By Eleanor Whitmore, Senior Policy Analyst

The most revealing fact about Korea Electric Power Corporation isn't that it's large. It's that one company can simultaneously represent energy security, industrial policy, decarbonisation risk, regulated-price politics, and sovereign balance-sheet logic in a single institutional form. KEPCO was founded on 1 July 1961, and by the end of 2023 it had 83,235 MW of installed generating capacity across 794 units, operated 35,596 circuit kilometres of transmission lines, generated KRW 88.22 trillion in revenue, and employed 23,138 people, according to KEPCO's corporate profile.

That scale matters beyond South Korea. For G20 ministers, KEPCO is a compact case study in the hardest public-policy problem in energy today: how to preserve reliable and affordable electricity while shifting an incumbent system away from carbon-intensive generation, all without breaking the utility expected to carry out the transition. The same tension runs through debates on grids, nuclear power, industrial competitiveness, and transition finance across advanced and emerging economies.

The lesson is uncomfortable. A strong state utility can accelerate national strategy, but it can also trap a country in slower market adaptation if governance, tariffs, and grid incentives aren't aligned. That is why KEPCO deserves to be read not as a domestic corporate story, but as a multilateral governance problem. For readers tracking how summit diplomacy is increasingly shaped by power-system constraints, the broader frame is already visible in this analysis of G7 and G20 energy governance.

Table of Contents

- Introduction Why KEPCO Matters to Global Governance

- The Anatomy of a State-Owned Energy Colossus

- A Carbon-Intensive Portfolio in Transition

- Navigating Financial and Regulatory Headwinds

- The Monopoly Bottleneck in Korea's Renewable Transition

- KEPCO's Global Ambitions and Geopolitical Role

- Conclusion Policy Lessons for Multilateral Energy Governance

Introduction Why KEPCO Matters to Global Governance

KEPCO matters because it sits at the point where sovereignty and infrastructure meet. Governments often talk as if climate policy, industrial policy, and energy security are separate agendas. In practice, utilities like KEPCO are where those agendas collide.

South Korea's power system gives that collision unusual clarity. A utility with system-wide reach can support long-horizon planning and keep reliability at the centre of decision-making. But the same concentration of authority means that when incentives are misaligned, the consequences are also system-wide. A pricing error doesn't stay in retail tariffs. A grid bottleneck doesn't remain a local permitting issue. A delayed transition doesn't remain a corporate emissions problem.

Why G20 policymakers should read KEPCO closely

Three policy questions converge in the KEPCO case:

- Can states protect affordability without undermining investment? KEPCO shows how consumer protection can weaken the very institution expected to build new infrastructure.

- Can monopoly coordination speed up decarbonisation? It can, but only if grid access, procurement rules, and capital allocation point in the same direction.

- Can transition finance work when incumbent fleets remain carbon-intensive? KEPCO demonstrates that investment-grade credibility and fossil exposure can coexist for longer than many policy narratives assume.

Practical rule: If a government wants a utility to deliver energy security and decarbonisation at the same time, it must align tariffs, grid governance, and capital access. Fixing only one of those levers won't be enough.

That is why KEPCO is a useful G20 reference point. It condenses the broader challenge facing many major economies. The next decade won't be defined only by who builds more clean generation. It will be shaped by who can reform institutions fast enough to let cleaner power move through the system.

