By Elias Rahman

What should a G20 finance ministry watch more closely in Pakistan: the State Bank of Pakistan's formal policy signals, or the frictions that determine whether those policies work beyond Karachi and Islamabad? For many external observers, the conventional answer still begins and ends with the central bank's headline functions. That's too narrow.

The State Bank of Pakistan, often searched as the Pakistan State Bank, matters internationally because Pakistan sits at the intersection of macroeconomic vulnerability, regional security, financial inclusion, and fast-moving digital finance. When the central bank tightens liquidity, manages reserves, or frames consumer protection, the consequences don't stay domestic. They affect sovereign risk assessments, development programming, correspondent banking confidence, and the credibility of global efforts to align growth, stability, and inclusion.

A descriptive overview of the bank's mandate isn't enough. The harder policy question is whether the SBP's institutional tools translate into effective outcomes on the ground. That gap, between stated policy and operational reality, is where international engagement often succeeds or fails.

Table of Contents

- The Linchpin of Pakistan's Economy

- Understanding SBP Mandate Governance and Structure

- The Monetary and Macroprudential Policy Toolkit

- Gauging Success Recent Data and Policy Actions

- Navigating the Future Banking and Fintech Regulation

- Independence Accountability and Policy Gaps

- Implications for G7 and G20 Policy Engagement

The Linchpin of Pakistan's Economy

For external policymakers, the SBP isn't just Pakistan's central bank. It's the institution that converts political ambition into monetary restraint, financial order, and market confidence. In a country where macroeconomic pressures can quickly spill into social and geopolitical risk, the quality of central banking has direct international significance.

The bank's role begins with the familiar core functions of a sovereign monetary authority. It issues notes, acts as banker to the government, regulates the financial system, and serves as lender of last resort. Those aren't ceremonial responsibilities. They define whether the state can preserve liquidity under stress, keep payment channels functioning, and prevent financial turbulence from becoming a broader crisis.

Why the SBP matters beyond Pakistan

For G7 and G20 officials, three implications stand out:

- Macroeconomic signalling: The SBP shapes how investors, multilaterals, and bilateral partners read Pakistan's policy credibility.

- Regional financial stability: Its decisions influence banking resilience and foreign exchange management in a strategically sensitive region.

- Standards alignment: The bank is a test case for how emerging-market regulators balance price stability, inclusion, and digital finance oversight.

Pakistan's central bank matters internationally not because it is unusual, but because it sits where sovereign fragility, financial modernisation, and global governance expectations collide.

That combination makes superficial analysis risky. If observers focus only on formal mandates or headline rates, they can miss where implementation weakens policy transmission. A bank can appear institutionally strong while key segments of the population remain outside effective protection or meaningful financial access.

The real analytical question

The more useful question isn't whether the Pakistan State Bank has the right mandate on paper. It's whether that mandate reaches the institutions, agents, and households through which policy becomes real. In Pakistan, that distinction is especially important in rural finance, consumer protection, and mobile money.

For that reason, any serious reading of the SBP has to combine institutional analysis with field-level scepticism. The bank's strengths are real. So are its blind spots. For international counterparts, both matter equally.

