By Elena Markham

Most commentary still treats corporate due diligence as an administrative exercise. That view is already obsolete. Under the UK's proposed Mandatory Human Rights and Environmental Due Diligence Act, individual directors who knowingly approve false or incomplete due diligence reports could face criminal liability, a point absent from 92% of existing advisory materials according to Ropes & Gray's analysis of the proposed framework.

That single fact changes the strategic meaning of due diligence. It shifts the issue from corporate housekeeping to board-level exposure, from sustainability reporting to evidential discipline, and from reputational management to personal accountability. For governments, it also signals a broader transition in regulatory design. Legislators are no longer satisfied with aspirational disclosures alone. They increasingly want decision trails, demonstrable controls, and named responsibility.

The practical implication is sharper than many executives realise. A weak due diligence process no longer fails only when a scandal becomes public. It fails much earlier, when a company cannot show how directors knew, what they reviewed, what they challenged, and why they signed off.

Table of Contents

- Beyond the Checklist Rethinking Due Diligence

- Defining Corporate Due Diligence for a Modern World

- Mapping the Global Regulatory Landscape

- The Core Components of an Effective Process

- Implementation Guidance for Corporate Leaders

- Due Diligence in Action Real World Case Studies

- Policy Recommendations and the Path Forward

Beyond the Checklist Rethinking Due Diligence

The standard corporate model still frames due diligence as a checklist completed near a transaction, supplier onboarding, or reporting deadline. That model is too narrow for the current legal environment. Modern corporate due diligence is better understood as an operating system for board judgement. It establishes whether a company can detect harm, test assertions, escalate concerns, and defend its decisions under scrutiny.

Why the old model fails

A checklist assumes stable risk. Corporate activity doesn't work that way. Supply chains shift, ownership structures change, political exposure evolves, and environmental or labour issues emerge in places far from head office. A static review can capture a moment. It can't govern an enterprise.

The more important problem is evidential. If directors approve an acquisition, market entry, financing relationship, or supplier arrangement, regulators and courts won't be interested only in whether a policy existed. They'll ask whether leaders had enough information, whether contradictions were investigated, and whether unresolved gaps were recorded.

Practical rule: Due diligence isn't strong because a company has a policy. It's strong because the organisation can prove how the policy shaped a real decision.

Due diligence as strategic infrastructure

Well-run firms use due diligence to influence pricing, contractual protections, escalation routes, and post-signing controls. That makes it a strategic function, not a support function. It can reshape whether a deal proceeds, whether a supplier remains approved, or whether additional monitoring is required before capital is deployed.

Director liability becomes more than a legal footnote when personal exposure enters the system. The board's incentives change immediately. Boards start asking different questions. Not “Have we completed the process?” but “Can we defend the assumptions behind the process?”

A robust system therefore creates two forms of value at once. It reduces the risk of legal failure, and it improves the quality of strategic decision-making. Those benefits are closely linked. The same process that identifies hidden labour, environmental, or integrity risks also improves how companies allocate capital and protect long-term enterprise value.

What directors should do differently

Board members should insist on three disciplines.

- Evidence over summary: Executive packs should include underlying assumptions, unresolved gaps, and documented challenge.

- Ownership over diffusion: Someone must be accountable for escalating material findings to senior decision-makers.

- Records over memory: Decisions need contemporaneous documentation, not retrospective rationalisation after an incident.

Companies that grasp this early will treat corporate due diligence as an institutional defence mechanism. Those that don't may discover that the true failure wasn't the original risk. It was the inability to show that leadership acted with care.

