By Eleanor Vance

The most important fact in green energy investing isn’t a stock tip. It’s that the UK’s renewable energy capacity reached 51.6 GW by the end of 2024, and renewables generated 47% of UK electricity in 2024, while the sector attracted £50 billion in foreign direct investment since 2020, according to the UK Department for Energy Security and Net Zero. That changes how ministers should read green energy stocks.

These equities are not merely a market theme. They are transmission mechanisms between public policy, infrastructure deployment, pension capital, and energy security. For G20 ministers, the relevant question isn’t whether green energy stocks are fashionable. It’s whether policy design creates investable cash flows at the pace required for system transition, and whether capital markets are rewarding firms that strengthen resilience rather than merely capturing momentum.

Too much public commentary still treats the sector as a generic basket of climate-aligned companies. That misses the fundamental policy problem. A critical gap remains in assessing how UK-specific policy frameworks, particularly post-Brexit energy strategy and the windfall tax, influence valuations and investor behaviour, as noted in Morningstar’s discussion of renewable energy stocks. That gap matters well beyond the UK. Every G20 government faces the same strategic test: can it convert climate ambition into bankable returns without socialising excessive risk?

Table of Contents

- The Indispensable Role of Green Energy Stocks in Policy

- Mapping the Global Green Energy Market Landscape

- Analysing Key Policy and Subsidy Drivers

- Navigating Financial and Energy Transition Risks

- Applying ESG and Governance Assessment Frameworks

- Portfolio Construction for Institutional Investors

- An Actionable Roadmap for Mobilising Capital

The Indispensable Role of Green Energy Stocks in Policy

Green energy stocks now sit at the centre of industrial strategy. They shape the cost of capital for project developers, the credibility of government transition plans, and the willingness of large institutions to commit patient capital. When policymakers ignore equity market signals, they often misread the practical consequences of their own regulation.

That’s especially dangerous in sectors where governments need private balance sheets to fund public objectives. The state can announce auctions, targets, and climate laws. It still depends on listed developers, grid operators, infrastructure vehicles, and storage providers to turn those commitments into electricity supply, transmission stability, and investable assets.

Why ministers should treat equities as policy indicators

A listed renewable company’s valuation is a live judgement on policy credibility. If governments provide stable revenue frameworks, investors price lower policy risk into those firms. If governments change course abruptly, investors demand a higher return, and projects become harder to finance.

That makes green energy stocks useful for three distinct policy tests:

- Capital mobilisation: Do public rules attract institutional investors that need long-duration, predictable returns?

- System resilience: Are markets rewarding companies that improve dispatch, balancing, and network reliability, not just generation headlines?

- Strategic autonomy: Do domestic policy frameworks help national firms scale in ways that support energy security?

Practical rule: If a policy can’t be understood by infrastructure investors, it usually won’t deliver infrastructure at scale.

The real analytical gap

The policy conversation often stops at broad support for renewables. It rarely connects fiscal tools, auction design, tax policy, and regulatory consistency to actual valuation outcomes in listed markets. Yet that connection is precisely what ministers need to understand when they’re trying to align climate targets with pension fund allocation and sovereign investment strategy.

In that sense, green energy stocks are not peripheral to policy. They are one of the clearest market-based tests of whether policy is investable.

Mapping the Global Green Energy Market Landscape

By the end of 2024, the UK had built a renewable power base measured in tens of gigawatts and attracted substantial foreign direct investment into the sector. For ministers and institutional investors, the more important point is what that scale changes. Green energy equities can no longer be treated as a thematic corner of the market. They now sit at the intersection of electricity security, industrial policy, and long-duration capital allocation.

The first analytical mistake is to group all green energy stocks together. Listed developers, regulated network companies, storage operators, and yield-oriented infrastructure vehicles respond to different policy signals and produce different cash flow patterns. A pension fund assessing inflation-linked income is solving a different problem from a government trying to expand domestic turbine supply chains. Policy works only when those distinctions are explicit.

The UK illustrates this clearly. As noted earlier, renewables now account for a large share of power generation, renewable capacity has expanded materially, and foreign capital has followed. That combination matters because it shows a market moving from subsidy dependence toward system importance. Once a clean power segment becomes material to national supply, the investment question shifts from growth alone to resilience, balancing capability, and political durability.

What the UK example implies for capital allocation

Three conclusions follow.

First, listed green energy companies should be read by ministers as part of market structure, not just climate signalling. Companies such as Ørsted and SSE connect planning systems, grid access, procurement cycles, and wholesale power markets to real-world delivery. Their valuations reflect how credible those policy conditions appear over the life of an asset, not merely investor enthusiasm for decarbonisation.

