By Eleanor Whitmore, Senior Policy Analyst

China's latest planning cycle should change how G7 and G20 officials read economic strategy. The most revealing number isn't a trade balance or a headline growth figure. It is the target to raise core digital industries to 12.5% of GDP in the 2026 to 2030 planning cycle, alongside a target to keep annual R&D spending growth above 7% according to the World Economic Forum's summary of the new plan and the earlier Asia Society China Executive Briefing on the 14th Five-Year Plan. That combination signals something larger than industrial ambition. It shows that Beijing is trying to convert state direction into measurable technological scale.

For policymakers outside China, the 5 Year Plan China debate is often treated as a specialist topic for economists or China desks. That's too narrow. These plans are among the clearest forward indicators available for where China will direct capital, regulation, research effort, and political attention. They don't tell us everything, but they do tell us where Beijing wants bottlenecks removed, where market access may narrow, and where global competition may intensify.

That's why counterparts preparing for the next G20 cycle should read China's planning documents as strategic intelligence, not as archival ideology. For officials working on trade, climate, standards, development finance, or technology governance, the practical question isn't whether the plan will be implemented perfectly. It's how much of the world economy will need to respond to the direction it sets. For a broader multilateral context, the debate also sits alongside the wider question of how the G20 may evolve in the next cycle, as explored in this analysis of America's G20 presidency in 2026.

Table of Contents

- Introduction Decoding China's Global Blueprint

- The Architect of Modern China

- Decoding the 14th Five Year Plan 2021-2025

- From Blueprint to Reality Implementation Mechanisms

- Anticipating the 15th Five Year Plan 2026-2030

- Global Implications for G7 and G20 Nations

- Actionable Recommendations for Policymakers

Introduction Decoding China's Global Blueprint

China's Five-Year Plans have become one of the most closely watched policy documents in the world because they consolidate economic, technological, social, and security priorities into a single state framework. For foreign governments, few texts offer a clearer view of how Beijing intends to direct capital, regulation, procurement, and administrative attention over a multi-year period.

For G7 and G20 policymakers, the analytical challenge is to read the plan correctly. The contemporary 5 year plan China system functions less as a fixed production ledger than as a strategic signal to ministries, provinces, state firms, and politically important private actors. It identifies preferred sectors, channels financing, shapes local incentives, and indicates which policy outcomes will carry political weight even when headline targets are later adjusted.

The practical implication is straightforward. Treat the plan as an early warning system for state-backed market shifts.

Practical rule: Read the plan less as a forecast of exact outcomes and more as a guide to where Beijing will reduce friction for capital, talent, regulation, and procurement.

The significance for policymakers is that China's planners increasingly combine industrial objectives with resilience goals. Priorities in digital infrastructure, advanced materials, or foundational software are rarely only about growth. They also point to import substitution, supply-chain reconfiguration, export competition, and future standards-setting. Those second-order effects often shape the external environment more than the plan's headline language.

That is the policy relevance for allied capitals preparing for the next cycle of G20 coordination. A planning document drafted for domestic governance can alter trade patterns, investment screening debates, and industrial subsidy pressures well beyond China's borders. For officials considering how major economies may respond in the next multilateral cycle, this assessment of America's G20 agenda in 2026 offers a useful parallel on how national strategy translates into international economic positioning.

The Architect of Modern China

China's planning system is often misunderstood because observers use the wrong historical template. They imagine a Soviet-style command instrument and miss how the contemporary version operates. Today's Five-Year Plan is better understood as a political-economic framework that aligns ministries, provinces, state firms, and regulated private actors around common priorities.

From command plan to strategic signal

The evolution matters. Early plans focused on central allocation and heavy industry. Modern plans are broader. They still have a directive function, but they also serve as a high-level coordination device across social welfare, industrial upgrading, regional development, and technology policy.

That shift is why foreign policymakers shouldn't read the plan as a relic. They should read it as a statement of political intent backed by administrative machinery. The plan doesn't replace markets. It shapes them. It defines which technologies are strategic, which sectors deserve protection or acceleration, and which local officials will be rewarded for alignment.

