By Daniel Mercer, Senior Policy Analyst

State Grid Corporation of China serves over 1.1 billion people across China's 26 provinces, according to the World Economic Forum profile of the company. That single fact changes how ministers should view it. This isn't merely a large utility. It operates at the scale of a national operating system for electricity.

For G20 energy ministers, the fundamental policy question isn't whether State Grid Corporation of China is large, or even whether it is technologically capable. It is what a utility of that scale, under state ownership and with an expanding international footprint, means for grid transition strategy elsewhere. Western debate often treats grid modernisation as a financing or engineering problem. SGCC suggests it is also a governance problem. Who decides on transmission buildout, who absorbs long-term investment risk, and who controls the digital layer of power systems may matter as much as any individual technology choice.

That is why SGCC deserves close attention from governments far beyond China. Its model combines domestic system stewardship, strategic industrial policy, and external infrastructure investment. For policymakers facing grid congestion, renewable integration challenges, and political resistance to long-duration capital programmes, resilient grid planning has become central to the wider energy transition debate.

Table of Contents

- An Introduction to the World's Largest Utility

- A Behemoth Defined Ownership Governance and Domestic Mandate

- Powering China's Decarbonisation Journey

- Expanding the Grid SGCCs Global Investment Footprint

- Engineering Dominance UHV Smart Grids and Exportable Tech

- Geopolitical Implications and Systemic Risks

- A Policy Roadmap for G7 and G20 Engagement

An Introduction to the World's Largest Utility

More than 1.1 billion people receive electricity through State Grid Corporation of China. Few entities in any sector operate at that scale. For G20 policymakers, the starting point is not corporate size alone, but what that scale allows a state-directed grid operator to do in planning, financing, and system coordination.

State Grid Corporation of China, established in 2002, is widely described as the world's largest utility. Its significance, however, extends beyond headline metrics. SGCC sits at the intersection of infrastructure policy, industrial strategy, and public administration. That makes it a poor fit for standard comparisons with investor-owned utilities in liberalised power markets, where network expansion is usually shaped by regulatory incentives, fragmented jurisdiction, and more limited tolerance for long payback periods.

A useful frame for ministers considering how resilient grids underpin the broader energy transition is this: SGCC operates less like a conventional company and more like a state-backed system planner with operational responsibilities. In practice, that changes the tempo of investment decisions and the range of tools available to management.

Why scale changes the policy lens

The main policy question is not whether SGCC is large. It is how a utility of this size behaves when ownership, financing capacity, and national policy direction reinforce one another.

A company serving most of a continental power system can spread costs across regions, maintain service obligations in weaker provincial markets, and pursue transmission buildout with a time horizon that many Western operators would struggle to justify to investors or regulators. This is one reason SGCC matters in G7 and G20 discussions about grids. It offers a live example of what happens when transmission is treated as strategic state capacity rather than a regulated asset category alone.

That comparison also exposes a blind spot in many Western debates. Grid transition is often presented as a financing problem. The Chinese case suggests that institutional fragmentation can be just as constraining as capital scarcity, especially where permitting, planning, digital standards, and network ownership sit in separate bureaucratic or commercial silos.

Why SGCC matters beyond China

SGCC should not be treated as a template for direct replication. Different political systems, legal frameworks, and capital markets set clear limits on that. Yet dismissing the company as an outlier would miss the wider lesson.

Its record shows that state-led coordination can accelerate grid expansion and digital deployment under certain conditions. It also shows the trade-off. The same model that can compress decision cycles and align investment with industrial policy can concentrate operational, financial, and political power in ways that many market economies would regard as difficult to accommodate.

For G20 energy ministers, the analytical value of SGCC lies in this tension. It clarifies what market-led systems may gain from stronger public coordination, and what they may still choose to reject in order to preserve competition, transparency, and institutional checks.