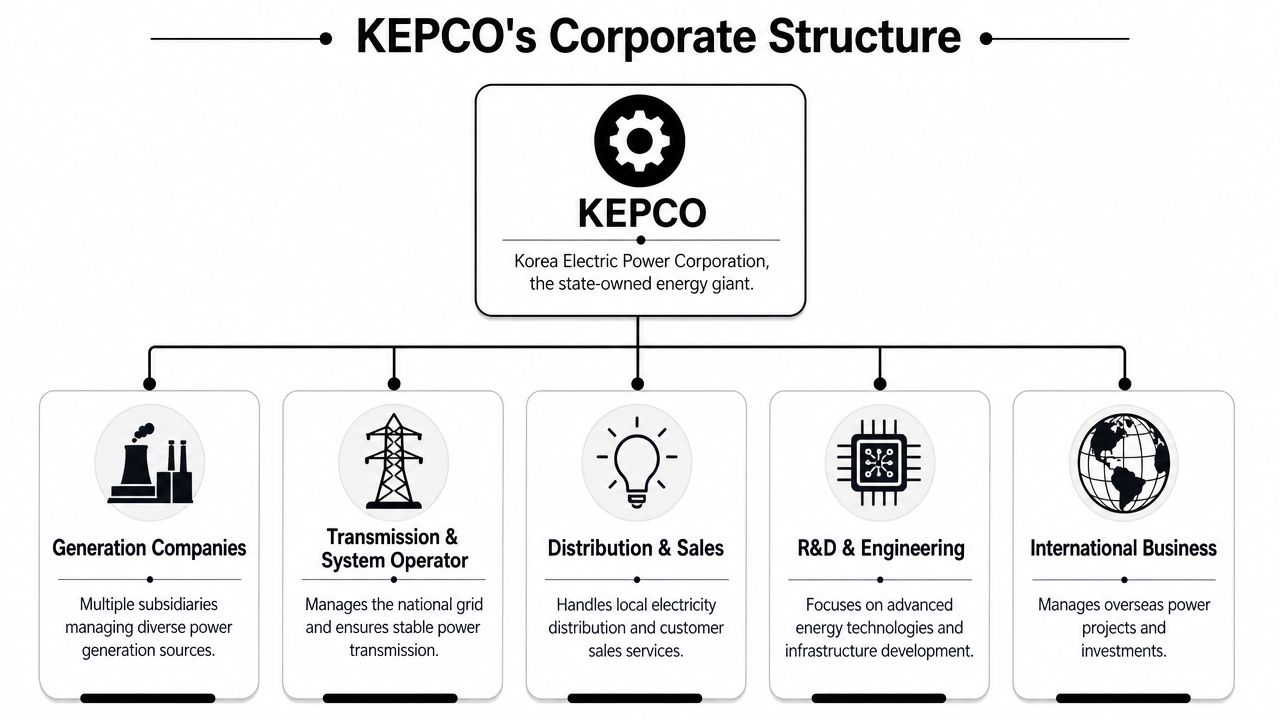

The Anatomy of a State-Owned Energy Colossus

KEPCO is the kind of institution that can determine whether a country's energy strategy succeeds or stalls.

Scale is policy power

As noted earlier, KEPCO's footprint spans generation, transmission, and a workforce large enough to give the company operational presence across the national power system. For a G20 policymaker, the point is not the headline size alone. The point is that scale, when fused with public ownership and system responsibility, turns a utility into a policy instrument.

That institutional design changes how analysts should evaluate KEPCO. In more fragmented markets, governments often rely on regulation to steer multiple firms toward public goals. In Korea, a large share of that coordination problem sits inside one corporate structure. Decisions on network investment, maintenance discipline, procurement, and system planning therefore have macroeconomic consequences, not just corporate ones.

KEPCO's relevance extends beyond Korea. It offers a practical reference point for governments asking how much transition capacity can be concentrated inside a state-backed incumbent before coordination advantages begin to collide with reform constraints.

Vertical integration reshapes every policy lever

In KEPCO's model, generation, transmission, system operation, and end-user service are tightly connected. That means tariff policy, reliability management, capital allocation, and decarbonisation planning cannot be treated as separate files. A delay in one part of the system can quickly affect the rest.

Several implications follow.

- Planning authority is concentrated. Central coordination can support long-lead infrastructure and system adequacy if investment signals are aligned.

- Operational trade-offs sit within one structure. Fuel choices, grid constraints, maintenance schedules, and balance-sheet pressures affect the same institutional core.

- Policy errors spread system-wide. Poor incentives at the centre can distort investment, pricing, and reliability across the entire electricity sector.

For readers comparing state-led electricity models, this profile of State Grid Corporation of China provides a useful comparison. Both cases show how monopoly or near-monopoly utilities can serve industrial policy and energy security goals, while also making reform more politically and administratively demanding.

The engineering burden is also substantial. Running a national power system at this scale requires disciplined asset management, outage planning, and maintenance practices that are often overlooked in high-level transition debates. Technical references such as Forge Reliability's power generation solutions are useful here because they point to the operational realities behind policy ambition.

KEPCO's strategic importance comes from the interaction of ownership, scale, and control over system infrastructure.

That combination explains why KEPCO should be read as more than a domestic utility. It is a compact case study in the G20's central energy dilemma: how to use state capacity to protect affordability, reliability, and industrial competitiveness without further locking the system into slow-moving institutional arrangements.