For anyone studying statecraft and strategic leadership, there is a useful parallel in Silicon Valley Speakers' leadership insights. The comparison isn't ideological. It is structural. Large systems move when leadership translates vision into incentives, institutions, and measurable priorities. China's planning process does exactly that at national scale.

Why the 13th plan still matters

The 13th Five-Year Plan (2016 to 2020) remains the clearest baseline for understanding the modern system. According to the US-China Economic and Security Review Commission summary.pdf), it set a 6.5% average annual GDP growth target, aimed to raise the service sector's share of GDP from 50.5% in 2015 to 56% by 2020, and sought to increase universal social security coverage for the senior population from 82% to 90%.

Those figures show three things at once.

| Signal from the 13th plan | What it meant inside China | Why outsiders should care |

|---|---|---|

| 6.5% average annual GDP target | Growth still mattered politically | Demand conditions and policy support remained centrally managed |

| Services from 50.5% to 56% of GDP | Rebalancing away from older growth drivers | Export opportunities shifted towards higher-value goods and services |

| Senior coverage from 82% to 90% | Social policy was part of development planning | The plan functioned as a social contract, not just an industrial scheme |

The less obvious conclusion is the most important one. China's Five-Year Plans are not solely about factories, steel, or infrastructure. They are governance documents that link social stability to economic restructuring. That's why they remain predictive. If Beijing wants a transition, it rarely pursues it with industrial tools alone.

Decoding the 14th Five Year Plan 2021-2025

China entered the 14th Five-Year Plan period with C¥2.4 trillion in R&D spending in 2020, a signal that science and technology had moved to the centre of national strategy. As the Asia Society China Executive Briefing noted early in the cycle, Beijing gave innovation unusually high policy weight and linked it directly to long-term power, resilience, and growth.

That shift changed how the plan should be read abroad. The 14th plan was not merely an updated development agenda for 2021 to 2025. It was a strategic response to external pressure, slower productivity gains, climate commitments, and growing concern in Beijing that dependence on foreign technology could become a systemic vulnerability.

Innovation became the organising principle

Under the 14th plan, technology ceased to be one priority among many. It became the framework through which Beijing approached industrial policy, supply security, energy transition, and military-civil fusion.

