By Eleanor Whitmore

By August 2025, the UK had more than 19 GW of installed solar capacity across more than 1.6 million homes, according to government data summarised by Sunsave's UK solar statistics overview. That single fact changes the policy lens. A roof solar panel system is no longer best understood as a household appliance purchase. At national scale, it becomes distributed infrastructure embedded in the built environment.

That shift matters for G20 policymakers because distributed generation changes how governments think about resilience, peak demand, grid investment, industrial standards, and social legitimacy in the energy transition. A country with millions of small generators isn't managing a retail technology trend. It's governing a decentralised layer of the power system.

Table of Contents

- The Strategic Ascent of Rooftop Solar

- Technology and Performance Benchmarks

- The Economic Case for Distributed Solar Power

- Crafting Effective Regulatory Frameworks

- Integrating Rooftop Solar for Grid Resilience

- Lessons from G7 and G20 Nations

- Actionable Policy Pathways for 2026

The Strategic Ascent of Rooftop Solar

Global solar capacity reached about 1.6 TW in 2023, with roughly 46 million households using solar systems worldwide, according to Green's solar statistics compilation. At that scale, rooftop solar is no longer a marginal retail technology. It is a distributed generation fleet with consequences for national security, industrial policy, and power system design.

From consumer purchase to state concern

A roof solar panel fleet affects three areas of state responsibility at once. It diversifies generation across millions of sites, which reduces reliance on a smaller number of central assets and can limit exposure to fuel supply shocks. It converts climate policy into operating infrastructure, because each installed system adds zero-fuel generation capacity that can persist for decades. It also changes grid management, since power now flows from behind the meter into networks that were built for one-way delivery.

This shift has policy implications that are easy to miss if rooftop PV is framed mainly as a household purchasing decision. Governments that focus only on bill savings understate the strategic value of distributed solar in periods of price volatility, import dependence, or constrained grid expansion. The stronger interpretation is that rooftop solar functions as privately owned infrastructure with system-level public effects.

Why scale changes the policy task

Once deployment reaches national significance, public policy has to move from market stimulation to system coordination. Interconnection rules, inverter standards, export pricing, installation quality, data access, and battery readiness begin to matter more than awareness campaigns. The policy question is no longer whether households are interested. It is whether the state can integrate a large, decentralised asset base into a reliable electricity system.

That places rooftop solar within the same strategic debate as wider analysis of the global energy transition. Distributed assets are becoming part of core system architecture, alongside transmission, storage, and demand response.

Rooftop solar is infrastructure dispersed across private property but carrying public value.

That governance model is unusual. Households and businesses own the panels, but network operators and governments manage many of the consequences, including voltage stability, midday surplus, system visibility, and equity across tariff classes. The result is a clear state interest in standards and orchestration, even where ownership remains private.

Delivery capacity also matters. National targets are often constrained less by political ambition than by permitting delays, installer availability, inspection bottlenecks, and uneven local implementation. For a practical illustration of how these deployment chains work in one subnational market, guidance on how to install solar panels in NSW shows the operational steps that sit between policy design and commissioned rooftop capacity.

