By Dr Eleanor Marsh

The most revealing fact about the koers pond euro in 2026 is not drama but restraint. As of late June 2026, the GBP/EUR exchange rate averaged approximately 1.159, within a 52-week trading range of 1.1277 to 1.1755, while the year-on-year move was only 0.99% lower, according to Wisselkoers.nl's pound exchange rate data. In a period marked by wider geopolitical and macroeconomic uncertainty, that relative steadiness says something important about the current UK-Eurozone relationship.

For policymakers, that matters more than the daily screen price. A bilateral exchange rate between two advanced European economies is a live summary of many forces at once: trade frictions, monetary policy divergence, growth expectations, institutional credibility, and political risk. When the pound moves against the euro, it often captures changes in confidence before they are fully visible in trade data or fiscal projections.

That is why the pound-euro rate deserves to be treated as an economic barometer, not merely a traveller's reference number. It shapes procurement costs, import prices, export margins, balance-sheet valuations, and the accounting treatment of cross-border obligations. It also offers a compact way to read the temperature of UK-EU relations at a time when G7 and G20 discussions increasingly connect currency resilience with supply-chain security, inflation management, and strategic autonomy.

Table of Contents

- Introduction Navigating the GBP-EUR Economic Barometer

- The Pound Euro Exchange Rate Explained

- A Historical View of the GBP to EUR Rate

- The Four Key Drivers of the Pound Euro Exchange Rate

- Implications for Policy Trade and Finance

- How to Monitor the Rate Using Reliable Data

- Conclusion Future Scenarios and Strategic Takeaways

Introduction Navigating the GBP-EUR Economic Barometer

A stable exchange rate can be as informative as a volatile one. In the current case, the pound's narrow recent band against the euro suggests that markets are not assigning an immediate crisis premium to either side of the relationship. That does not mean risk has vanished. It means risk is being processed through institutional expectations rather than panic.

For ministers, central bankers, export finance teams and international organisations, the useful question isn't whether sterling is up or down on a given day. The better question is what kind of signal the pair is sending. A stronger pound can ease imported cost pressures for the UK, but it can also erode exporter competitiveness. A firmer euro can strengthen the Eurozone's purchasing power while tightening conditions for UK sellers into continental markets.

The pound-euro pair is one of the clearest short-form indicators of how markets assess the practical state of UK-EU integration after Brexit.

This exchange rate also has unusual policy value because it sits at the junction of economics and governance. It reflects not only inflation and interest-rate expectations, but also customs arrangements, regulatory alignment, legal certainty, and the credibility of fiscal choices. In that sense, the koers pond euro is less a narrow market metric than a scoreboard for institutional trust.

A disciplined reading of the pair can therefore improve decision-making across three domains:

- Trade strategy: Firms can adjust pricing, invoicing, and market-entry timing.

- Public finance: Governments can manage cross-border accounting exposures more accurately.

- International cooperation: G7 and G20 actors can infer where UK-EU economic coordination is tightening or loosening.

The Pound Euro Exchange Rate Explained

The pound-euro exchange rate is the price of one currency expressed in the other. If sterling strengthens, one pound buys more euros. If the euro strengthens, one pound buys fewer euros. That sounds basic, but the interpretation often goes wrong because many readers compare unlike rates.

Mid-market rates and transaction rates

Think of the market as a see-saw. On one side sits demand for pounds. On the other sits demand for euros. New information, such as a policy announcement or inflation release, shifts weight from one side to the other. The see-saw moves, and the rate adjusts.

The first distinction to keep clear is between the mid-market rate and the rate a household or small firm receives. The mid-market rate is the neutral benchmark between the buy and sell price in wholesale markets. Commercial banks and payment providers then add a spread, and often fees, to produce the customer-facing rate. That difference explains why published market quotes and realised conversion costs rarely match.