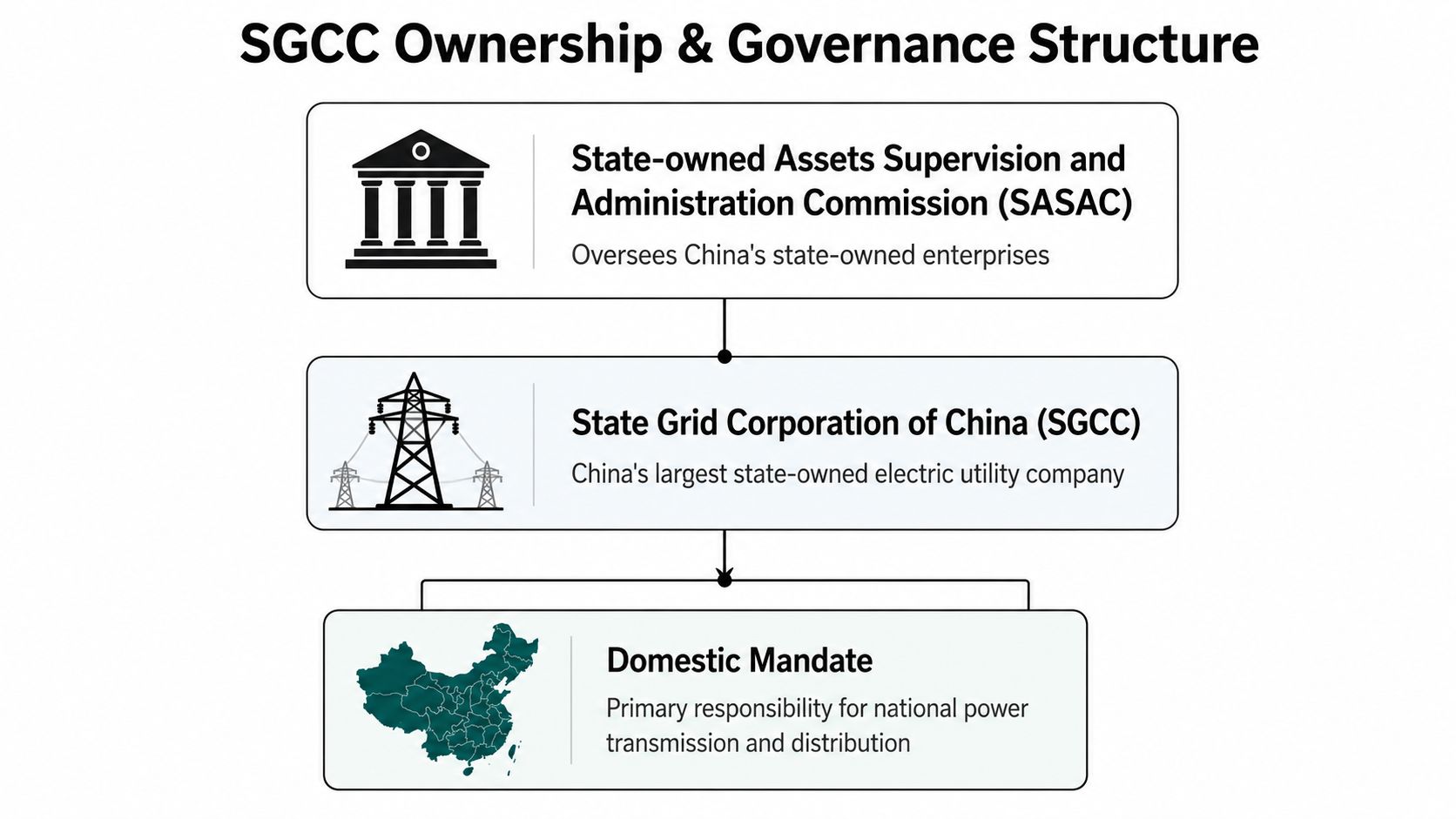

A Behemoth Defined Ownership Governance and Domestic Mandate

SGCC is best understood as an instrument of state capacity with corporate form. That distinction matters for policy analysis because it shapes how the company allocates capital, absorbs risk, and responds to political instruction.

Why ownership changes the analytical frame

As noted earlier, SGCC's service footprint covers most of China's population and much of its provincial geography. The policy implication is larger than scale alone. In practice, the company operates less like a regional utility and more like a nationally significant network platform whose investment choices carry consequences for industrial competitiveness, energy security, and administrative coordination.

