By Eleanor Whitmore

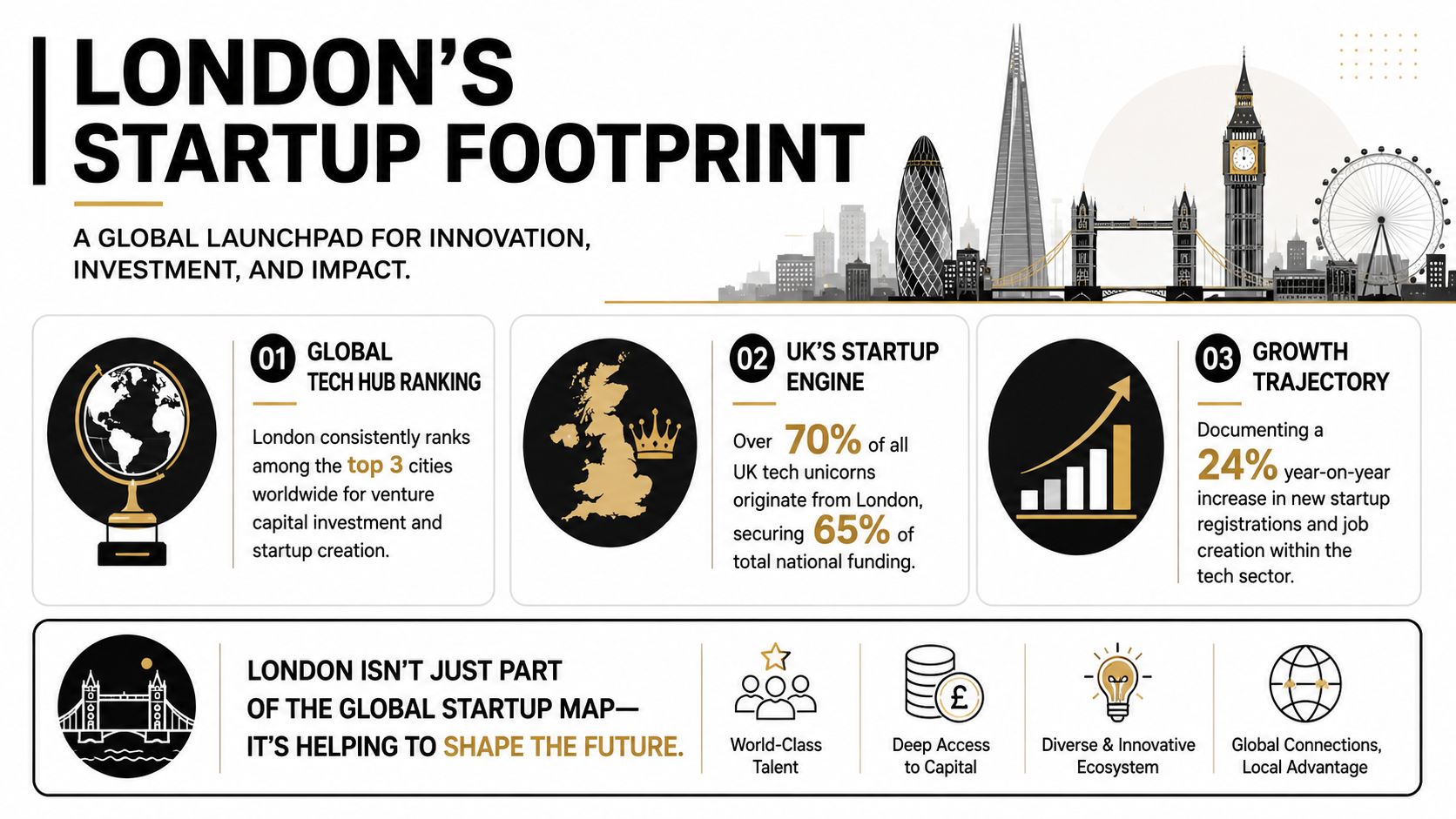

Around 58% of UK equity investment went to London-based companies in 2024. That single figure, cited in a Cambridge-backed briefing, is the clearest starting point for understanding a startup in London. The core issue is not branding or founder mythology. It is the degree to which capital, networks, specialist services, and policy attention are concentrated in one city.