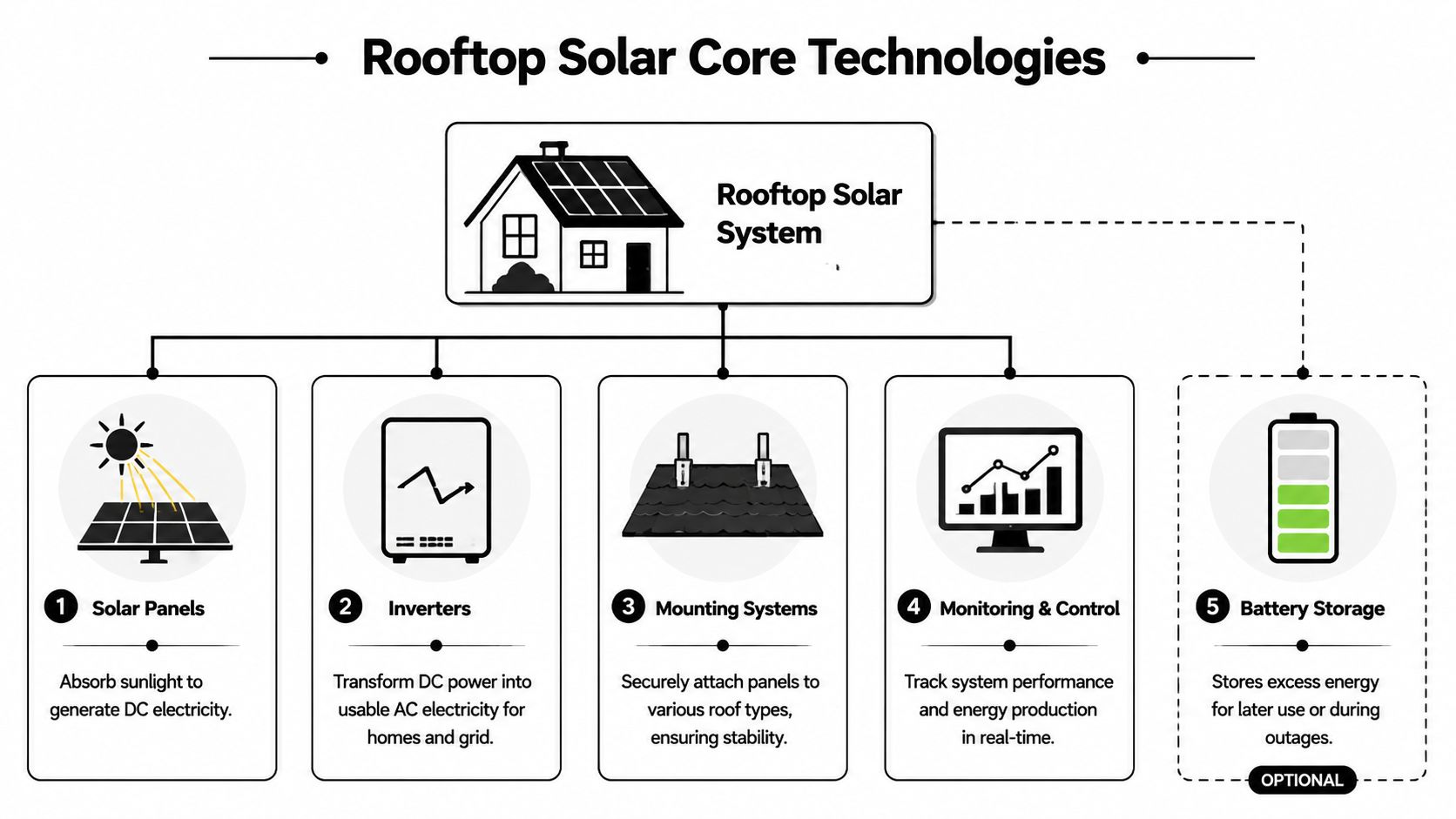

Technology and Performance Benchmarks

About 40 percent of final energy-related CO2 emissions are tied to buildings, according to the IEA. That makes rooftop solar a building-sector technology with system-level consequences. Performance benchmarks therefore matter for more than procurement. They determine how much urban surface can be converted into dependable generation capacity, how predictable that output becomes for network operators, and how much strategic value governments can extract from distributed assets.

A practical planning metric is roof productivity. A typical 5 kW rooftop system generally needs about 20–25 m² of usable roof area, and higher-wattage modules reduce the square metres required per installed kilowatt, according to Maysun Solar's panel sizing guide. For national planners, that is a housing-stock question before it is a subsidy question.

