By Edward Hall

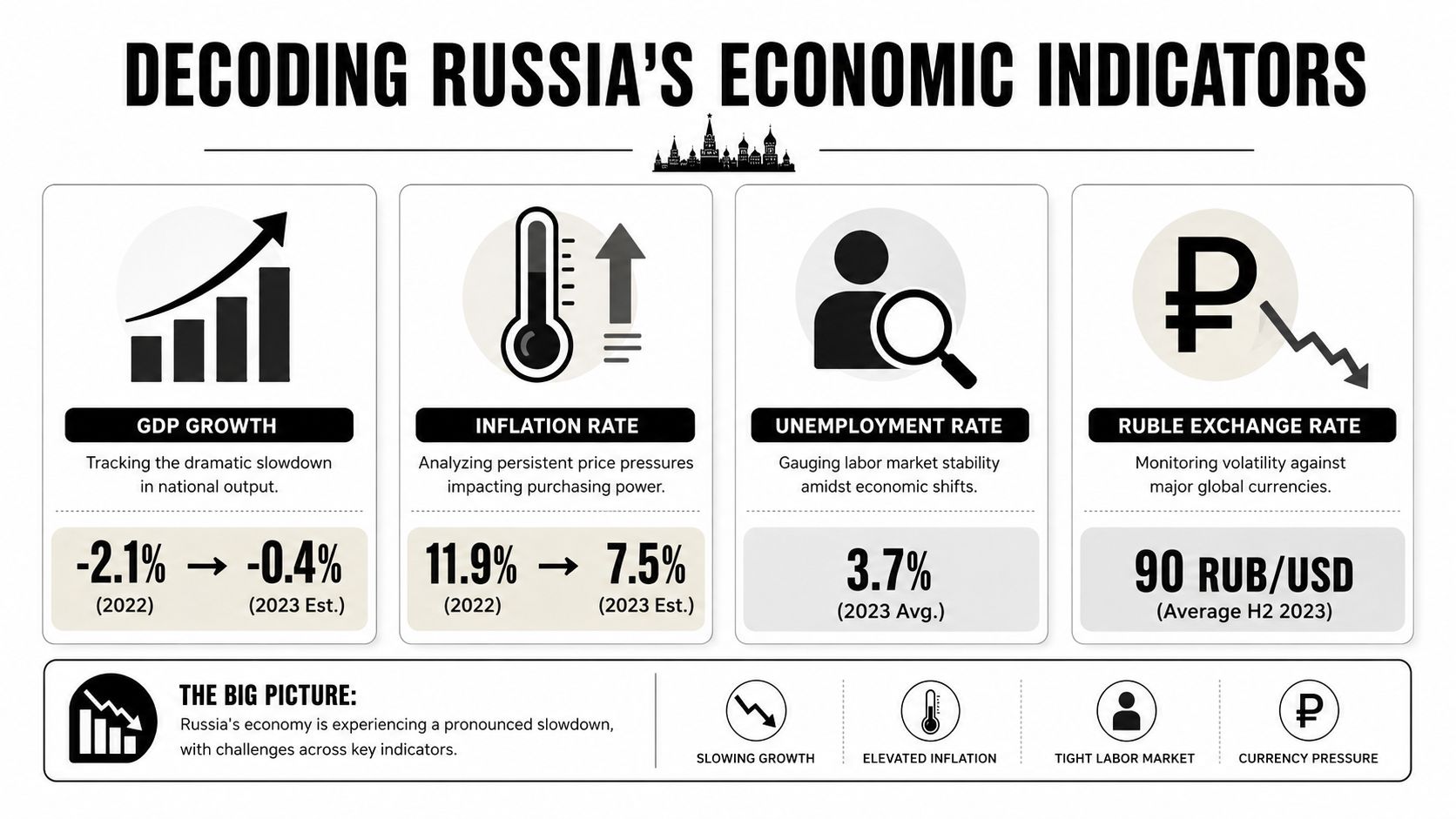

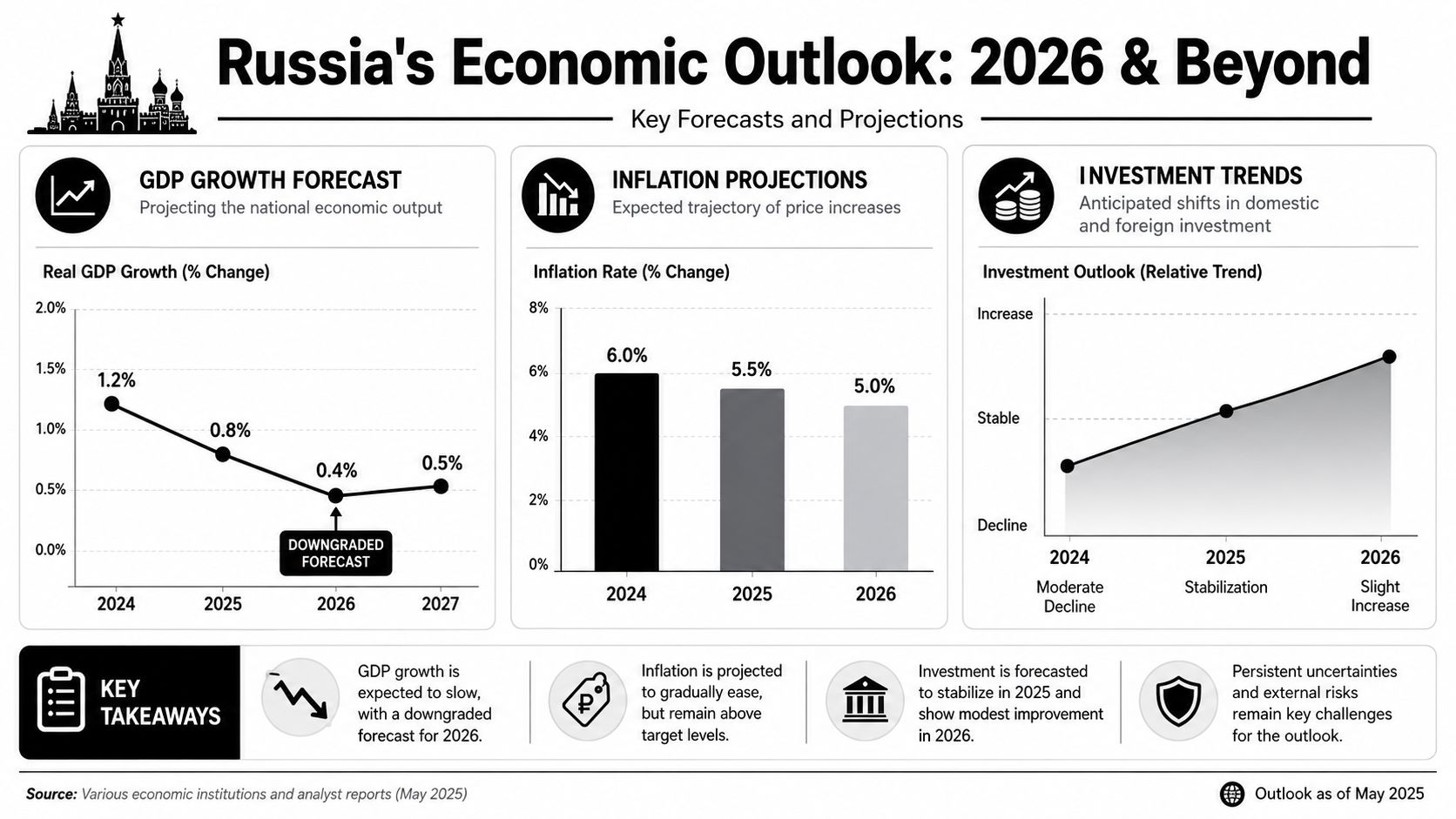

The most important fact in current Russian economy news isn't that Russia avoided collapse after the invasion of Ukraine. It's that the economy now looks materially weaker even without a dramatic external shock. Preliminary Rosstat data showed GDP growth of just 1% in 2025, down from 4.1% in both 2023 and 2024, according to BoFIT's review of the Russian economy. For G7 and G20 finance ministers, that shift changes the policy question. The issue is no longer whether Russia can stabilise under pressure. It is whether the current model can sustain military spending, price stability, and domestic political tolerance at the same time.