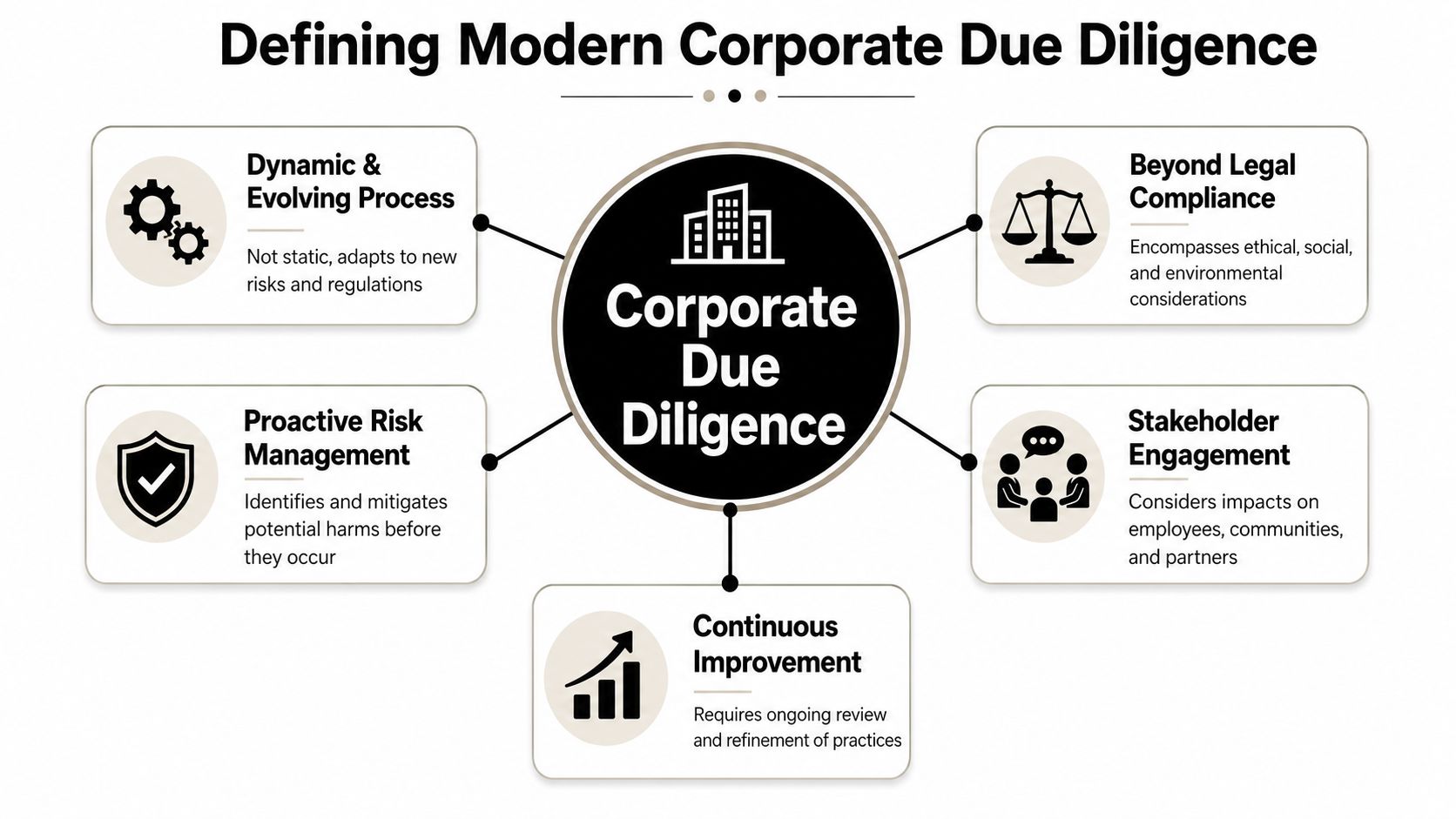

Defining Corporate Due Diligence for a Modern World

Corporate due diligence now extends far beyond financial verification, legal title, and basic counterparty checks. In modern practice, it is a continuous process through which a company identifies, assesses, prevents, mitigates, documents, and revisits risks linked to its operations, business relationships, and wider value chain.

A useful analogy is maritime navigation. Traditional diligence checked whether the ship was seaworthy before departure. Modern diligence is the radar, route correction system, weather feed, incident log, and captain's bridge communication combined. It doesn't operate once. It operates continuously.

What falls inside the modern definition

A contemporary due diligence system usually combines several layers of review rather than a single compliance test.

- Corporate structure: Firms need clarity on subsidiaries, shareholders, directors, and beneficial ownership.

- Relationship purpose: Teams should understand why the relationship exists and what commercial activity it is meant to support.

- Operational conditions: Labour practices, environmental controls, governance arrangements, and site-level realities matter.

- Decision evidence: Findings must be recorded in a way that supports later audit, challenge, and remediation.

This broader view matters in sectors where digital infrastructure, intangible assets, and complex ownership models intersect. For example, companies exploring RWA tokenization development face a governance challenge that is not purely technical. When real-world assets are structured, digitised, and linked to new financing models, the due diligence burden expands to include legal rights, asset provenance, counterparty risk, and documentation integrity.

