By Dr Eleanor Markham

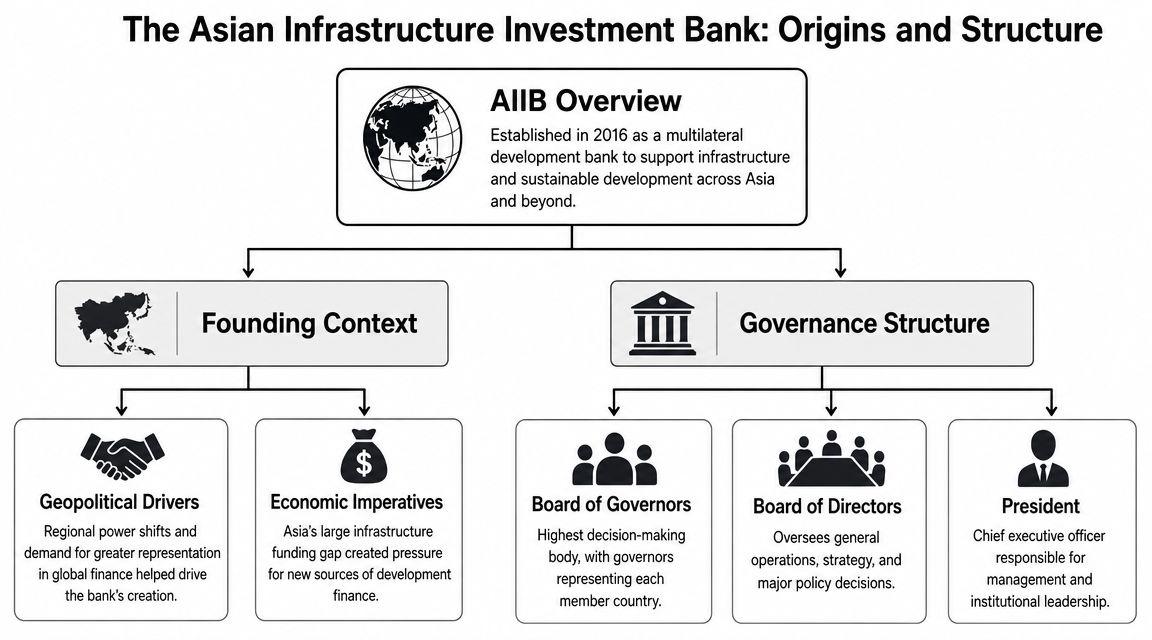

From a standing start in 2016, the Asian Infrastructure Investment Bank has become a lender that G20 finance ministers cannot treat as symbolic. AIIB began operations on 16 January 2016 with 57 founding signatories. It now presents itself as a global institution with broad membership, a substantial capital base, and top-tier credit ratings. Those features matter because they give the bank staying power in sovereign finance and credibility with borrowers, co-financiers, and capital markets.

The policy question has therefore shifted. For G20 governments, the issue is less whether AIIB should be read only through a China lens and more whether participation still offers practical influence over standards, project selection, and institutional direction. That question is especially sharp for G7 members such as the UK, whose membership can be interpreted in three ways at once: as a channel for shaping rules from within, as a diplomatic hedge in a more fragmented multilateral system, or as a reputational exposure if governance and political expectations diverge.

One useful comparator is broader balance-sheet scale across international finance. Readers tracking where AIIB fits relative to much larger banking institutions may find Visbanking's 2025 bank asset rankings for financial institutions helpful as context for how specialised development banks differ from commercial giants.

That distinction has strategic consequences. AIIB is not trying to replicate the World Bank's breadth across social sectors, governance reform, and poverty programming. Nor is it competing with private banks on short-horizon commercial lending. Its role is narrower and more consequential than either description suggests: infrastructure finance, often through co-financing, in a sector where project standards, procurement norms, climate priorities, and geopolitical access all intersect.

For the UK and other non-regional members, that makes AIIB a test case for twenty-first century multilateralism. If these members remain engaged, they may retain some capacity to shape an institution that sits between established MDB practice and a more contested order. If they disengage, they risk confirming a result they say they want to avoid: a large, credible bank in which advanced democracies have presence on paper but diminishing influence in practice.