That creates a governance logic that differs sharply from the one familiar across many G7 systems. Investor-owned or heavily market-disciplined utilities usually work within a tighter boundary between commercial return and public obligation. SGCC sits inside a different settlement. Financial performance matters, but it is assessed alongside state priorities, including long-horizon infrastructure buildout and system stability.

For ministers comparing models, this is the key point. The Chinese case joins ownership, planning, and network control in one institutional architecture.

How state ownership shapes investment behaviour

The contrast with market-led systems is clearest when viewed through incentives rather than ideology.

| Dimension | Typical market-led utility model | SGCC model |

|---|---|---|

| Primary accountability | Investors, regulators, customers | State ownership and national strategic objectives |

| Investment horizon | Often constrained by market incentives and regulatory cycles | Can support longer-term buildout under state direction |

| System role | Network operator within a regulatory market design | National infrastructure backbone with strategic mandate |

| Policy function | Implements rules set by government and regulator | Also acts as an instrument of state capacity |

This does not mean SGCC operates without constraint. It means the relevant constraints are political, administrative, and strategic as much as commercial. That difference helps explain why the company can support projects justified by system resilience, regional balancing, or national development goals even when the payoff profile would be harder to defend in a narrower shareholder framework.

China's planning process reinforces this model. Decisions on infrastructure sequencing do not emerge from grid regulation alone. They sit within a broader state planning system, including the priorities set through China's five-year planning framework, which helps align energy, industry, and regional development objectives.

Practical rule: Where the state owns the backbone network, grid expansion becomes a question of administrative coordination and strategic intent, not only market appetite.

That has direct relevance for G20 debates. First, SGCC shows how a state-backed operator can compress the distance between national policy goals and transmission investment decisions. Second, it highlights the trade-off. The same structure that can accelerate buildout also concentrates operational authority and reduces the institutional separation that many Western systems use to protect transparency, competition, and independent oversight.

The broader conclusion is not that G7 countries should copy SGCC. It is that grid governance choices shape build speed, digital integration, and policy coherence as much as financing does. Western debates often treat those issues separately. The SGCC model shows what happens when they are combined under one owner and one strategic mandate.

Powering China's Decarbonisation Journey

China's decarbonisation challenge is defined by distance. Major renewable resources sit far from many coastal and industrial demand centres, so the pace of emissions reduction depends not only on how much clean generation is built, but on whether the grid can move that power at scale and keep the system stable. That is the point at which SGCC becomes strategically important for G20 policymakers.

Transmission as climate policy

In China, transmission functions as part of climate policy, industrial policy, and security policy at the same time. Grid expansion determines whether remote wind, solar, and hydropower can displace coal generation in load centres rather than remaining stranded behind provincial or regional bottlenecks.

This has wider relevance than China alone. In many G7 and G20 economies, grid investment is still treated as a slower, more procedural complement to clean energy deployment. SGCC shows the consequences of a different institutional design. A state-led operator can sequence transmission, generation integration, and system balancing under a single national mandate, which reduces coordination frictions that often delay market-led systems.

The strategic implication is not that other countries should replicate China's governance model. It is that transmission planning cannot remain a secondary regulatory exercise if governments expect electrification and clean power targets to be met on time.

A similar point appears in debates around multilateral infrastructure finance, including the role of the Asian Infrastructure Investment Bank in cross-border energy and connectivity projects. Capital matters, but institutional capacity to approve, build, and operate networks often matters more.

Why digitalisation matters but does not settle the debate

Digitalisation strengthens grid performance by improving forecasting, dispatch, visibility, and system control. It does not remove the need for wires, substations, land access, and long-horizon capital planning. Any assessment of SGCC that focuses only on smart grid rhetoric misses the harder policy lesson. Digital systems can improve how a network runs, but they cannot compensate for underbuilt transmission.

That distinction is highly relevant to Western grid debates. Market-led systems often assume that better data, more flexible demand, and improved software can defer large-scale network expansion. Some of that is true at the margin. It is less convincing when electrification, renewable buildout, and regional rebalancing all accelerate at once.

The more useful comparison is institutional. SGCC's model suggests that states able to align planning authority, financing capacity, and operating control may build transmission faster than systems that split those functions across multiple regulators, private owners, and subnational jurisdictions. Yet the same concentration of authority raises harder questions about transparency, accountability, cyber resilience, and the treatment of competing market participants.