That distinction matters because slowdowns inside heavily managed economies are easy to misread. A state can preserve output in priority sectors for longer than many market economists expect. It can't do so indefinitely without creating inflation, fiscal strain, and misallocation. Russia now appears to be entering that phase.

What follows should be read less as a news recap and more as an operating brief for policymakers. The headline indicators matter. But the more useful task is to convert them into decisions about sanctions design, energy market management, financial surveillance, and coalition strategy.

Table of Contents

- An Economy at a Crossroads

- Decoding the Headline Economic Indicators

- The Dual Pressure of Sanctions and State Response

- Energy Exports and the Rouble's Managed Decline

- The Economic Outlook for 2026 and Beyond

- Implications for Global Governance and Markets

- Conclusion Policy Pathways for G7 Nations

An Economy at a Crossroads

Russia's economic debate has entered a different phase. The dominant question in earlier years was resilience under sanctions. The more relevant question now is endurance under tightening internal constraints. Russian economy news increasingly points to an economy that remains operational, but at significantly higher cost and with less policy flexibility.

The strategic significance lies in the mix, not any single data point. Slower growth on its own wouldn't force a policy rethink. High inflation on its own might still be manageable. Tight rates on their own could be temporary. Together, they indicate that wartime stimulus is no longer producing the same macroeconomic return and is now colliding with capacity limits, budget pressure, and central bank restraint.

Why this moment matters

For G7 and G20 officials, Russia is no longer best understood as either a collapsing sanctioned economy or a fully successful sanctions-resistant one. It is an economy caught between two policy logics.

- Military prioritisation remains central: The state still directs resources towards strategic sectors and can suppress some adjustment costs.

- Macroeconomic discipline has become unavoidable: Monetary authorities and fiscal planners can't ignore inflationary pressure and weaker revenue conditions.

- External pressure works cumulatively: Sanctions don't need to trigger immediate breakdown to be effective. They can narrow room for manoeuvre over time.

Practical rule: When a sanctioned economy still grows but loses monetary and fiscal flexibility, policymakers should shift from asking whether pressure works to asking where pressure now bites most efficiently.

That is the crossroads. Russia has demonstrated short-term adaptability. It now faces a medium-term environment in which adaptation itself is becoming more expensive.

Decoding the Headline Economic Indicators

A swing from 4.1% growth in 2024 to 1% in 2025 changes the policy question. The issue is no longer whether Russia can sustain output under sanctions. It is which constraints now bind first, and where G7 and G20 governments can raise those constraints at the lowest spillover cost.

Growth has slowed but not collapsed

The headline output data point is clear. Preliminary Rosstat reporting indicated GDP growth of 1% in 2025, after 4.1% in both 2023 and 2024, as noted earlier in the article. Separate quarterly reporting and analyst commentary also pointed to weaker momentum over the course of 2025 rather than a one-off statistical distortion.

That distinction matters for ministers. A lower annual growth rate can still mask a stable economy if the slowdown reflects normalization after an exceptional surge. Russia's pattern looks less benign. Earlier wartime expansion relied on heavy fiscal support, redirected industrial orders, and forced substitution across supply chains. By 2025, those supports were still present, yet incremental growth had weakened.

This points to an economy that can still produce output, but at rising marginal cost.

A useful cross-check is inflation behavior. Output that slows while prices remain under pressure usually indicates capacity strain, labour shortages, procurement friction, or all three at once. The broader logic is similar to the pricing mechanics described in Market Edge B2B pricing insights, where price signals often expose underlying pressure before top-line volume data fully catches up.