Table of Contents

- The AIIB's Ascent in Global Finance

- Understanding AIIB's Founding and Governance

- Capital, Mandate, and Financial Instruments

- Mapping the AIIB's Investment Portfolio

- AIIB's Role Among MDBs and G20 Priorities

- Analysing the Critiques and Risks Facing the AIIB

- Policy Recommendations for Engaging with the AIIB

The AIIB's Ascent in Global Finance

More than a decade after its launch, the Asian Infrastructure Investment Bank is no longer a provisional entrant in multilateral finance. It is a standing institution that borrowers, co-financiers, and capital market participants now have to account for. That shift matters because institutional permanence changes behaviour. Governments submit projects differently, peer MDBs adjust their coordination strategies, and shareholders face a harder question than whether the bank should exist. They have to decide how, and how far, they intend to shape it.

The policy significance of AIIB lies in the effect it has had on the wider system. It has added another source of infrastructure finance, but its larger contribution is competitive pressure. An institution built around infrastructure speed, project preparation, and cross-border connectivity has forced established lenders to defend their own relevance in areas where demand remains high and fiscal space is tight. For a broader comparison of how global finance is fragmenting across institutions and strategic blocs, see this analysis of international finance drifting into separate spheres.

Strategic relevance for advanced economies

For G7 members, especially the UK, the central issue is no longer whether AIIB reflected Chinese diplomatic ambition at birth. That point is historically important, but strategically incomplete. The sharper question is whether membership offers a usable channel of influence inside a multilateral institution that still carries political sensitivities, or whether continued participation creates more reputational exposure than policy return.

The UK is the clearest test case. Early participation gave London access, board representation, and a basis for shaping standards from within. If that access is not used to influence lending discipline, governance practice, and climate credibility, membership starts to look less like statecraft and more like symbolic hedging. For ministers, the lesson is straightforward. Presence without strategy rarely produces influence.

This distinction is often missed in debates that reduce AIIB to a proxy for China-West competition. In practice, advanced economy shareholders confront a three-part calculation. They can treat AIIB as an influence channel, a diplomatic hedge against further fragmentation in the multilateral system, or a reputational risk if governance concerns intensify. Those categories are not mutually exclusive. The balance between them will shift with the bank's project choices, transparency record, and relationship with other MDBs.

A bank that changed the policy conversation

AIIB's rise has also changed what counts as mainstream multilateral finance. Infrastructure is now discussed less as a narrow development subsector and more as a strategic instrument tied to supply chain resilience, energy security, and industrial competitiveness. That change has been reinforced by the bank's focus on connectivity and by the fact that public balance sheets alone cannot meet long-horizon investment needs.

Capital market credibility is part of that story. High-grade multilateral borrowers occupy a distinct position in global finance because they can intermediate policy priorities through low-cost funding and long maturities. Readers looking for scale comparisons across the financial system can consult the 2025 bank asset rankings for financial institutions, but the more relevant point for policymakers is qualitative. MDB balance sheets matter less because they rival large commercial banks in size than because they can direct capital toward public goods that private finance prices cautiously or avoids.

For the G20, AIIB's ascent is therefore a test of institutional adaptation. If established shareholders use membership actively, the bank can remain a venue where standards, co-financing discipline, and strategic infrastructure priorities are contested and improved. If they disengage while retaining formal membership, they increase the chance that AIIB becomes something narrower: a bank that is multilateral in form, but shaped by a smaller set of governments in practice.

Understanding AIIB's Founding and Governance

AIIB was born out of dissatisfaction with representation and speed in the existing multilateral system, but that shorthand misses the deeper point. The institution also responded to a practical financing need: large-scale infrastructure requires patient capital, technical structuring, and institutions able to work across borders.

Why the institution was created

The familiar story is that emerging economies wanted greater voice. That's true, but incomplete. The more interesting reading is that AIIB was designed to join governance ambition to a narrower operating focus. By concentrating on infrastructure rather than the full spread of development policy, the bank could define a clearer institutional identity than broader MDBs often manage.

That design choice matters for ministers because focused institutions can move faster, attract specialist staff, and build a recognisable policy franchise. They also create clearer political tests. If the mission is infrastructure, then project quality, connectivity logic, climate integrity, and co-financing discipline become the main measures of success.

AIIB's importance lies partly in what it chose not to be. It didn't try to replicate every function of older development institutions.

How formal power is organised

The governance debate usually centres on influence. In practice, influence in a multilateral bank comes through several channels at once: shareholding, board processes, management access, coalition-building among members, and the credibility of technical interventions.

