As the 2026 French presidency seeks to revive the G7’s raison-d’être – which it sees as macroeconomic policy coordination – G7 leaders have an opportunity to do more here than they have in the recent past. History shows they did more before, suggesting that they can do it again this year.

Deliberation

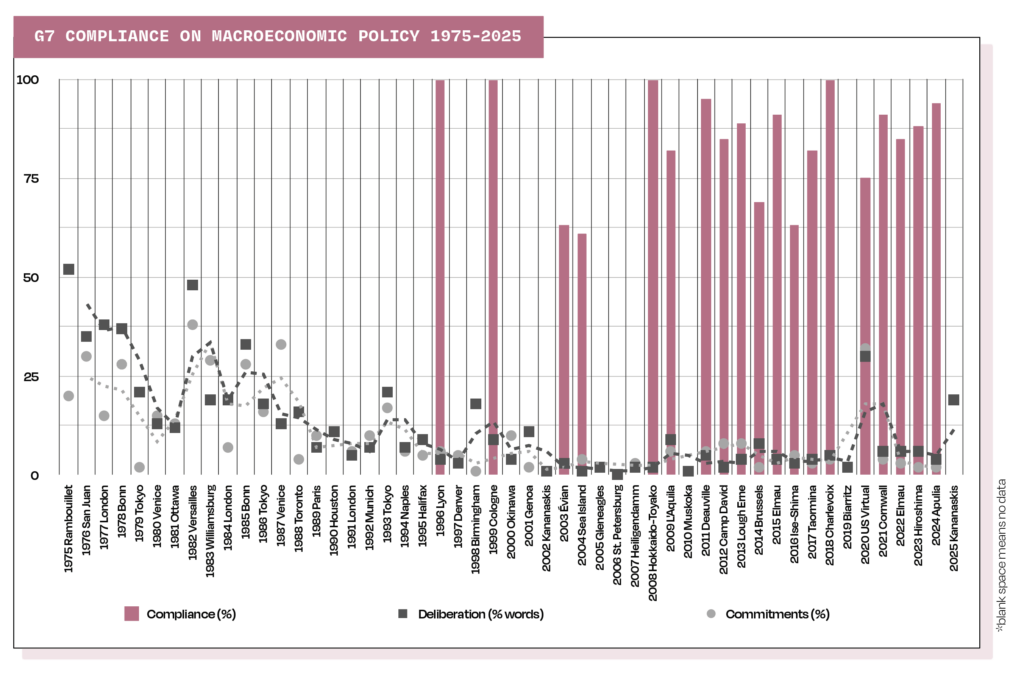

G7 summits have emphasised macroeconomic policy periodically since their start in 1975, but little since the early 2000s. In 1975, macroeconomic policy peaked at 52% of the communiqué. From 2002 to 2008, it stayed below 3%. The smallest share came at the G8 summit (with Russia) at St Petersburg in 2006, at just 0.2%. It rose to 9% in 2009, due to the 2008 global financial crisis, but then declined. It jumped to 30% in 2020 amid the Covid-19 pandemic, but dipped to 6% from 2021 to 2023. In 2024, it dropped to 4%, but rebounded to 19% in 2025.

Commitments

From 1975 to 2025, G7 leaders made 339 commitments on macroeconomic policy, for 4% of the 7,843 commitments they made overall. But there were none among the 150 they made in 2025. They also made none in 2019 and 2010. From 2014 to 2024, less than 6% of their commitments addressed macroeconomic policy, except in 2020 with 32% – from eight of the 25 commitments made then and a level not seen since 1987. The most commitments on macroeconomic policy were made in 2022, but these 19 commitments accounted for only 3% of the total. Commitments on macroeconomic policy in both 2023 and 2024 accounted for 2%.

Compliance

G7 compliance with macroeconomic policy commitments averaged a high 85%, based on the 34 assessed by the G7 Research Group. This is well above the G7’s all-subject average of 78%.

Compliance on macroeconomic policy started high, averaging 100% for 1996 and again for 1999. Commitments made in 2003 and 2004 averaged 63% and 61% compliance respectively. Compliance returned to 100% for 2008, and then remained between 82% and 95% until 2017, except for 2014 when it dipped to 69%. It returned to 100% for 2018. Compliance for 2020 was 75%, and then rose to 91% for 2021, followed by 85% for 2022, 88% for 2023 and 94% for 2024.

By member, Canada ranks first with an average of 89% compliance. France, the United States and the European Union come second with 88%. The United Kingdom follows with 86%, then Germany with 83%, Japan with 82% and Italy with 71%.

Recommendations

Compliance on commitments supporting domestic demand was generally high, reaching 100% in 1999. It was also high on ensuring macroeconomic stability – although the 2022 commitment on financial sector stability had only 57% compliance. When the G7 redirected its desire for stability to price levels in 2023, compliance soared to 100%. More generally, commitments on the financial sector had lower compliance. Putting debt-to-gross domestic product “on a sustainable path” saw compliance rise from 69% for 2014 to 88% for 2015, then dip to 63% for 2016.

Commitments on global macro-

economic policy coordination –

specifically global growth and recovery – had generally low compliance. Members averaged 78% compliance for 2013 on recovering from the global financial crisis, but only 63% on achieving strong economic growth after the Covid-19 pandemic. Similarly, the commitment to restore growth to the level anticipated before the pandemic had only 50% compliance.

Compliance with G7 macroeconomic policy commitments can be increased by holding more meetings of G7 finance ministers and central bank governors each year and committing them to report back to the leaders, and by having leaders involve the private sector, as both are associated with high compliance. G7 leaders should also make more ambitious commitments, as the 17 such commitments assessed averaged 88% compliance, compared to 81% for the others.

France’s 2026 presidency has stated that reducing global imbalances, and thus macroeconomic policy, will be the top priority at Évian. Given that the G7 has had high compliance on this issue, at évian the leaders should indeed focus on correcting global imbalances, especially by making commitments on members’ domestic demand, the reduction of the debt-to-GDP ratio and the use of education to promote growth, by mobilising their finance ministers, central bank governors and the private sector, and by making ambitious commitments overall.

However, correcting global imbalances requires action beyond the G7, so G7 leaders should act on industrial overcapacity in China, investment in developing countries and trade

tensions.