Inflation and interest rates reveal the primary constraint

The harder signal comes from monetary conditions. The Bank of Russia reported that inflation remained high through 2025, and policy rates stayed exceptionally high by international comparison. For a current guide to the institution's role and policy framework, see this profile of the Central Bank of the Russian Federation.

The significance is straightforward. Governments can sustain output with directed spending for longer than many forecasts assume. They have much less room once inflation becomes persistent and credit costs remain punitive. In that environment, defence production and politically protected sectors continue to receive funding, while private investment, regional balance sheets, housing, and consumer credit absorb more of the adjustment burden.

Later 2025 assessments from the Bank of Finland Institute for Emerging Economies and the IMF Article IV materials on Russia described the same broad pattern. Inflation pressure had not fully receded, and monetary policy remained tight enough to signal concern about overheating, labour scarcity, and demand running ahead of available supply.

For external policymakers, this is more than a macro snapshot. It identifies transmission channels. Measures that raise import costs for industrial inputs, limit technology substitution, or increase financing friction are more likely to bite when the central bank is already forced to keep money tight.

Why these indicators matter for ministers

The combined reading is more useful than any single indicator.

| Indicator | What it suggests | Policy relevance |

|---|---|---|

| Weaker GDP growth | Expansion is continuing, but the pace has dropped sharply | Endurance matters more than short-term resilience |

| Persistent inflation | Capacity limits and demand pressure remain misaligned | Economic stress is more likely to spread through prices and household purchasing power |

| High interest rates | Authorities still see inflation risks as serious | Additional external pressure is likely to hit non-priority sectors before protected state activity |

The strategic implication is narrow but important. Russia retains administrative capacity and can still shift resources toward priority uses. What it has less of is macroeconomic slack.

For G7 and G20 decision-makers, that changes the policy objective. The most effective measures are no longer those designed around immediate collapse scenarios. They are the ones that steadily increase fiscal, monetary, and technological trade-offs inside the Russian system.