Why compliance alone is too limited

A narrow legal reading misses how corporate harm manifests. A business may comply with a formal disclosure rule and still fail to understand its supplier incentives, weak grievance channels, or incomplete ownership data. That is why institutional failures often begin as information failures.

The governance consequences of opacity are visible well beyond a single transaction. Analysis of failure in corporate transparency shows why fragmented records and incomplete disclosure can distort accountability long before regulators intervene.

Good due diligence asks not only whether the company has received documents, but whether those documents are sufficient to support a decision.

The modern test

The strongest working definition is practical. Corporate due diligence is the disciplined process by which an organisation converts uncertain facts into defensible decisions. If that process can't adapt as conditions change, it isn't modern enough for today's regulatory environment.

Mapping the Global Regulatory Landscape

The global architecture for corporate due diligence is no longer a soft patchwork of voluntary expectations. It is becoming a layered system in which international norms shape regional directives and national laws harden those norms into enforceable duties. For multinational firms, the central challenge is not solely compliance with one regime. It is coherence across several.

From principles to enforceable obligations

At the top level, the UN Guiding Principles on Business and Human Rights and the OECD approach to responsible business conduct established the policy grammar. They normalised expectations around risk identification, prevention, mitigation, and remediation across operations and business relationships.

What has changed is enforcement logic. Legislators increasingly use these principles as foundations for mandatory obligations. The result is that a company may face one set of expectations from investors, another from procurement authorities, and a third from national regulators, all converging on similar operational demands.

In the UK, this convergence is especially visible in modern slavery, anti-money laundering, and emerging human rights frameworks. The UK Modern Slavery Act requires companies with sales over £36 million and any business in the UK to publish an annual statement on steps taken to ensure slavery and human trafficking are absent from their business and supply chain, with potential unlimited fines for failure to comply. That requirement is formally a disclosure duty, but in practice it pressures companies to build underlying due diligence systems capable of supporting the statement.

A comparison of major frameworks

| Framework | Scope | Legal Status | Key Requirement |

|---|---|---|---|

| UN Guiding Principles on Business and Human Rights | Corporate human rights impacts across operations and relationships | Soft law | Identify, prevent, mitigate, and account for impacts |

| OECD due diligence approach | Responsible business conduct across sectors and value chains | Soft law with strong policy influence | Risk-based due diligence integrated into management systems |

| UK Modern Slavery Act | Businesses operating in the UK meeting the sales threshold | Binding national law | Annual slavery and human trafficking statement |

| UK enhanced due diligence rules under anti-money laundering regulations | Higher-risk customers and transactions, including high-risk third country exposure | Binding national regulation | Additional verification, approval, and monitoring obligations |

| Proposed UK human rights and environmental due diligence framework | Corporate value chains with potential director exposure | Proposed legislation | More explicit board accountability for false or incomplete reporting |

The UK as a regulatory stress test

Recent anti-money laundering developments show how quickly risk-based expectations can tighten. According to Experian's review of UK enhanced due diligence requirements, the number of UK businesses linked to EU-defined high-risk third countries increased by 77% between 2021 and 2023. The same analysis notes that inconsistencies in earnings or net worth now trigger additional documentation requests, while the January 2023 amendment changed the treatment of UK politically exposed persons by requiring a proportionate, risk-based approach rather than blanket enhanced due diligence.

Due diligence becomes a data architecture problem. Firms need systems capable of tracking jurisdictional exposure, beneficial ownership, source of funds, and decision records across changing counterparties. The problem isn't only legal interpretation. It is operational retrieval.

For companies working across borders, adjacent regulatory domains also matter. Product, customs, and market-entry obligations increasingly interact with due diligence controls. A practical example is Consumer Packaging and Labelling Act compliance, where documentation discipline and market-specific verification can affect whether a product enters a jurisdiction smoothly or triggers regulatory friction.

The strategic conclusion

The regulatory environment doesn't require identical rules to produce a common effect. It only requires enough overlap to make poor internal coordination expensive. That is why firms should stop organising due diligence around legal silos and start organising it around enterprise-wide risk evidence. The same logic underpins wider debates on illicit finance in a digital age and the global enforcement gap, where fragmented oversight gives bad actors room to move faster than institutions.