This concentration gives the UK a real strategic advantage. London has the density of investors, legal expertise, global customers, and international talent needed to produce firms that can compete with peers in Silicon Valley and New York. Yet the same concentration creates a distribution problem for national policymakers. If one metropolitan hub captures a disproportionate share of risk capital and high-growth firms, other cities face slower ecosystem formation, thinner investor networks, and weaker access to the support systems that help startups scale.

That tension matters beyond the UK.

For G7 and G20 governments, London is a useful policy case. Advanced economies want globally competitive innovation centres, but they also need regional legitimacy, wider access to finance, and a growth model that is not confined to one dominant city. London shows that startup success and territorial imbalance can develop at the same time.

The policy question, then, is not whether London should remain strong. It should. The harder question is how to preserve London's global position while building a national startup strategy that spreads capital formation, talent development, and scale-up capacity more evenly across the UK.

Table of Contents

- Defining the London Startup Ecosystem

- Core Sectors Fueling London's Tech Economy

- Analyzing London's Concentrated Funding Landscape

- The Interplay of Talent Immigration and Regulation

- Public Sector Support and Global Connectivity

- A Policy Blueprint for UK-Wide Startup Growth

Defining the London Startup Ecosystem

In 2021, London recorded 83.4 business startups per 10,000 people, the highest rate among UK cities. Statista also indicates that London remained the leading UK city for startup formation in 2023 (Statista on UK city startup rates).

Startup density is a stronger policy signal than raw city size alone because it shows where entrepreneurial activity is being reproduced at unusual intensity. A large capital can dominate business counts by having more residents and more firms. London's rate points to something more durable. Founders are choosing to start companies there at a pace that reflects concentrated advantages in finance, skills, customers, and business services.

Why London matters nationally

London's startup ecosystem is best understood as a dense coordination system, not just a large urban economy. High firm formation in one place reduces search costs for founders, early employees, investors, and specialist advisers. It also raises the likelihood that knowledge, capital, and experienced operators circulate repeatedly within the same local network.

That has national consequences.

A founder building in London is more likely to encounter investors familiar with venture risk, lawyers who understand equity structures, and commercial partners able to test new products quickly. Those advantages compound over time. They help explain why the capital functions as the UK's main node for startup creation, company scaling, and international market entry.

Practical rule: When one city combines high startup formation with dense support networks, policymakers should treat it as national economic infrastructure.

A global hub with domestic consequences

London also operates as the UK's main gateway into global startup networks, as noted earlier in the article. Its role is not only symbolic. It connects the UK to internationally mobile founders, cross-border capital, and customers in sectors where speed, regulation, and market access shape outcomes early.

For national policymakers, that creates a dual obligation. They need to preserve London's competitiveness against other global hubs while limiting the degree to which one metro area captures a disproportionate share of entrepreneurial opportunity. The issue is not whether London is too successful. The issue is whether the UK has built institutions that can spread some of the benefits of that success beyond the capital.

| Policy lens | What London represents |

|---|---|

| National lens | The UK's dominant centre for startup formation, financing, and commercial intermediation |

| Global lens | The country's primary entry point into contested international technology markets |

| Regional lens | A concentration point that can widen geographic inequality if policy remains London-centric |

The policy challenge, then, is management of concentration rather than correction of success. If government treats London's scale as proof that the system is working, regional gaps are likely to widen. If it treats London's dominance only as a political problem, the UK risks weakening its strongest globally competitive ecosystem. A credible national strategy has to do both at once. Protect the capital's international function, and build transmission mechanisms that shift talent, capital, and commercialization capacity into other UK city-regions.

Core Sectors Fueling London's Tech Economy

A small number of sectors account for a large share of London's startup momentum. That concentration is an advantage in global competition, but it also shapes where public support, private capital, and high-skilled labour flow inside the UK.

Software and data as the base layer

London's strongest startup sectors sit on top of a shared capability base. Software engineering, applied data work, cloud infrastructure, product management, and enterprise sales all travel across multiple verticals. As noted earlier, London ranks highly in software and data by international comparison. The policy implication is straightforward. Foundational digital capabilities create spillovers across fintech, AI applications, cybersecurity, enterprise software, regtech, and data-heavy business services.

That cross-sector reuse helps explain why London produces depth rather than simple breadth. A city with dense pools of engineers, specialist lawyers, growth marketers, and venture investors can support many firms building different products from a similar operating model. For industrial policy, this is a significant point. Governments often back sectors one by one, but London's experience suggests that horizontal capabilities can produce stronger returns than narrow vertical targeting alone.