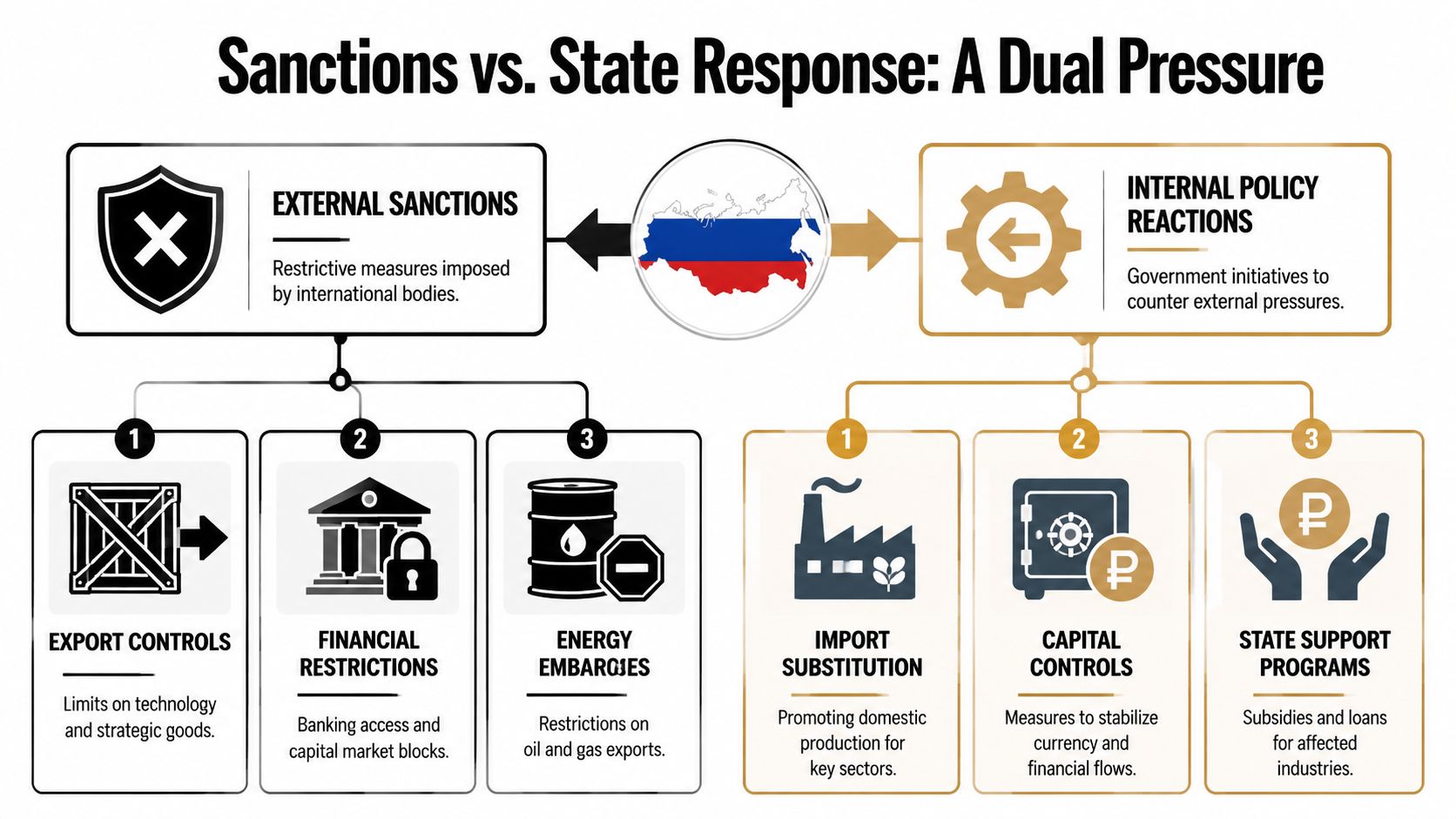

The Dual Pressure of Sanctions and State Response

The sanctions debate often gets flattened into a binary question. Did they work or not? Current Russian economy news points to a more useful answer. Sanctions have not produced abrupt economic failure. They have, however, helped create a more difficult budget arithmetic for the Russian state.

Revenue pressure is now structural

A UK-based economic analysis estimates that Russia faces a USD 25–30 billion structural revenue shortfall, driven by a roughly 25% fall in the value of Urals crude, as explained in BISI's revised economic forecasts for Russia. That matters because a structural shortfall differs from a temporary financing squeeze. It implies that the state must repeatedly make harder choices over outlays, taxation, and domestic investment.

Sanctions should be understood as cumulative rather than theatrical. Export controls, financial restrictions, and pressure on energy earnings don't need to stop all trade to alter state behaviour. They only need to reduce margin and increase friction.

For readers who want a concise conceptual primer on how these instruments work across trade, finance, and diplomacy, Model Diplomat explains economic sanctions in a way that usefully complements the macro evidence.

The state response is adaptation, not resolution

Moscow's answer has been to redistribute pressure rather than remove it. Officials can reprioritise expenditure, extract more from certain sectors, and protect strategic industries. They can also rely on the policy apparatus around the Central Bank of the Russian Federation to preserve financial stability where possible.

But adaptation has limits.

- Tax trade-offs intensify: Raising more revenue from business may support the budget, but it can depress investment incentives.

- Spending priorities harden: Resources directed to state priorities aren't available for broader productivity gains.

- Domestic demand weakens: Tight monetary conditions make it harder to offset revenue pressure through internal expansion.

The budget picture makes this sharper. GIS Reports, cited in wider 2025 analysis, pointed to a federal budget deficit forecast of 1.7% of GDP, and draft amendments put it as high as 2.6% of GDP in assessments referenced by the Atlantic Council. That doesn't signal imminent breakdown. It does signal diminishing flexibility.

