By Daniel Mercer

Is National Commercial Bank Saudi still a bank you can analyse on a standalone basis, or is that now the wrong question? For UK policymakers, investors, and corporate risk teams, that distinction matters more than the legacy brand suggests. A great deal of commentary still treats NCB as though it remains a separate operating identity. In practical terms, that can lead to the wrong counterparty assessment, the wrong governance assumptions, and the wrong view of how Saudi financial policy is transmitted into the economy.

The more useful lens is this: National Commercial Bank is now best understood as a legacy institution within the present-day Saudi National Bank framework. That shift changes how external stakeholders should read the bank's strategic role. It is no longer just a story about the Kingdom's oldest licensed bank. It is a story about scale, merger-driven concentration, sovereign linkage, and policy execution in a system where banking institutions can also function as instruments of national transformation.

Table of Contents

- Understanding the Legacy of National Commercial Bank

- A Timeline From NCB's Founding to the SNB Merger

- SNB's Post-Merger Governance and Operations

- Analysing SNB's Financials and Market Position

- Geopolitical Considerations and Regulatory Oversight

- SNB as an Instrument of Vision 2030 and Sustainability

- Key Takeaways and Avenues for Engagement

Understanding the Legacy of National Commercial Bank

Why does the old NCB name still appear in due diligence notes, archived contracts, and policy commentary if the institution now operates as Saudi National Bank? For UK policymakers and investors, the answer is more than a branding point. It affects counterparty identification, ownership analysis, and how Saudi banking links to state priorities under Vision 2030.

Much of the public material still refers to National Commercial Bank under its historic identity, while the current institution is Saudi National Bank, or SNB, following the merger with Samba Financial Group, as noted in the Saudi National Bank background summary. That distinction matters because legacy references can obscure the fact that the relevant counterparty today is a larger, more systemically important bank with a different governance and risk profile than the pre-merger NCB.

NCB's importance, then, should be read as inherited strategic weight rather than as a stand-alone current entity. Its historic position helps explain why the franchise retained significance in regional finance, why the merged institution commands close official attention, and why foreign stakeholders still encounter the NCB name in legal and commercial records.

Why the name still matters

The practical issue is straightforward. Older documentation, market commentary, and relationship histories often continue to use the NCB label long after the corporate structure has changed. For credit teams, sanctions specialists, export finance desks, and policymakers, that creates room for avoidable error if identity, ownership, and decision-making channels are assessed on the basis of a legacy name rather than the current institution.

Practical rule: when someone refers to National Commercial Bank Saudi today, they are usually referring to a legacy franchise whose present strategic relevance sits within SNB.

This has a second-order implication for sovereign risk analysis. A bank that carries the client relationships, market memory, and institutional standing of NCB, but now sits inside SNB, should be assessed through the lens of concentration and state linkage, not simple historical continuity. That is why comparisons with other major Saudi lenders can be useful. This overview of development finance and Banque Saudi Fransi shows how commercial banks in the Kingdom can also serve broader national policy objectives.

The central analytical shift is therefore about function. Historic scale still matters, but mainly because it has been folded into a larger vehicle that sits closer to the Kingdom's financial core. For international stakeholders, the key question is what the former NCB franchise now signals about sovereign linkage, market access, and the channels through which Saudi Arabia aligns banking capacity with economic transformation goals.