Why fintech and AI fit London's structure

The strongest sectoral fit appears where three conditions are present at once. Companies need repeated access to risk capital. They operate under meaningful regulatory scrutiny. They sell into international or multi-jurisdictional markets early in their growth cycle.

That combination favours fintech and AI in particular. Fintech firms benefit from proximity to banks, payment networks, insurers, regulators, compliance talent, and specialist advisers. AI startups benefit from access to advanced technical labour, cloud credits, enterprise buyers, and investors comfortable with long product-development cycles and uncertain commercial timing. In both cases, London offers coordination advantages that are hard for smaller UK ecosystems to replicate quickly.

This also helps explain why some sectors are less naturally suited to the capital. Startups that depend on industrial land, pilot manufacturing, or lower operating costs may gain less from London's density and more from regional ecosystems built around production capacity, university research, or sector-specific supply chains.

A practical way to frame the issue is through market fit and policy fit.

| Sector type | London advantage | Limits of the London model |

|---|---|---|

| Fintech and AI | Dense investor networks, specialist regulatory expertise, global business links | Growth can become too dependent on a narrow set of funders and service providers |

| Software platforms | Large hiring pool, enterprise customers, strong professional services base | High wages and office costs can slow early-stage experimentation |

| Science-based spinouts | Better access to later-stage investors and commercial partners | Scaling often still depends on lab space, prototyping capacity, and research ecosystems outside London |

For capital-market design, the broader lesson is that sector success follows institutional depth as much as founder quality. The UK's wider capital markets development agenda should therefore distinguish between sectors that need metropolitan financial density and sectors that need place-based industrial capacity.

Founders making sector-specific fundraising choices can also use market maps such as Find top UK investors for your startup to assess where investor expertise is concentrated.

The national policy conclusion is not that every region should imitate London. It is that the UK should assign functions more deliberately. London should remain the country's main platform for sectors that depend on global finance, regulatory intermediation, and international client access. Other city-regions need targeted support in sectors where their cost base, research assets, or industrial capabilities provide a stronger comparative position.