Second, foreign and domestic institutional capital do not enter all segments at the same pace. Utility-scale generation can attract large pools of capital once revenue visibility improves. Grid reinforcement, storage, and flexibility often need a clearer regulatory route before capital scales with similar confidence. This creates a policy sequencing issue. Governments that accelerate generation without equal attention to networks and balancing can produce an investable headline and an unstable system.

Third, market composition matters for energy security. A country with many listed clean generation names but weak domestic exposure to grids, storage, power equipment, or system services may still face strategic dependence. For a broader policy context, Global Governance Media's analysis of the global energy transition is useful because it places equity markets within a wider contest over supply chains, infrastructure control, and industrial competitiveness.

Why market structure matters more than sector labels

The phrase "green energy stocks" hides the segmentation that drives both valuation and policy effectiveness:

- Generation developers: Companies exposed to permitting, construction timetables, equipment costs, and power market design.

- Infrastructure vehicles: Businesses centred on operating assets and cash distribution, often better aligned with pension funds and insurers seeking predictable income.

- Grid and flexibility platforms: Firms that benefit as higher renewable penetration increases demand for transmission upgrades, storage, balancing, and demand response.

- Emerging transition technologies: Areas such as hydrogen or advanced storage, where policy ambition often runs ahead of commercial maturity.

This segmentation produces a practical framework for decision-makers. If the policy goal is rapid capacity deployment, ministers should assess whether listed developers can secure equipment, permits, and grid connections at acceptable cost. If the goal is to mobilise pension and sovereign capital, the relevant universe is more likely to include infrastructure vehicles and regulated network exposures. If the goal is strategic autonomy, policymakers should ask whether domestic equity markets give investors access to the parts of the value chain that improve system control, rather than only generation growth.

A generic renewable equity screen cannot answer those questions. Market structure can.

Analysing Key Policy and Subsidy Drivers

For institutional capital, the decisive question is rarely whether governments support clean power in principle. It’s whether governments provide a mechanism that turns volatile wholesale markets into sufficiently stable long-term revenues. The UK’s Contracts for Difference (CfD) scheme remains one of the clearest examples of how policy can do that at scale.

Since 2014, the scheme has allocated £14.5 billion in revenue support, catalysed a 162% rise in renewable capacity, delivered 12-15% average annual returns for stocks like Greencoat UK Wind, and de-risked £30 billion in private investment by 2025, according to the UK government’s Contracts for Difference collection.

Why CfDs changed the investment case

The strength of the CfD model lies in its simplicity from an investor’s perspective. It reduces exposure to extreme price swings by providing a clearer revenue framework. That doesn’t eliminate project risk, but it changes the financing conversation. Banks, insurers, pension funds, and public markets can underwrite assets with far greater confidence when policy gives them a better view of cash flow.

For ministers, the lesson is broader than one British programme. Effective subsidy design doesn’t mean subsidising everything. It means targeting the point of greatest financing friction. In many renewable markets, that friction is revenue uncertainty, not lack of engineering capability.

A well-designed support mechanism usually delivers four policy benefits at once:

- Lower financing risk for developers and listed companies.

- Better auction discipline than open-ended subsidy promises.

- Clearer price discovery for government and investors.

- Higher institutional participation because liabilities can be matched against more predictable income streams.

Comparison of key policy support mechanisms for renewables

| Mechanism | Investor Certainty | Cost to Government | Market Efficiency Impact | Primary Beneficiary Sector |

|---|---|---|---|---|

| Contracts for Difference | High where auction design is credible | Direct revenue support commitment | Strong when competitive allocation is maintained | Capital-intensive generation, especially large-scale wind and similar assets |

| Tax credits | Moderate, depends on tax capacity and policy continuity | Fiscal expenditure through tax system | Can be efficient, but less uniform across investor types | Developers and investors with usable tax appetite |

| Renewable portfolio standards | Variable, depends on enforcement and certificate market design | More indirect than direct subsidy | Mixed, often depends on market liquidity and compliance quality | Broad generation market, especially where certificate trading is mature |

The strategic implication is that governments shouldn’t ask which mechanism is ideologically preferable. They should ask which mechanism best addresses the specific risk premium blocking capital formation.

Policy test: If support lowers risk but weakens competitive discipline, the state may end up paying too much. If it preserves competition but leaves revenues too uncertain, private capital stays on the sidelines.

For a wider multilateral lens on how policy design can support climate delivery, this G20 climate action analysis is a useful companion.