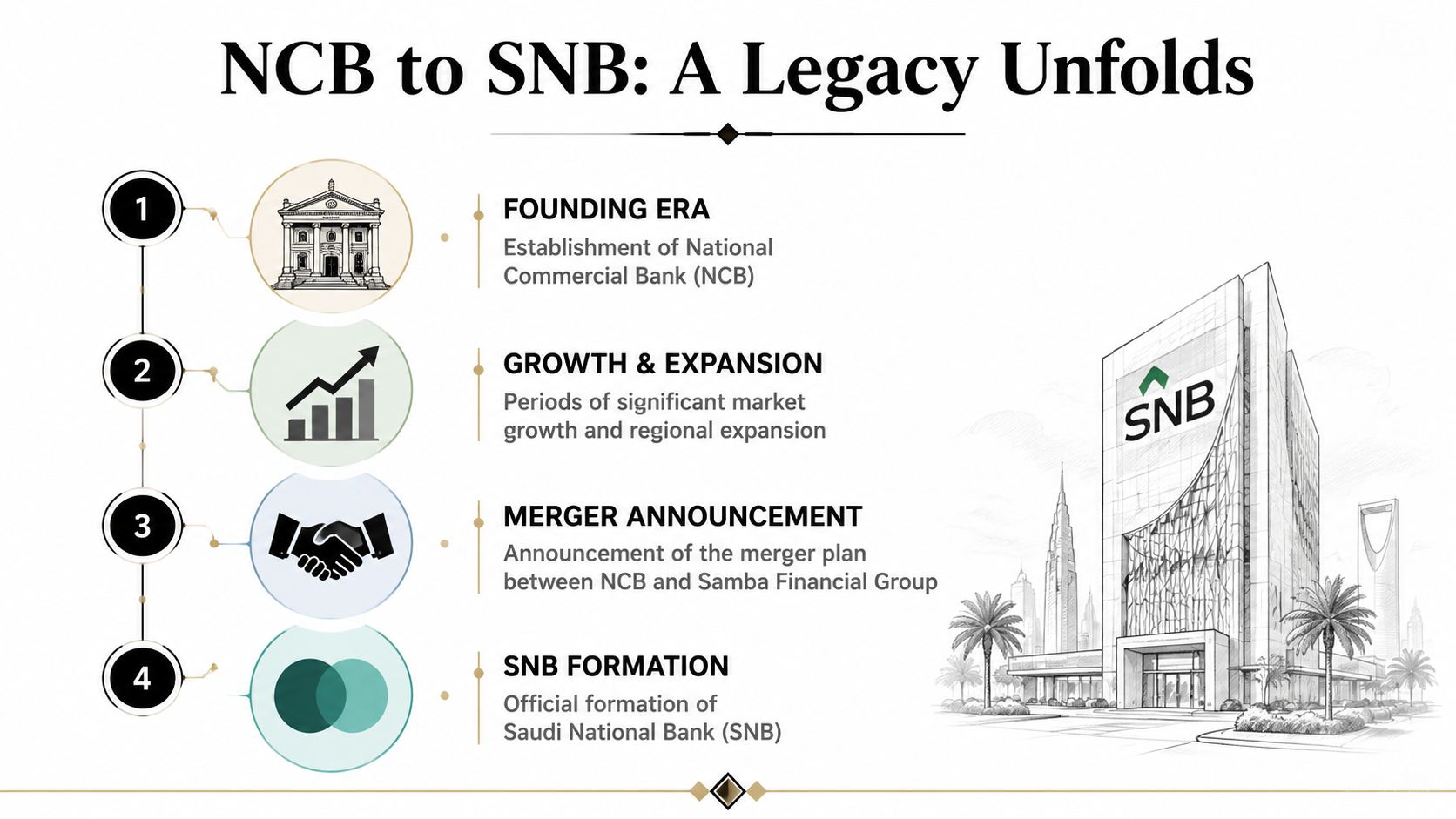

A Timeline From NCB's Founding to the SNB Merger

What does a bank's timeline tell international counterparties once the bank no longer exists under its original name? In NCB's case, the chronology matters because it shows how a long-standing domestic franchise was folded into a larger institution whose importance now lies in state linkage, financing capacity, and policy execution rather than legacy branding alone.

NCB was established in 1953, as noted earlier. That date matters less as a commemorative marker than as a signal of institutional depth. Early establishment in a bank-based financial system usually creates durable advantages in client acquisition, regulatory familiarity, and access to the country's main commercial networks. For UK investors and officials, that helps explain why references to "National Commercial Bank Saudi" still persist in market conversation even though the relevant counterparty today is SNB.

From early market position to systemic relevance

NCB's historical role was reinforced by its physical and organisational presence in Jeddah, the Kingdom's traditional commercial hub. Its headquarters, completed in 1983, stands 126 metres tall, rises 27 storeys, and has a 57,400 m² gross area, according to Skidmore, Owings & Merrill's project record. The point is not architectural prestige. A flagship headquarters of that scale reflected a period in which major Saudi banks concentrated decision-making, senior management, and client signalling in one dominant institution.