Analyzing London's Concentrated Funding Landscape

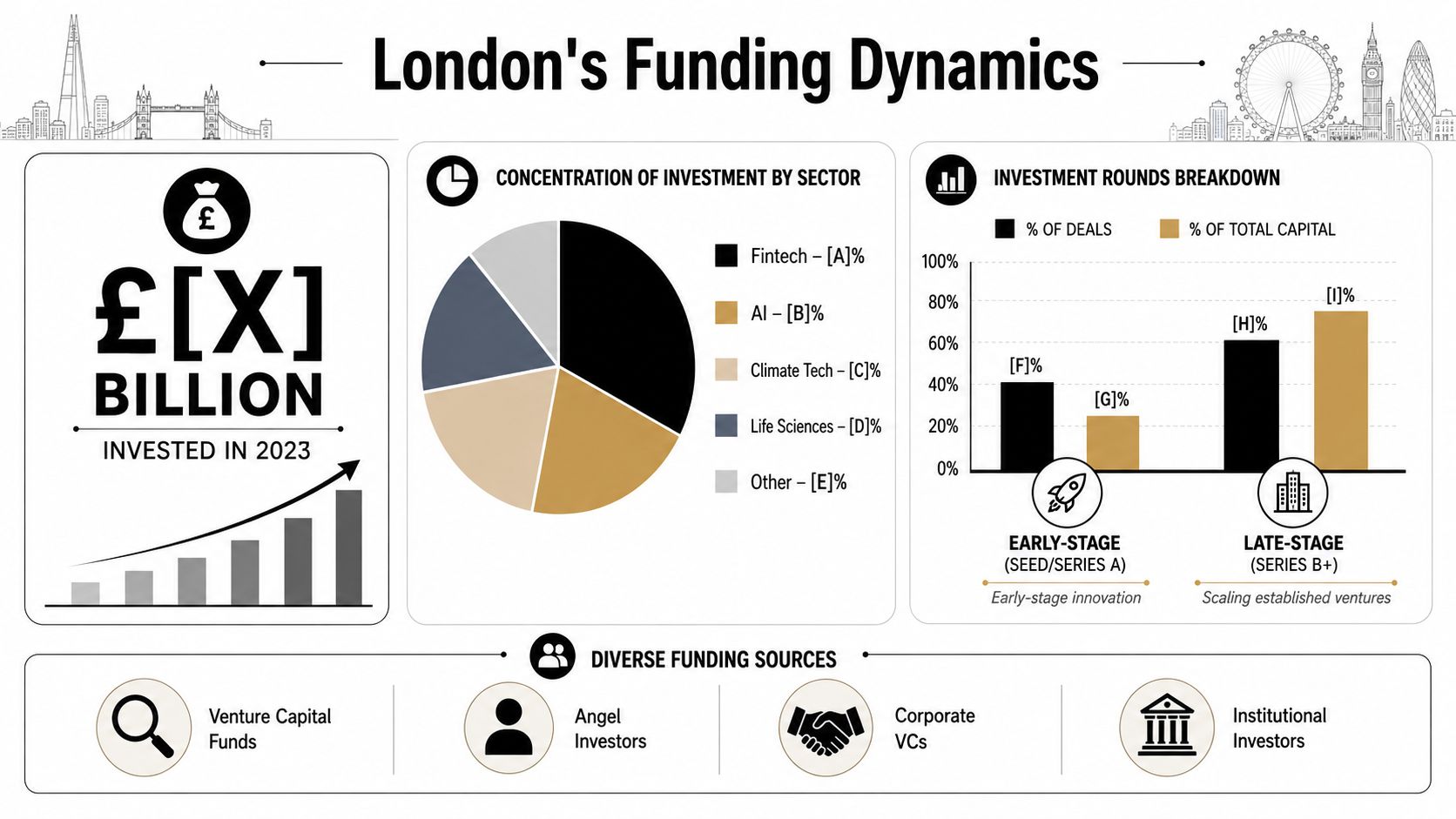

In 2023, London-based startups took $13.5 billion in venture funding, equal to 65% of all UK VC investment that year. That is not just a sign of scale. It shows how strongly British risk capital remains tied to one city.

Capital strength and capital concentration

London offers founders the UK's deepest pool of venture investors, advisers, later-stage financiers, and corporate buyers. That density lowers search costs and shortens the distance between a first meeting and a term sheet. It also changes company behaviour early. Firms often choose where to incorporate, hire, and spend management time based on where follow-on capital is easiest to secure.

As noted earlier, other evidence points in the same direction. London accounts for a disproportionately large share of UK equity investment and venture-backed firms. The policy issue is therefore broader than annual deal totals. Capital concentration influences the geography of company formation itself.

For founders trying to understand that investor map in practical terms, curated tools such as Find top UK investors for your startup can be useful because they show how heavily investor discovery still centres on the capital.

A wider view of UK capital markets development and institutional financing capacity also matters here. Startup location often follows the structure of national financial systems, including where specialist investors sit, how quickly capital can be recycled, and which regions have enough institutional depth to support repeat company building.

The concentration pattern also persists as firms mature. Recent industry analysis has argued that London continues to capture an outsized share of larger early-stage rounds, which means the gap is not confined to seed formation. It extends into the stages where firms hire at scale, expand internationally, and become visible to major acquirers.

Why this matters for national policy

A concentrated funding market can still produce globally competitive firms. The harder question is whether it also weakens national economic breadth.

Three effects deserve closer attention.

- Regional capital shortages become self-reinforcing. Places with fewer active investors also have fewer repeated interactions between founders, angels, lawyers, and later-stage funds. That reduces local pattern recognition and makes each funding round harder to syndicate.

- Growth policy becomes overly London-centric. Public programmes can drift toward helping already fundable companies move faster, rather than expanding the investable pipeline in regions with strong universities, industrial assets, or lower operating costs.

- Economic geography starts to reflect investor convenience rather than national comparative advantage. Firms may cluster in London even when their research base, workforce model, or production needs would be better served elsewhere in the UK.

This creates a strategic dilemma for government. London's scale is a national asset in international competition for capital. Yet if policymakers treat concentration as an efficient end state, they risk underbuilding the regional financing systems needed for broader productivity growth.

The practical conclusion is disciplined rather than anti-London. The UK should keep London globally competitive while using targeted policy to widen access to early-stage and scale-up finance elsewhere. That means stronger regional funds, better pathways from local angel capital to institutional follow-on rounds, and clearer alignment between national innovation policy and the places where sector-specific strengths already exist.