A second point is mechanical but essential. In the UK's domestic currency system, one pound sterling is divisible into exactly 100 pence, which underpins all pricing and transactional calculations in currency conversion, as noted in Lynx's reference on British pound sterling. The arithmetic of exchange-rate conversion rests on that fixed subdivision even when the broader market context is complex.

Why small moves still matter

Short-term changes can look trivial on a chart and still be consequential in procurement, treasury, and trade. A procurement officer doesn't care whether a move seems visually small. They care whether it changes the local-currency cost of a contract, the value of an invoice, or the reported worth of a foreign-currency asset.

Practical rule: Use wholesale market rates to analyse direction. Use your actual executable rate to make budget decisions.

For policymakers, the key lesson is simple. Don't read the koers pond euro as a single number. Read it as a layered signal with at least three levels: wholesale benchmark, institutional execution price, and final all-in cost after spreads and fees.

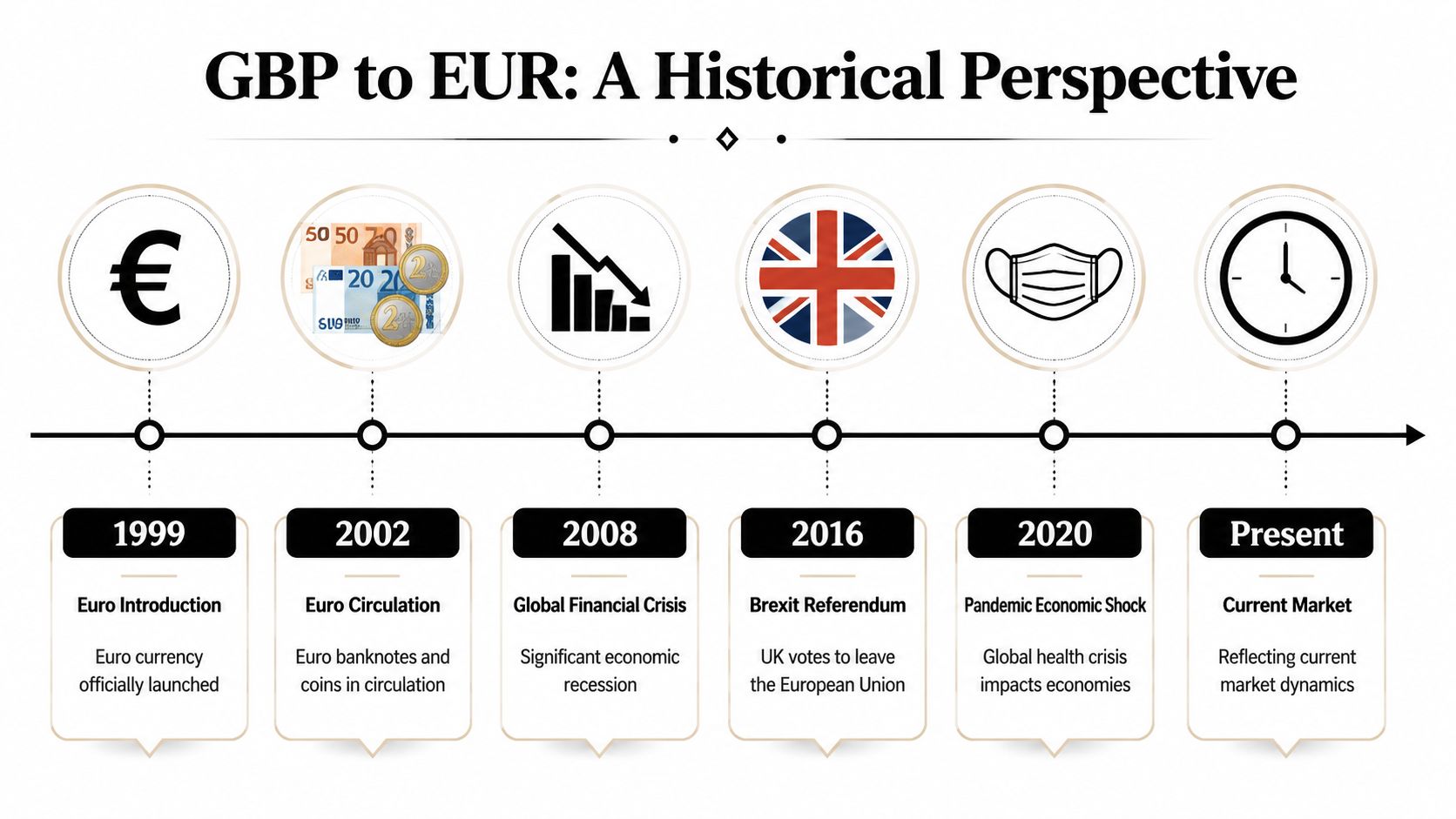

A Historical View of the GBP to EUR Rate

The long-run story of the pound against the euro begins with asymmetry. When the euro was introduced in January 1999, the initial benchmark was equivalent to 1 GBP ≈ 1.419 EUR, according to GWK Travelex's pound-to-euro historical converter. By mid-2026, that starting point implied an approximate 30% depreciation of sterling against the euro from the launch-era benchmark.

From launch premium to structural adjustment

In the early phase of the euro era, sterling retained a clear premium over the single currency. That premium reflected relative growth perceptions, institutional path dependence, and market confidence in the UK's position outside monetary union. It also reflected the fact that the euro itself was a new political and financial construct still earning credibility.

The first major break came with the global financial crisis. Sterling then behaved less like a permanently superior European currency and more like a currency exposed to financial-sector stress and external repricing. The second decisive break followed the 2016 Brexit referendum. Markets began to price not just a trade shock, but a multi-year renegotiation of the UK's economic relationship with its largest nearby market.

A useful way to read this history is not as a single trend line but as a sequence of repricing events:

- Institutional launch period: the euro's early years tested confidence in a new monetary order.

- Crisis repricing: global financial stress narrowed the perceived premium attached to sterling.

- Brexit adjustment: the pound absorbed a structural political discount tied to future market access and regulatory uncertainty.

The video below gives a broader macro backdrop to how currency relationships absorb political and financial shocks over time.

What history still tells us

The most important historical lesson is that the pair does not move only on cyclical data. It also moves on constitutional and institutional questions. Markets can process a disappointing growth release quickly. They take longer to process a change in a country's long-term economic operating model.

A pound that remains below its original euro-era premium is not merely a market story. It is a verdict on changed expectations about the UK's place in European commerce.

That matters today because many observers look at current calm and assume normality has fully returned. History suggests a more nuanced conclusion. The current rate can be stable while still embodying a durable repricing of the UK-EU relationship.