AIIB's structure includes a Board of Governors, a Board of Directors, and a President. For policymakers, the practical takeaway is that the institution blends formal multilateral procedures with an operational model that has often been described as leaner than the Bretton Woods tradition. That can raise efficiency, but it also increases the importance of scrutiny because fewer layers can mean fewer veto points.

A simple way to think about the power map is below:

| Governance actor | Practical role |

|---|---|

| Board of Governors | Sets top-level direction and represents member states at the highest level |

| Board of Directors | Oversees operations and policy choices |

| President | Leads management and shapes the bank's day-to-day strategic execution |

The UK and other G7 members should read this not as an abstract chart but as an operating environment. In a governance system where shareholding matters, passive membership rarely produces results. Influence has to be organised, sustained, and linked to identifiable outcomes such as procurement standards, climate metrics, portfolio transparency, or co-financing rules.

There's also a second-order implication. Because AIIB sits outside the historical architecture of Bretton Woods while still borrowing many multilateral features, members can't rely on inherited habits. They need an explicit strategy for engagement. That's especially true for non-regional members that want to shape norms without being seen as trying to re-fight the bank's creation.

Capital, Mandate, and Financial Instruments

The fastest way to misunderstand AIIB is to look only at its headline capital number. The strategic question isn't just how large the bank is on paper. It's how that capital structure supports lending, market borrowing, and policy credibility.

According to AIIB's investor presentation, the bank is a USD 100 billion multilateral development bank with 20% assigned paid-in capital, and its FY26 funding programme is up to USD 11 billion. That tells ministers something important: AIIB's lending capacity rests on a structure in which a relatively limited paid-in base is amplified by the wider capital framework and access to capital markets.

Why the balance sheet matters

That architecture is common in MDB logic, but AIIB's case is strategically notable because it shows how a newer institution can earn market confidence without decades of legacy operations behind it. The ability to fund at scale depends on capital adequacy, liquidity discipline, and confidence that shareholders stand behind the institution when needed.

A recent credit opinion adds nuance. It notes that AIIB holds AAA ratings and preferred creditor status, while one estimate placed its weighted average borrower rating at “ba3” at end-2024, as outlined in this credit opinion. In plain terms, AIIB's strength doesn't come from lending only to top-rated borrowers. It comes from conservative financial management and selective risk-taking.

Practical rule: When an MDB keeps top ratings while lending into weaker credit environments, policymakers should study the institution's risk controls at least as closely as its headline project list.

That distinction matters for G20 finance ministries because many are trying to stretch public balance sheets further without eroding sovereign credibility. AIIB offers a live example of how institutional design can create lending headroom, though not without governance demands.

What the mandate means in practice

AIIB is often associated with the phrase “lean, clean, and green”. The slogan is useful, but ministers should interrogate how slogans translate into incentives. “Lean” affects staffing and decision processes. “Clean” points to governance and integrity standards. “Green” speaks to project selection and the bank's long-run legitimacy in a climate-constrained world.

The more technical issue is instrument choice. A bank's mandate only becomes real when it is embedded in financing tools and approval standards. AIIB's operating relevance comes from its ability to deploy sovereign-backed finance, non-sovereign financing, equity participation, and guarantees in ways that can draw in partners rather than displace them.

For officials considering co-financing or blended structures, the larger lesson is that institutional flexibility matters as much as headline capital. Such flexibility makes debates about private mobilisation concrete. The policy challenge isn't merely finding more money. It's matching instrument design to project risk, procurement realities, and political acceptability. That's also why debates on innovative instruments for infrastructure progress mobilising the private sector have become more central across the multilateral system.

A bank with AIIB's profile can therefore matter beyond the volume it lends directly. It can influence which projects become financeable, which standards are normalised, and which partnerships become routine.