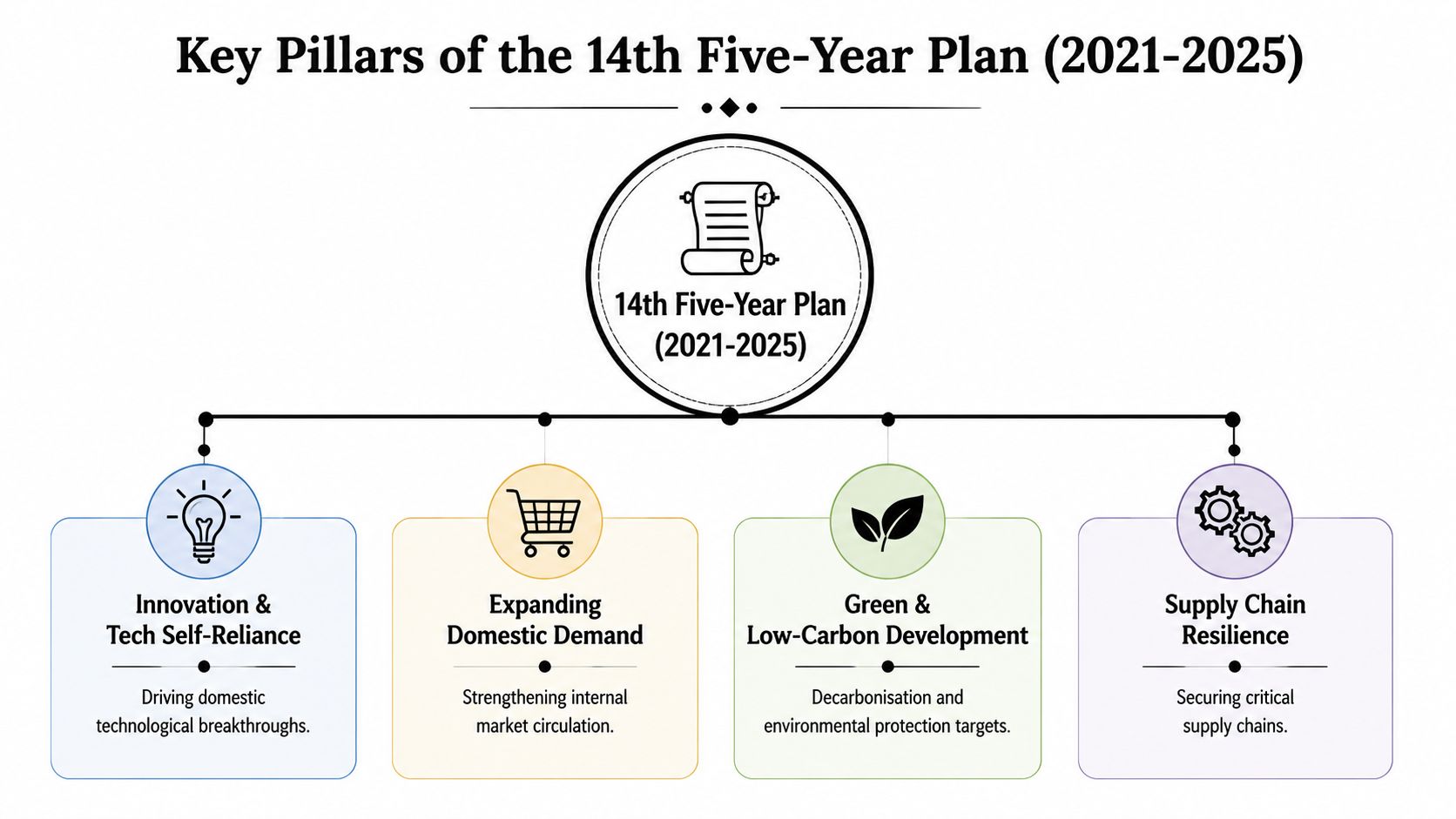

Four pillars shaped that framework:

- Innovation and technological self-reliance: Beijing treated domestic capability in critical technologies as a state priority rather than a long-term aspiration.

- Domestic demand: The "dual circulation" approach aimed to make internal demand and domestic production more resilient to external shocks.

- Green development: Decarbonisation was integrated into industrial upgrading, especially in energy, transport, and manufacturing.

- Supply-chain resilience: Economic security increasingly depended on controlling, localising, or substituting critical inputs and systems.

A short briefing video captures how these themes were framed in broader public discussion:

The significance of China's 14th plan is its fusion of economic modernisation with strategic insulation. That combination changes how other governments should interpret Chinese trade, investment, and technology policy.

The non-obvious point for G7 and G20 officials is that these pillars reinforce each other. Support for clean energy manufacturing can reduce import dependence, build export strength, absorb industrial subsidies, and improve China's bargaining position in climate diplomacy at the same time. A policy that appears environmental on paper can function as industrial competition in practice.

Why the plan changed China's external posture

For foreign policymakers, the external consequences were immediate. Once self-reliance became a development objective, trade policy, standards setting, export controls, data governance, and foreign investment screening all became instruments of the same strategy. Market access did not disappear, but it became more selective and more closely aligned with Chinese upgrading goals.

At this point, climate and technology policy begin to converge. A decarbonisation push inside a state planning system affects far more than emissions trajectories. It influences the future geography of batteries, electric vehicles, power equipment, industrial software, and grid technology. Governments that separate climate policy from industrial competition will underestimate the strategic coherence of the 14th plan.

A second-order effect is overcapacity risk. If Beijing channels capital, land, procurement, and political support into priority sectors, domestic champions can scale faster than domestic demand alone can absorb. The result is often intensified export pressure, lower global prices, and sharper trade friction. That pattern has implications for anti-subsidy policy, industrial adjustment funds, and alliance coordination across the G7.

A third effect concerns supply-chain bargaining power. China did not signal a full retreat from globalisation. It signalled an effort to restructure interdependence on safer terms from Beijing's perspective. That means counterparts should expect selective openness, especially where foreign firms can still transfer know-how, supply high-end inputs, or support Chinese production goals, and tighter constraints where domestic substitution is politically or strategically preferred.