For G20 ministers, that creates a sharper conclusion than the usual debate between state control and market competition. Grid transition strategies should be judged by delivery capacity. Can the governance model approve corridors, mobilise capital, integrate variable renewables, and maintain public trust in system operation? SGCC offers evidence that central coordination can speed physical buildout. It also shows that digital modernisation, on its own, is not a sufficient test of system quality.

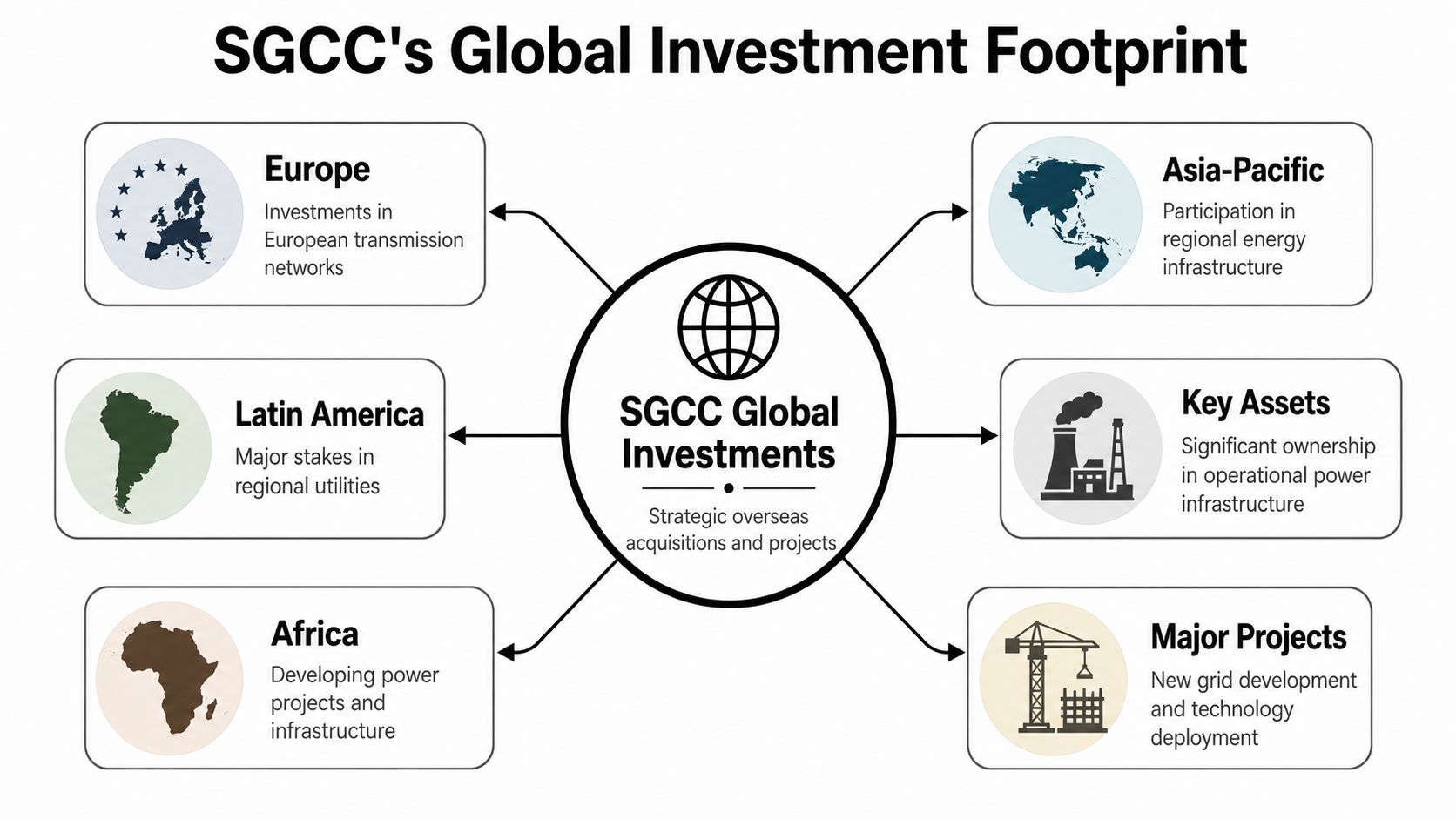

Expanding the Grid SGCCs Global Investment Footprint

SGCC's significance doesn't stop at China's borders. It has become an international grid investor with enough geographic spread to matter for foreign ownership debates, resilience planning, and strategic infrastructure screening.