What policymakers need to know about the hardware

The policy objective is not to maximise module count. It is to maximise reliable yield per constrained square metre while keeping distributed generation visible, safe, and grid-compatible.

| Policy concern | Why it matters |

|---|---|

| Roof area | Sets the physical ceiling for deployment across housing types, public buildings, and commercial stock |

| Module efficiency | Higher efficiency raises output from constrained urban surfaces |

| Inverter quality | Conversion performance and control functions shape real-world yield and grid behaviour |

| Compliance standards | Standardised equipment lowers technical failure risk and improves lender and regulator confidence |

Technical specifications used in rooftop PV programmes commonly require crystalline silicon modules, MPPT-controlled inverters, compatibility with 50 Hz grids, module compliance such as IEC 61215-type qualification, module efficiencies around 15–16%+, and inverter efficiency of at least 95%. Those parameters belong in policy design because they affect system yield, inspection quality, and the credibility of public support schemes.

Roofs are a national infrastructure constraint

Utility-scale solar is constrained mainly by land, transmission access, and permitting. Rooftop solar is constrained by geometry, shading, orientation, and building quality. That distinction has strategic implications. A country can publish a large rooftop target and still miss it if its urban building stock cannot host the capacity at acceptable performance levels.

This is why capacity planning should start with parcel-level or district-level roof assessments. Governments that map usable roof area, feeder constraints, and load centres can target deployment where distributed generation reduces network stress and import exposure. Governments that rely on headline national targets alone risk overestimating technical potential and underpreparing distribution systems.

Practical rule: Rooftop solar policy should begin with a housing and building-stock map linked to grid data.

Performance is operational, not theoretical

Installed capacity is a weak proxy for strategic value. What matters is delivered electricity during actual operating conditions, including partial shading, seasonal temperature effects, roof complexity, inverter performance, and maintenance discipline.

That has direct policy consequences. Quality assurance after commissioning should receive the same attention as installation incentives. For municipalities, housing providers, and public asset managers setting upkeep standards, these solar panel maintenance tips show the kind of operational detail that can protect output over time.

A wider implication follows. Urban energy policy should treat roofs, façades, and glazing as a single class of productive surface. The same spatial logic appears in building-integrated solar cell windows. In dense cities, surface efficiency is not a design preference. It is a strategic constraint on domestic generation capacity.