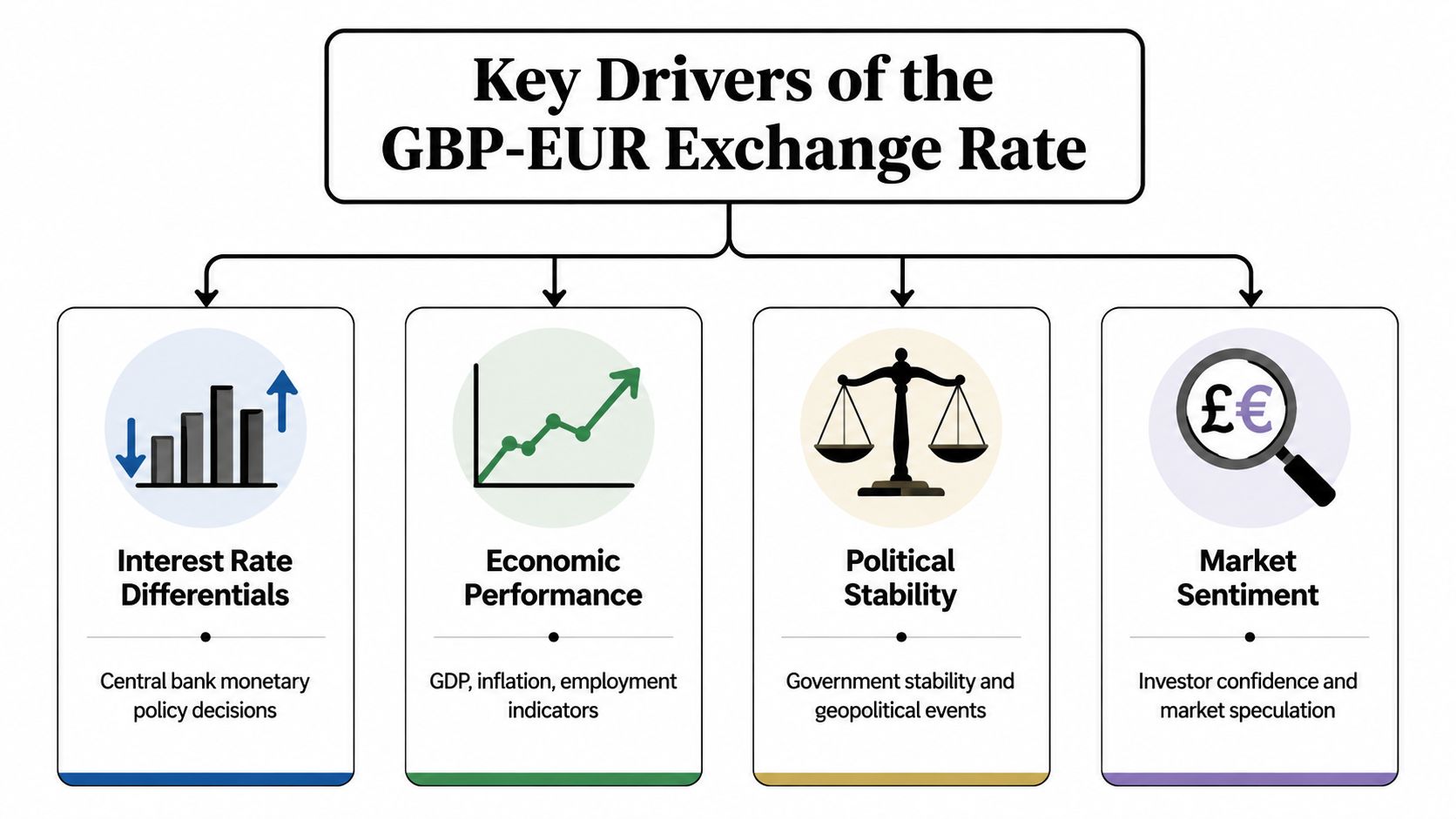

The Four Key Drivers of the Pound Euro Exchange Rate

At any given moment, the koers pond euro reflects four forces acting together. Analysts often isolate one headline cause, but that usually oversimplifies the move. Currency pricing is cumulative. Markets compare monetary paths, growth credibility, trade realities and political risk all at once.

Monetary policy divergence

Interest-rate expectations remain the fastest transmission channel into exchange rates. When investors believe the Bank of England will hold tighter policy than the European Central Bank, sterling may gain support. When they expect the ECB to look firmer or more persistent, the euro may strengthen instead.

What matters isn't only the current policy rate. Markets react to the expected path, the tone of central-bank communication, and the credibility of inflation control. Even without citing fresh numerical projections, the mechanism is clear: anticipated yield differentials alter capital allocation and, in turn, relative currency demand.

For policymakers, this creates a sequencing problem. A domestic policy stance designed to stabilise inflation can tighten financial conditions and support the currency, yet that same stronger currency can complicate export performance. Currency management is therefore never the sole objective of a central bank, but it is always one consequence of credible policy.

Economic performance

Exchange rates also price relative economic quality. Investors compare productivity, inflation persistence, labour-market resilience, consumer demand, and fiscal credibility. Stronger expected performance can support a currency because it increases confidence in returns on local assets and in the durability of public finances.