A policy reading of the 14th plan

For ministries, regulators, and economic security teams, the practical reading is straightforward:

- Track capital allocation, procurement, and standards policy, not only headline slogans. The strongest signal is where the state concentrates support.

- Identify sectors exposed to Chinese substitution or excess capacity. Commercial dependence can erode quickly once local capability becomes a planning priority.

- Assess climate policy as industrial policy. In China's system, the two are often intertwined.

- Prepare coordinated responses early. By the time overcapacity appears in export data, the underlying state support has usually been in place for years.

The 14th plan should therefore be treated as more than a domestic planning document. For G7 and G20 governments, it is a forward indicator of where Chinese policy will reshape trade flows, technology competition, supply-chain geography, and the policy choices required in response.

From Blueprint to Reality Implementation Mechanisms

The effectiveness of China's planning system depends less on rhetoric than on implementation. The key question for outside observers is how broad strategic priorities turn into bankable projects, procurement preferences, local targets, and regulatory advantages.

How political intent becomes sectoral action

Implementation usually works through layered alignment. Central authorities set direction. Ministries interpret priorities into sectoral guidance. Provincial and local governments translate those priorities into investment plans, industrial parks, subsidy frameworks, and administrative support. State-owned enterprises often anchor major initiatives, while private firms adapt when incentives are clear enough.

That process is why the plan has predictive value even when execution varies by province or sector. A technology named as strategically important is more likely to attract supportive finance, talent programmes, and regulatory accommodation. A technology left outside the core narrative may still grow, but it won't enjoy the same policy tailwind.

For firms and governments trying to read enforcement and digital control issues around implementation, sectoral context matters. A practical primer on navigating China's internet regulations is useful because digital governance often reveals how strategic priorities are operationalised through compliance systems rather than public announcements alone.

What outsiders should monitor

Foreign ministries often focus too heavily on the national document and not enough on the cascade beneath it. Better monitoring comes from following implementation pathways.

- Provincial alignment: If multiple provinces adopt similar priorities, Beijing's signal is being translated into coordinated action.

- Procurement and standards activity: These often show where the state wants domestic capability to deepen.

- Financial channel behaviour: Preferential lending, guidance funds, and local backing indicate which priorities are becoming real projects.

- Administrative fast-tracking: Permitting, land allocation, and talent support can matter as much as direct subsidies.

A useful comparison sits in other institution-building efforts where central intent is channelled through layered governance, including regional finance initiatives such as the Asian Infrastructure Investment Bank. The lesson is similar. Formal architecture only tells part of the story. The operational centre of gravity lies in how priorities are implemented through institutions.

Operational test: Don't ask whether a plan target sounds ambitious. Ask which agencies, provinces, and firms have already begun behaving as if it is mandatory.

That question usually yields better intelligence than headline commentary.