The Interplay of Talent Immigration and Regulation

Capital alone doesn't explain why a startup in London can scale quickly. The city also benefits from a layered labour market. It draws from domestic graduates, experienced operators, and internationally mobile professionals who are willing to relocate for ambitious firms.

That advantage, however, isn't evenly distributed across founders. Startup Genome notes that London's ecosystem provides a stronger advantage to founders whose startups can benefit from dense investor networks and attract internationally mobile talent. It also notes that policy discussion is shifting towards sector-specific support and stronger spinout programmes outside London (Startup Genome on London's ecosystem dynamics).

Who benefits most from the London model

This is one of the most important distinctions in the current debate. London's talent model particularly favours firms that can recruit globally, pay competitively, and turn network proximity into speed. Venture-backed software, fintech, and AI firms often match that profile.

Other founders don't necessarily benefit in the same way. Teams building in less network-dense sectors, or operating with constrained early-stage budgets, may face London's costs more directly than its advantages. The same applies to firms whose commercialisation path depends less on investor access and more on specialised facilities, local supply chains, or research translation outside the capital.

A practical labour-market lens can help founders and policymakers assess those trade-offs. Resources such as this 2026 UK salary guide are useful not because they resolve the talent question, but because they show how compensation expectations shape location decisions across sectors and stages.

Talent policy can't be separated from ecosystem design

Migration and startup policy are often treated as separate files inside government. That is a mistake. If policymakers want high-growth firms in globally contested sectors, they need immigration systems that recognise how startups hire. Small firms don't recruit on the same timelines or with the same administrative capacity as large corporates.

At the same time, talent policy has to be linked to national distributional goals. A country cannot rely entirely on one city to absorb global talent while expecting other regions to build comparable innovation ecosystems from domestic pipelines alone. The policy challenge is to make mobility work for the whole national system.

That requires a broader framework for a path for migration to work for all, especially if governments want to reconcile economic openness with regional legitimacy.

A more balanced approach would combine three ideas:

- Keep London open to global talent in sectors where international competition is intense.

- Build regional specialist pipelines tied to universities, spinouts, and sector clusters.

- Reduce frictions for firm growth outside London so talent mobility doesn't automatically become talent concentration.

The policy objective isn't to move talent away from London. It is to stop London being the only place where top talent can easily meet capital, customers, and commercial support.

Public Sector Support and Global Connectivity

London's startup ecosystem is not purely market-made. Public institutions, university links, local programmes, and trade-facing infrastructure all contribute to its resilience. The policy lesson is that ecosystems don't emerge from capital alone. They are organised through support stacks that reduce friction for founders.

The support stack around founders

At a practical level, startup support usually works through a layered model rather than a single flagship scheme.

- National innovation bodies help de-risk research, commercialisation, and technical development.

- Accelerators and incubators give early teams access to mentors, investors, and structured programme support.

- City-level networks connect founders with legal, financial, and operational expertise.

- Universities and research institutions feed talent, intellectual property, and spinout potential into the market.

A government looking to strengthen entrepreneurship should think in systems rather than grants. The most effective interventions often connect finance, advisory capacity, and institutional credibility in one pipeline. That is one reason entrepreneurship policy works best when linked to a wider agenda for facilitating entrepreneurship.

Why global connectivity amplifies local policy

London's support system is amplified by geography and connectivity. The city operates as an international meeting point for investors, multinational firms, founders, and service providers. English as a business language, London's time-zone position, and its role in global finance all make it easier for startups there to build across markets rather than only within one.

Public support has a higher return when founders can rapidly connect domestic assistance to foreign demand. A startup that receives local support in a globally connected city can often use that support to win international customers, raise cross-border capital, or recruit specialised expertise faster than a similar firm in a less connected location.

A useful way to think about London is as a multiplier. Domestic policy inputs are often worth more there because they are plugged into international networks. That is one reason national governments keep backing globally connected capitals even when regional imbalances are politically costly.

Public support is most powerful when it doesn't stop at firm creation. It should help firms move from local capability to international market access.

The challenge for the UK is to reproduce parts of that multiplier effect outside London. Not every region can become another London, nor should it try. But more regions can build stronger links between research, infrastructure, export support, and founder finance.