The Economic Case for Distributed Solar Power

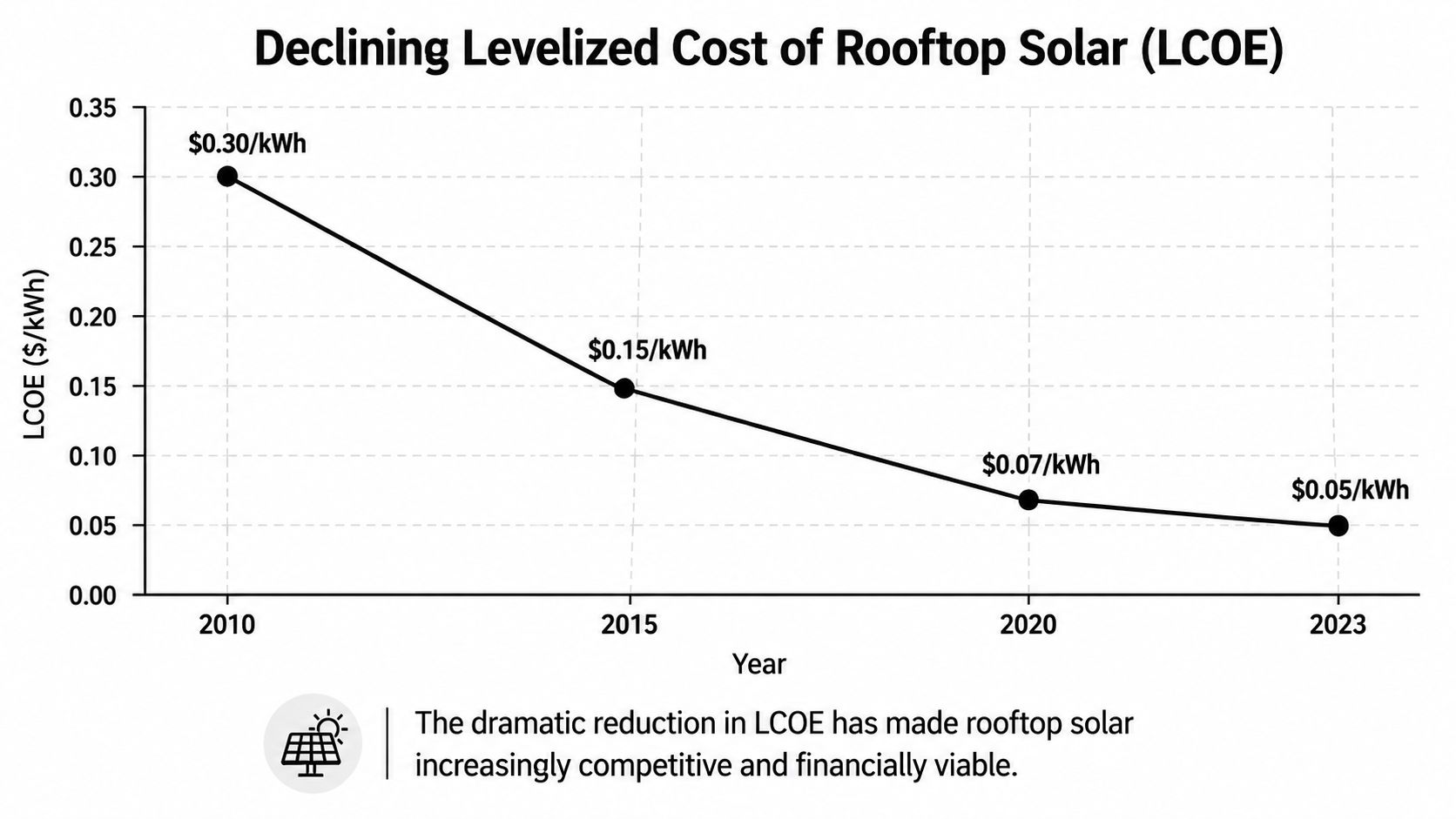

Distributed solar has moved from a niche subsidy case to a capital allocation question. For governments, the central issue is whether rooftop capacity is priced and regulated as strategic infrastructure that lowers peak demand, reduces fuel imports, and defers network investment. Where those system benefits are recognised, projects become financeable at scale. Where they are ignored, deployment remains fragmented even if module costs fall.

Equipment quality still matters, but the economic argument is broader than hardware selection. Higher-performing modules and reliable inverters improve output per square metre and reduce underperformance risk, as noted earlier. The larger point is that financial returns depend on whether regulation converts technical output into dependable revenue and measurable system value.

Early in any market, visual evidence can clarify the investment story.

Returns depend on policy quality

A technically sound roof solar panel project can still fail economically under unstable rules, weak interconnection processes, or poorly designed compensation. The reverse is also true. Clear policy can turn modest rooftop resources into a bankable asset class.

Three policy levers shape that outcome:

- Revenue certainty through stable export compensation, self-consumption rules, or public procurement structures.

- Financing access through low-cost credit, aggregation vehicles, guarantees, or public de-risking.

- Performance assurance through equipment standards, installation oversight, and post-commissioning verification.

The policy test is simple. Can private capital trust that projected output will translate into cash flow over the life of the asset?

Capital follows standardisation

Institutional investors prefer assets that can be aggregated, underwritten, and compared across portfolios. Rooftop solar becomes easier to finance when governments standardise permitting, metering, interconnection, and contract terms. Those reforms cut transaction costs that often matter more than module prices in multi-site deployment.

This point has national significance. Apartment blocks, municipal estates, logistics facilities, schools, and small commercial roofs can function as a distributed generation fleet if policy treats them as a portfolio rather than a series of isolated consumer purchases. That shift expands the investable pipeline and improves energy security by placing generation close to demand.