That legacy still matters. It helps explain why the former NCB franchise carried strategic weight well beyond ordinary retail banking and why its eventual combination with another major lender had implications for concentration, state alignment, and market structure across Middle East banking and capital market analysis.

The merger as a strategic event

The merger into SNB is the decisive milestone because it changed how external parties should assess the institution. The issue is not brand continuity. The issue is whether a larger balance sheet, broader client coverage, and closer sovereign linkage increase the bank's relevance to project finance, public investment priorities, and cross-border commercial engagement under Vision 2030.

For legal and transaction teams, merger analysis also depends on execution quality. A practical external reference such as this checklist for confident M&A closings is useful because integration risk often turns on governance, documentation, approvals, and post-closing control, not simply on strategic logic announced at signing.

Timeline highlights

- 1953: NCB was founded, establishing a franchise that became firmly embedded in Saudi commercial banking.

- 1983: The completion of the Jeddah headquarters marked the bank's maturity as a national financial institution with concentrated executive authority.

- Pre-merger era: NCB evolved into one of the Kingdom's most consequential banking franchises, with significance rooted in relationships and institutional standing as much as in scale.

- Merger into SNB: The legacy franchise was absorbed into a larger vehicle that international stakeholders should assess through sovereign linkage and systemic importance.

The practical conclusion is straightforward. The timeline matters because it explains the origin of the franchise, but the merger determines its present meaning. For G20 governments, export credit agencies, and institutional investors, "NCB" is now best understood as the historical foundation of SNB rather than as a separate contemporary counterparty.