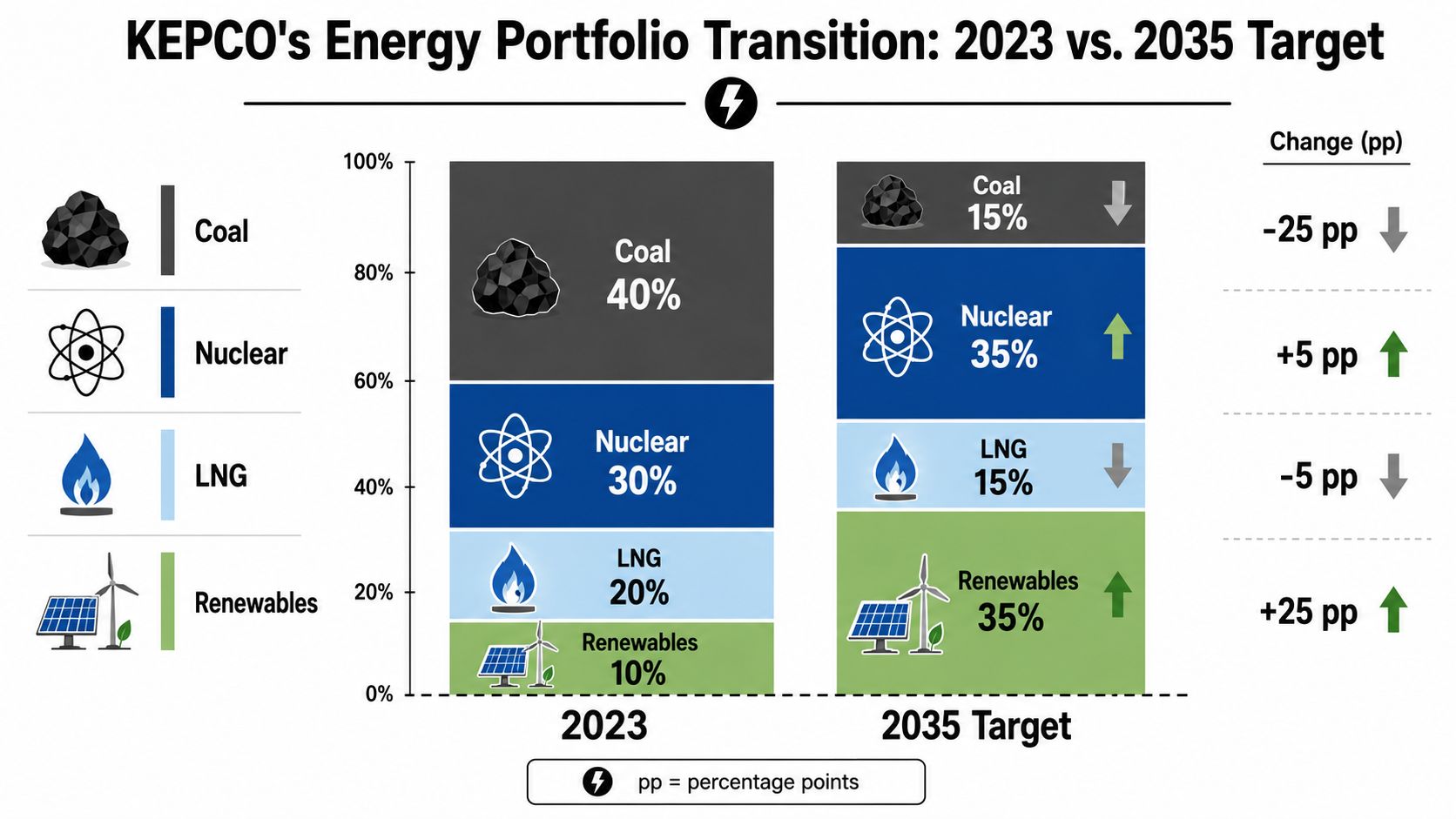

A Carbon-Intensive Portfolio in Transition

The central strategic problem is straightforward. KEPCO is large enough to matter for decarbonisation, yet its fleet remains firmly tied to thermal generation.

The portfolio problem is structural

BankTrack reports that KEPCO and its affiliates have 82.5 GW of installed capacity, with a generation mix of 39.5% coal and 21% LNG, according to BankTrack's KEPCO profile. For any government benchmarking transition pathways, that is the key starting point. KEPCO's fleet-level reality is still carbon-intensive.