This briefing offers useful context on how the investment narrative is commonly presented to wider audiences:

Public policy should crowd in, not crowd out

The strongest markets do not depend on open-ended subsidy. They use public policy to lower uncertainty, widen access to finance, and reward delivered performance. That approach attracts private capital while preserving fiscal discipline.

Policy design at the state or provincial level often determines whether rooftop solar is treated as a strategic asset or a retail add-on. Even outside a G20 framing, regional incentive structures show how investor behaviour responds to rule design. This review of 2026 Texas solar panel incentives illustrates how tax treatment, rebates, and local utility arrangements can alter project economics.

A rooftop system is financially attractive when the policy regime values what the system does, not just what it installs.

That distinction matters because installed capacity is only a deployment metric. Economic value comes from avoided grid costs, improved resilience, lower fuel exposure, and electricity delivered when the system is needed. Governments that price those outcomes correctly do more than support rooftop solar. They build a distributed infrastructure base with national strategic value.

Crafting Effective Regulatory Frameworks

The next policy frontier isn't whether governments support rooftop solar. It's whether they reward the right outcomes. Legacy incentive models often privilege raw annual generation and export volumes. That made sense in an earlier phase of market creation. It's less adequate in a system increasingly shaped by smart tariffs, batteries, and changing demand patterns.

The most telling example is roof orientation. Debate in the UK around east-west versus south-facing systems reveals a larger design flaw in many regulatory frameworks. As EnergySage's discussion of solar orientation and angle notes, east- and west-facing roofs can still perform well, direction often matters more than tilt, and cloudy conditions reduce the penalty for non-ideal angles. The deeper policy implication is that incentives must evolve to reward self-consumption and grid stability, not just raw kilowatt-hour export.

Why orientation has become a policy question

A south-facing array may maximise annual generation. But households, buildings, and local grids don't necessarily need maximum generation at midday above all else. In many systems, the greater public value comes from better alignment with demand patterns, especially when battery storage and time-of-use pricing are in play.

That changes the evaluation framework.

- Export-maximising logic rewards the highest annual output.

- System-value logic rewards generation that reduces strain at useful times.

- Consumer-value logic often sits between the two, depending on tariff design.

Governments that continue using narrow export-centred compensation may distort installation choices. They can unintentionally discourage systems that deliver stronger local balancing benefits.

Regulation must address friction as well as incentives

Compensation design matters, but so do process rules. A rooftop market slows down when planning approvals are unclear, interconnection rules vary by region, and local authorities lack standard templates. It also slows when building codes don't anticipate solar readiness for new housing or major retrofits.

A more effective framework usually contains:

- Simple permitting pathways for standard residential systems.

- Clear interconnection rules so installers and utilities apply the same logic.

- Solar-ready building requirements for suitable new construction.

- Tariff structures that reflect self-consumption, flexibility, and storage.

If policy pays only for exported units, it undervalues the rooftop systems that reduce pressure on the rest of the network.

The best regulatory design is therefore dynamic. It should begin with market formation, then mature toward system optimisation. A government that doesn't update rules as adoption rises will lock in yesterday's incentives for tomorrow's grid.