A network investor not a passive shareholder

According to the verified data drawn from the Belt and Road portal's SGCC overview, the company has 13 backbone energy network projects across 10 countries and regions and overseas assets totalling RMB320 billion. The same source notes active operations in developed markets including Portugal, Italy and Greece.

That combination is strategically important. These aren't only investments in frontier markets where capital scarcity may outweigh governance concerns. They include advanced economies with established regulatory systems and higher political sensitivity around critical infrastructure. SGCC's role abroad therefore needs to be read as participation in the ownership and operation of strategic networks, not as portfolio diversification.

For ministers in G7 and G20 capitals, that means SGCC has become part of a broader question about who owns and influences electricity backbones in an era of geopolitical competition. It is no longer enough to ask whether a foreign investor brings capital. Governments also have to ask what kind of state relationship stands behind that capital.

A useful adjacent debate concerns the wider architecture of cross-border infrastructure finance, including institutions often discussed in relation to strategic development capital such as the Asian Infrastructure Investment Bank.

Why host governments treat grid ownership differently

Electricity networks are unlike many other infrastructure assets because they combine territorial reach, public necessity, and operational data. Ownership therefore carries implications beyond finance.

Three host-country concerns tend to shape policy responses:

- Sovereign control: Transmission and distribution systems sit close to national resilience planning, emergency response, and industrial continuity.

- Regulatory influence: A backbone investor may gain long-term influence through standards, procurement relationships, and technical dependencies.

- Political signalling: Accepting or rejecting investment from a state-backed foreign utility can itself become a foreign policy message.

This is why SGCC's overseas pattern matters even where it doesn't directly operate a domestic utility in a given country. It has become a benchmark case in how governments think about strategic openness. The central issue is not only China. It is whether the old distinction between “commercial investor” and “strategic actor” still holds in electricity networks. In SGCC's case, it often doesn't.