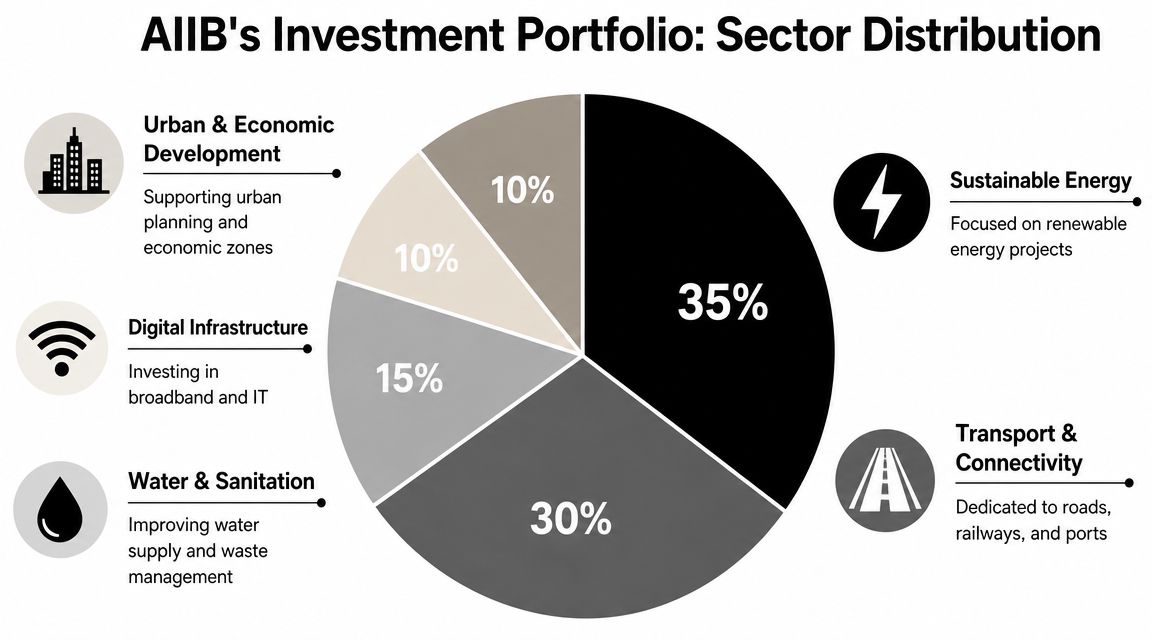

Mapping the AIIB's Investment Portfolio

In its first year of operations, AIIB committed USD 1.73 billion across nine projects, and six were co-financed with other multilateral lenders, according to the Asian Infrastructure Investment Bank entry on Wikipedia. That ratio matters. It suggests the bank's early portfolio was built less around institutional separation than around credibility transfer from established partners.

From cautious co-financing to portfolio definition

For a new MDB, co-financing is not only a funding arrangement. It is a governance signal. Joint projects lower operational risk, expose staff to established due diligence systems, and reassure shareholders that project selection is being tested against recognised standards rather than political ambition alone.

That starting point is especially relevant for G7 members that joined AIIB, including the UK. The strategic question was never merely whether the bank would fund infrastructure in Asia. It was whether membership would give non-regional shareholders a practical channel to shape standards from within, or whether their presence would mainly confer legitimacy on decisions shaped elsewhere.

The portfolio now offers a clearer basis for that judgment. By 2024, AIIB reported that cross-border connectivity projects accounted for one-third of its total financing, with USD 3.8 billion directed across 18 transport projects, as the same source notes. This concentration gives the bank a distinct profile within the MDB system because connectivity finance affects trade routes, customs efficiency, logistics resilience, and the political economy of regional integration.

Why connectivity matters more than sector labels suggest

Transport and corridor finance should be read as geoeconomic infrastructure. A road, port, rail connection, or energy interconnector can alter commercial dependence patterns for decades. It can also redistribute bargaining power among neighbouring states, especially where supply chains, transit revenues, or strategic chokepoints are involved.

For finance ministers, that has three consequences:

- For borrowing governments: infrastructure choices can harden external economic relationships and reduce room to rebalance later.

- For shareholders such as the UK and other G7 members: portfolio composition is a more reliable indicator of AIIB's strategic direction than institutional messaging alone.

- For co-financing partners: shared projects can spread risk across institutions, but they also create shared exposure if procurement, debt sustainability, or political alignment later become contested.

This is also where reputational risk becomes concrete rather than abstract. If G7 members remain shareholders while the bank's connectivity portfolio becomes associated with disputed corridor politics, membership may look less like influence and more like passive endorsement. That is why due diligence should extend beyond project bankability to include governance, supply-chain exposure, and partner-country political risk, including lessons drawn from cross-border risk strategies for Israeli firms.

The broader conclusion is straightforward. AIIB's portfolio should be assessed as an institutional strategy expressed through asset selection. For China, that can support regional economic centrality. For the UK and other G7 members, it raises a harder policy test. Membership has value only if it changes decisions, standards, or disclosure in ways visible in the portfolio itself.