Integrating Rooftop Solar for Grid Resilience

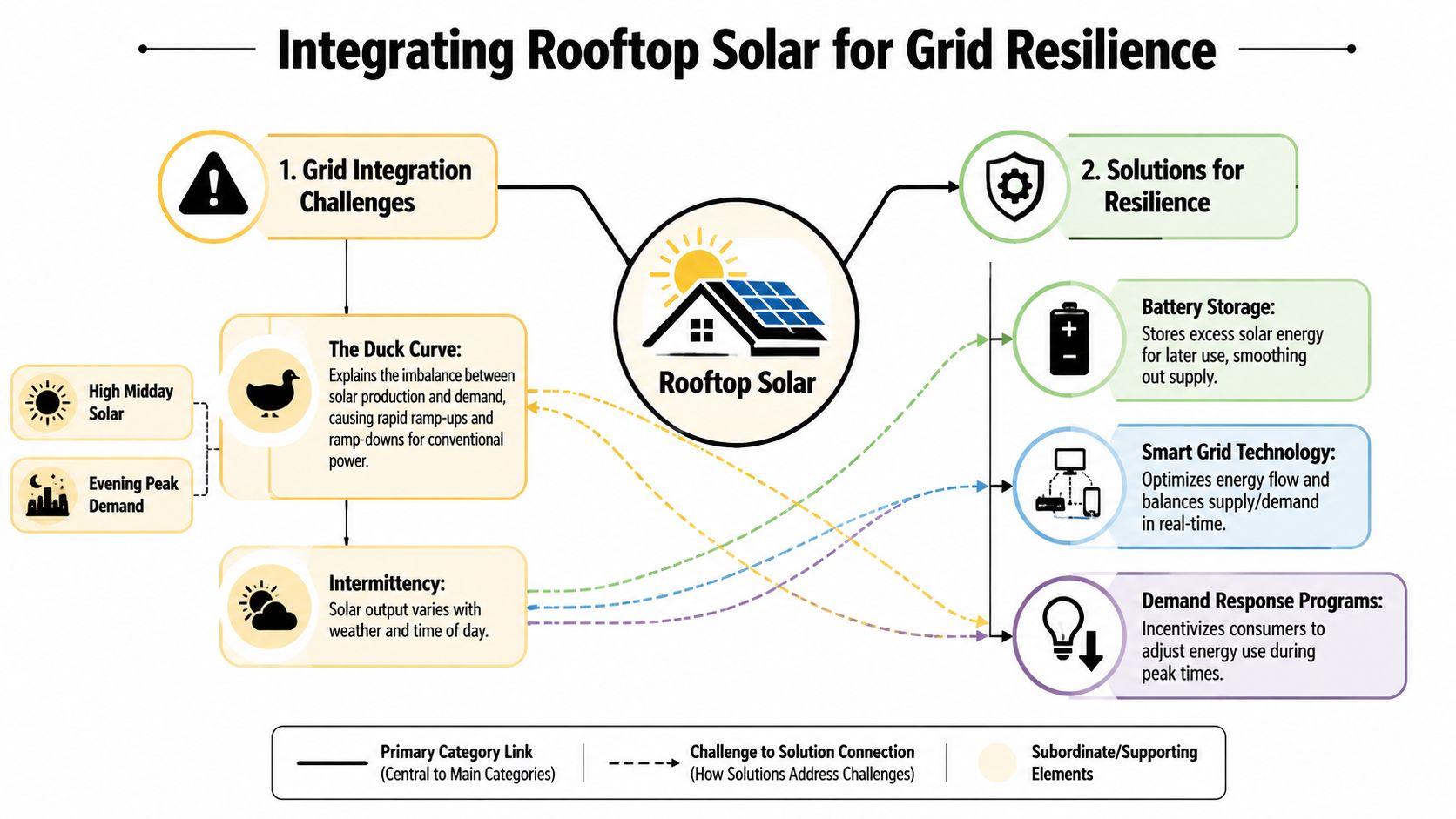

Grid operators often treat widespread rooftop solar as a management problem first. That instinct is understandable. Output varies by time of day and weather, while demand peaks often arrive when solar production has weakened. The result can be sharp operational imbalances, commonly described through the “duck curve” concept.

The important policy point, however, is that rooftop solar becomes far more valuable when paired with flexibility tools. Without them, it can intensify midday surpluses and evening ramping pressures. With them, it can support a more distributed and resilient grid.

The challenge is timing, not just volume

A country can add substantial rooftop capacity and still struggle operationally if that capacity isn't visible, controllable, or complemented by storage and demand flexibility. Integration problems usually arise from three conditions:

| Grid issue | What policymakers should ask |

|---|---|

| Midday surplus | Can excess generation be stored, shifted, or locally absorbed? |

| Evening ramp | Do tariffs and devices reduce the jump in conventional supply needs? |

| Output variability | Can system operators forecast and coordinate distributed assets effectively? |

This is why battery policy shouldn't sit in a separate silo. Storage determines whether rooftop solar acts as intermittent injection or managed flexibility.