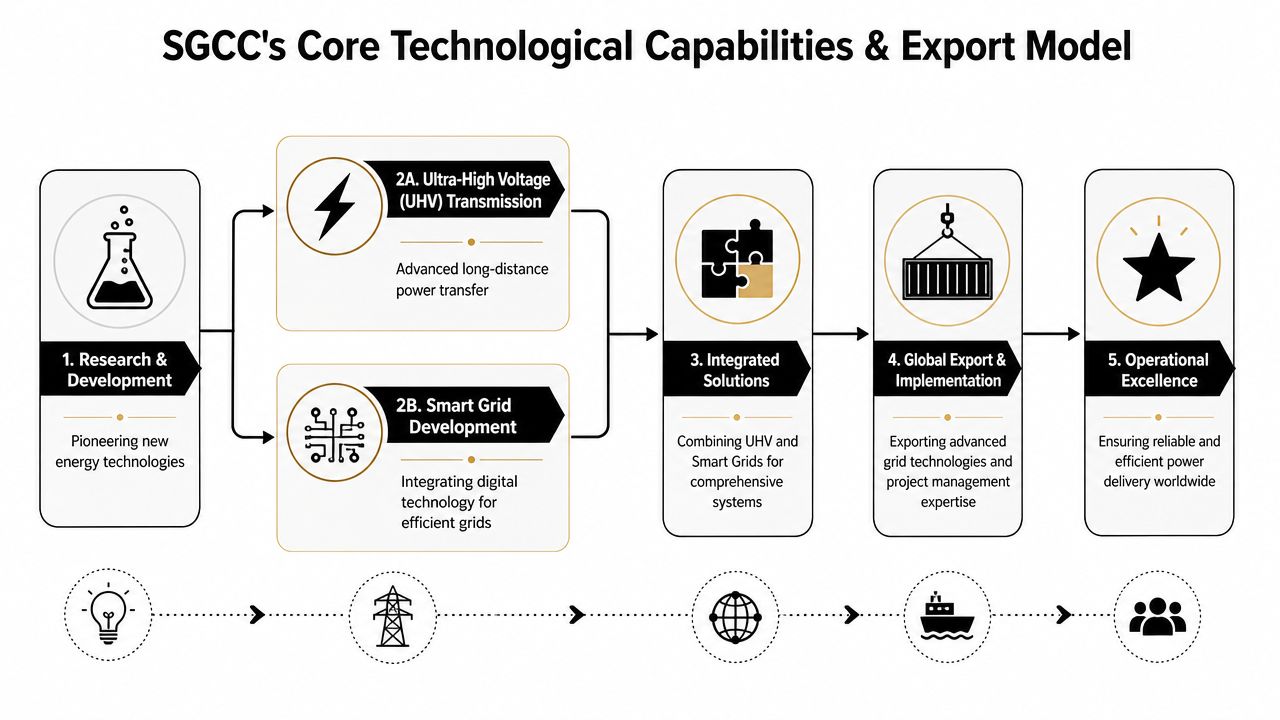

Engineering Dominance UHV Smart Grids and Exportable Tech

The most important feature of SGCC's technology position is not any single piece of hardware. It is the integration of transmission, digital control, and project execution into a coherent system offer.

An integrated infrastructure offer

The verified record states that SGCC's overseas footprint includes operations in 51 countries, signalling a highly exportable grid-integration model, according to the Belt and Road reporting page on its international activities. That same source presents SGCC's scale in deploying cross-border and backbone grids as a benchmark for procurement strategy, resilience planning, and interoperability standards for large-system operators globally.

That point deserves emphasis. The exportable product isn't just equipment. It is a package. Planning assumptions, grid architecture, technology standards, implementation know-how, and operating logic can travel together. For procurement officials, that creates a very different decision environment from buying isolated components.

The embedded video below gives a useful visual reference point for how SGCC presents its grid model and engineering identity in public-facing terms.

Standards influence follows system integration

In infrastructure markets, standards influence often follows installed systems. Once a country adopts a tightly integrated network model, future procurement, maintenance, cybersecurity design, and interoperability choices may begin to narrow.

That is why SGCC's technological relevance extends into policy. A company operating at very large scale in multiple jurisdictions can shape what becomes normal in backbone-grid design. Governments therefore shouldn't look only at capex bids or engineering performance. They should examine control systems, supply chains, upgrade paths, and the role of data-bearing network components.

For ministries trying to modernise substations, industrial control environments, and distributed network operations, technical scrutiny has to reach the automation layer as well. Practical work on secure automation networks is relevant here because the resilience of modern grids increasingly depends on how communications, devices, and control architectures are connected and governed.

The strategic issue isn't who sells a transformer. It's who defines the operating environment around the grid for decades.

In that sense, SGCC's engineering strength is inseparable from its institutional strength. Domestic scale has allowed it to develop and deploy an integrated model that can be exported abroad. The procurement consequence is straightforward. Technology choice and strategic dependence can become the same decision.