This matters analytically because many policy discussions collapse all transition signals into a single narrative of momentum. That can be misleading. A utility can talk about solar, wind, and nuclear expansion and still remain structurally anchored to fossil generation in the near to medium term. In KEPCO's case, both things are true at once.

The policy implication is sharper than it first appears. When a utility of KEPCO's size retains such a substantial coal and LNG base, decarbonisation is no longer only about adding clean capacity. It becomes a question of retirement sequencing, system adequacy, fuel security, and political tolerance for change.

A short explainer on the broader energy context appears below.

Transition rhetoric meets fleet reality

A carbon-intensive portfolio doesn't automatically imply strategic failure. It often reflects legacy infrastructure, industrial demand patterns, reliability requirements, and state preferences around supply security. The problem arises when policymakers mistake a phased transition for a completed one.

That distinction matters in three ways:

| Policy question | KEPCO case | Why it matters internationally |

|---|---|---|

| Fleet composition | Coal and LNG still occupy a large share of installed capacity | Climate comparisons must account for incumbent thermal exposure |

| Transition financing | New low-carbon investment must coexist with legacy assets | Capital frameworks need to fund replacement and reliability together |

| Energy security | Thermal assets still support system stability | Governments won't abandon firm capacity without credible substitutes |

A utility can be in transition without yet being transformed. KEPCO is a clear example of that intermediate state.

For G20 officials, this is the deeper lesson. The hard part of power-sector decarbonisation isn't announcing a cleaner destination. It's managing the coexistence of old and new systems without causing affordability or reliability shocks. KEPCO shows what that coexistence looks like when the incumbent utility remains the primary carrier of national energy security.

Navigating Financial and Regulatory Headwinds

The most misunderstood part of the KEPCO story is its balance sheet. Commentaries often treat utility losses as a company problem. In reality, KEPCO's financial condition is a policy signal.

A strong credit signal can hide a policy weakness

Fitch affirmed KEPCO's AA- long-term issuer default rating on 13 February 2026, according to Fitch's KEPCO rating page. That rating tells markets that KEPCO retains high investment-grade standing. It suggests access to funding remains strong enough to support continued capital raising.

But that shouldn't be read as proof that the underlying transition model is comfortable. Strong credit and structural stress can coexist, especially when investors assume the state has compelling reasons to preserve the utility's functioning. In a strategic sector, credit strength can partly reflect sovereign importance rather than an easy operating environment.

Tariff politics shape decarbonisation capacity

Recent public reporting also indicates KEPCO posted a quarterly deficit of nearly 7.8 trillion won when retail electricity prices were kept artificially low by policy. That fact changes the policy interpretation of its finances. The issue isn't just cost management. It's tariff suppression as a transition risk.

A utility under political pressure to absorb shocks for consumers faces a difficult triad:

- It must keep power affordable.

- It must maintain system reliability.

- It must invest in grid upgrades and new supply.

Those goals are all legitimate. They are not always simultaneously financeable if pricing policy blocks cost recovery for extended periods.

For officials thinking about climate finance, that is a major governance lesson. Transition funding frameworks often focus on whether money is available. The KEPCO case points to a prior question. Can the institutional recipient convert capital into sustained delivery if domestic regulation weakens revenue stability?

A broader policy discussion of investable transition pipelines is relevant here in this analysis of energy transition investment frameworks.

Key judgement: When governments suppress tariffs to shield households and industry, they may also suppress the utility's capacity to finance decarbonisation.

That doesn't mean consumer protection is wrong. It means tariff design must be integrated with infrastructure planning and utility finance. Otherwise, the state transfers transition costs from bills to the balance sheet of the monopoly utility, and eventually back to the public sector in another form. KEPCO shows how that cycle can become embedded.