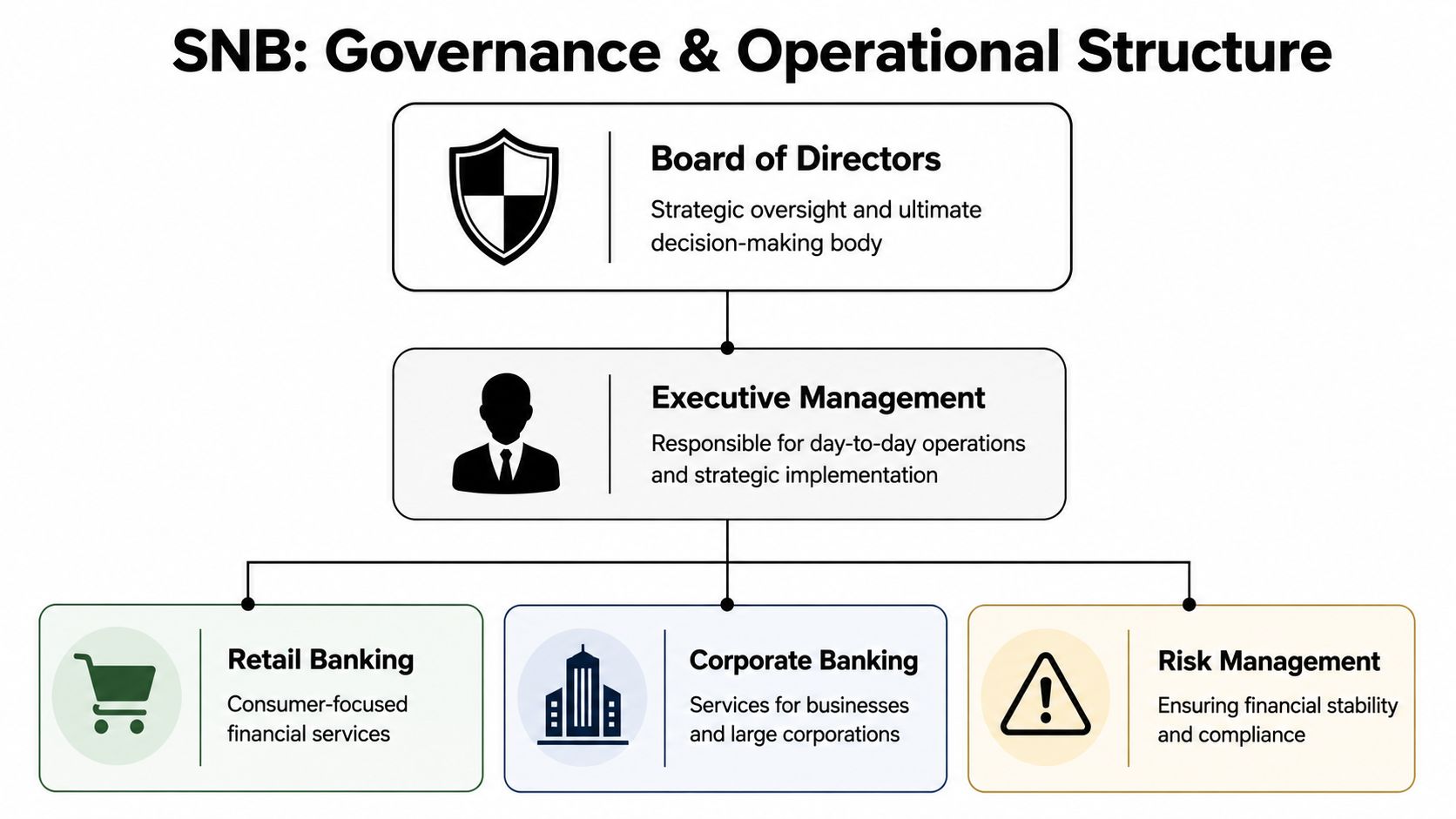

SNB's Post-Merger Governance and Operations

The most important operational fact about the post-merger institution is that it isn't a mono-line bank. The NCB prospectus filed with the Capital Market Authority described the bank as having share capital of SAR 20 billion divided into 2 billion ordinary shares, and operating through five principal segments: Retail Banking, Corporate Banking, Treasury, Capital Markets, and International. That segment mix is analytically significant because it signals a diversified universal bank.

Why segment diversification changes the risk profile

A bank with these operating lines behaves differently from a lender focused mainly on consumer deposits and domestic loans. Treasury and capital markets operations affect liquidity management and market sensitivity. International operations create additional compliance, jurisdictional, and funding considerations. Corporate banking ties the institution more closely to large domestic projects and state-linked commercial flows.

That means UK institutions should avoid analysing SNB through a purely retail-banking template. Its earnings drivers and risk transmission channels are broader.

| Operating segment | Strategic implication |

|---|---|

| Retail Banking | Anchors domestic customer relationships and deposit base |

| Corporate Banking | Connects the bank to large firms and project financing needs |

| Treasury | Shapes liquidity and interest-rate exposure |

| Capital Markets | Extends fee generation and market intermediation |

| International | Expands cross-border relevance and compliance complexity |

Governance should be read through function, not just form

Post-merger governance also needs to be read in a practical way. A bank with this structure must coordinate credit allocation, liquidity, capital markets activity, and international positioning within one institutional umbrella. That tends to strengthen strategic coherence, but it can also concentrate decision-making.

For public policy observers, that matters because large diversified banks often become transmission points between national policy priorities and private capital allocation. A universal bank can support retail demand, corporate activity, funding markets, and external financial relationships at the same time. That's a very different role from that of a simpler domestic lender.

A five-segment operating model tells you the institution can influence several parts of the economy simultaneously.

The implication for investors is straightforward. Governance assessment shouldn't stop at board structure or management biographies. It should focus on how effectively the bank balances universal-bank breadth with risk discipline, especially when strategic national priorities may place demands on multiple business lines at once.

Analysing SNB's Financials and Market Position

What changed for foreign counterparties when National Commercial Bank ceased to exist as a standalone name and became part of Saudi National Bank? The answer starts with inherited scale. A corporate profile published by The Worldfolio stated that National Commercial Bank reported revenue of US$ 9.8 billion, employed about 16,084 people, and had paid-up capital of SR 15,000 million, equivalent to US$ 4,000 million. Those figures matter because they show the merger combined already-systemic capacity with a new institutional wrapper, rather than rescuing a marginal lender.