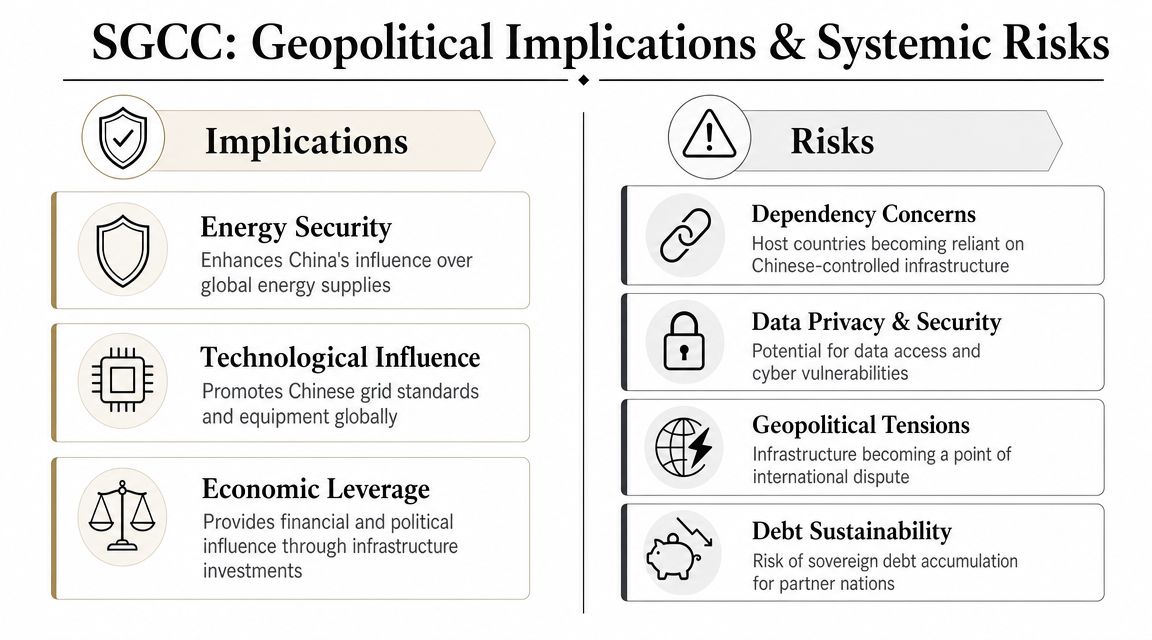

Geopolitical Implications and Systemic Risks

The policy debate around SGCC often swings between two weak positions. One treats the company as a uniquely capable builder that can help close infrastructure gaps. The other treats it as self-evidently unacceptable because it is Chinese and state-owned. Neither position is sufficient for ministers making real decisions under time pressure.

Critical infrastructure is not a neutral asset class

Electricity networks are critical national infrastructure. That phrase is frequently used, but not always unpacked. In practical terms, it means a grid operator or strategic investor can affect reliability, maintenance logic, emergency planning, equipment pathways, and long-term system configuration. If the owner or technology provider is state-backed, host governments have to ask whether commercial governance alone is enough to manage strategic risk.

The concern isn't that every foreign stake automatically creates political influence. It is that electricity networks create channels through which such influence could matter at moments of stress. A government may discover that resilience depends on vendor responsiveness, software trust, access to replacement components, or decision rights around upgrades. Those dependencies can remain invisible in normal market conditions.

SGCC's profile holds significance. It is large enough, state-backed enough, and internationally present enough to force governments into a more serious framework for infrastructure screening.

Digital grids create a second layer of exposure

As grids become more digital, the security question changes. Traditional network risk centred on physical assets and operational continuity. Modern grid risk also involves data, software, communications architecture, and system visibility.

That creates a second layer of exposure:

- Operational data sensitivity: Grid data can reveal usage patterns, critical loads, and infrastructure constraints.

- Cybersecurity governance: Trust depends not only on devices but on update chains, access controls, vendor relationships, and incident response.

- Technology lock-in: Once digital systems are embedded, replacing them can become costly, politically difficult, and operationally risky.

Ministerial test: Before approving strategic grid investment, ask whether the country could still operate, maintain, and upgrade the system on sovereign terms during a geopolitical dispute.

This doesn't make engagement impossible. It does make passive openness irresponsible. Countries need due diligence that goes beyond competition policy or conventional takeover review. They need to examine whether foreign participation introduces governance asymmetries in the digital layer of the grid.

The financing advantage comes with policy trade-offs

SGCC's attraction to some host countries is understandable. Large state-backed entities can support long-duration infrastructure investment in sectors where commercial returns may be slow, politically constrained, or heavily regulated. That can be particularly appealing where domestic capital is scarce or where governments need rapid network expansion.

But the financing advantage can blur real trade-offs. Cheap or patient capital is only one variable. Governments also need to assess how ownership, operational influence, and technical architecture affect strategic autonomy over time.

A balanced risk framework should distinguish between at least four dimensions:

| Risk dimension | Why it matters for SGCC-related decisions |

|---|---|

| Ownership risk | State backing means commercial incentives may not be the only driver |

| Operational risk | Network involvement can influence maintenance, resilience, and contingency planning |

| Digital risk | Smart-grid systems can create data and cybersecurity exposure |

| Standards risk | Integrated technology choices may shape future interoperability and vendor dependence |

There is also a broader geopolitical effect. If major economies allow strategic grid assets or digital infrastructure layers to become dependent on foreign state-backed entities, they may weaken their bargaining position in unrelated policy disputes. Energy infrastructure can become part of a wider map of interdependence.