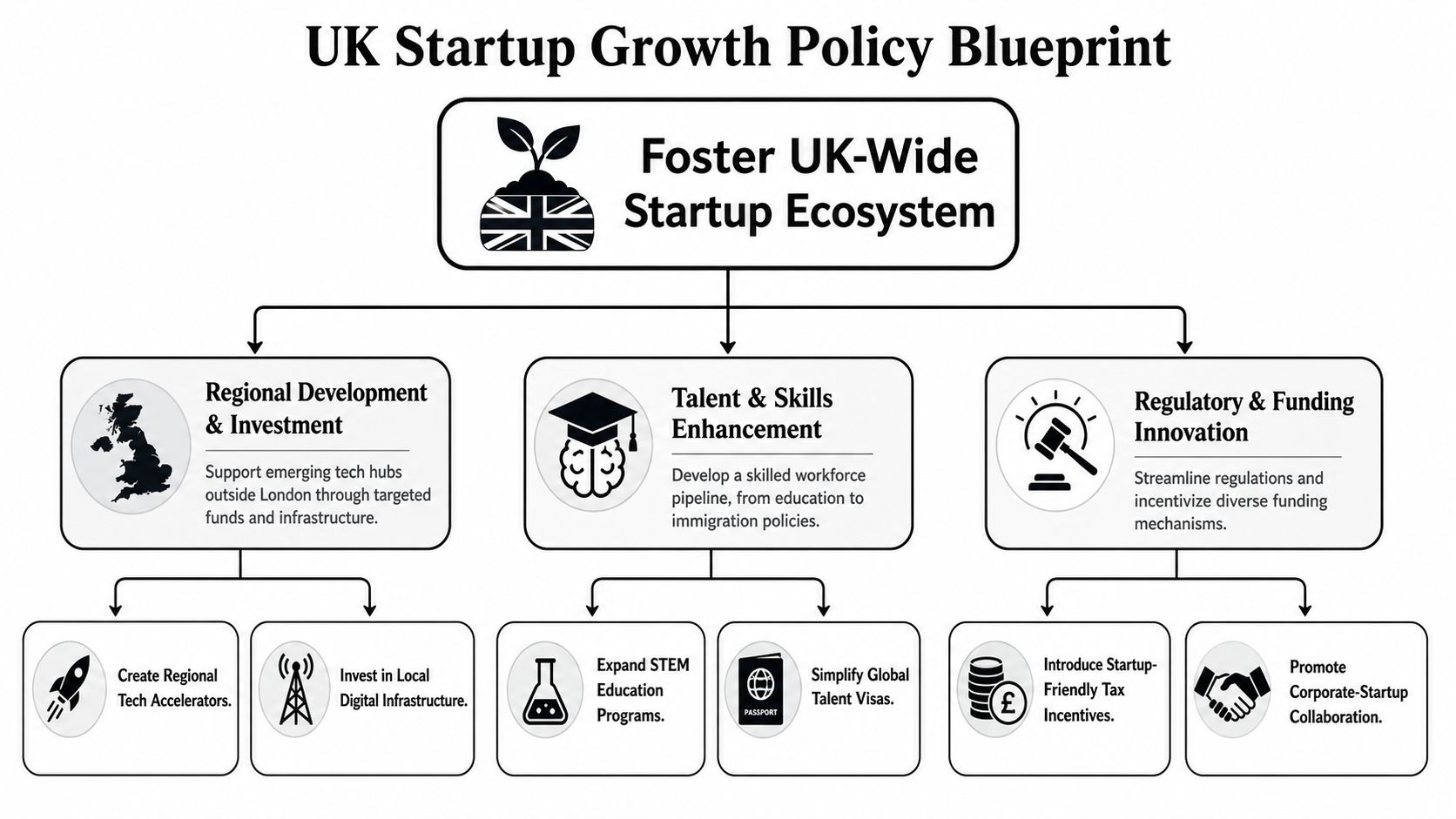

A Policy Blueprint for UK-Wide Startup Growth

Nearly half of UK startups that have raised more than £100,000 are based in London, and, as noted earlier, the concentration is even sharper among firms founded in 2023 and 2024. That pattern is no longer best described as a cyclical market outcome. It is a policy problem about where risk capital, high-growth firms, and commercial opportunity are allowed to accumulate.

A credible national response starts from two facts. London remains one of the few UK assets with clear global scale in venture-backed technology. The rest of the country cannot rely on passive spillovers from the capital to build investable companies at sufficient pace.