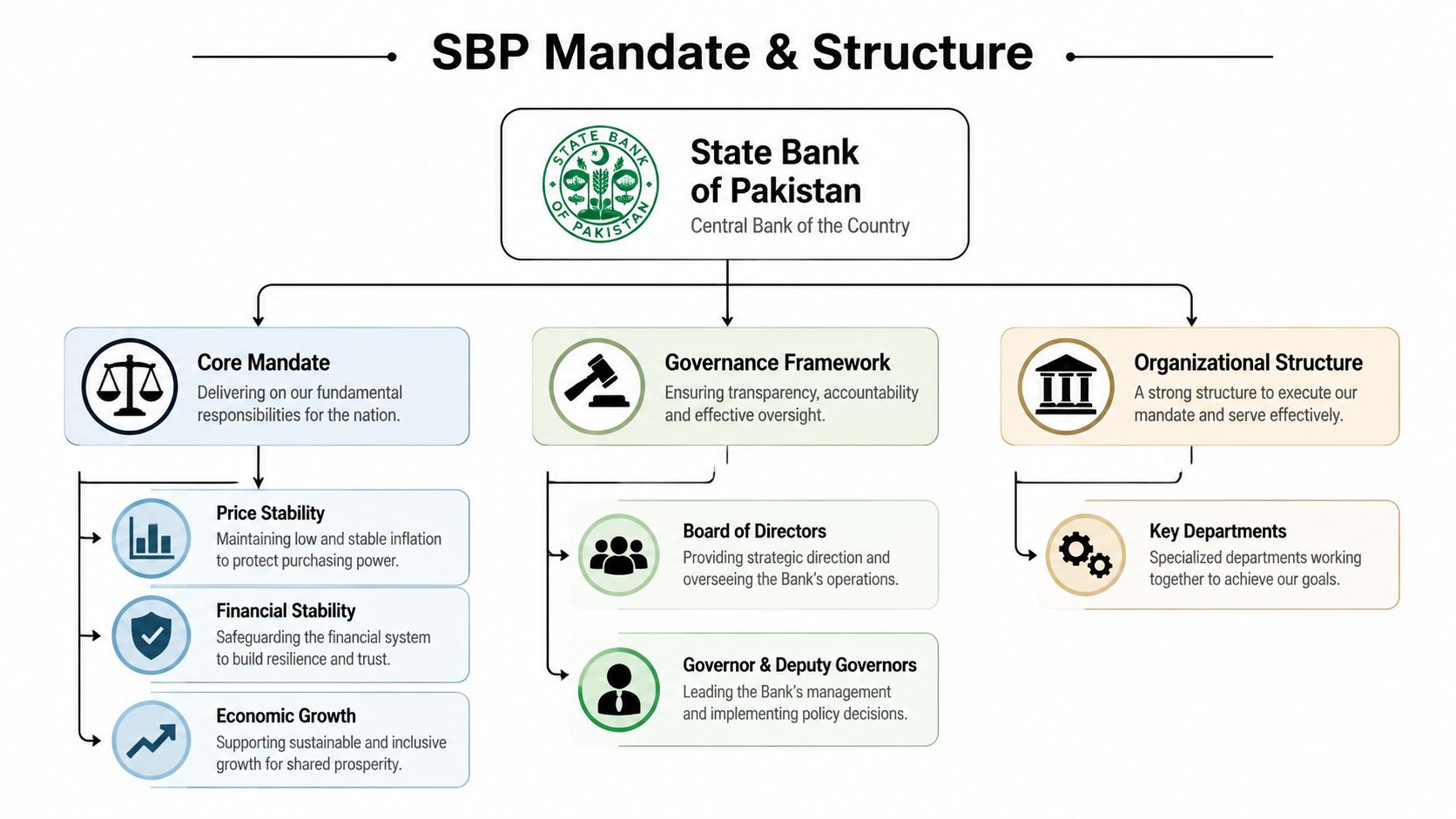

Understanding SBP Mandate Governance and Structure

The SBP's authority rests on a long state-building arc rather than a recent technocratic redesign. The bank was officially established on January 7, 1948, and its operations continue to be governed by the State Bank of Pakistan Act 1956, with implementation support from the SBP Banking Services Corporation operating through 16 offices across the country, as summarised in this institutional background on the State Bank of Pakistan.

A central bank with a public mandate

That legal architecture matters because it clarifies what the institution is for. The SBP was created as a public authority rather than a commercial enterprise. Its work is anchored in monetary management, regulatory oversight, and support for state financial operations.

A useful analogy is to think of the bank as both referee and infrastructure operator. As referee, it sets rules for monetary and financial conduct. As infrastructure operator, it helps the state's financial system function across geography and institutions. Those roles have to reinforce each other. If the rule-setting side is strong but the delivery side is weak, the formal mandate loses force.

The Banking Services Corporation is important here. Its network gives the SBP an operational reach beyond the headquarters function. For international readers comparing institutional models, that combination of central authority and distributed implementation is one reason the bank shouldn't be analysed only through policy communiqués.

Why structure matters for policy credibility

Central bank governance isn't abstract. It determines who can make difficult decisions, who can sustain them, and who is accountable when implementation falters. In the SBP's case, the governance picture combines top-level policy leadership with an operational arm capable of carrying policy through the system.

That's one reason comparative analysis matters. Readers interested in how central banks organise authority in politically sensitive environments may find it useful to contrast the SBP with other institutional models, including the Central Bank of the Russian Federation.

Institutional lesson: A central bank's legal text tells you what it may do. Its organisational structure tells you what it can do consistently.

For G20 officials, the practical takeaway is straightforward. The Pakistan State Bank should be evaluated not just as a policy issuer, but as a governance system with varying implementation capacity across the country. That distinction becomes decisive once monetary tightening, bank supervision, and financial inclusion begin to interact.

The Monetary and Macroprudential Policy Toolkit

The SBP's toolkit is conventional in form but politically consequential in effect. It uses the policy rate, open market operations, reserve requirements, and supervisory enforcement to shape inflation, liquidity, and credit conditions. What makes the toolkit more significant is the legal authority behind it.

Autonomy changed the operating model

The key institutional break came with the 1994 autonomy reform, which legally established the SBP as the sole regulatory authority and strengthened enforcement mechanisms. That framework supports the bank's primary goal of price stability, with a target inflation rate of 7.5% and a demonstrated capacity to manage money supply growth, which it decreased by 28% in 2024, according to this summary of SBP autonomy and policy tools.