This doesn't mean one GDP release determines the pair. It means cumulative macro signals shape the narrative. If the UK looks more resilient than the Eurozone, sterling may gain. If the Eurozone looks more balanced and politically cohesive, the euro can attract support even when growth is modest.

A useful analytical test is to ask which side appears more policy-coherent. Currencies often reward coherence before they reward speed.

Trade and investment flows

Trade links create regular demand for conversion between pounds and euros. UK firms buying goods or services from the Eurozone need euros. Eurozone customers purchasing from the UK need pounds. Investment flows layer on top of that routine trade demand.

Post-Brexit arrangements matter here because they influence the friction attached to otherwise ordinary transactions. Customs administration, regulatory divergence, and legal uncertainty don't need to trigger crisis conditions to affect exchange rates. They only need to alter expected profitability, settlement risk, or foreign direct investment choices at the margin.

For readers interested in the wider institutional setting, the broader conditions that sustain confidence in cross-border markets are closely connected to the conditions for financial stability. Exchange rates sit downstream from those conditions. They don't create trust on their own. They reflect it.

Political climate and risk

Political developments can move the pair even when no hard data have changed. Elections, leadership transitions, fiscal plans, and UK-EU regulatory negotiations all affect the confidence premium attached to each currency. In practical terms, markets ask a simple question: which side looks easier to price over the medium term?

A stable political environment usually lowers the risk premium on a currency. A contested one raises it. The effect may appear before any measurable shift in trade or inflation data because foreign-exchange markets discount future uncertainty quickly.

Consider the comparative logic in brief:

| Driver | How it affects GBP/EUR | Policy relevance |

|---|---|---|

| Monetary policy | Changes expected returns on sterling and euro assets | Influences inflation control and capital flows |

| Economic performance | Shapes confidence in growth and fiscal sustainability | Alters investor and business sentiment |

| Trade and investment | Determines routine currency demand and structural attractiveness | Affects competitiveness and inward investment |

| Political risk | Adjusts the premium or discount markets assign to each jurisdiction | Changes financing conditions and planning horizons |

None of these drivers works in isolation. The strongest reading of the pair comes from watching how they reinforce or offset one another.

Implications for Policy Trade and Finance

The practical effects of pound-euro moves become clearest when viewed through the decisions real institutions have to make. Exchange rates do not stay in dealing rooms. They flow into invoices, contracts, public accounts, and board papers.

For exporters and importers

A UK exporter selling into the Eurozone faces one set of incentives when sterling is weaker and another when it is stronger. A weaker pound can improve euro-area price competitiveness if the exporter invoices in euros or converts euro revenue back into sterling. A stronger pound does the reverse, but it may reduce the local-currency cost of imported components.

An importer sees the mirror image. A firmer pound can relieve cost pressure on euro-denominated purchases. That matters in sectors where margins are thin and procurement cycles are long.

Hedging policy should follow commercial exposure, not market opinion. Firms lose money when they treat treasury as a forecasting contest.

For that reason, many treasury teams focus less on being “right” about direction and more on process discipline. Forward cover, matching currency of costs and revenues, and clearly defined risk limits all help protect trading capital when the pair moves against expectations.

For treasuries and public finance

Public-sector exposure is different because accounting standards and compliance rules often require a formal benchmark. Here the ECB reference exchange rate matters directly. On 24 June 2026, the ECB recorded 0.86165 EUR per GBP, and that benchmark serves as the official reference for accounting, tax and compliance in UK-Eurozone financial interactions, according to the ECB exchange rate portal.

That distinction is not technical trivia. A finance ministry, a local authority, or a cross-border public agency may transact at a market rate but report, value, or reconcile obligations using an official benchmark. If the operating rate and the reporting rate diverge, budget management becomes more difficult. That is especially relevant for procurement frameworks, grant administration, and reserve management.

Readers who follow the fiscal side of the UK policy debate will recognise how quickly exchange-rate shifts can feed broader questions about state capacity, debt costs and resilience, themes that also surface in analysis of whether Britain is bankrupt.