Anticipating the 15th Five Year Plan 2026-2030

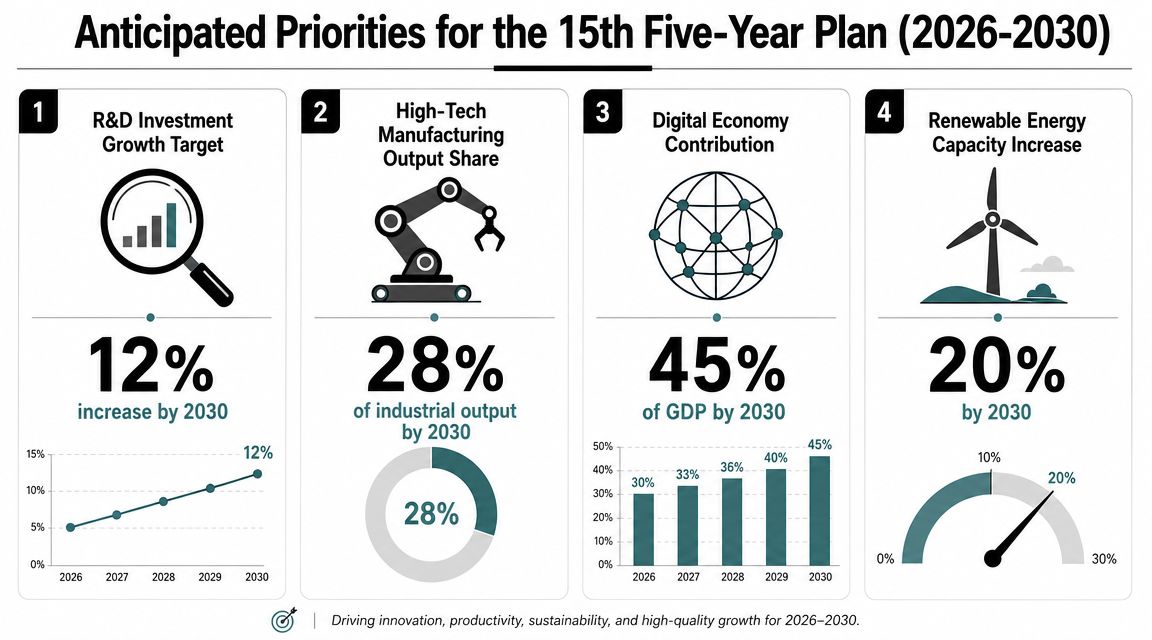

Core digital industries are expected to account for 12.5% of GDP under China's 2026 to 2030 planning framework, according to the World Economic Forum's summary of the new plan. That target matters less as a headline growth number than as a signal of policy concentration. Beijing is directing state capacity toward choke points that shape performance across multiple industries, especially where foreign technology, equipment, or software still constrains domestic firms.

The bottleneck logic

The likely structure of the 15th plan points to targeted systems engineering. The stated push for breakthroughs in integrated circuits, machine tools, foundational software, and advanced materials shows a policy method aimed at technical dependencies rather than broad sectoral expansion. This is a more disciplined approach than simple scale building. It focuses on the parts of the production system that determine whether gains in one industry can spread across the wider economy.

That distinction has strategic consequences for other major economies. A shortage or foreign restriction in one upstream node can slow progress in defence manufacturing, energy equipment, industrial automation, transport, and advanced computing at the same time. Chinese planners appear to have drawn that lesson from export controls, supply disruptions, and previous gaps between assembly strength and upstream technological control.

| Targeted bottleneck | Strategic purpose | Likely external effect |

|---|---|---|

| Integrated circuits | Reduce exposure in critical computing components | Stronger competition in mature nodes and more selective import demand in high-end segments |

| Machine tools | Improve manufacturing autonomy and precision capacity | Pressure on foreign suppliers of specialised production equipment |

| Foundational software | Cut reliance on overseas digital infrastructure and design tools | Greater standards divergence, localisation requirements, and ecosystem fragmentation |

| Advanced materials | Support aerospace, energy, electronics, and transport upgrading | New export competition in high-value industrial inputs and intermediate goods |

What this changes for G7 policymakers

The main policy implication is analytical. Exposure to China can no longer be assessed only at the level of finished sectors such as autos, chemicals, or electronics. It has to be mapped at the level of technical nodes, production equipment, design tools, and material inputs. That is where Beijing is concentrating effort, and it is where second-order effects are most likely to appear first.

Some of those effects will be indirect. If China gains ground in machine tools or foundational software, foreign firms may face weaker pricing power well before they lose share in final goods. If China reduces dependence in advanced materials, allied economies could see supply chains rerouted through third countries, changing investment patterns without an obvious trade shock in the initial stage.

The sharper question for G7 capitals is not whether China will meet every target. It is where China's chosen bottlenecks overlap with our own points of dependence, and how quickly that overlap could alter trade, investment, and industrial resilience.

That overlap will shape the next phase of competition. It will also determine where defensive trade tools are too slow, where allied coordination is still too shallow, and where domestic industrial policy needs to shift from broad sector support to narrower upstream capabilities.

Global Implications for G7 and G20 Nations

The most under-analysed consequence of China's planning system is not domestic growth. It is the global spillover from state-backed scale. The 15th plan is likely to intensify investment in advanced manufacturing and related sectors, and recent commentary highlighted by Sightline Climate argues that this may deepen industrial overcapacity and create spillovers into third markets.