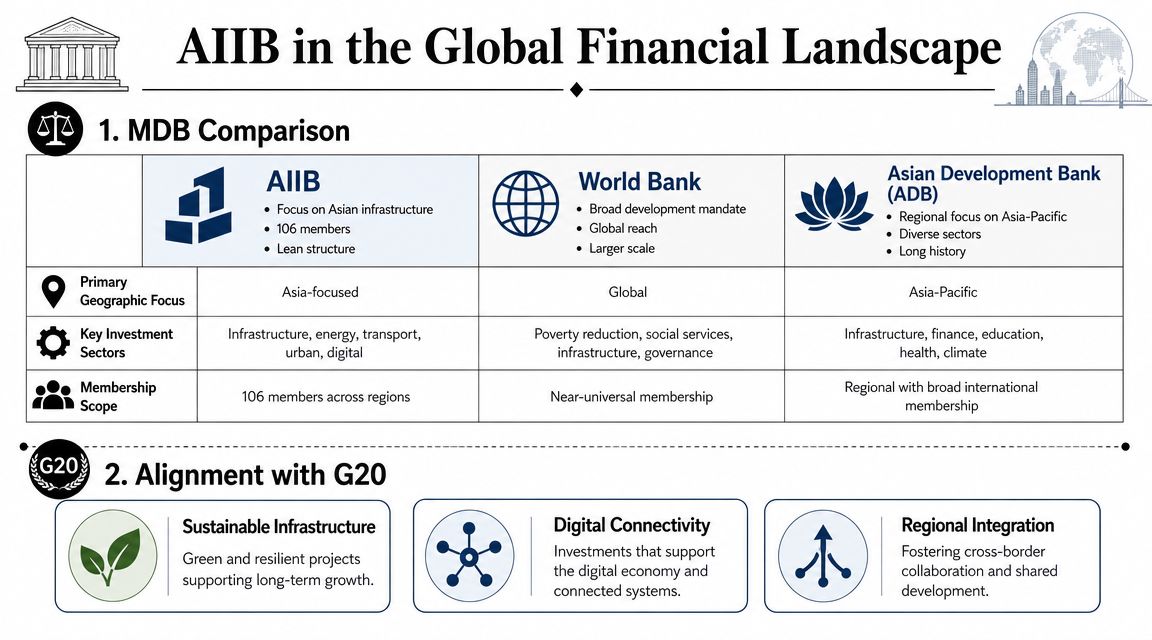

AIIB's Role Among MDBs and G20 Priorities

AIIB occupies a hybrid position in the MDB environment. It collaborates enough to be systemically relevant, yet it is distinct enough to alter bargaining dynamics among existing institutions.

A collaborator first, but not only that

The strongest evidence from AIIB's early years points toward collaboration. Its first-year pattern of joint projects with other MDBs showed that the bank sought acceptance through shared transactions rather than immediate institutional confrontation. But collaboration shouldn't be mistaken for subordination.

Once a new MDB builds a record, market access, and internal process confidence, cooperation can evolve into selective competition. That competition needn't be ideological. It can be procedural. Which institution moves faster? Which one shapes project terms? Which one becomes the default partner for a government seeking corridor finance or a politically salient transport scheme?

A brief comparison is useful:

| Institution | Distinctive profile |

|---|---|

| AIIB | Infrastructure-centred, newer, and designed to operate with a leaner institutional model |

| World Bank | Broader development mandate with global reach and wider policy coverage |

| Asian Development Bank | Regional depth in Asia-Pacific with long-established operational experience |

Where AIIB intersects with G20 agendas

For the G20, AIIB's relevance is less about institutional branding than agenda overlap. Several issues now sit at the centre of ministerial discussions across advanced and emerging economies: sustainable infrastructure, digital connectivity, resilience, and regional integration. AIIB works directly in that zone.

That's why the right question isn't whether AIIB duplicates existing MDBs. The better question is whether it adds execution capacity and strategic optionality in areas where demand already exceeds what older institutions can easily deliver.

Readers following summit-level performance may find it useful to compare this against broader G20 performance on infrastructure investment. The gap between collective commitments and actual financing pathways remains one of the defining weaknesses of multilateral economic governance.

The AIIB test for the G20 is simple. Can ministers treat new MDBs as instruments to solve shared problems, while still enforcing standards that protect the legitimacy of the system as a whole?

That balancing act is where AIIB's future role will be decided. If it remains primarily a co-financing partner, it will strengthen the existing system. If it uses its growing autonomy to shape norms on its own terms, then G20 governments will need a more deliberate strategy.