What this means for sanctions strategy

The right benchmark isn't collapse. It's whether sanctions force the Kremlin to finance one objective by sacrificing another.

That benchmark now appears more relevant than before. The policy lesson for G7 states is to target bottlenecks that deepen those trade-offs, especially where revenue formation, technology access, and financing conditions intersect.

Energy Exports and the Rouble's Managed Decline

Russia's external earning capacity still turns heavily on energy. That remains true even as trade routes, buyers, and logistics have shifted. The operational question for policymakers isn't whether Russia still sells energy. It does. The sharper question is whether those exports generate the same quality of revenue, under the same level of control, and with the same stabilising effect on the wider economy. They don't appear to.

Energy still anchors the system

The state has spent the post-invasion period building workarounds. Shipments can move through less transparent commercial channels. Contracts can be restructured. Sales can be redirected to buyers outside the sanctions coalition. Insurance, transport, and payment arrangements can be adapted in ways that dilute the impact of formal restrictions.

That doesn't mean the old energy model remains intact. It means Russia has preserved export flow better than it has preserved export efficiency. Revenue quality, bargaining power, and transaction certainty matter more over time than the mere existence of trade.

A strategic reading of Russian economy news should therefore distinguish between continuity and strength. Export continuity tells us Russia can still operate. It doesn't tell us that the system is producing comfortable fiscal outcomes or restoring wider macroeconomic balance. For G7 and G20 officials working on energy governance, analysis on shaping the world's energy future through G7 G20 governance is useful because it places these trade adjustments inside a broader policy architecture rather than treating them as isolated sanctions evasion stories.

The rouble is being managed under constraint

The currency side reflects the same pattern. Russian authorities retain tools to shape financial conditions. Capital controls, interest rate policy, and administrative supervision can all influence exchange-rate behaviour and market expectations. But when a currency must be defended by heavy policy effort, that defence is itself a signal of strain.

The rouble's story is therefore less about free-market valuation than about managed adaptation. Authorities are trying to avoid the sort of disorder that would amplify import costs, worsen inflation pressure, and erode confidence. That strategy can work for a period. It also imposes costs on credit conditions, corporate planning, and private-sector flexibility.

Two policy implications follow.

First, energy and currency pressures should be analysed together. Revenue weakness affects currency management. Currency weakness feeds domestic prices. Domestic prices then compel tighter monetary policy.

Second, the more Russia relies on administrative control to smooth external shocks, the more vulnerable non-priority sectors become. In a wartime economy, the state can preserve strategic activity while letting broader efficiency decline. That is a survivable model in the short run. It is a poor foundation for renewed growth.

The Economic Outlook for 2026 and Beyond

The medium-term signal has become clearer. Russia's macro outlook for 2026 was revised down to 0.4% GDP growth from 1.3%, while inflation is still expected at 5.2% and real incomes at 1.6%, according to reporting on the downgraded 2026 forecast. That combination points to a lower-growth environment in which demand resilience is weakening faster than inflation is normalising.

A lower ceiling for growth

This downgrade matters less for the decimal point than for what it reveals about the growth model. An economy doesn't drift down to such a low forecast after several years of war mobilisation unless the earlier drivers are losing force. Financing is expensive. Revenue conditions are less favourable. Policy options are narrower.

That doesn't imply an imminent crisis. It implies a lower ceiling.

For comparative context, broader discussions of major economies by GDP analysis are useful because they highlight a core strategic point. Size alone doesn't determine influence. The composition, resilience, and financing conditions behind GDP matter just as much.

Why stagnation is the more plausible baseline

The strongest policy case is for expecting protracted stagnation rather than sudden rupture.

- High borrowing costs suppress breadth: Priority sectors may continue to receive support, but broad-based expansion becomes harder.

- Fiscal pressure reduces optionality: A tighter budget environment limits the state's ability to stimulate without worsening inflation or deficits.

