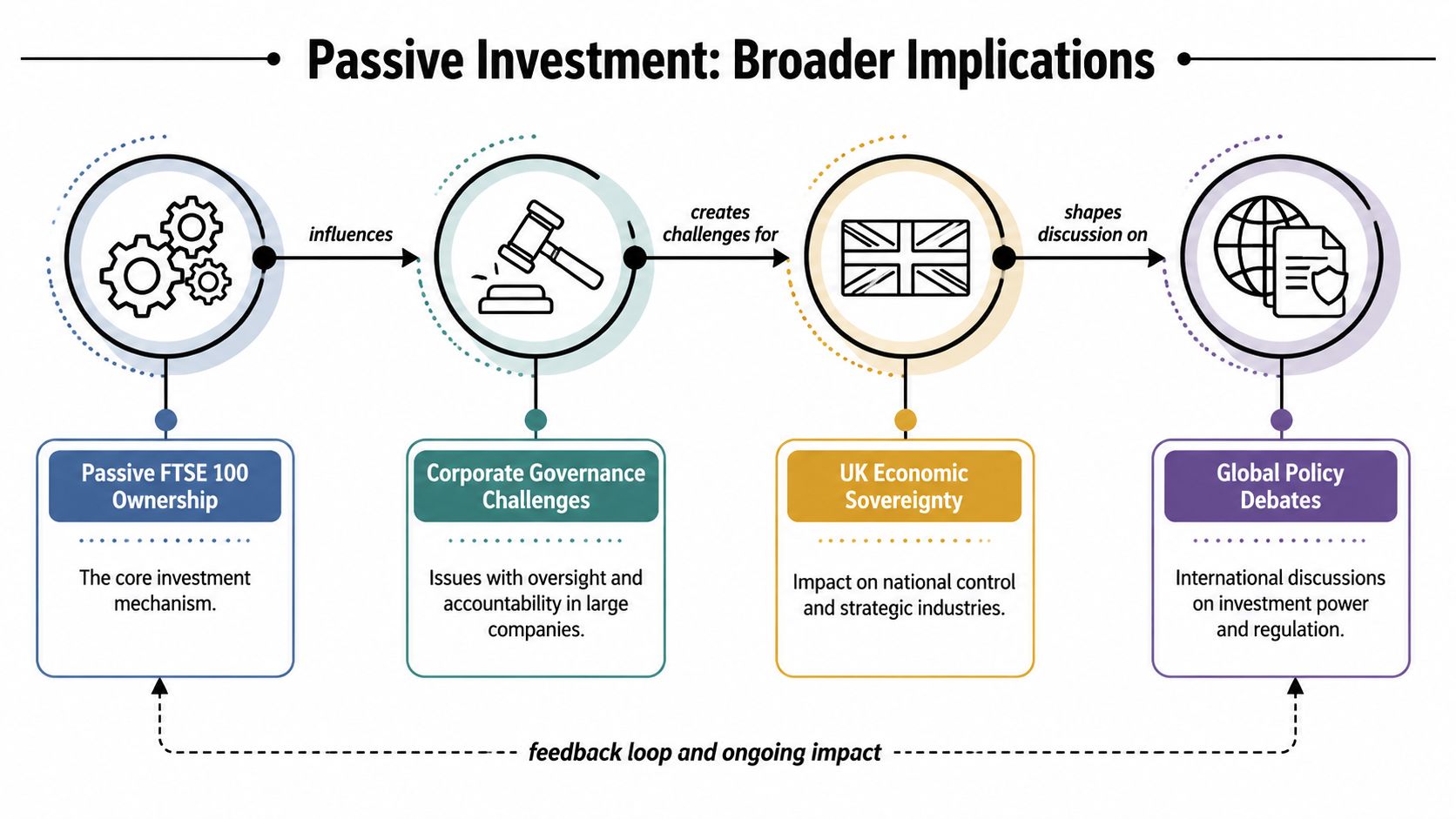

Implications for UK Economic Sovereignty and Global Policy

When a major index fund becomes a durable owner of strategic UK companies, the debate moves beyond stewardship technique. It becomes a question of economic sovereignty. Not sovereignty in the crude sense of nationality alone, but sovereignty in the sense of who exerts routine influence over the governance norms of nationally significant firms.

The Vanguard FTSE 100 sits inside that debate because it links UK corporate ownership to a broader global asset-management model. The fund is available through regulated structures that connect domestic equity exposure with cross-border investment channels. That's efficient. It also means the governance of British corporate champions can be shaped by policies developed within large international asset-management organisations whose stewardship frameworks are often designed for global consistency first.

Stewardship is no longer purely domestic

That creates a subtle mismatch. UK policymakers may tighten expectations around disclosure, transition planning or responsible ownership. But a global manager may still prefer a harmonised stewardship template applied across many markets. The result isn't open conflict. It is drift. National regulation becomes more demanding while the operational model of passive ownership remains built for scale.

This matters most in sectors with strategic weight. Where large listed companies influence energy resilience, pharmaceutical capacity, financial stability or consumer infrastructure, ownership practices affect more than shareholder returns. They affect the credibility of domestic governance regimes.

A country can retain formal control over its listing rules and still find that practical governance influence is exercised through globally standardised shareholder policies.

What G7 and G20 policymakers should focus on

The Vanguard FTSE 100 is one example of a wider policy class. Similar issues arise wherever passive vehicles hold central positions in nationally important markets. That's why the topic belongs in G7 and G20 discussions about non-bank financial institutions and market resilience.

A practical agenda would focus on four areas.

- Stewardship disclosure quality: asset managers should show how voting and engagement reflect local governance reforms, not only global house policies.

- Concentration mapping: regulators should pay closer attention to where benchmark concentration turns passive owners into system-level governance actors.

- Cross-border accountability: domicile, distribution and ownership chains should not obscure who is answerable when stewardship falls short.

- Public-policy alignment: governments need a clearer view of whether passive ownership models support or dilute national governance objectives.

The underlying insight is easy to miss because index funds look operational rather than political. In reality, they are both. A benchmark tracker that holds the corporate centre of a major economy is part of that economy's governing architecture whether anyone intended it or not.

Conclusion The Future of Indexing and Corporate Governance

The Vanguard FTSE 100 should no longer be analysed only as a low-intervention investment tool. It is a durable ownership mechanism embedded in the UK's most important listed companies. That status creates obligations that are bigger than tracking accuracy and broader than consumer choice.

The central policy issue is no longer whether passive investing is efficient. It plainly is. The issue is whether governance systems built around active scrutiny can function properly when a growing share of ownership is rules-based, centralised and designed for scale. If the answer is uncertain, then regulators need to stop treating index funds as neutral market plumbing.

Several outcomes are now plausible. Asset managers may move towards a more explicit passive-plus model in which stewardship is treated as a core product function rather than a compliance adjunct. Regulators may demand sharper disclosure on how passive funds respond to UK-specific governance reforms. Trustees and institutional allocators may begin to ask not only whether a fund tracks well, but whether it governs well.

That would be a healthy shift. The UK doesn't need less passive capital. It needs clearer expectations for what passive capital must do once it becomes a major owner of strategic firms. The future of indexing will be decided not just by costs and flows, but by whether large passive shareholders can prove that low-discretion investing is still compatible with high-accountability ownership.

Global Governance Media examines exactly these kinds of cross-border policy questions, where financial mechanics shape public outcomes. If you want more analysis on capital markets, stewardship, economic sovereignty and G7 and G20 governance debates, explore Global Governance Media.