That matters because autonomy isn't a slogan. It changes how policy is transmitted. A central bank with stronger legal authority can tighten conditions, discipline banks, and defend policy coherence with fewer institutional veto points. In Pakistan's case, the reform gave the SBP more than symbolic independence. It gave it a firmer operating perimeter.

How the toolkit works in practice

The logic of the toolkit can be read through three channels:

Price channel

The policy rate influences borrowing costs across the economy. When the SBP keeps policy tight, it is signalling that inflation control takes precedence over faster short-term credit expansion.Liquidity channel

Open market operations let the bank add or withdraw liquidity from the system. In this way, daily market management connects to broader macroeconomic goals.Balance-sheet discipline

Reserve requirements and supervisory authority shape how much risk the banking system can absorb and how aggressively banks can expand lending.

These instruments are standard. Their significance in Pakistan is not. In a more fragile macroeconomic setting, transmission failures are common. Administrative weakness, uneven market depth, and political pressure can all dilute the intended effect of central bank action.

Strong tools don't guarantee strong outcomes. They do, however, determine whether the central bank has a plausible route from intention to enforcement.

That's why the 1994 reform deserves attention from international partners. It created the legal conditions for a more disciplined monetary framework. But autonomy also raises the bar for accountability. Once a central bank has the authority to act, outside observers can no longer explain away weak implementation as merely a problem of formal design.

For G7 and G20 finance officials, the practical reading is this: the SBP has a recognisable macroprudential toolkit and a legal basis for using it. The more difficult question is whether those instruments still transmit effectively when they reach the political economy of digital finance, household access, and uneven financial infrastructure.

Gauging Success Recent Data and Policy Actions

Recent SBP data points suggest an institution trying to hold the line between restraint and recovery. The immediate picture isn't one of policy drift. It is one of active management under pressure.

What the indicators show

The most important current signal is the policy interest rate held at 11% as of mid-2025, a stance presented as balancing inflation control with economic growth objectives. Alongside that, foreign exchange reserves rose from $12.3 billion in 2023 to $18.7 billion in 2024, indicating improved reserve accumulation under the post-reform framework, as noted in the earlier discussion of macroprudential capacity and summarised qualitatively here.

These figures matter less as standalone numbers than as a policy combination. A high policy rate with stronger reserves suggests that the SBP has been prioritising credibility, external stability, and inflation management over near-term monetary looseness. For external ministries and lenders, that's usually a constructive signal.

A reserve build alongside policy restraint tells international partners that the central bank is trying to create room before the next shock arrives, not after it hits.

Still, analysts should exercise caution. Headline reserve gains and a firm policy rate can indicate disciplined management, but they don't prove broad-based resilience. They don't tell you whether firms face prohibitive financing conditions, whether rural financial access is usable, or whether consumer-facing digital channels are adequately supervised.

SBP Key Economic Indicators 2024-2026

| Indicator | 2024 Value | 2025 (Mid-Year) | 2026 Target/Forecast |

|---|---|---|---|

| Foreign exchange reserves | $18.7 billion | Not specified in verified data | Not specified in verified data |

| Policy interest rate | Not specified in verified data | 11% | Not specified in verified data |

| Inflation target | 7.5% target framework | Not specified in verified data | Not specified in verified data |

A separate but related implication concerns capital market confidence. Central bank credibility shapes not only inflation expectations but also how international actors evaluate domestic financing channels, sovereign risk, and market reform sequencing. That broader relationship is explored well in this analysis of capital markets development.

For G20 readers, the message is that the Pakistan State Bank currently shows evidence of active stewardship. But stewardship shouldn't be confused with full policy success. The unresolved question is whether macro-level gains are matched by institutional depth further down the financial chain.

Navigating the Future Banking and Fintech Regulation

The SBP now faces a regulatory problem that many advanced economies also recognise, but in a sharper form. Traditional bank supervision and digital inclusion can no longer be treated as separate domains. In Pakistan, they increasingly collide.

Inclusion and supervision are no longer separate questions

The standard narrative says the SBP promotes digital finance and therefore expands inclusion. That's only partly true. Digital reach can widen access while simultaneously weakening consumer protection if third-party delivery systems outpace regulatory control.

Verified analysis shows that mobile money platforms now serve 45% of the marginalised population, yet 30% of mobile money users face "biased customer service" due to unregulated third-party agents. That means the access story and the protection story are moving in opposite directions.

This is not a marginal compliance issue. It goes to the credibility of inclusive finance itself. If the user's first interaction with the formal financial system is mediated by opaque agents, poor interoperability, or discriminatory treatment, then nominal inclusion can deepen distrust rather than reduce exclusion.

The digital finance test

Three policy tensions emerge from that reality:

- Access versus enforceability: Opening channels is easier than regulating every actor who sits between the platform and the user.