- External adaptation has diminishing returns: Workarounds can preserve activity, but they rarely restore full productivity or investment confidence.

The central forecast for Russia shouldn't be collapse. It should be a prolonged period in which the state can still allocate resources forcefully, but can't generate durable, broad-based growth.

That distinction should shape G7 and G20 planning. If stagnation is the baseline, then policy should focus on limiting Russia's ability to convert partial adaptation into strategic regeneration.

Implications for Global Governance and Markets

A weaker Russian economy doesn't automatically mean a less consequential Russia. That is the central international policy mistake to avoid. States under economic strain can become more selective, more transactional, and in some domains more disruptive.

A weaker Russia can still disrupt

Russia's domestic constraints will continue to feed external behaviour in at least three ways.

First, energy market management remains a geopolitical tool even when underlying revenue conditions worsen. States facing tighter fiscal conditions often become more sensitive to price swings, logistics frictions, and buyer relationships.

Second, budget pressure can deepen economic alignment with non-Western partners on terms driven by immediate financing and market access rather than long-term efficiency. That can reshape trade patterns, sanctions enforcement gaps, and diplomatic bargaining inside multilateral forums.

Third, prolonged macro strain can encourage narrower state prioritisation. In practice, that means preserving strategically important sectors while allowing broader civilian efficiency to erode. For global markets, this creates uneven signals. Commodity influence may remain meaningful even as underlying growth momentum fades.

A wider geopolitical reading can be found in analysis of US and Russia relations, which helps place economic developments inside the broader strategic rivalry rather than treating them as standalone market data.

The G20 challenge is coordination under divergence

The practical challenge for the G20 is that members won't interpret these developments in the same way. Some will see a weakening Russia and favour tighter pressure. Others will focus on energy affordability, payment channels, and food-system spillovers. Still others will try to preserve room for diplomatic engagement while avoiding secondary economic shocks.

That divergence doesn't remove the need for coordination. It raises the premium on precise coordination.

A workable agenda for ministers should focus on areas where consensus is still possible:

- Financial transparency: Improve visibility over trade financing, routing, and sanctions circumvention networks.

- Energy market resilience: Reduce volatility exposure among vulnerable importers so that enforcement decisions don't fracture coalitions.

- Targeted diplomatic channels: Preserve communication on high-risk issues where economic confrontation could spill into broader instability.

The key insight is simple. Russia's economy may be weakening, but the international management burden is not.

Conclusion Policy Pathways for G7 Nations

A policy rate held at exceptionally high levels, alongside a widening fiscal strain noted earlier in the article, points to the same conclusion. Russia's economy is still functioning, but at a rising cost to future stability. For G7 governments, that matters less as a headline and more as an operating reality for policy design.

The priority is to convert macroeconomic stress into targeted constraints. Measures that tighten access to financing, industrial inputs, and higher-end technology are most effective when they force harder budget choices inside the Russian state, especially between military production, social spending, and currency management. The objective is not rhetorical escalation. It is to reduce Moscow's room to buffer one pressure point with another.

A second track is defensive rather than punitive. Russia has redirected trade, payments, and commodity flows through a wider set of intermediaries, which means sanctions durability now depends on the resilience of partner economies. G7 ministers should treat energy security, trade finance transparency, and support for exposed third countries as part of one enforcement architecture, not as separate files handled in isolation.

Diplomatic channels also retain a practical function. Limited engagement on financial stability, nuclear risk, food shipments, or maritime incidents can lower the odds that economic pressure produces unintended systemic shocks. Pressure works best when it is paired with clear boundaries and clear signaling.

The strategic test is discipline. Russia's constraints are real, but they do not guarantee rapid policy failure in Moscow. They create openings for sustained, selective pressure that raises the cost of adaptation over time.

For G7 decision-makers, the policy lesson is straightforward. Judge Russian economy news by whether it reveals shrinking fiscal, monetary, and external options, then build responses that turn those constraints into cumulative disadvantage.