Distributed resilience is a governance choice

A decentralised network of solar, batteries, smart inverters, and demand response can support resilience in several ways. It can reduce pressure on transmission systems, improve local balancing, and make the power system less dependent on a small number of centralised assets. None of that happens automatically. Governments have to establish the market rules and technical standards that let distributed assets participate.

Three priorities stand out:

- Visibility: Operators need better data on distributed generation and storage.

- Interoperability: Equipment should be able to respond to common control and communication requirements.

- Flexibility markets: Households and aggregators need routes to provide services, not just consume power.

For decision-makers considering the wider role of storage in power-system design, the strategic logic is well aligned with this analysis of why battery energy storage is key to a clean energy future.

Grid resilience doesn't come from adding rooftop solar alone. It comes from governing rooftop solar as part of a responsive system.

The policy mistake to avoid

Many governments still separate rooftop PV policy from network modernisation. That divide is no longer workable. A roof solar panel programme without smart metering, dynamic tariffs, storage compatibility, and utility coordination creates avoidable friction. A joined-up programme turns the same assets into resilience infrastructure.

The implication for G20 governments is straightforward. Rooftop deployment targets should be matched with grid digitisation, local flexibility procurement, and storage integration plans from the beginning.

Lessons from G7 and G20 Nations

Rooftop solar has now moved far enough in several G7 and G20 economies to yield a practical policy lesson. The central question is no longer whether distributed PV can scale. It is whether public institutions can absorb that scale without creating fiscal waste, network friction, or political backlash.

The country cases matter because each exposes a different state capacity problem. The UK shows what happens when rooftop solar reaches mainstream penetration in a mature power market. Germany shows the value of long-duration policy credibility, and the costs of leaving early support mechanisms in place after market conditions change. Australia shows how quickly distributed generation can outgrow regulatory assumptions once adoption becomes socially normal rather than policy-led.

The UK lesson is that rooftop solar becomes a system-planning issue

The UK case demonstrates a shift in category. Once rooftop deployment reaches national significance, it can no longer be managed as a marginal clean-energy programme. It starts to affect power-market operations, network investment, balancing arrangements, and the politics of cost allocation.

That is the strategic implication. A large rooftop base changes the shape of the demand-supply system itself, particularly during daylight hours and in distribution networks with uneven hosting capacity.

Germany's lesson is that credibility creates markets, but policy must evolve

Germany established an early template for market formation. The enduring lesson is not that every country should replicate the same subsidy design. It is that investors respond to rule stability, administrative clarity, and a credible expectation that policy will persist long enough for capital recovery.

That same history also shows the limits of static support. Instruments that are effective during early deployment can become fiscally inefficient or poorly targeted once costs fall and deployment accelerates. Governments that fail to adjust support structures often end up defending legacy arrangements instead of designing the next phase of market integration.

Australia's lesson is that high uptake exposes distribution-system limits quickly

Australia is instructive because rooftop solar reached mass adoption fast enough to force operational change. At that point, the policy challenge shifts from installation volume to system management. Export constraints, voltage issues, tariff reform, storage coordination, and local network visibility become immediate governance questions rather than technical footnotes.

This is the wider warning for G20 governments. Supply expansion and falling technology costs can compress the time available for institutional adaptation. Countries that wait for grid stress to appear before reforming interconnection rules, pricing structures, and data systems usually face a more expensive correction.

What these cases show collectively

The common pattern is sequential.

First, governments create a bankable market through legible rules. Second, they tighten quality control and technical compliance to protect public confidence. Third, they adapt compensation and network rules once deployment begins to alter system conditions. Fourth, they integrate rooftop solar into broader energy security and grid-planning frameworks.