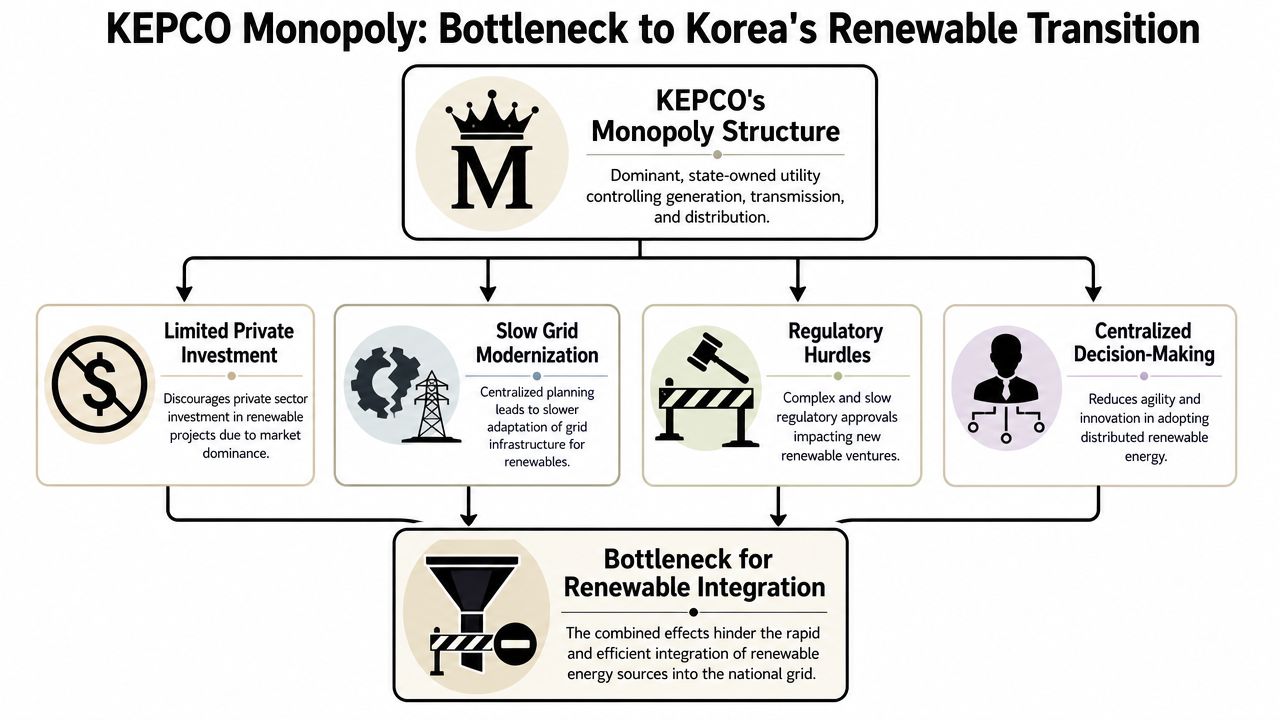

The Monopoly Bottleneck in Korea's Renewable Transition

The most important policy insight in the KEPCO case doesn't sit in generation statistics or credit ratings. It sits in the gap between renewable build-out and renewable delivery.

Capacity growth is no longer the whole story

According to IEEFA's analysis of renewable integration bottlenecks in South Korea, South Korea's renewable capacity rose sixfold from 2013 to 2023, but renewable electricity generation increased only threefold. IEEFA identifies KEPCO's monopoly structure, underdeveloped transmission and distribution systems, and ineffective PPAs and Renewable Portfolio Standard arrangements as major constraints.

That gap is analytically decisive. It suggests the bottleneck has shifted. The challenge isn't only adding projects. It is moving power through the network and aligning market rules so that renewable capacity can convert into usable generation at scale.

Why grid governance now matters most

When a monopoly utility controls core system access, several frictions can emerge even without overt obstruction:

- Connection priorities can lag system needs. Grid expansion may not keep pace with where renewable development is most viable.

- Commercial arrangements can remain weak. If PPAs don't function effectively, project bankability suffers.

- Planning can favour stability over speed. That can be rational from a reliability perspective, but costly for transition momentum.

For readers interested in the infrastructure logic behind more open network design, how open grid systems benefit construction offers a useful practical lens on why access architecture affects project delivery.

A monopoly model can still deliver rapid decarbonisation, but only if it is deliberately retooled for that task. KEPCO's case suggests South Korea has entered a new phase where grid governance matters more than headline deployment ambition.

The strategic question is no longer, "Can Korea build more renewables?" It is, "Can the system operator and market architecture absorb them efficiently?"

That question resonates far beyond Korea. Many G20 economies face some version of the same challenge, whether through connection queues, weak transmission planning, or poorly aligned procurement rules. KEPCO brings that issue into sharp relief because the institutional responsibility is so concentrated. When one utility dominates the system, reform can be powerful if it happens. But delay can also become systemic.