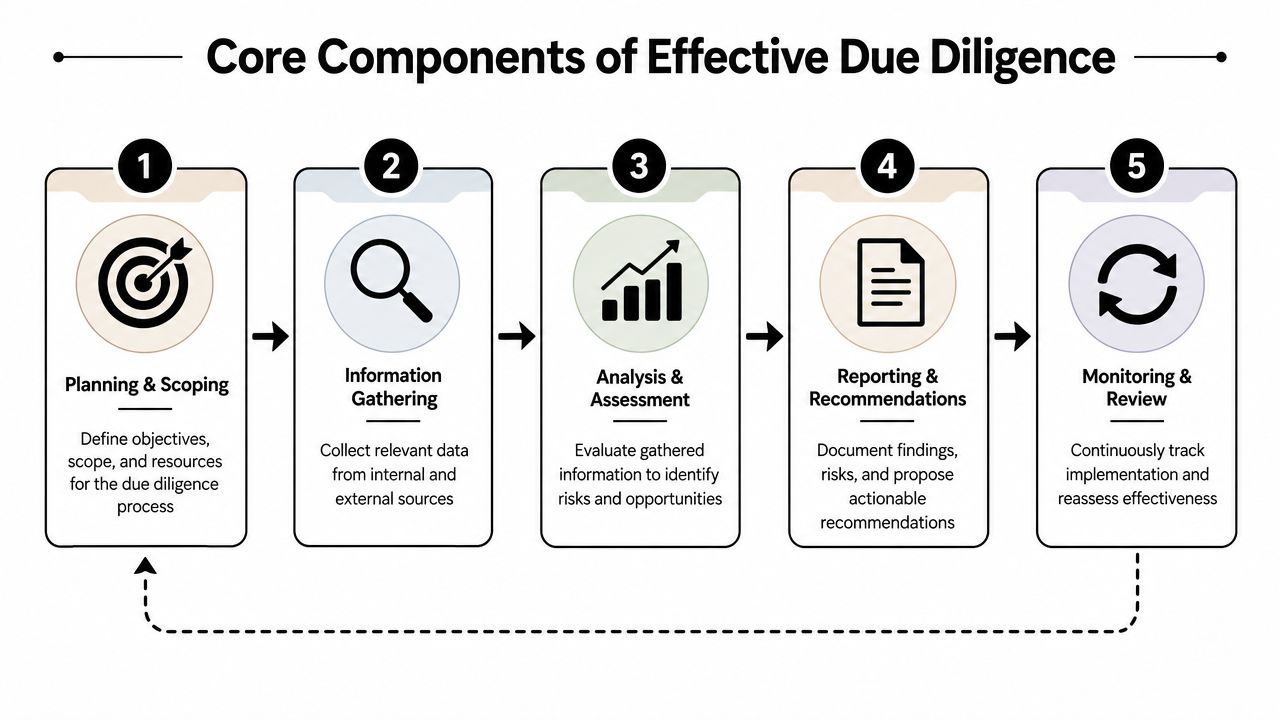

The Core Components of an Effective Process

An effective corporate due diligence process is cyclical. It begins with scoping, but it doesn't end with a report. The process must feed findings back into governance, contracts, monitoring, and remediation. When one stage fails, the whole system weakens.

Start with scope, not paperwork

Scoping determines whether the review is proportionate and decision-useful. A board paper, supplier onboarding exercise, investment committee review, or distributor appointment won't require identical testing. Teams need to define the business objective, identify the relevant risk domains, and decide which relationships, jurisdictions, and sites require deeper scrutiny.

For UK company transactions and corporate reviews, established practice described by Cooley Go's due diligence process guidance uses a structured data request covering corporate structure, litigation history, and finance, tax, and VAT status, often through a secure cloud data site. That same guidance describes a segmented process of Week 0–1 for scope and risk mapping, Week 1–4 for data stream execution and interim readouts into a single issues log, and Week 4–6 for converting findings into pricing, terms, or onboarding controls, followed by a 90-day review against assumptions.

Build a serious information base

Collection should include internal records, public data, transaction documents, and operational evidence. But effective teams don't merely assemble documents. They test consistency across them. A supplier questionnaire, payroll records, site visit notes, board resolutions, and ownership filings may all describe the same entity differently. Those inconsistencies are often where risk sits.

In larger reviews, technology can improve speed and consistency if it is used for triage rather than blind substitution. Tools for powerful AI document review can help teams compare clauses, flag anomalies, and extract structured information from large document sets, but human reviewers still need to decide what those anomalies mean in context.

Assess material risk in operational terms

This is the point where many programmes become superficial. They gather information yet fail to evaluate management quality, implementation capacity, and practical exposure. A stronger model requires an assessment of operating systems, not just policy statements.