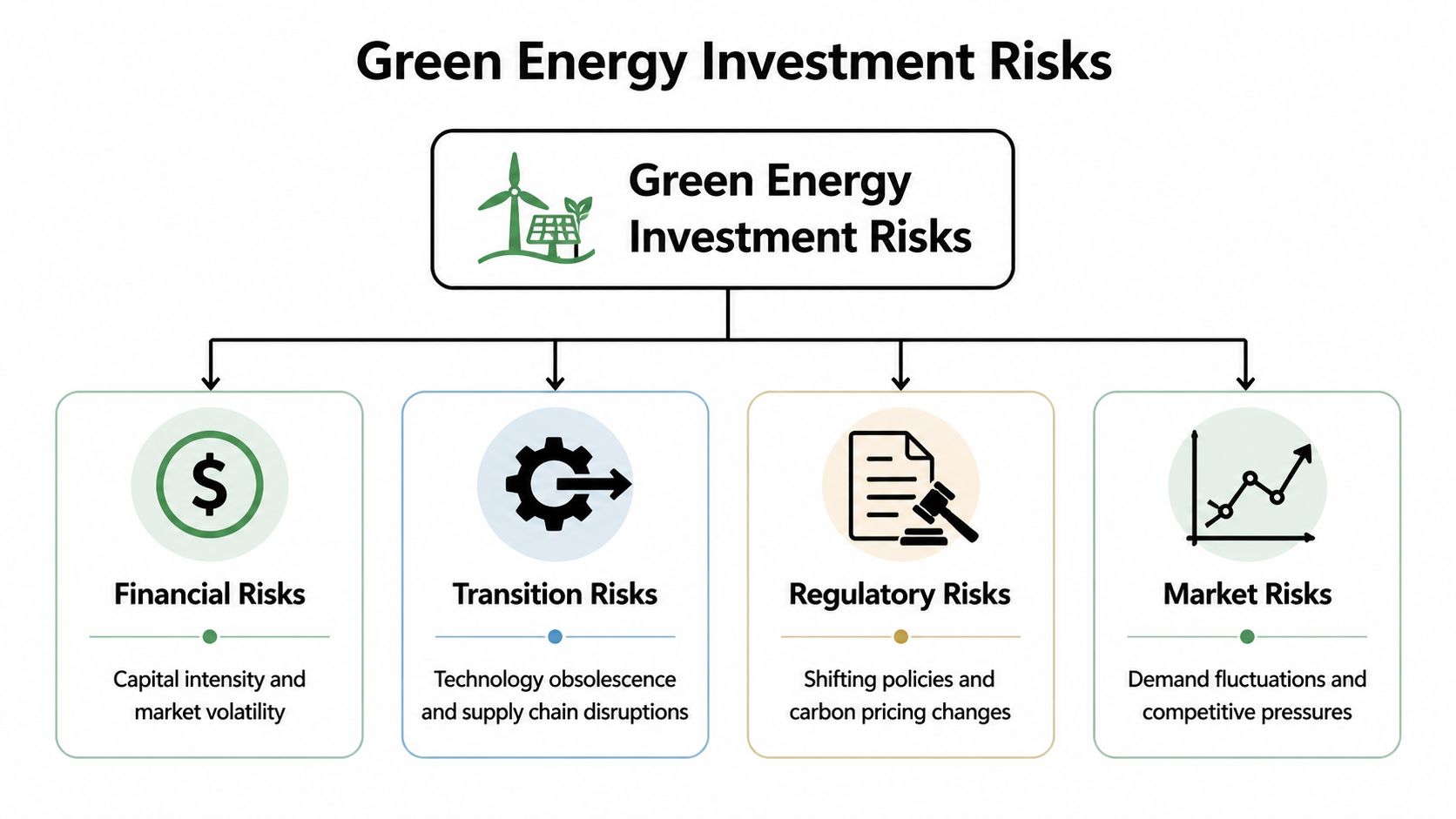

Navigating Financial and Energy Transition Risks

Renewables attract capital because operating costs are low and long-term demand is backed by decarbonisation policy. Yet the listed equities tied to that buildout can remain highly volatile. The reason is straightforward. Energy transition assets reduce fuel-price exposure, but they increase dependence on interest rates, grid access, permitting discipline, and policy continuity.

For ministers and institutional investors, this changes the risk question. The issue is not whether green energy stocks are aligned with the transition. The issue is which risks belong on private balance sheets, which should be reduced through market design, and which signal that capital is being directed into the wrong part of the power system.