KEPCO's Global Ambitions and Geopolitical Role

KEPCO also matters because it is not confined to the domestic arena. State-backed utilities often travel as extensions of national strategy, carrying financing, engineering credibility, and political relationships into overseas markets.

A utility that travels with the state

In that sense, KEPCO should be read as part of South Korea's geopolitical toolkit. Its overseas role has long been associated with the export of power-sector capability, especially where governments want partners that can combine technical delivery with state-level reliability. That matters most in nuclear and large-scale infrastructure discussions, where counterparties are often choosing not only a contractor but a strategic relationship.

This is why KEPCO's international profile can't be separated from wider questions of industrial policy. A utility with domestic operational depth can support export diplomacy in ways that private developers often can't. It can present itself as a long-horizon partner rather than a purely commercial bidder.

Why other governments should care

For other G20 governments, there are two implications.

First, KEPCO is a competitor. In markets where governments are reassessing nuclear power, grid reinforcement, and strategic infrastructure partnerships, a utility with strong state backing can become a serious external actor.

Second, KEPCO is a potential partner. Governments seeking technically capable counterparts for complex energy infrastructure may find state-linked utilities attractive, particularly when reliability and sovereign confidence matter as much as price.

That external role sharpens the contradiction at the centre of the company. KEPCO can project advanced energy capability abroad while still wrestling at home with carbon intensity, pricing constraints, and renewable integration bottlenecks. That isn't hypocrisy. It's the actual condition of many major energy institutions in the transition era. They are expected to operate legacy systems, fund new systems, and compete internationally at the same time.

The geopolitical lesson is clear. Energy statecraft now depends less on abstract pledges and more on whether countries possess institutions able to build, finance, and operate strategic infrastructure under pressure. KEPCO has that capability. The unresolved question is whether its domestic governance model will strengthen or constrain its long-term international standing.

Conclusion Policy Lessons for Multilateral Energy Governance

KEPCO makes a larger point than many international energy statements do. The decisive variable in the transition is institutional capacity. Countries can adopt ambitious targets and still fall short if the utility at the centre of the power system cannot finance investment, connect new supply fast enough, or absorb political pressure over prices.

For G20 ministers, KEPCO is less a Korean story than a concentrated version of a shared problem. It shows how energy security, industrial competitiveness, public affordability, and decarbonisation collide inside one balance sheet and one governance structure. That is the level at which multilateral policy often becomes practical or fails.

What ministers should take from the KEPCO case

- Treat utility finance as part of transition architecture. A utility that cannot recover costs on a durable basis will defer grid upgrades, slow procurement, and weaken investor confidence, even under strong climate commitments.

- Judge renewable progress by delivered power and system absorption. Capacity announcements are an incomplete metric if curtailment, connection delays, or transmission limits prevent output from reaching consumers.

- Address grid governance before bottlenecks become political crises. Where one incumbent controls interconnection and network planning, transmission rules and access procedures shape the pace of decarbonisation as much as headline subsidies do.

- Distinguish borrowing capacity from transition quality. Credit strength can fund investment for a period, but it does not resolve weak tariff design, exposure to fossil generation, or misaligned regulatory incentives.

For multilateral governance, the central lesson is straightforward. International forums still separate clean finance, energy security, market reform, and industrial policy into different conversations. KEPCO shows that power-sector institutions must execute all four functions simultaneously.

Governments decarbonise power systems through institutions with balance sheets, legacy assets, regulatory obligations, and political constraints.

That point should reshape the G20 energy agenda. Ministers need a more institutionally literate framework that gives sustained attention to utility solvency, regulated price formation, transmission access, and state-owned enterprise governance. These may appear administrative. In practice, they determine whether climate policy can be implemented at scale.

KEPCO therefore deserves attention as a case study in multilateral governance, not only national reform. Many countries are asking incumbent utilities to preserve reliability, contain costs, support industry, and cut emissions at the same time. The systems that manage those trade-offs with clear incentives and credible financing will build durable low-carbon capacity. The systems that avoid those governance questions will keep producing a gap between announced transition and delivered transition.

If you want more analysis like this from Global Governance Media, follow its coverage of G7 and G20 energy, climate, and economic governance. The most useful policy debates now sit at the intersection of infrastructure, finance, and state capacity, and that's exactly where sharper public analysis is needed.