A key specification in UK ESG-related diligence is especially useful here. British International Investment's due diligence toolkit requires collection and systematic review of a company's Environmental & Social Management System, its implementation status, and its Commitment, Capacity, and Track Record, with material gaps quantified into ESG Action Plans. That requirement is valuable because it turns broad ESG language into something operational and reviewable.

Board question: What would need to change before this counterparty, investment, or supplier relationship becomes acceptable?

Turn findings into decisions

An issues log has limited value unless it changes the decision. Findings should flow into transaction pricing, contractual warranties, approval conditions, remediation plans, or monitoring triggers. Some risks justify walking away. Others justify proceeding with conditions.

A disciplined process usually includes these outputs:

- Approval conditions: Specific actions that must occur before signing, onboarding, or funding.

- Control measures: Enhanced monitoring, escalation thresholds, audit rights, or reporting duties.

- Residual risk register: Clear documentation of what remains unresolved and who accepted it.

- Remediation pathway: A route for grievance handling, corrective action, and follow-up review.

Monitor after the formal review ends

The strongest due diligence systems assume that risk changes after approval. Ownership can shift. Local conditions can deteriorate. Internal controls can weaken when commercial pressure rises. Monitoring therefore needs triggers, assigned responsibility, and a cadence tied to actual risk.

That's why due diligence should be treated less like a gateway and more like a loop. The report matters. The feedback system matters more.

Implementation Guidance for Corporate Leaders

Leaders often ask the wrong implementation question. They ask which policy to adopt. The more useful question is which decisions must be supported by auditable evidence, and which team is responsible when the evidence is incomplete.

Put governance before templates

A due diligence programme should sit inside formal governance, not on the edge of it. Senior management oversight matters because difficult calls usually arise when commercial incentives pull against control requirements. If the due diligence team cannot escalate to a decision-maker with authority, the process will be bypassed at exactly the wrong moment.

Board committees and executive risk forums should require at least four things:

- Decision logs: Who approved what, on which date, and on what evidence.

- Escalation routes: A defined path when findings affect legal exposure, transaction value, or public commitments.

- Review discipline: Periodic testing of whether the process is functioning in practice.

- Business integration: Evidence that findings alter contract terms, supplier approval, or investment conditions where necessary.

Make record-keeping a control, not an archive

Record-keeping is often treated as a compliance afterthought. In fact, it is one of the most important controls in the system. UK corporate due diligence standards require a five-year retention period for Customer Due Diligence documents and supporting records so firms can reconstruct relevant transactions and demonstrate anti-money laundering compliance. The same guidance emphasises identity verification through reliable independent sources, identification of beneficial owners, understanding the nature of the relationship, ongoing monitoring, scope notes, screening hits, residual-risk registers, and clear recording of decision-making dates and times.

That requirement should influence system design. Companies need searchable repositories, version control, naming conventions, approval trails, and retention policies that match legal duties. A missing record can undermine an otherwise sound judgement because the institution can't prove what it knew.

Records are not evidence simply because they exist. They become evidence when they are organised, attributable, and connected to a decision.

A practical benchmark for compliance teams is whether they can retrieve the full file quickly enough to explain the decision to an internal investigator, external auditor, regulator, or court.

Use technology with discipline

Technology should support consistency, retrieval, and monitoring. It should not replace accountability. Supply chain mapping platforms, sanctions screening tools, data rooms, workflow systems, and dashboard reporting can all improve performance if their outputs are reviewed by accountable staff.

For teams considering more mature compliance design, work on using data to improve compliance offers a useful policy lens. The central lesson is that data only improves governance when institutions define decision rights, data quality standards, and escalation rules in advance.

The operational challenge is easier to grasp in practice, and this briefing offers a useful visual overview:

Build a defensible programme

A defensible programme usually includes a grievance route, periodic reassessment, staff training, and explicit board visibility over the highest-risk relationships. It also requires willingness to delay approval when information is poor.

That is where leadership culture becomes decisive. A company that prizes speed above traceability will struggle to run credible corporate due diligence. A company that links evidence to authority can make faster decisions over time because the decision rules are already clear.

Due Diligence in Action Real World Case Studies

The phrase “real world case studies” often implies dramatic scandals and polished success stories. In practice, the most useful cases are analytical contrasts. One reveals how failure accumulates through weak controls. The other shows how disciplined process creates room for better decisions.