That said, governments shouldn't overcorrect into blanket exclusion without strategy. Such a response can leave them with another vulnerability, namely underinvestment and delayed grid expansion. The key policy challenge is to separate useful engagement from avoidable dependency.

A disciplined approach usually involves three questions. First, is the asset commercially important or systemically critical? Second, does the transaction involve passive capital, operating influence, or technology lock-in? Third, can the host state preserve auditability, cybersecurity control, and emergency authority after the deal is signed?

If ministers can't answer those questions clearly, the problem isn't only the investor. It is the policy framework.

A Policy Roadmap for G7 and G20 Engagement

Electricity demand, network congestion, and clean-energy connection queues are rising at the same time in many major economies. That combination makes grid policy a first-order economic issue, not a technical afterthought. For G7 and G20 ministers, the practical question is what SGCC's state-led model reveals about the weaknesses of market-led grid transition frameworks.

The relevant lesson is institutional, not ideological. SGCC shows what becomes possible when a state treats transmission, distribution, digital control systems, and long-horizon capital allocation as part of one national strategy. Most G7 systems will not, and should not, replicate that governance model. Their legal structures, ownership patterns, and political constraints are different. But the comparison is still useful because it exposes a persistent Western policy gap. Generation targets are often clearer than the delivery model for the networks needed to support them.

That gap has strategic consequences.

A credible response starts with three judgments. First, transmission and distribution need explicit strategic status in energy policy, industrial policy, and fiscal planning. Second, digitalisation cannot be treated as a software layer added after physical bottlenecks appear. Third, regulatory systems must reward timely buildout, resilience, and interoperability rather than focusing too narrowly on short-term cost containment.

Several policy lessons follow from that diagnosis:

- Treat grids as enabling infrastructure for the whole transition. Decarbonisation plans fail in practice when network expansion remains slower than generation deployment, electrification, and new industrial load.

- Create longer investment horizons. Grid assets require policy settings that support patient capital, predictable returns, and anticipatory investment where future system needs are reasonably clear.

- Integrate physical and digital planning. Advanced dispatch, monitoring, and demand flexibility produce better results when paired with network reinforcement, substation upgrades, and stronger system architecture.

- Clarify public authority. In many market-led systems, responsibility is fragmented across regulators, utilities, system operators, local permitting bodies, and private investors. Fragmentation protects pluralism, but it can also slow delivery unless ministers assign clear decision rights.

The hardest conclusion is also the most important. Many democratic systems have preserved market principles without building institutions capable of executing grid expansion at the required speed.

Policy should therefore focus less on abstract arguments about state versus market and more on capability. G7 and G20 governments need frameworks that preserve competition and regulatory independence while still allowing the state to plan, permit, finance, and secure strategically important network infrastructure.

A practical agenda includes five steps.

Tighten screening for critical grid investments. Review mechanisms should distinguish passive capital from transactions that create operational influence, privileged data access, or long-term technology dependence.

Set interoperability requirements before procurement decisions harden. Strategic grid equipment and software should be auditable, replaceable, and compatible with multi-vendor systems.

Build domestic and allied industrial capacity. If governments want alternatives to state-backed foreign suppliers, they need targeted support for transmission equipment, power electronics, control software, and cybersecurity assurance.

Reform network governance where delivery is too slow. Ministers should examine whether current regulatory incentives, planning rules, and permitting systems can deliver transmission corridors and digital upgrades on the timetable implied by national climate and industrial goals.

Coordinate standards and screening approaches across the G7 and G20. Fragmented rules create arbitrage opportunities. Greater alignment would reduce the risk that dependencies accumulate through the least restrictive jurisdiction.

The central insight is straightforward. SGCC is not only a company to assess. It is a test of whether other major economies can combine openness with strategic discipline.

That is the policy challenge for G20 energy ministers. The objective is not to centralise by imitation. It is to build democratic, market-based systems that can still act with coherence, mobilise long-term capital, and retain sovereign control over critical grid assets and digital infrastructure.

For ongoing analysis of G7 and G20 energy policy, summit agendas, and the strategic choices shaping grid transition, follow Global Governance Media.