Analysing the Critiques and Risks Facing the AIIB

Serious analysis of AIIB starts where promotional narratives end. The institution faces three persistent critiques: that it serves geopolitical purposes linked to China, that governance risks may outpace oversight, and that its climate positioning may outrun its actual portfolio.

The geopolitical critique is too narrow

The geopolitical critique isn't wrong. It's incomplete. Yes, AIIB emerged in a context shaped by Chinese power and institutional ambition. But treating that as the whole story blinds policymakers to the harder issue: institutions can begin with one political interpretation and still evolve into arenas where multiple states pursue influence simultaneously.

That's particularly relevant because recent analysis has highlighted a growing question for the UK and other non-regional members. Is membership an influence channel, a diplomatic hedge, or a reputational risk as AIIB expands activity beyond Asia and develops greater institutional autonomy? AIIB's own framing allows collaboration with members worldwide, and that makes the strategic calculus more complicated than a simple inside-versus-outside debate.

Risk analysis in this context has to move beyond labels. It needs to ask how exposure is managed across jurisdiction, counterpart, and institutional reputation. Readers interested in practical approaches to managing multi-market uncertainty may find this guide to cross-border risk strategies for Israeli firms useful as a private-sector parallel.

Climate credibility is now a testable question

The sharper challenge now concerns climate and nature credibility. AIIB promotes sustainable infrastructure and frames co-benefits in sector strategies, including its health strategy publication. But a 2025 independent analysis specifically examined whether the bank's portfolio aligns with Paris temperature goals, raising a more difficult question than generic ESG branding allows.

That question matters because climate legitimacy for MDBs is no longer rhetorical. Borrowers, shareholders, and civil society increasingly want to know whether “green” language changes actual project selection, or repackages conventional infrastructure finance in more acceptable terms.

A short briefing video is useful context for how these debates have entered public policy discussion.

AIIB's climate test isn't whether it uses the right vocabulary. It's whether its portfolio, over time, looks materially different because of that vocabulary.

There is a broader governance implication as well. If AIIB's autonomy is increasing, then external confidence will depend less on founding narratives and more on disclosure quality, safeguard enforcement, and the consistency between public strategy and lending behaviour. That is where reputational risk becomes operational risk.

Policy Recommendations for Engaging with the AIIB

For G7 and G20 governments, the central mistake would be to treat AIIB as settled. It isn't. The institution is established enough to matter and still fluid enough to shape. That combination creates a narrow but important window for strategic engagement.

For UK policymakers in particular, the core issue goes beyond China geopolitics. As AIIB's activities broaden and its institutional autonomy grows, membership can function as an influence channel, a diplomatic hedge, or a reputational liability, as reflected in AIIB's about page and the associated strategic debate. The right answer depends on whether membership is used actively.

For G7 and G20 governments

Governments should shift from symbolic positioning to operational objectives. That means defining a small number of outcomes they want from engagement, then using board participation, coalition-building, and co-financing policy to pursue them.

A disciplined approach would include:

- Set priority asks: Focus on a limited agenda such as climate integrity, transparency, cross-border project standards, or procurement practice. Broad rhetorical pressure rarely changes institutions.

- Use membership collectively: Non-regional members often have more influence when they coordinate rather than intervene alone.

- Judge the bank by portfolio behaviour: Speeches matter less than project selection patterns, co-financing choices, and implementation discipline.

For partner institutions and outside stakeholders

Other MDBs and IFIs should treat AIIB neither as a rival to isolate nor as a partner to romanticise. The practical task is to identify where cooperation adds value and where discipline is needed to prevent standards drift.

Civil society and private-sector stakeholders should do the same. Scrutiny is most effective when it is specific. Which sectors are expanding? Which safeguards are applied consistently? Where do co-benefits appear credible, and where do they look overstated? Those questions are more powerful than generalised accusations.

Effective engagement with AIIB requires a portfolio lens, not a slogan lens.

The wider strategic conclusion is straightforward. AIIB now sits inside the working machinery of multilateral finance. The question for finance ministers isn't whether it exists as an alternative. It's whether they will shape its trajectory while they still can.

Global Governance Media tracks the institutions, negotiations, and policy choices shaping the G7 and G20 agenda. If you want sharper analysis on multilateral finance, development banks, climate diplomacy, and the future of economic governance, follow Global Governance Media for ongoing briefings and expert commentary.