Overcapacity is the second-order risk

Many explanations, however, stop short. They describe China's domestic priorities but don't ask what happens when subsidised or policy-accelerated capacity outgrows domestic absorption. The answer is that the pressure often moves outward through export channels, price competition, and standards influence.

For G7 governments, the issue isn't abstract. It affects industrial strategy, trade defence, clean-tech deployment, and political support for the energy transition. If domestic producers in strategic sectors face sustained margin pressure from policy-driven competition, governments may find that climate goals and industrial goals become harder to reconcile.

This also changes how officials should assess “rebalancing.” A Chinese shift towards domestic demand or higher-value production doesn't automatically reduce external pressure. In some sectors, it can increase it by improving the competitiveness and scale of exportable technologies.

A wider trading-system perspective is helpful here, particularly in debates about fragmentation and systemic rivalry such as this discussion of the US-China split in the world trading system. China's planning framework doesn't sit outside that story. It is one of the mechanisms driving it.

Standards and systems competition

Industrial scale also affects rule-making. When a country expands domestic capability in digital systems, advanced manufacturing, and climate-linked technologies, it gains more influence over standards, certification expectations, and commercial norms. That doesn't require overt coercion. It can happen through market weight, procurement ecosystems, and platform adoption.

Three implications follow for G20 policymakers:

- Trade policy can't be separated from industrial policy. China's plans explicitly connect technological self-reliance, security, and supply-chain resilience.

- Third markets matter. Competition may land not only in G7 home markets but in developing economies where financing, equipment packages, and standards travel together.

- Climate diplomacy is shaped by industrial structure. Cooperation remains possible, but it takes place within a sharper competitive environment.

If policymakers focus only on bilateral deficits or tariff disputes, they'll miss the more durable shift. China is using planning to shape the industrial conditions under which future trade takes place.

That is a strategic challenge, not just a commercial one.

Actionable Recommendations for Policymakers

The right response to China's planning system isn't alarmism and it isn't passivity. It is disciplined, sector-specific statecraft. G7 and G20 governments need to treat Chinese Five-Year Plans as actionable signals, then build institutions that can respond before market dislocation forces reactive policy.

A practical playbook

First, governments should build implementation tracking units that watch not only central documents but also provincial rollouts, procurement changes, standards activity, and sector-specific financing signals. The planning document sets direction. The downstream measures reveal priority intensity.

Second, policymakers should organise exposure around technology nodes rather than broad sectors. That means identifying dependencies in specialised equipment, industrial software, advanced materials, and other enabling inputs. A sectoral dashboard is no longer enough.

Third, governments should separate areas for selective cooperation from areas requiring structured de-risking. Climate engagement, public goods, and some standards dialogues still matter. At the same time, critical technologies and strategically sensitive supply chains require tighter scrutiny and domestic capability-building.

Fourth, G7 members should coordinate earlier on overcapacity indicators and third-market effects. Waiting until price pressure reaches domestic producers is too late. Shared monitoring of export surges, localisation pushes, and standards displacement would improve collective response.

Fifth, industrial policy at home should become more precise. The goal isn't to mimic China's model. It is to ensure that democratic economies can sustain competitiveness in sectors that underpin resilience, security, and the low-carbon transition.

A final point is political. China's Five-Year Plans work partly because they align bureaucratic attention over time. Democratic systems won't replicate that structure, and shouldn't try to. But they do need more continuity between trade, technology, climate, and security policy. Fragmented government remains one of Beijing's quiet advantages.

The strategic implication of the 5 Year Plan China story is therefore simple. These plans are not background reading. They are advance notice. Governments that read them closely can prepare for supply-chain shifts, market pressure, and standards competition before those dynamics harden into crises. Governments that don't will keep mistaking long-range policy signals for sudden shocks.

Global Governance Media brings together the policy analysis, expert perspectives and summit-focused coverage that decision-makers need to address issues like China's Five-Year Plans with greater clarity. If you want more evidence-based briefings on G7 and G20 strategy, trade, climate, technology governance and multilateral policy, follow Global Governance Media.