Countries do not need identical sunshine, housing stock, or tariff models to learn from this sequence. They need to identify which stage they are in, and which institutional capability is missing.

Four lessons stand out:

- Policy durability matters more than short bursts of ambition. Capital formation depends on confidence that programme rules will not be repeatedly reset.

- Standards should arrive early. Weak equipment quality or inconsistent interconnection practice creates political and financial costs that are harder to reverse later.

- Integration should begin before saturation. Waiting until congestion, export disputes, or network imbalance become visible usually raises system costs.

- Distributional design matters. If the gains accrue narrowly while network costs are socialised broadly, public support weakens.

For G20 delegations, the strategic conclusion is clear. Rooftop solar should be assessed as distributed national infrastructure with private points of installation, not as a niche retail technology category. That shift in framing changes what governments measure, how regulators plan, and which ministries need to be at the table.

Actionable Policy Pathways for 2026

Rooftop solar now sits at the junction of energy security, decarbonisation, and grid modernisation. The strategic task for 2026 isn't to persuade the world that distributed solar matters. That case has already been made by scale, adoption, and system relevance. The task is to govern it deliberately.

A roof solar panel strategy should therefore be designed as a national infrastructure programme with private ownership characteristics. That requires more discipline than many governments currently apply.

Seven priorities for G20 leaders

Classify rooftop solar as strategic infrastructure

Energy ministries, finance ministries, regulators, and housing departments should stop treating rooftop PV as an isolated consumer-product file. It belongs in infrastructure planning, resilience policy, and power-system reform.Tie deployment policy to building stock reality

National targets should reflect usable roof area, housing type, and urban form. A target disconnected from roof suitability will create political overpromising and weak delivery.Mandate quality, not just volume

Technical standards for modules, inverters, and interconnection should be compulsory and enforceable. Capacity installed without dependable performance undermines trust and weakens the economics for both households and financiers.Redesign incentives around system value

Compensation frameworks should recognise self-consumption, flexibility, and local network value. Tariffs built only around exported output no longer capture the full public benefit of distributed generation.Integrate storage from the start

Battery compatibility, smart inverters, and time-sensitive price signals should be embedded in rooftop policy. Storage shouldn't be a later add-on to fix predictable balancing problems.Standardise process across jurisdictions

Permitting, interconnection, data requirements, and safety checks should be harmonised as far as possible. Fragmented local rules raise costs and slow deployment.Protect social legitimacy

Governments should ensure that renters, social housing residents, apartment dwellers, and lower-income households aren't excluded from the distributed energy transition. If rooftop solar becomes identified with unequal access, political support will erode.

What strong policy looks like in practice

Strong policy doesn't necessarily mean generous subsidy. It means coherence. A coherent framework aligns building rules, technical standards, utility obligations, tariff design, and storage policy around a common objective: turning dispersed private roofs into reliable public-value assets.

That also requires institutional honesty. Not every roof is suitable. Not every tariff is fit for the next phase of market maturity. Not every utility is ready for distributed coordination. Governments should design with those constraints in mind rather than papering over them with headline targets.

The strategic conclusion

The central insight is simple but underappreciated. Rooftop solar isn't merely a way to produce cleaner electricity. It is a way to reorganise where generation sits, who participates in the energy system, and how resilience is built into daily life. At sufficient scale, that is a statecraft issue as much as an energy issue.

G20 leaders who recognise that shift can use rooftop solar to strengthen energy sovereignty, reduce system fragility, and accelerate decarbonisation with broad public visibility. Those who don't will still get solar growth, but they'll get it in a less orderly, less equitable, and less resilient form.

The strategic opportunity for 2026 is to move from passive adoption to active governance.

Global energy policy is moving quickly, and decision-makers need analysis that connects climate ambition with practical system design. Follow Global Governance Media for policy-focused coverage on the G7, G20, energy transition, resilience, and the multilateral choices that will shape the next phase of rooftop solar deployment.