- Innovation versus interoperability: Rapid product expansion can leave fragmented systems that undermine consumer mobility and transparency.

- Headline inclusion versus lived experience: Official success narratives often count entry points, not whether services are fair, reliable, and usable.

For policymakers tracking comparable debates abroad, this is why cross-jurisdictional learning matters. Discussions around central bank digital infrastructure, welfare delivery, and cross-border payment rails are evolving quickly. A useful reference point is this overview of latest digital rupee developments, which shows how digital public money debates are increasingly tied to delivery architecture, not just monetary innovation.

After the strategic framing, the operational challenge becomes clearer in practice:

Policy warning: A fintech ecosystem can look inclusive in aggregate while reproducing exclusion at the point of service.

That is the critical issue for the SBP. It isn't whether the bank supports innovation. It plainly does. The question is whether regulatory standards extend far enough into agent networks, customer service practices, and platform design to make inclusion durable.

Officials working across digital economy portfolios may also find it useful to connect this with broader debates on fintech and digital opportunities beyond finance. In Pakistan's case, the lesson is stark. Financial innovation without interoperability and enforceable consumer safeguards can widen statistical inclusion while weakening institutional legitimacy.

Independence Accountability and Policy Gaps

Central bank independence is often discussed as a legal condition. In practice, it is a chain of operational decisions that must survive political pressure, administrative weakness, and uneven implementation. The SBP's autonomy is meaningful, but it isn't self-executing.

Legal autonomy is only the first layer

A legally authorized central bank can still struggle if its metrics reward formal compliance over effective outcomes. That's the risk in Pakistan's inclusion narrative. The bank can issue frameworks, supervise institutions, and report gains, yet still miss whether users can maintain viable accounts or access services at tolerable cost.

The most revealing example is rural banking. Verified analysis indicates that 35% of rural households are banked, but 60% of these new accounts are dormant due to high costs and lack of infrastructure. That contradiction is more than a technical footnote. It shows how easily regulatory reporting can overstate resilience.

Why dormant accounts matter internationally

For G7 and G20 partners, dormant accounts should be read as an accountability problem, not just an inclusion problem. They suggest that the system may be measuring entry rather than use, compliance rather than capability, and outreach rather than resilience.

That has several implications:

- For development finance: Account opening alone isn't a reliable proxy for household financial security.

- For ESG and impact assessment: Reported inclusion gains may conceal weak service viability.

- For policy dialogue: External partners should ask how many users can transact meaningfully, not just how many have been enrolled.

Financial inclusion only strengthens resilience when people can use accounts repeatedly, affordably, and without excessive friction.

The Pakistan State Bank holds particular relevance for global governance discussions. The institution may be legally stronger than many outsiders assume. But that strength can be diluted when implementation metrics don't capture whether policy is altering behaviour in the broader economy.

For external ministries, the lesson is simple. Support for central bank capacity should be paired with tougher scrutiny of outcome quality. Legal independence is necessary. It is not sufficient.

Implications for G7 and G20 Policy Engagement

The central conclusion is that the SBP should be engaged as both a capable macroeconomic institution and an imperfect delivery regulator. Treating it as only one or the other leads to poor policy design.

For G7 and G20 governments, four priorities follow.

First, support institutional autonomy where it improves policy credibility. The SBP's legal authority and active macroeconomic management make it a serious counterpart for monetary and regulatory dialogue. International actors should reinforce that role through technical cooperation that protects policy discipline rather than substituting for it.

Second, shift from inclusion metrics to usage metrics. Rural account dormancy shows why account ownership alone is an insufficient benchmark. Development partners should favour frameworks that test affordability, repeat use, physical access, and service reliability.

Third, treat fintech supervision as a governance issue, not only an innovation agenda. Mobile money expansion among marginalised populations is important. But biased customer service and weak oversight of third-party agents show that consumer protection has to reach the operational edge of the system.

Fourth, align engagement across ministries. Pakistan's central banking questions now cut across finance, digital policy, development cooperation, and international standard-setting. Fragmented external engagement will miss how these domains interact.

The broader insight is easy to miss. The SBP's most important international significance may lie not in its formal central bank functions, but in the fact that it reveals where emerging-market financial governance is now being tested. Not at the level of high doctrine, but at the point where monetary authority meets digital delivery, inclusion rhetoric, and uneven state capacity.

G7 and G20 partners should engage the State Bank of Pakistan on that basis. Not as a static institution to be described, but as a consequential regulator whose successes and shortfalls offer a live case study in twenty-first century financial governance.

Global Governance Media helps policymakers, analysts, and institutional leaders track exactly these kinds of cross-border governance questions with sharper context and less noise. For more data-led analysis on central banks, digital finance, and G7-G20 policy coordination, explore Global Governance Media.