Three pressures matter most.

First, green infrastructure is capital-intensive. Valuations are therefore unusually sensitive to the cost of debt, refinancing conditions, and the credibility of future cash flows. A company can have strong demand prospects and still underperform if higher rates compress project economics or delay final investment decisions.

Second, system integration risk is rising. New wind and solar capacity does not automatically translate into a more resilient electricity system. Without transmission upgrades, flexible demand, storage, and clearer dispatch incentives, additional generation can increase curtailment, depress captured power prices, and weaken returns across the value chain.

Third, transition policy can create as much dispersion as technology itself. Stable auction regimes, predictable tax treatment, and credible planning rules lower the cost of capital. Abrupt redesigns do the opposite. For listed companies, that means country exposure often matters as much as technology exposure.

A useful framework separates four distinct risk channels rather than treating the sector as a single thematic allocation:

- Financial risk: higher funding costs, refinancing pressure, covenant strain, and sensitivity to discount-rate changes

- Transition risk: technology substitution, changing equipment standards, supply chain concentration, and input-cost volatility

- Regulatory risk: auction redesign, permitting delays, tariff changes, market reform, and weaker policy credibility

- Market risk: power-price movements, cannibalisation in saturated renewables markets, demand uncertainty, and competitive margin compression

This distinction has portfolio consequences. An investor may appear diversified across several green energy stocks while still holding the same underlying exposure to one policy regime, one equipment bottleneck, or one wholesale market structure.

Storage illustrates the point clearly.

Battery assets are often analysed as a stand-alone clean technology theme. In practice, they function as a system stabilisation tool. Where policymakers compensate flexibility, storage can reduce curtailment, support frequency response, and improve the revenue quality of adjacent wind and solar assets. Where regulation rewards megawatt-hours of generation but undervalues balancing capacity, the system becomes harder to finance and harder to defend politically.

That leads to a less obvious conclusion. Some green energy stocks should be assessed less like pure growth equities and more like regulated infrastructure proxies whose performance depends on whether public policy closes system gaps in time. Companies exposed to transmission, balancing services, grid equipment, and storage may therefore offer a different risk profile from developers whose earnings depend mainly on continuous additions of new renewable capacity.

For public authorities, the policy test is practical. If market rules favour capacity additions without securing flexibility, transmission, and connection reform, the result is not only technical inefficiency. It is a higher equity risk premium across the transition chain. If governments align generation support with flexibility and grid investment, they improve both energy security and the investability of the sector.

Institutional allocators should respond in the same structured way. Stress-test holdings against rate sensitivity, curtailment exposure, merchant-price dependence, supply chain concentration, and jurisdiction-specific policy risk. That approach does more than protect portfolios. It identifies where public intervention can lower system-wide financing costs without shielding weak business models.

Applying ESG and Governance Assessment Frameworks

Many investors stop at the environmental label. That isn’t enough. A company can develop renewable assets and still perform poorly on governance, labour standards, procurement integrity, or community consent. For public institutions and long-horizon investors, those weaknesses are not secondary issues. They are indicators of execution risk and legitimacy risk.

Look past the environmental label

A thorough ESG assessment of green energy stocks should start with the social and governance dimensions that are easiest to overlook.

- Supply chain discipline: Investors should ask how management oversees procurement, contractor conduct, and labour standards across manufacturing and construction.

- Community licence: Developers that handle consultation poorly can face delay, litigation, and reputational damage even when the asset itself supports decarbonisation.

- Political conduct: A board’s lobbying positions should be consistent with the company’s stated transition strategy. Mixed signals usually indicate a governance problem.

- Executive incentives: Pay structures should reward operational delivery, safety, and long-term transition performance, not only short-term market movements.

A governance screen for policymakers and allocators

For ministers shaping public finance rules, and for sovereign or pension allocators, a practical governance screen can be built around a few recurring questions:

- Does the board have the technical competence to oversee project execution, grid issues, and regulatory engagement?

- Are capital allocation decisions consistent with the company’s stated transition identity?

- Does management disclose policy dependencies clearly, or does it rely on vague sustainability language?

- Are community and supply chain controversies treated as strategic risks or merely communications issues?

Good governance in green energy is not decorative. It determines whether public support turns into durable public value.

This matters especially where governments are trying to attract private co-investment. If public money or policy support is helping create investable returns, citizens and counterparties will expect stronger standards than those applied to a purely speculative growth sector.