For investors and cross-border institutions

International investors care about returns after currency conversion, not before. A solid asset performance in local terms can still disappoint if the reporting currency moves unfavourably. That is why pension funds, insurers, sovereign entities and multilateral institutions usually monitor the pound-euro pair alongside the underlying asset.

Cross-border institutions also need operational clarity. They must know which rate to use for settlement, which for valuation, and which for audited reporting. Failure to separate those functions creates governance risk as much as financial risk.

How to Monitor the Rate Using Reliable Data

Good exchange-rate analysis starts with source discipline. Policymakers shouldn't rely on a single dashboard because different rates answer different questions. A wholesale benchmark helps with market interpretation. An official reference rate helps with accounting and compliance. A retail quote shows execution conditions faced by households or smaller enterprises.

Which benchmark answers which question

For institutional market monitoring, the mid-market rate is the cleanest starting point. On 24 June 2026 at 20:33 UTC, Xe reported 1.15927 EUR per 1 GBP, describing it as a mid-market rate derived from aggregated global foreign-exchange venues, as shown on Xe's GBP to EUR converter page. That benchmark is useful because it strips out the provider-specific spread and gives policymakers a neutral reference for pricing direction.

Use a simple decision rule:

- For market direction: track the mid-market rate.

- For official valuation: use the relevant reference benchmark from a central bank.

- For implementation: compare executable quotes, fees and settlement terms across providers.

The quality of the dataset matters as much as the number itself. Analysts who want a clearer framework for evaluating consistency, fields and provenance should revisit the basics of what a dataset is. Exchange-rate interpretation often fails because users treat all data outputs as interchangeable when they are not.

A disciplined monitoring routine

A sound monitoring process usually includes four habits:

- Check benchmark type first: Don't compare a consumer quote with a wholesale benchmark and call the difference “market movement”.

- Track official and market rates separately: One is for governance, the other for live pricing.

- Watch the context around the move: Rate changes need to be read alongside central-bank communication, fiscal announcements and trade developments.

- Record your use case: Treasury hedging, policy briefing, and public accounting each require a different interpretation.

Reliable currency analysis begins with an unglamorous question: what exactly is the rate on your screen designed to measure?

That question saves time, prevents reporting errors, and improves the quality of policy judgement.

Conclusion Future Scenarios and Strategic Takeaways

The near-term path for the koers pond euro is unlikely to depend on one variable alone. A plausible scenario is relative range-bound trading if UK and Eurozone policy expectations remain broadly aligned and no new political shock emerges. Another is euro strength if ECB credibility appears firmer than the UK policy mix. A third is sterling support if UK macro conditions look more coherent and politically stable than markets currently assume. These are scenarios, not current facts, and each depends on the interaction of the drivers discussed above.

The strategic conclusion is more durable than any single forecast. The pound-euro pair should be treated as a live policy indicator of the UK-EU economic relationship. It compresses questions of inflation, competitiveness, institutional trust and geopolitical positioning into a form that can be monitored daily but understood only structurally.

For senior decision-makers, the briefing note is straightforward:

- Separate benchmarks from execution: Use market rates for analysis and official rates for governance.

- Read stability carefully: A calm market can still embody a long-term structural repricing.

- Integrate currency risk into policy design: Procurement, trade promotion, debt management and industrial strategy all carry exchange-rate consequences.

- Focus on coherence: Markets tend to reward credible institutions and predictable policy paths.

- Build better analytical routines: Teams that need more systematic scenario work may benefit from tools such as PlotStudio AI for automated data analysis when comparing time-series signals across rates, policy announcements and macro releases.

The best use of exchange-rate analysis isn't prediction for its own sake. It is better statecraft and better strategic planning.

Stay ahead of summit agendas, economic risk, and cross-border policy shifts with Global Governance Media. Subscribe for summit alerts, follow the latest data-led analysis, and use the mobile app to keep critical global economic developments in view.