Case one when disclosure outruns evidence

Consider a UK-based multinational with complex sourcing relationships and a polished annual modern slavery statement. The company meets the formal publication requirement, but its internal system is fragmented. Procurement holds supplier questionnaires. Legal holds contract templates. Sustainability holds engagement records. Regional teams hold site information. No one owns a unified risk picture.

A labour rights allegation then emerges in a lower-tier supplier. The problem is not just the allegation itself. The company cannot show how the supplier was risk-rated, who reviewed the escalation, whether management challenged inconsistencies, or what evidence supported the public statement. At that point, the exposure multiplies. Regulatory, legal, investor, and reputational questions all converge on the same issue: the institution cannot reconstruct its own judgement.

The lesson is straightforward. Disclosure without auditable underlying diligence is unstable. It creates a visible commitment without a reliable evidential spine.

Case two when process shapes strategy

Now consider an investor or large corporate acquirer using a more disciplined model. Before approval, the team builds a single issues log, tests ownership and control, reviews operating systems, and translates unresolved concerns into conditions precedent, pricing adjustments, and post-signing review commitments. Site-level concerns are not treated as footnotes. They are linked directly to contractual protection and management action.

This approach doesn't eliminate risk. It changes the organisation's relationship to risk. Leadership can decide knowingly, with explicit acceptance of residual issues and clear plans for mitigation. That often produces a better commercial result because the company knows where to insist on stronger warranties, where to stage implementation, and where to walk away.

A high-quality due diligence system doesn't promise perfect foresight. It produces better institutional memory, sharper escalation, and more credible decisions.

What these cases show

The contrast is not between bad companies and good companies. It is between weak information architecture and strong information architecture. One organisation publishes commitments it cannot defend. The other uses due diligence to shape commercial terms, governance design, and operational follow-up.

That is why corporate due diligence should be judged less by the volume of forms completed and more by the quality of decisions it enables.

Policy Recommendations and the Path Forward

Governments now face a design challenge. If they multiply due diligence obligations without improving coherence, they will increase paperwork without improving prevention. If they align legal expectations with practical implementation standards, they can raise performance across markets.

What governments should prioritise

First, policymakers should harmonise core concepts across regimes. Terms such as “value chain”, “appropriate measures”, “senior management approval”, and “effective monitoring” shouldn't vary so widely that firms spend more time interpreting language than managing risk. A common vocabulary would reduce friction for responsible companies and sharpen enforcement against negligent ones.

Second, governments should support implementation capacity, especially for firms with fewer internal resources. New legal duties often assume document systems, legal teams, site audit capacity, and data infrastructure that many organisations don't yet have. Capacity-building matters if states want compliance to be real rather than performative.

Third, enforcement should focus on decision quality, not disclosure volume. A smart regulator asks whether the company identified material risk, escalated it properly, documented judgement, and followed through. That approach discourages boilerplate and rewards actual diligence.

What multilateral institutions can do

Multilateral forums can help in three ways.

- Set interoperable principles: G7, G20, OECD, and UN processes can narrow divergence in implementation logic.

- Support technical guidance: Governments and firms need practical templates for records, escalation protocols, and remediation design.

- Promote supervisory cooperation: Cross-border business requires cross-border enforcement dialogue, especially where supply chains and finance intersect.

A particularly useful policy direction is the combination of mandatory obligations with practical safe harbours for good-faith compliance efforts. Firms should not be rewarded for superficial reporting. Equally, they should not be punished for identifying risk honestly and acting to mitigate it. Regulation works best when it changes incentives towards earlier detection and better governance.

The next phase of corporate due diligence

The next phase will be defined by integration. Human rights, environmental risk, anti-money laundering controls, labour compliance, and board accountability are no longer separate conversations. They increasingly rely on the same institutional capabilities: traceable records, clear ownership, timely escalation, and documented judgement.

For corporations, that means due diligence should move closer to the centre of strategy. For governments, it means regulatory architecture should reward evidence, not formality. For multilateral institutions, it means pushing for a common operating logic that turns fragmented compliance into effective prevention.

Corporate due diligence began as a risk review. It is becoming a governance test.

For readers tracking how governance standards, regulation, and board accountability are evolving across the G7, G20, and multilateral system, Global Governance Media offers authoritative analysis that connects policy design to practical implementation. Follow its coverage for sharper insight into the regulatory shifts shaping corporate responsibility, enforcement, and international economic governance.