What national government should do next

National government should treat London as a strategic asset while correcting the financing and institutional gaps that keep other regions from converting research and industrial capability into scalable firms. Those goals are compatible. In fact, they depend on one another. An economy that relies too heavily on one city becomes more exposed to sector shocks, asset-price cycles, and political backlash against uneven growth.

The first task is to preserve London's international competitiveness in software, fintech, AI, and data-intensive services. That means regulatory predictability, access to global talent, and capital-market reforms that improve the path from startup formation to scale-up financing. Weakening the capital would not produce stronger regional hubs. It would more likely reduce the UK's overall attractiveness relative to New York, Paris, Berlin, Singapore, and Toronto.

The second task is more neglected. Government should build regional capital pathways rather than assume that early-stage support will translate into follow-on finance. In much of the UK, the drop-off happens after grant funding, incubator support, or university spinout formation. Firms can start locally, but many still need London-based investors, customers, or advisers to grow. That creates a structural pull toward relocation, even where the underlying company could scale elsewhere.

The third task is to align policy with sector fit. Regional growth strategies work best when they are tied to assets that already exist: research strengths, specialised labour pools, anchor firms, public procurement demand, or industrial infrastructure. A generic startup strategy spreads funds thinly and often rewards branding over execution.

A practical national package would include:

- Targeted regional funds tied to sectors where local comparative advantages are already visible.

- Stronger spinout conversion systems so universities outside London produce more investment-ready companies.

- Co-investment vehicles that bring in private capital without making a move to London the default next step.

- Procurement reforms that give startups outside the capital a clearer route to first customers in health, energy, defence, and digital public services.

- Geographic performance metrics so HM Treasury and relevant departments assess where public innovation spending produces firms, jobs, and later-stage investment.

What regional and multilateral actors should do

Regional agencies should stop copying London's full-stack model. London benefits from agglomeration, global finance, and institutional density that took decades to build. Regional strategies need sharper choices and clearer economic logic.

One area may have a credible advantage in applied research commercialisation. Another may be better placed to support advanced manufacturing software, energy systems, or health technologies linked to local hospital and university networks. The policy test is not whether every city can replicate London's breadth. It is whether each region can reach enough depth in selected sectors to attract repeat capital and specialised talent.

This matters beyond the UK. Across the G7 and G20, innovation-led growth is concentrating in a small number of metropolitan centres. The policy dilemma is not solely redistribution versus efficiency. It is how to preserve the productivity benefits of clustering while preventing national innovation systems from becoming too narrow geographically and politically fragile.

That agenda has four practical implications:

| Stakeholder | Recommended action |

|---|---|

| National treasuries | Assess startup tax incentives and public investment programmes by geographic distribution as well as aggregate growth |

| Regional agencies | Concentrate resources on sector-specific capabilities instead of generic founder promotion |

| Innovation and industry ministries | Link research funding to commercialisation institutions outside capital cities |

| G7 and G20 forums | Compare policy tools for balancing globally competitive hubs with broader territorial growth |

A disciplined blueprint for the UK follows five principles.

- Protect the engine. London should remain the UK's principal global startup centre because international competition for capital and talent is intensifying.

- Broaden access to finance. Viable firms outside London need earlier access to angel, seed, and growth capital without relocation becoming a condition for scale.

- Back place-based specialisation. National policy should support distinct regional strengths rather than impose a uniform model.

- Connect migration policy to national capacity. Talent systems should serve the whole innovation economy, not only the capital's labour market.

- Measure concentration openly. Government should publish regular data on where startup finance, spinout activity, procurement wins, and scale-up formation are occurring.

The central policy error has been to assume that London's success would diffuse widely without institutional design. It has not. Concentration can produce spillovers, but spillovers do not replace region-specific finance, commercialisation support, and customer access.

For a G7 or G20 audience, the broader lesson is clear. London demonstrates what a world-class startup centre can achieve. It also shows the limits of a national model built around one dominant city. The next phase of UK startup policy should accept concentrated growth as an economic reality, then respond to it with equally deliberate national coordination.

Global Governance Media brings policy leaders, analysts and institutions into the same conversation on the economic, technological and governance choices shaping the G7 and G20 agenda. If you want more evidence-led analysis on innovation policy, regional growth, capital markets and international cooperation, explore Global Governance Media.