Historical disclosures, as noted earlier, point in the same direction. Before the merger, NCB already had the balance-sheet depth, deposit base, and earnings profile of a bank embedded in the Kingdom's core financial system. For analysts, that is the relevant starting point. SNB should be read as a consolidation of strategic banking capacity inside Saudi Arabia, not solely as a rebranding exercise.

That distinction has practical consequences. A bank formed from a large incumbent franchise generally enters the post-merger period with stronger client entrenchment, broader distribution, and greater policy relevance than a newly assembled institution without that legacy. For UK banks, exporters, and asset managers, the current name may be SNB, but part of the counterparty assessment still rests on understanding the NCB franchise that sits underneath it.

Reading market position through function

Market position is not only a question of asset size. It also concerns where a bank sits in domestic capital allocation, payments, household deposits, and corporate financing relationships. In Saudi Arabia, that placement carries strategic weight because the banking system is one of the main channels through which state priorities, private investment, and large-scale development financing intersect.

This is why the merger matters for external stakeholders. The combination strengthened an institution that was already central to domestic intermediation. That increases its relevance in areas such as syndicated lending, trade finance, capital markets access, and institutional partnerships linked to Vision 2030 execution.

For international readers trying to place one bank within the wider regional setting, this overview of Middle East banking and investment trends gives useful context.

What investors should infer

The main inference is straightforward. SNB's market standing did not begin with the merger. The merger concentrated existing strength and made the bank harder to analyse through conventional commercial metrics alone, because franchise value, sovereign linkage, and national development strategy now interact more closely inside one institution.

That makes a difference to three groups:

- Counterparty risk teams: They should assess franchise durability alongside capital and liquidity indicators, because domestic policy relevance can affect market confidence and external support assumptions.

- UK corporate treasurers: They should treat SNB as a gateway institution in Saudi finance, especially where local relationships, project exposure, and settlement capacity matter.

- Portfolio investors: They need to separate headline merger narratives from the slower-moving drivers of valuation, including concentration, state alignment, and earnings resilience. A concise decision framework for traders can help structure that judgement.

The broader point is easy to miss. Confusion over the old NCB name versus the current SNB identity is not a branding issue alone. It affects how overseas stakeholders map institutional continuity, assess strategic significance, and judge whether they are dealing with a standard large bank or with a financial actor that sits close to the centre of Saudi economic policy.

Geopolitical Considerations and Regulatory Oversight

A common mistake is to analyse a bank like SNB as though it were insulated from the sovereign environment that surrounds it. It isn't. The most important external fact for risk professionals is that the bank's credit profile can move with the Saudi state, not only with its own internal performance.

The clearest evidence comes from S&P Global's report on National Commercial Bank, which stated that NCB was downgraded after the Saudi sovereign downgrade. That is a concrete illustration of the sovereign-bank nexus. The institution's standing wasn't assessed only on standalone operating fundamentals. It was also shaped by the state's own credit trajectory.

Why this matters for UK firms

For UK corporates and financial institutions, that linkage changes how counterparty risk should be framed. The question isn't merely whether the bank is well managed or commercially diversified. The question is how sovereign conditions can affect pricing, confidence, and compliance treatment in cross-border business.

This matters especially in areas such as:

- Trade finance: Sovereign-linked rating pressure can affect how banks are viewed in international transaction chains.

- Correspondent banking: External institutions may adjust risk appetite when sovereign conditions change.

- Corporate treasury decisions: Firms may need to reassess concentration risk when one banking relationship is closely tied to state-linked dynamics.

Regulatory oversight and strategic interpretation

Saudi regulatory architecture still matters, but for external observers the bigger issue is interpretation. A large bank operating in a sovereign-linked system may look stable precisely because of its national importance. Yet that same closeness can transmit state-level pressure into the bank's own risk profile.

Don't treat sovereign support and sovereign sensitivity as opposites. In many systems, they arrive together.

That creates a more nuanced view of stability. A bank may be strategically protected because it matters to the national system. But it may also be strategically exposed because it cannot be fully decoupled from the sovereign's own rating and policy environment.