Portfolio Construction for Institutional Investors

Institutional investors need a portfolio architecture that reflects how the energy system is financed, regulated, and operated. Pension funds, insurers, sovereign wealth funds, and public development institutions are not selecting a handful of thematic winners. They are allocating capital against long-dated liabilities, policy uncertainty, and rising pressure to support energy security as well as decarbonisation.

That changes the investment question. The issue is not merely whether green energy equities offer growth. It is whether a portfolio can withstand shifts in subsidy design, interest rates, grid constraints, and supply chain bottlenecks without becoming a concentrated bet on one policy regime or one technology cycle.

Correlation often hides behind thematic labels

Green energy portfolios can look diversified by company count while remaining highly correlated in practice. Several concentrations tend to build at once.

- Technology concentration: heavy exposure to one segment, such as solar equipment or offshore wind development, ties returns to a narrow set of cost, permitting, and execution assumptions.

- Jurisdiction concentration: assets clustered in one market remain exposed to the same auction rules, tax credits, curtailment risks, and political cycle.

- Revenue model concentration: companies dependent on similar support structures often reprice together when governments revise subsidy frameworks or power market rules.

- Capital cycle concentration: businesses with similar financing needs are all vulnerable when higher rates or tighter credit conditions raise the cost of capital.

A resilient allocation spreads exposure across functions in the power system, not only across tickers.

For institutional capital, that usually means distinguishing between companies that build generation capacity, firms linked to transmission and grid equipment, storage and flexibility providers, and infrastructure-style vehicles with more visible cash flow characteristics. These segments respond differently to policy and market stress. A ministry designing support mechanisms should care about the same distinction, because a narrow investable universe limits private co-investment and raises the risk that public incentives fuel crowding rather than breadth.

Build portfolios around system roles

A practical framework is to group holdings by the role they play in the transition economy.

- Core exposure: businesses tied to established renewable generation and contracted or regulated revenue structures.

- System balancing exposure: firms linked to storage, demand management, grid modernisation, or other flexibility services that become more valuable as intermittent generation rises.

- Selective innovation exposure: smaller allocations to emerging transition themes where policy support is credible but commercial scaling risk remains higher.

- Cross-border diversification: exposure across multiple regulatory systems to reduce dependence on a single fiscal regime or election cycle.

This approach produces a better match between investment design and public policy goals. It gives allocators a way to participate in decarbonisation without relying on one political promise. It also gives governments a clearer test of whether their market design is investable at scale. Broader context on that public-private alignment appears in this analysis of financing the green global economy.

The video below gives a broader visual perspective on how investors are thinking about clean energy allocation.

The policy implication is straightforward. If governments want large institutional allocations, they must support a market structure that offers investable breadth across generation, networks, storage, and enabling technologies. If they do not, portfolios will remain concentrated, correlations will rise under stress, and the cost of capital for the transition will stay unnecessarily high.

An Actionable Roadmap for Mobilising Capital

The evidence points to a clear conclusion. Governments don’t mobilise capital at scale by announcing targets alone. They do it by reducing the mismatch between public ambition and private risk. Green energy stocks reveal whether that mismatch is narrowing or widening.

What ministers should do now

A credible roadmap for G20 governments should focus on five practical moves.

- Protect revenue visibility: Auction and support systems should give investors a clearer basis for underwriting long-lived assets.

- Value flexibility properly: Markets need investable pathways for storage, balancing, and grid support, not only generation.

- Reduce policy noise: Abrupt fiscal or regulatory shifts increase the cost of capital even when long-term strategy remains unchanged.

- Improve investable breadth: A stronger pipeline across generation, networks, and storage helps institutional investors diversify rather than crowd into a narrow subset of names.

- Raise governance expectations: Public policy should favour firms capable of meeting higher standards on disclosure, procurement, and social legitimacy.

For readers tracking the wider economic side of the transition, this analysis of financing the green global economy adds useful context on how public and private capital can be aligned more effectively.

The core policy principle

The most important strategic insight is that policymakers and capital allocators should stop treating green energy stocks as a downstream consequence of the transition. They are part of the transition architecture itself. Equity performance, valuation stability, and investable cash flows shape whether the next round of infrastructure gets built, how cheaply it is financed, and whether citizens experience the transition as secure and orderly.

If ministers want faster deployment, they need investable regulation. If they want lower financing costs, they need credibility across electoral cycles. If they want system resilience, they must support flexibility alongside generation. Those choices determine whether green energy stocks become instruments of national strength or merely cyclical market stories.

Global Governance Media brings policymakers, investors and institutional leaders closer to the decisions shaping climate, energy and the global economy. Explore more analysis, briefings and summit-focused insights at Global Governance Media.