A better framework for policy audiences

For UK policymakers, the correct frame is not “is SNB safe or risky?” That is too blunt. The better frame is:

- How tightly is the bank linked to sovereign credit conditions?

- How does that linkage affect cross-border commercial reliability?

- What additional compliance or pricing burden might arise when sovereign conditions shift?

That is the practical meaning of the sovereign-bank nexus. It turns a bank from a purely commercial counterparty into a partial proxy for the state environment in which it operates.

SNB as an Instrument of Vision 2030 and Sustainability

The post-merger institution should also be understood as part of Saudi Arabia's national development machinery. The available material on SNB indicates that the merger with Samba Financial Group was presented as part of supporting Vision 2030, as noted in the earlier cited background on the Saudi National Bank. That point is easy to repeat and easy to underanalyse. The more interesting observation is what it implies.

A bank with universal operating segments, strong legacy scale, and deep domestic relevance can do more than finance ordinary commercial activity. It can help channel capital into sectors that the state wants to prioritise, whether through corporate banking, capital markets capability, treasury support, or international linkages.

Why Vision 2030 changes the meaning of bank scale

Under a narrow commercial interpretation, scale means market share and earnings capacity. Under a national strategy interpretation, scale means execution capability. It means the bank can intermediate between public ambition and private financing needs.

That is why the old NCB story and the current SNB story shouldn't be separated too sharply. The legacy franchise supplied trust, client depth, and market infrastructure. The merged institution can use that base in support of a broader policy agenda.

A related point for resilience analysis is that large banks become especially important when governments pursue economic diversification. They often act as filters. They decide which projects get priority, which sectors receive sustained financial attention, and which counterparties gain access to a more strategic banking relationship. Readers thinking about this from a systems perspective may find the broader argument in this reflection on resilient banks and anti-fragile systems particularly relevant.

Sustainability should be read as strategic signalling

Without introducing unsupported metrics, it is still possible to make a grounded point about sustainability. For a bank of this scale and strategic importance, sustainability language is not merely reputational. It can signal where the Kingdom wants international capital, policy legitimacy, and long-term sector development to converge.

When a nationally significant bank adopts a sustainability narrative, external investors should ask what policy priorities that narrative is meant to support.

For G20 audiences, that means SNB is worth watching not just as a lender, but as an indicator. Its positioning can offer clues about how Saudi Arabia wants to present the next phase of economic modernisation to international partners.

Key Takeaways and Avenues for Engagement

The central conclusion is simple. National Commercial Bank Saudi is no longer best analysed as a standalone institution. It should be read as the legacy core of a larger post-merger bank whose strategic relevance now extends well beyond traditional commercial banking.

For policymakers, the first avenue of engagement is monitoring. Follow the institution not only through banking metrics but through its role in sovereign strategy, domestic project finance, and cross-border commercial relevance. In practical terms, SNB can serve as a barometer of how Saudi Arabia is aligning finance with national objectives.

For investors, the second avenue is analytical discipline. Don't rely on legacy brand familiarity. Focus instead on three variables:

- Institutional identity: Is the exposure really to a legacy NCB reference, or to the current SNB structure?

- Business model complexity: The five-segment model means the bank's opportunities and vulnerabilities are spread across several operating lines.

- Sovereign linkage: Credit interpretation should account for state-related sensitivity, not just standalone banking fundamentals.

For corporates, the third avenue is operational caution. Large Saudi banking relationships can offer reach and strategic access, but they should be assessed with legal, credit, and compliance teams working from the same entity map. That reduces the risk of using outdated assumptions in contracts, treasury arrangements, or counterparty onboarding.

The broader policy lesson is that Saudi banking consolidation is not just a domestic financial story. It has implications for international engagement, market concentration, and how state ambition is financed. Analysts who continue to treat the old NCB label as the full story will miss the more important point. The institution's significance today lies in what it has become, not only in what it once was.

If you want more analysis like this on sovereign risk, strategic banking, and the intersection of finance and geopolitics, follow Global Governance Media for ongoing briefings and policy-focused insight.